CHENG FENG CHIANG

All financial numbers in this article are in Canadian dollars unless noted otherwise.

Introduction

The earnings season has heated up. We’re now in the hottest phase of the season, with multiple railroads reporting their fourth-quarter results. One of them is the Canadian National Railway Company (NYSE:CNI). This railroad is one of the few Class I railroads that’s not a part of my portfolio, as I own Union Pacific (UNP), Norfolk Southern (NSC), and Canadian Pacific (CP). The reason to exclude CNI is not based on its qualities but on my already large industry exposure. I have often made the case that CNI is a terrific long-term (dividend) investment, thanks to its ability to outperform the market, consistently grow its dividend, and offer superior services.

In this article, we’ll assess the company’s fourth-quarter earnings, which confirm all of this. The company beat both EPS and revenue expectations, reported a very strong operating performance, and even avoided being pressured by rising costs.

The only thing that bothered investors was its weak guidance, which makes sense in light of slowing economic indicators.

However, I believe investors need to embrace stock price weakness. Getting CNI shares at a better valuation is the best way to build long-term wealth with this Canadian gem.

4Q22 – Dealing With Challenges

I like North American Class I railroads for several reasons:

- They tend to be fantastic dividend growth stocks.

- They have huge moats, thanks to limited competition.

- They tell us a lot about economic developments due to large footprints in various supply chains.

- They are very cyclical, which means when applying some timing and macro skills, investors can buy these stocks at tremendous prices.

In this article, I mainly want to focus on the last two bullet points.

Unlike in prior quarters, we’re now in a different situation. Volume growth is slowly turning into contraction, pricing gains are fading, and operating expenses remain an issue. On top of that, most railroads are still dealing with operating inefficiencies.

During the pandemic, railroads reduced employee levels and spending on equipment. After all, volumes had imploded. Once lockdowns ended, demand came back roaring, which overwhelmed supply chains – including railroads. Since then, railroads have worked on training new employees and dealing with congestion issues.

The good news is that Canadian National is doing what it does best: mastering challenges.

