urfinguss/iStock via Getty Images

Housing markets seem to be in a very interesting position. On one hand, it’s well known that there is a national housing shortage in the US. On the other hand, it’s also true that inflationary pressures and rising interest rates are damaging to the demand for housing. In the long run, the shortage will win out. But that doesn’t change the fact that, in the near term, we could still see some additional pain in the space. Despite the prospect of pain, one company that seems to be holding up pretty well in this current environment is Cavco Industries (NASDAQ:CVCO), an enterprise that generates revenue by producing and selling factory-built homes to customers that are often lower income than those who would buy more traditional homes.

Due in part to an acquisition, but also because of strong pricing power and strong demand, revenue has been rising significantly and profits have followed suit. If this trend continues, shares could experience a tremendous amount of upside. But with the prospect of the housing market weakening, there is some risk of financial performance reverting back to what it was in prior years. I truly have a hard time believing that the firm would experience a significant amount of downside should the market deteriorate further, but it’s also likely the case that upside is limited until current economic considerations clear up.

Great performance so far

The last time I wrote an article about Cavco Industries was back in June of this year. In that article, I talked about how the company had been hit hard by the general market downturn in the months leading up to the release of the article. I also warned that if financial performance were to revert back to the levels that we experienced during the company’s 2021 fiscal year, there could be some pain for investors. But any scenario shy of that would likely result in shares trading at attractive enough levels to offer either some upside or limited downside if things don’t go well. Since the publication of that article where I rated the company a ‘buy’, it has outperformed the broader market nicely, generating a return for investors of 8.8%. That compares to the 2.3% increase seen by the S&P 500 over the same time frame.