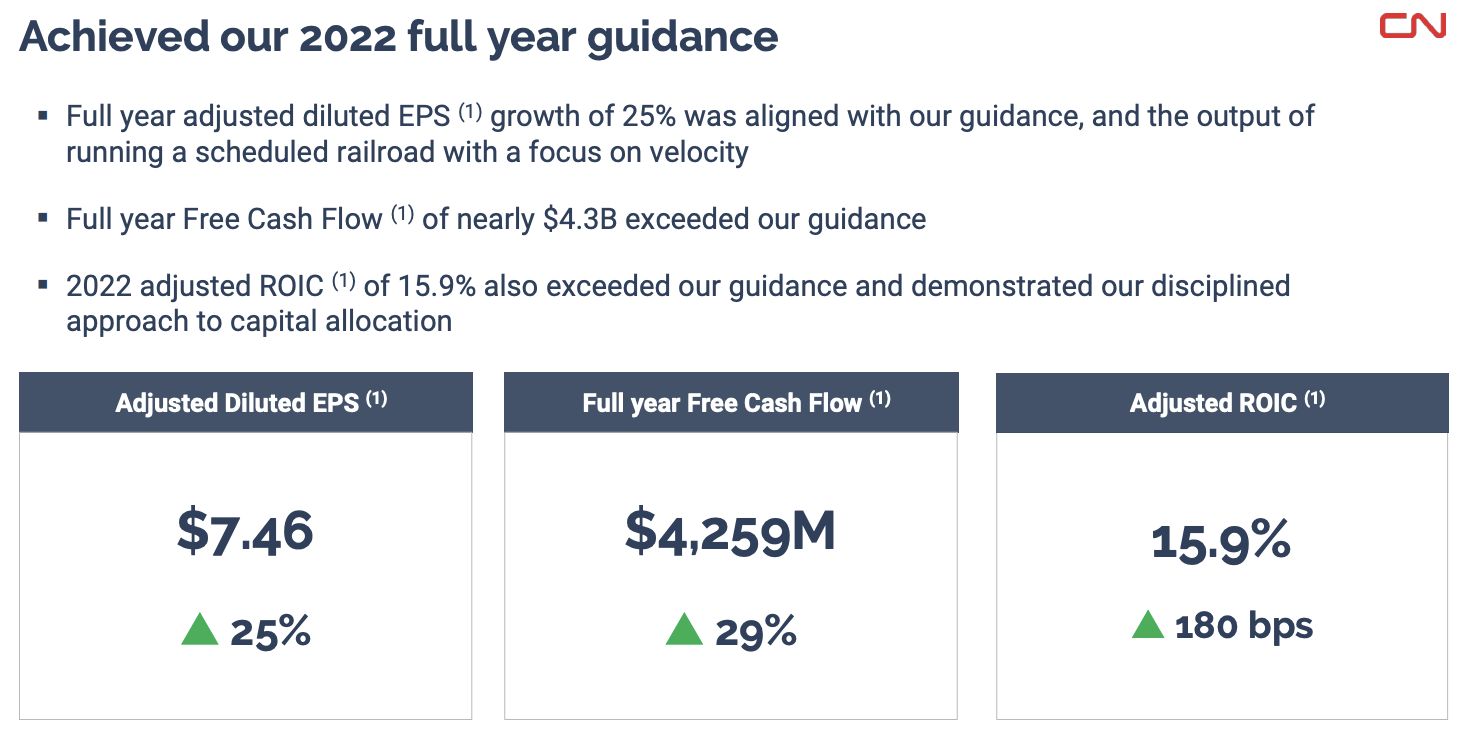

Moreover, the company achieved full-year guidance, as it grew diluted EPS by 25%, free cash flow by 29%, and adjusted return on invested capital by 180%.

Canadian National Railway

With that said, let’s dive into the details!

Impressive Top-Line Growth

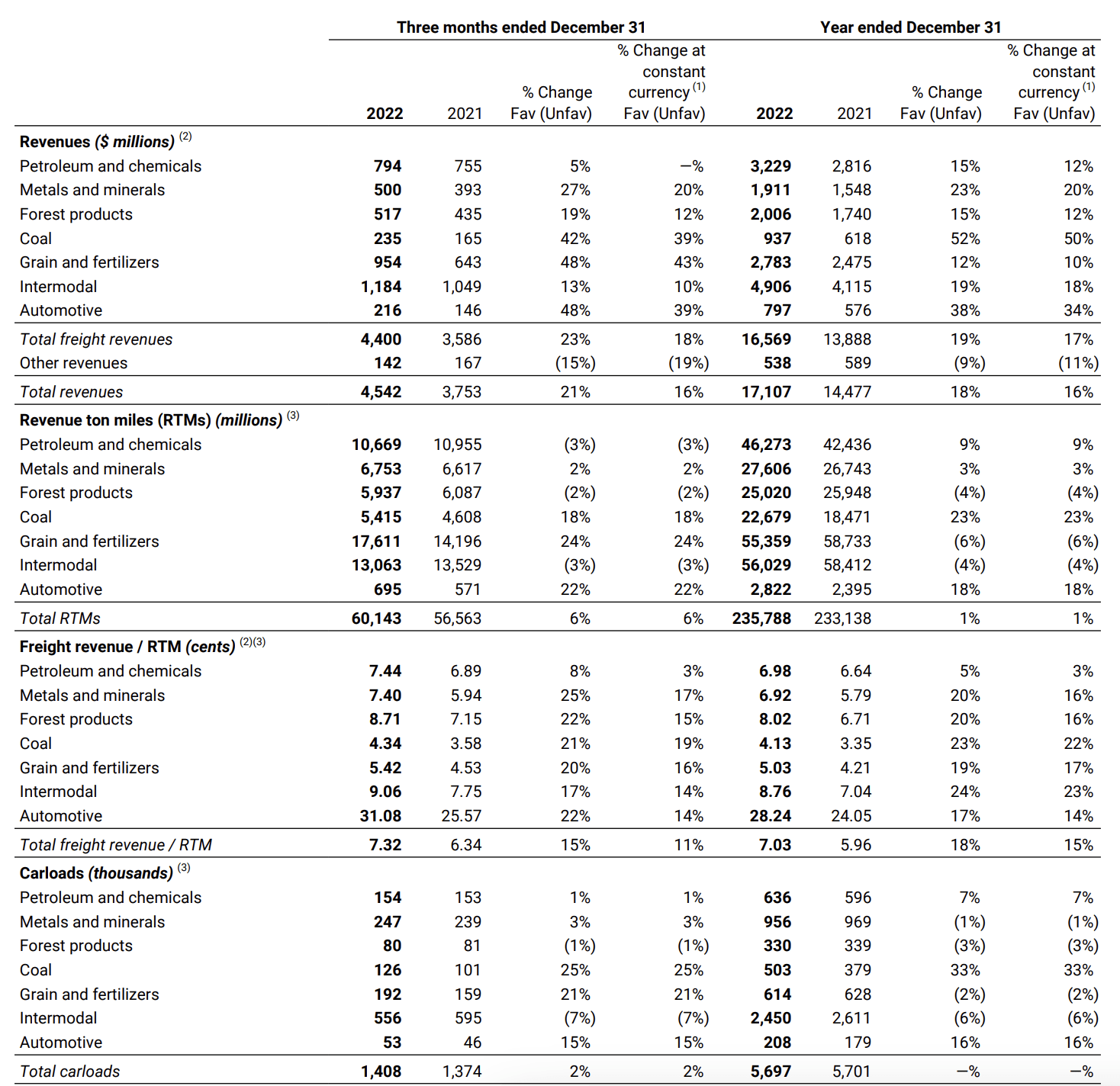

In its fourth quarter, the company did $2.10 in earnings per share. That number is $0.02 higher than expected. This result was provided by a 21.1% increase in revenue to $4.54 billion. That number is $60 million higher than expected.

As the table below shows, the company benefited from higher shipments. Total carloads rose by 2% as only forest products (a minor segment) and intermodal showed declines. The decline in intermodal is caused by inventory overstocking at retailers. Strength came from grains, which saw more than 20% growth. The month of October was the best month for grains in the history of the company. Other commodities like coal and energy were also strong, thanks to higher production and high export demand. Automotive shipments (a minor segment) were up by double digits as producers were finally able to turn backlog into finished vehicles. That’s due to easing supply chain issues.

Canadian National Railway

Revenue ton-miles (shipments adjusted for traveled miles) were up 6%.

When adding pricing, the company generated growth in every single segment. Pricing is mainly driven by fuel surcharges.

Operating Costs & Operating Efficiencies

The first Class I railroad reporting earnings this season was Union Pacific. Union Pacific reported 8% revenue growth and 14% higher operating expenses. It reduced operating income by 1%.

It was the result of ongoing investments in employees, new equipment, and high inflation. The Canadian National Railway suffered from the same issues. However, the situation was less dramatic.