Author – SEC EDGAR Data

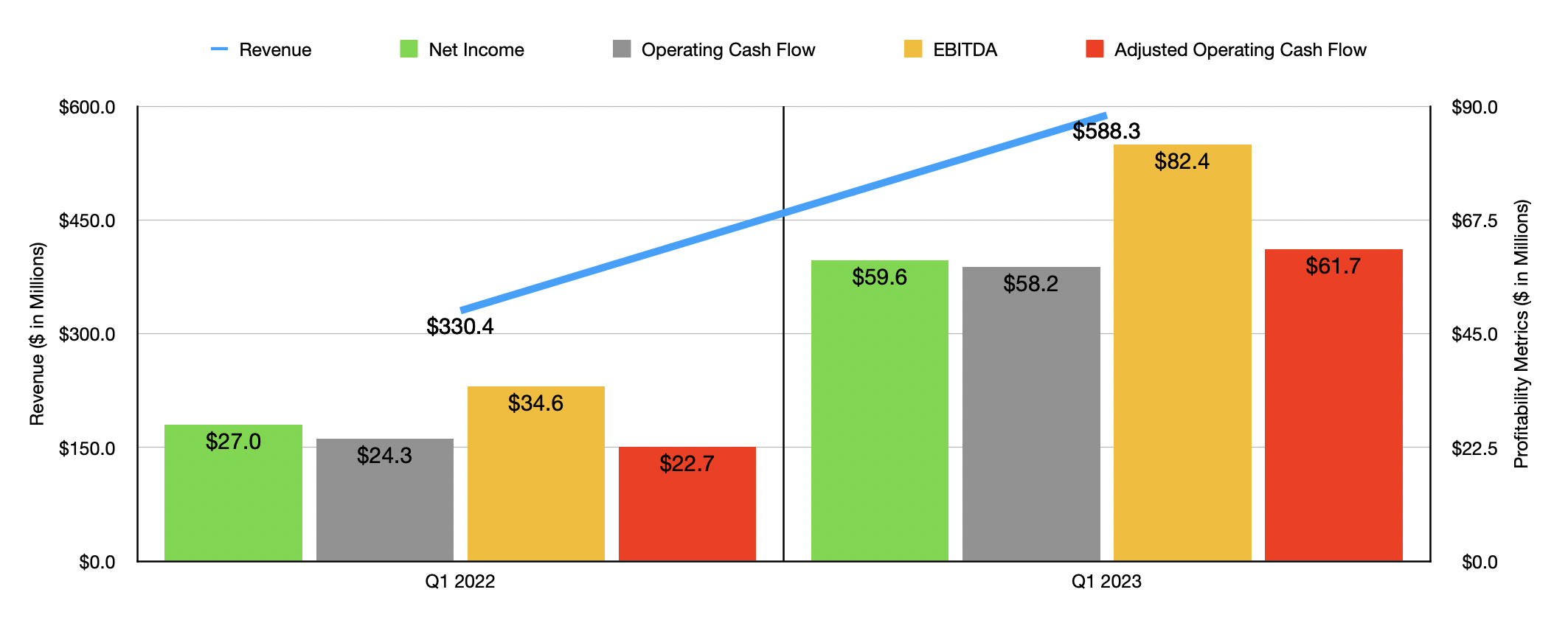

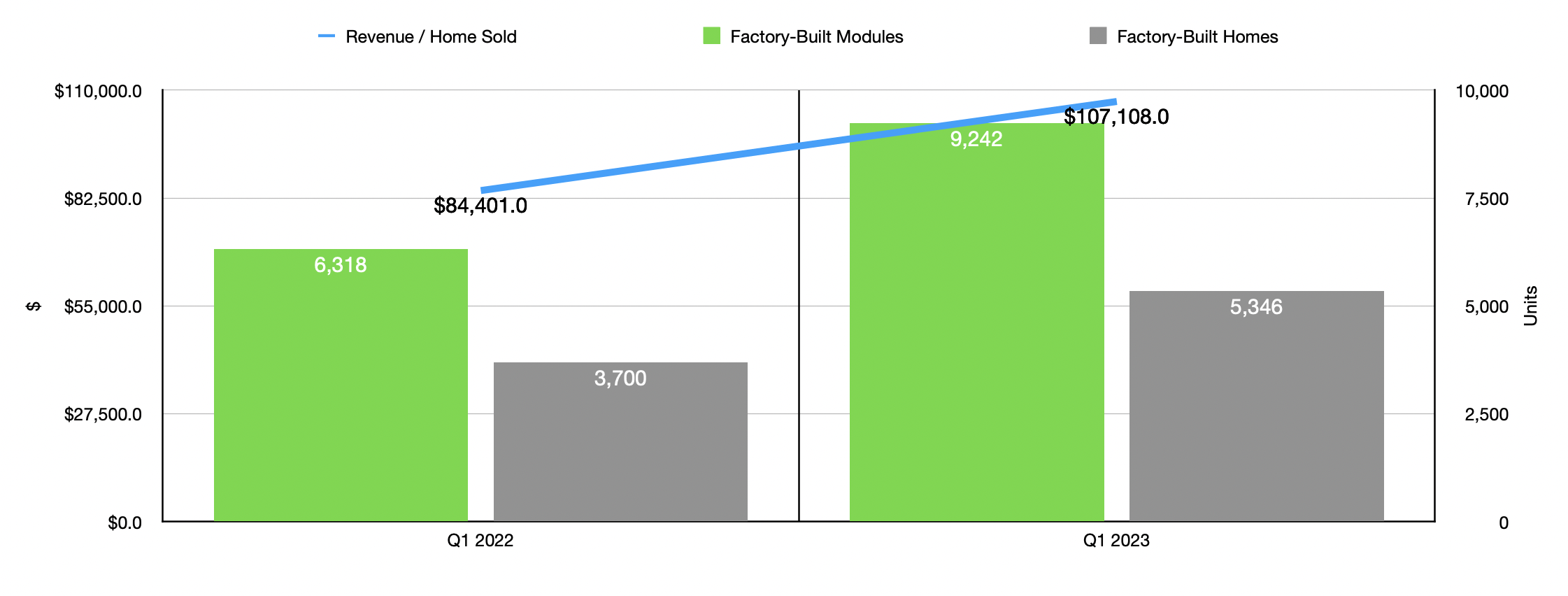

This return disparity was not without cause. In fact, I’m a little surprised that shares haven’t risen even more significantly. When I last wrote about the company, we only had data covering through the final quarter of the firm’s 2022 fiscal year. Fast forward to today, and we now have data covering through the first quarter of 2023 as well. What management has presented looks incredibly bullish in and of itself. As an example, we need only to look at revenue. Sales for the latest quarter came in strong at $588.3 million. That represents an increase of 78.1% over the $330.4 million in revenue generated the same time one year earlier. To be clear, about $101 million of this increase came from the company’s acquisition of rival Commodore. However, there were other contributors to the increase. For instance, the net factory-built housing revenue per home sold that the company generated came in at $107,108. That’s 26.9% above the $84,401 generated just one year earlier. In terms of overall product volume, the company saw the number of homes sold rise from 3,700 in the first quarter of its 2022 fiscal year to 5,346 the same time this year, while the number of modules grew from 6,318 to 9,242.

Author – SEC EDGAR Data

This rise in revenue brought with it a significant improvement in profitability. Net income for the quarter came in at $59.6 million. That’s more than double the $27 million generated the same time one year earlier. Although the company was hit by a decline in revenue associated with its financial services and a corresponding margin decrease in financial services activities, the gross profit margin associated with its factory-built housing rose from 21.2% to 24.4%. This was due, management said, mostly to higher average sales prices, increased home sales volume, and a few other items. This increase in profits also brought with it a rise in cash flow. Operating cash flow, for instance, rose from $24.3 million in the first quarter of 2022 to $58.2 million the same time this year. If we adjust for changes in working capital, the increase year over year would have been greater, with the metric climbing from $22.7 million to $61.7 million. Meanwhile, EBITDA for the company also increased, rising from $34.6 million to $82.4 million.

It is worth noting that there are some other items that warrant discussion. For instance, management was very active in buying back stock. During the first quarter alone, they allocated $39 million to buy back shares. Clearly, they are bullish about their own business. On top of that, the company has no debt and has cash and cash equivalents of $268.8 million. So the firm could buy a significant amount of stock back still or it can make sure it has a proper cash cushion to weather any pain that might be around the corner. The only bad thing that I saw recently was a decrease in backlog. The metric dropped from around $1.1 billion to $998 million. Admittedly, this is still higher than the $792 million seen just one year earlier. This is important because it’s a sign of future revenue. And in subsequent quarters, investors would be wise to keep a close eye on this to see just how the outlook for the space will look moving forward.