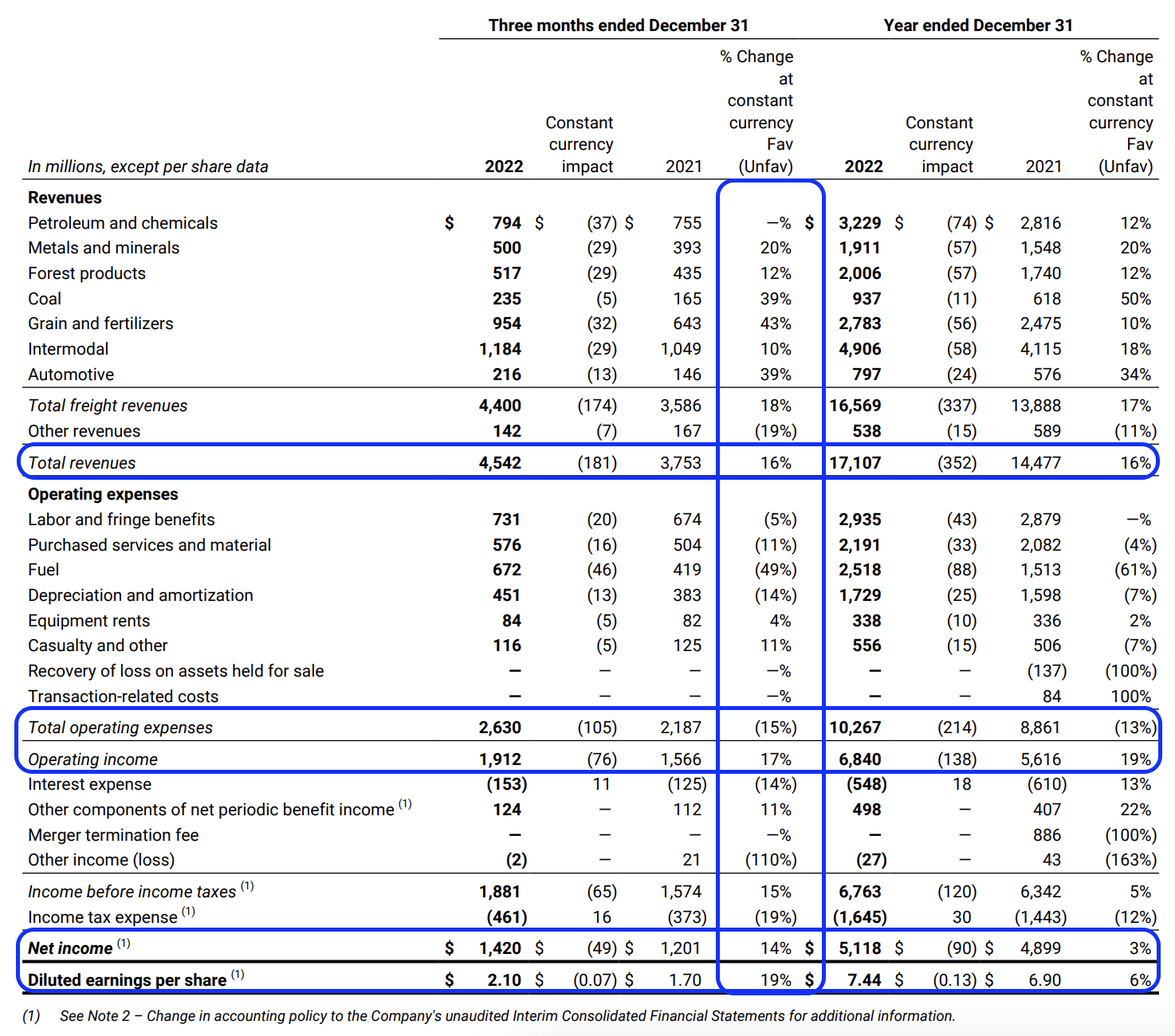

On a constant currency basis, the company generated 16% revenue growth with strength in every segment, as we just discussed. Operating expenses rose by 15% to $2.6 billion. As this growth rate is slower than the revenue growth rate, the company leveraged operating income, which rose by 17% to $1.9 billion.

Canadian National Railway (Author Annotations)

Unsurprisingly, the biggest growth rate was seen in fuel expenses, as diesel prices are much higher compared to last year.

As a result, the company reported an operating ratio of 57.9%. This is an improvement of 40 basis points (flat on an adjusted basis). This is an impressive performance, as most railroads are now dealing with operating ratios of more than 60%. I also doubt that a lot of railroads will be able to improve their operating ratio.

Even better, the company improved a wide range of operating metrics as system fluidity is returning.

Car velocity averaged 207 miles per day, which is an improvement of 10%. Origin train performance averaged 85%, which is also up 10%. Restoring network fluidity is tough. It is harder when dealing with Canadian weather conditions. In some areas, the railroad was dealing with temperatures dropping to minus 50 Celsius.

Our approach to scheduled railroading and focus of our employees helped us to restore fluidity on the network. I am amazed how the team responded and you can see it in the operating performance. So far this month alone, car velocity is hovering near 220 car miles per day, similar to the numbers that this company saw last summer. Now winter is far from over, but compared to last year, we are in a much better position to start the year, and it means we should be in a better position to come out of winter into the spring.

Free Cash Flow & Dividend

Free cash flow came in at $4.3 billion on a full-year basis. This is up from $3.3 billion in 2021. The company bought back shares worth $4.7 billion and distributed $2.0 billion in the form of dividends.

Before the earnings call, the company hiked its dividend by 8% for 2023. This marks the 27th consecutive year of dividend increases since the 1995 IPO.

The company now yields 1.9%.

The Board also approved a new share buyback program of up to 32 million shares for an amount in the range of $4 billion to be returned to shareholders through a normal course issuer bid from February 1, 2023, to January 31, 2024.

So far, so good, but what about the outlook?