Author – SEC EDGAR Data

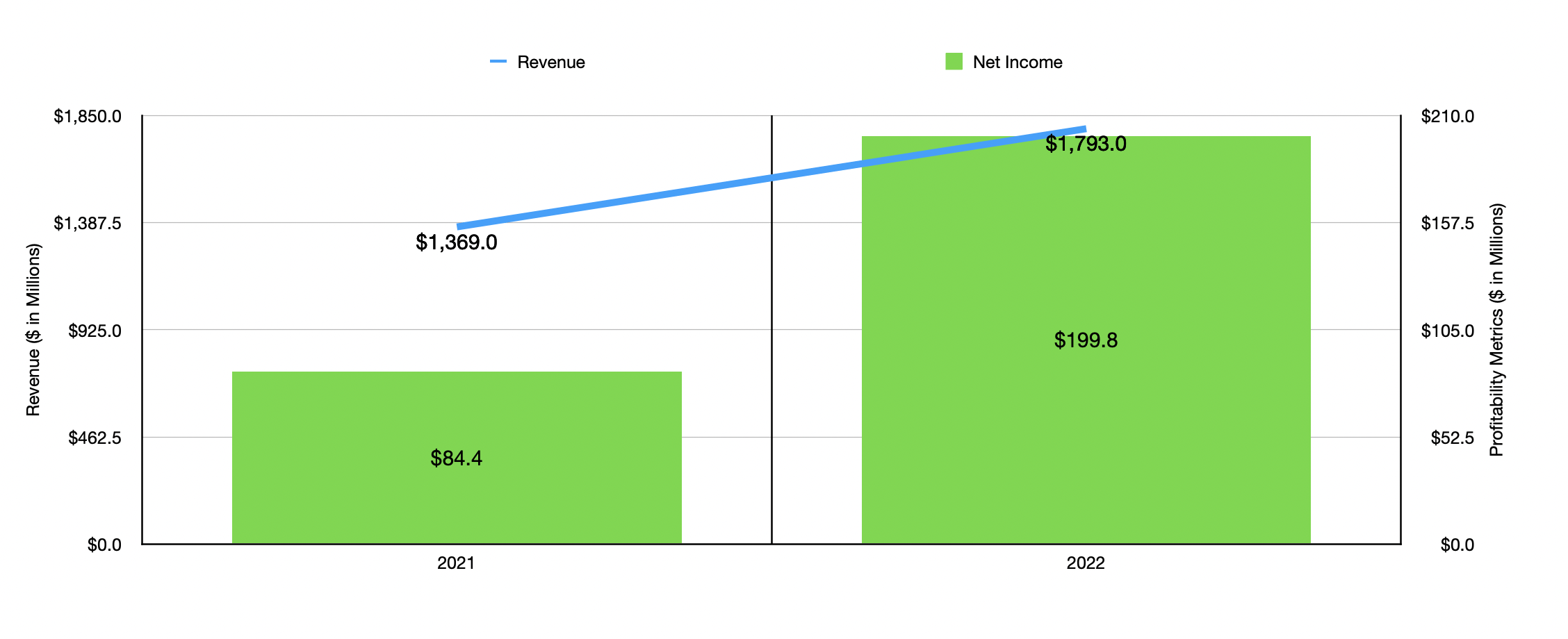

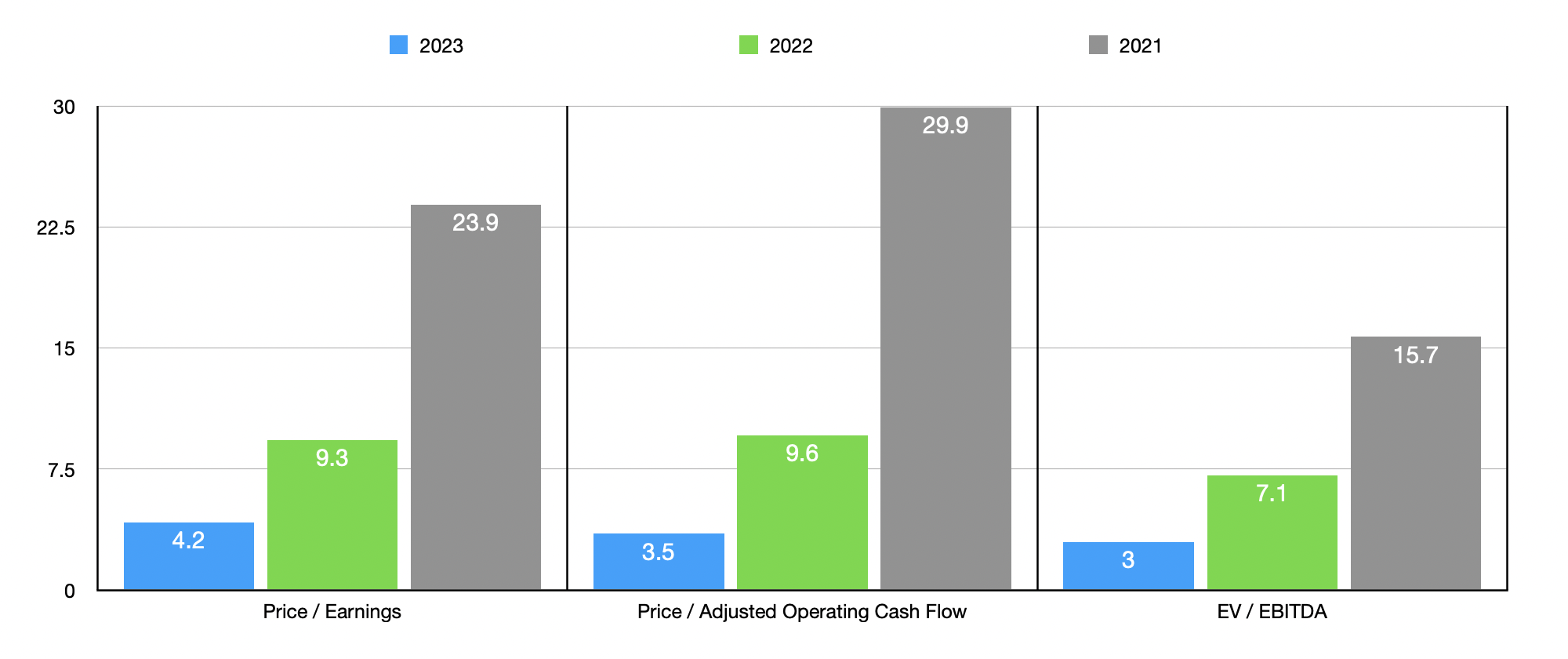

Management has not, unfortunately, provided any real guidance for the current fiscal year. But if we were to annualize results seen during the first quarter alone, we would anticipate net income of $436.4 million, adjusted operating cash flow of $520.5 million, and EBITDA of roughly $520.6 million. This would translate to a forward price to earnings multiple of 4.2, a forward price to adjusted operating cash flow multiple of 3.5, and a forward EV to EBITDA multiple of 3. Of course, it would be unwise to assume that market conditions will allow that trend to continue. If, instead, the company were to revert back to the levels of profitability seen in the 2022 fiscal year, these multiples would be 9.3, 9.6, and 7.1, respectively. Investors would be right to point out that the acquisition of Commodore made a complete turn back to 2022 levels unlikely. But it’s worth noting, as the chart above illustrates, that the difference in financial performance, particularly on the bottom line, that would have been seen had Commodore been incorporated for the entirety of the 2022 fiscal year, it’s not all that different than what the company did ultimately experience.

Author – SEC EDGAR Data

The real key here is to make sure that financial performance does not revert back to the levels experienced during 2021. That would translate to a price to earnings multiple of 23.9, a price to adjusted operating cash flow multiple of 29.9, and an EV to EBITDA multiple of 15.7. In these scenarios, I would make the case that shares are likely overvalued to some degree. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 2.7 to a high of 9.7. Four out of the five companies, using our 2022 figures, were cheaper than Cavco Industries. Using the price to operating cash flow approach, the range is between 4.4 and 25.7, with two of the five companies being cheaper than our prospect. And when it comes to the EV to EBITDA approach, the range is between 3 and 5.6. In this case, our target is the most expensive of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Cavco Industries (CVCO) | 9.3 | 9.6 | 7.1 |

| Taylor Morrison Home Corporation (TMHC) | 3.2 | 4.4 | 4.3 |

| M/I Homes (MHO) | 2.7 | 6.8 | 3.0 |

| Skyline Champion Corporation (SKY) | 9.7 | 13.0 | 5.6 |

| Tri Pointe homes (TPH) | 3.5 | 11.2 | 3.9 |

| Century Communities (CCS) | 2.7 | 25.7 | 3.4 |

Takeaway

Based on all the data provided, it seems to me as though Cavco Industries is having an exceptional time right now. Fundamental performance is incredibly robust and management has plenty of cash to cushion the company with while potentially buying back more shares. The backlog figures provided are somewhat concerning and could worsen in the upcoming quarters. And there is some risk that financial performance could revert back to what it was a couple of years ago. If that does transpire, shares might have some downside. But the evidence that we see right now suggests that such a fear might be premature to have. Long-term, I believe the future for the company is positive, but given the uncertainty we are seeing in the housing market and the fact that a company that sells lower-priced homes would likely be disproportionately impacted by a housing recession, I think a more appropriate rating for the company right now is a ‘hold’ instead of the ‘buy’ I had it at previously.

Be the first to comment