2023 Will Be Challenging

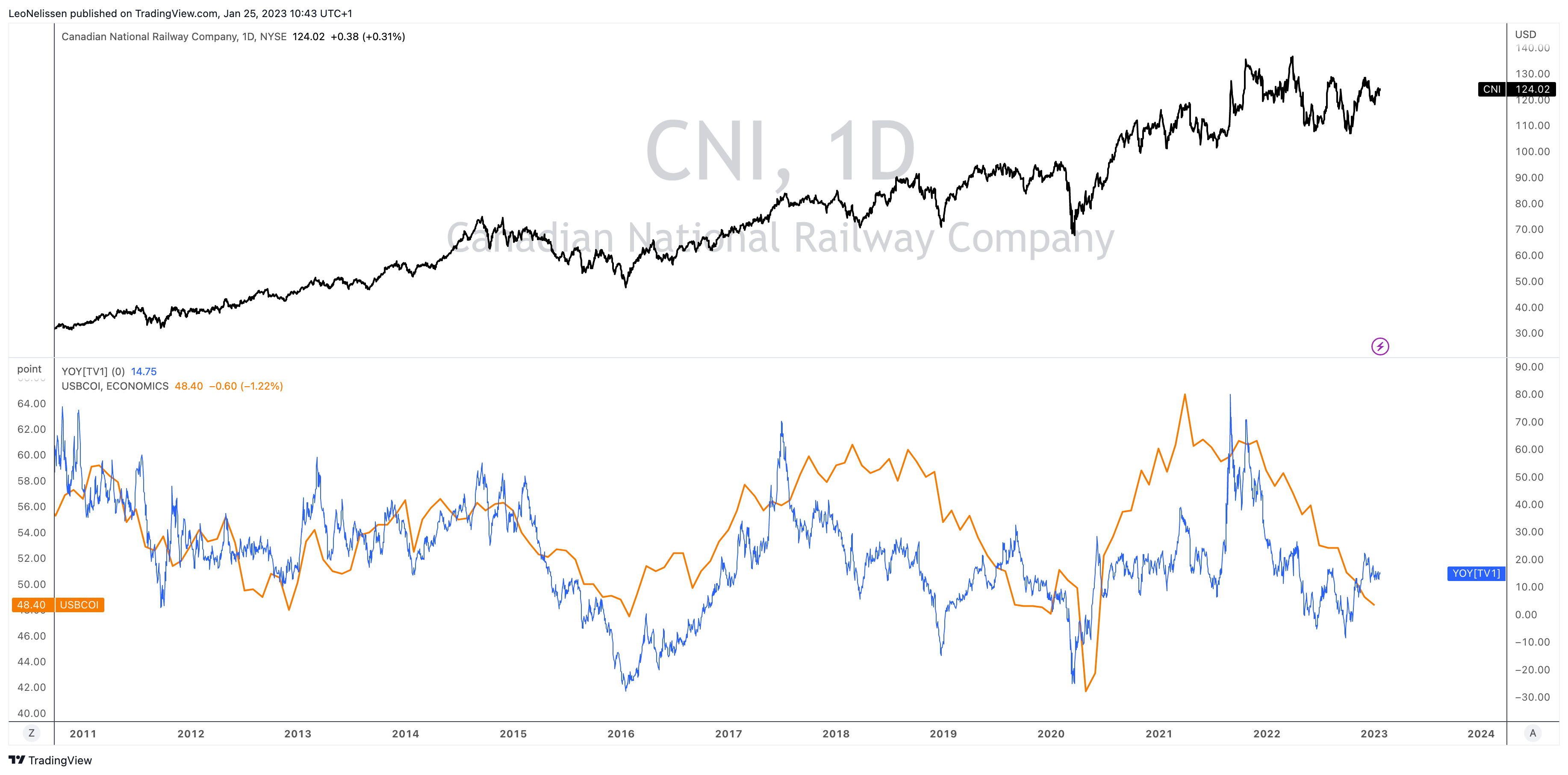

The figure below shows NY-listed CNI shares and the comparison between the year-on-year performance of the stock price and the ISM manufacturing index. For the first time since the 2018 peak, we’re in a situation where economic growth is accelerating to the downside.

TradingView (CNI, CNI Y/Y vs. ISM Index)

CNI shares are adapting to this new situation, albeit slowly.

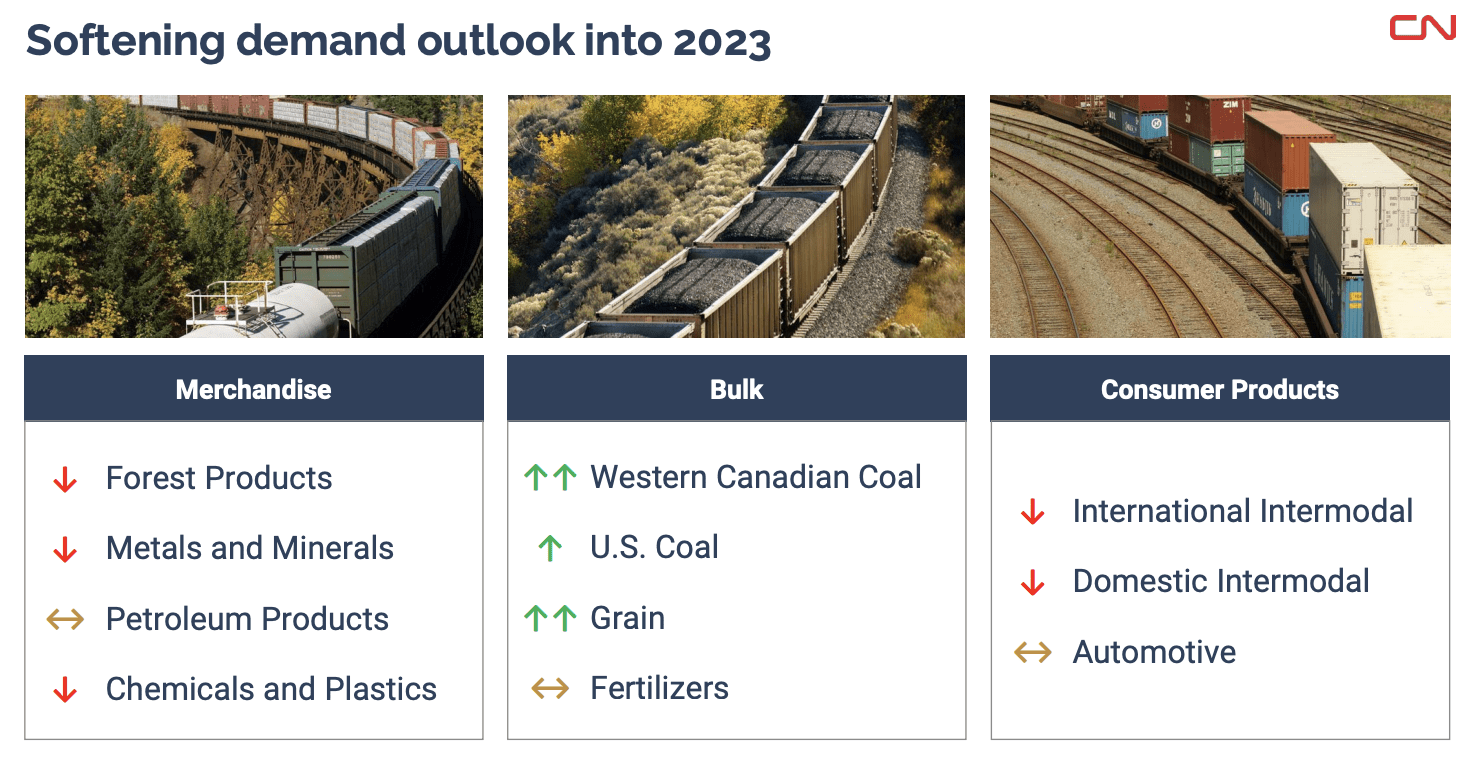

On a full-year basis, CNI has turned bearish on shipments. The company sees weakness in merchandise and consumer products, as cyclical product groups like forest products, metals, chemicals, and intermodal are all expected to show weakness. Coal and grains are expected to remain strong. I agree with that assessment, as I’m bullish on energy and agriculture volumes.

Canadian National Railway

The company is incorporating a view that is based on a mild recession. It’s a soft landing where the Fed is expected to get inflation down without doing too much damage to the economy.

According to the company:

The weakness that we began seeing in the fourth quarter is expected to persist through at least the first half of 2023. The international intermodal will have multiple blank sailings as the North American inventories rebalance.

Lumber will be slow to recover due to market oversupply and high interest rates dampening demand. Chemical and petroleum production is directly tied to the economy, so we expect demand to be soft in the first half of 2023. Automobiles are still in a tight supply situation, but this is changing with higher interest rates as well as part shortages.

To close, we are working closely with customers to monitor the economic environment as we run a scheduled railroad with a focus on velocity, we are achieving solid performance that will serve our customers well and continue to grow with our customers as the economy recovers.

Valuation

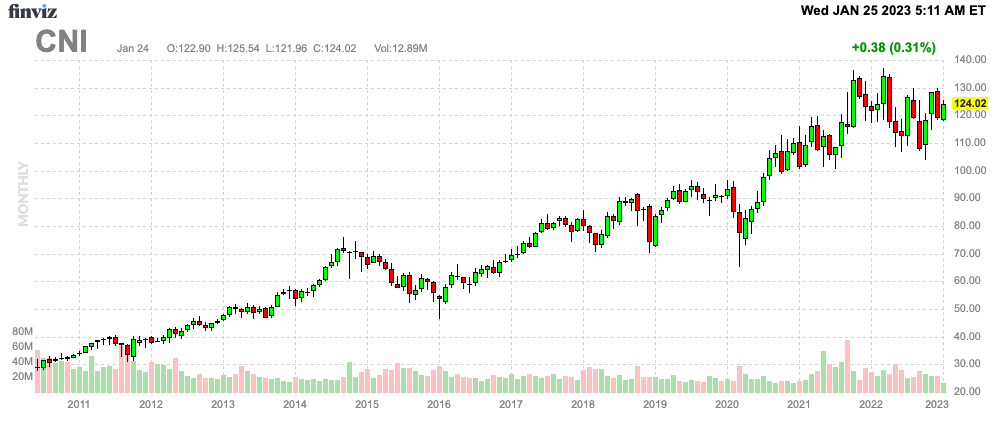

Canadian National shares in New York are just 10% below their 52-week-high while I am writing this. That’s an impressive performance and fully justified, given the company’s performance so far.

FINVIZ

Unfortunately, in light of economic challenges, this means the risk/reward is less favorable.

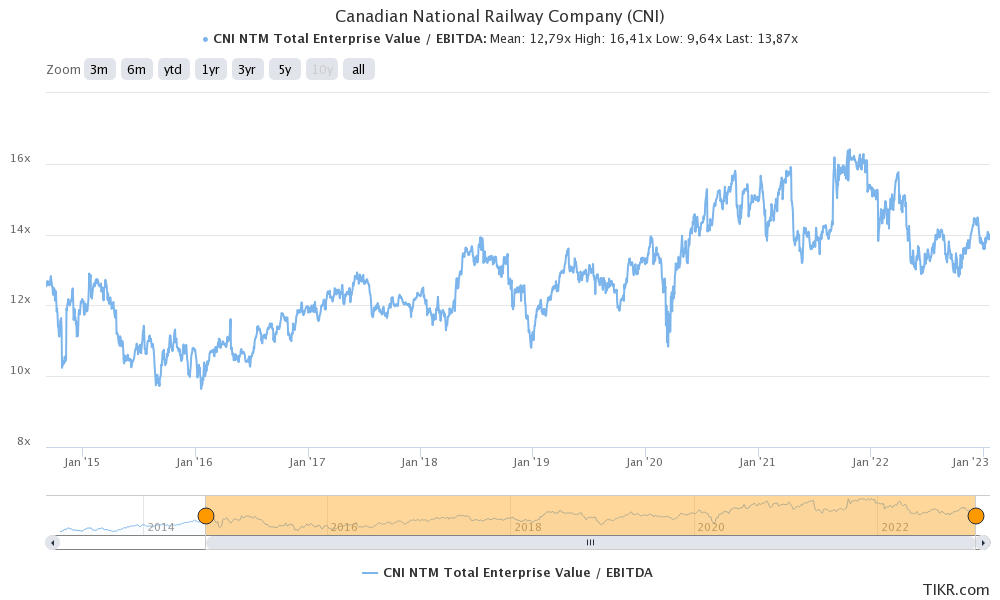

CNI shares are now trading at 14.0x 2023E EBITDA of $9.1 billion. This is based on its $127.2 billion market cap (in CAD, not USD), $14.1 billion in 2023E net debt, and $600 million in pension-related liabilities.

This valuation would be “OK” in an economic bull market, yet not in this environment. I would be more comfortable buying CNI with a multiple of less than 12x EBITDA.

TIKR.com

As I believe that the soft-landing thesis is too bullish, I think CNI (and other railroads) are due for more weakness in 2023. However, that’s a good thing as I mentioned earlier.

I’m embracing weakness, as I have a large war chest and a watchlist full of cyclical stocks. Investors looking for quality industrial exposure might enjoy adding the CNI ticker to their portfolios.

Takeaway

In this article, we discussed Canadian National’s earnings. The company did a tremendous job growing revenue and operating income, thanks to strong carloads, pricing benefits, and underperforming growth in expenses.

The problem is that the company’s stock price does not offer an attractive risk/reward. Thanks to its stellar performance, it is still close to its all-time high.

Now, economic growth is declining, resulting in expected revenue weakness in 2023. As I do not believe in a soft-landing scenario, I believe that CNI shares are in for more weakness.

However, that’s a good thing as weakness means new buying opportunities.

So, regardless of what happens, I think 2023 will be a good year for CNI investors.

Needless to say, I’ll keep you up to date!

(Dis)agree? Let me know in the comments!

Be the first to comment