Alexander Spatari/Moment via Getty Images

Clipper Realty, Inc (NYSE:CLPR) is a self-managed real estate investment trust (“REIT”) that operates multifamily residential and commercial properties in the New York metropolitan area, with operations in Manhattan and Brooklyn.

The company’s scale is small, with limited geographic exposure and less than ten primary properties in their portfolio. This exposes them to unique risks relating to the local New York economy, as well as building-specific risks.

In addition, they depend on a single government tenant in their office portfolio. While the space is fully occupied, the company could be at significant risk if they were to lose the tenant.

Though the company has posted solid operating metrics, their risk profile is high. An elevated debt load further compounds the risks relating to their limited scale. Over the past year, the stock has traded in a tight 52-week range and is down about 26%. While this is better than some others on a relative basis, it’s unlikely shares will outperform over the long run. For investors seeking new opportunities, CLPR is one best kept on the sidelines.

Current Ratings Summary

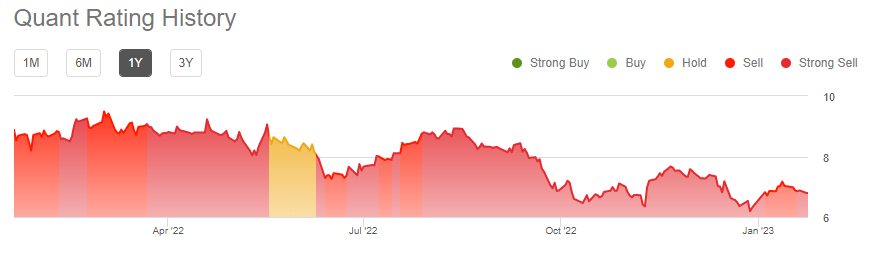

CLPR ranks very poorly on Seeking Alpha’s (“SA”) quant system. Presently, the quant is assigning shares a “strong sell” rating, with poor grades on every metric. In the middle of 2022, shares scored higher due to building momentum, but that proved short lived.

Seeking Alpha – Quant Rating History Of CLPR

Authors on SA and Wall Street analysts are both more receptive to the stock, though it’s worth mentioning the company is thinly covered. There have been just two SA pieces on the stock over the past 30 days and only three analysts on Wall Street have covered the stock in the last 90 days.

That being said, one should not get too excited about the current average price target on the stock, which is currently $12.50/share. That would imply upside of 85% from current levels. While that may sound appealing, the limited number of analysts covering the stock, especially in recent periods, diminishes the value of that target.

Current Portfolio Metrics

At the end of the third quarter, all of CLPR’s operating metrics were exceeding pre-pandemic levels. In addition, management noted continued demand strength in their markets.

New lease rental rates during the quarter were up 23%, while renewals were up 9%. And through nine reported months, new lease rates and renewals have increased 27% and 16%, respectively.

In addition, leased occupancy stood at about 99% at the end of the quarter. This was supplemented by strong overall collection rates of 95.5%.

Strong demand and stable portfolio metrics resulted in record revenue and net operating income (“NOI”) during the quarter.

Looking ahead, their newly developed property at 1010 Pacific Street is expected to lease-up through Q1FY23. Aside from this property, the company also has embedded opportunities within their newly acquired property at 953 Dean Street and their development at Prospect Heights.

While this could be accretive over the long-run, the development activities could constrain liquidity in the near-term.

Liquidity and Debt Profile

At September 30, 2022, CLPR’s total debt load amounted to +$1.2B. For their size, this is precariously high. To put this into perspective, they’ve generated +$44M in EBITDA through nine months of the year. Even at the forward annualized run rate, debt is hovering at nearly 20x earnings.

Total debt is also well above their current market capitalization and is about 85% of their reported gross assets.

CLPR also added to their total burden in the current year with their borrowings relating to the development of their 1010 Pacific Street property and the acquisition 953 Dean Street.

As an offset to their overly leveraged position is their maturity schedule, which is favorably skewed towards later years. In addition, most of their obligations are fixed rate, which hedges against the risk of changing interest rates.

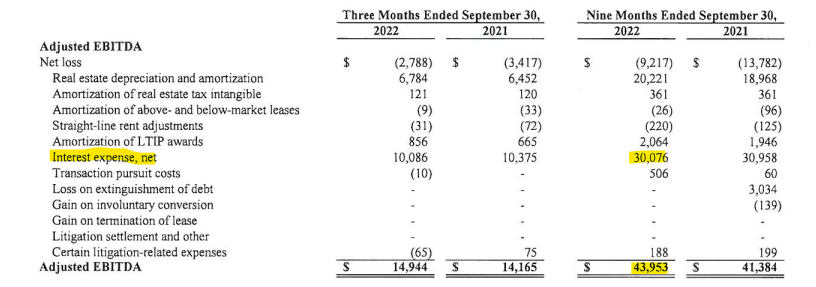

Still, interest expense is their single largest line item on their income statement. And EBITDA coverage is just under 1.5x.

Q3FY22 Investor Supplement – Reported Adjusted EBITDA In Relation To Total Interest Expense

While management does highlight their liquidity position as a strength, due to available cash of about +$35.5M, in addition to positive reoccurring operating cash flows, their overall financial position appears vulnerable.

Dividend Safety

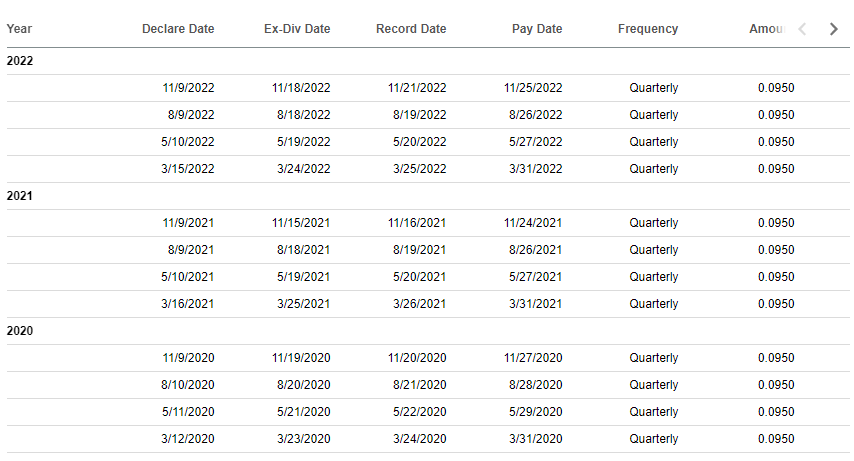

CLPR currently provides a quarterly payout of $0.095/share. At its current share price, this represents an annualized yield of about 5.6%.

Over the past several years, the quarterly rate has remained stable, even through 2020.

Seeking Alpha – CLPR Dividend Payout History Over Past Three Years

However, there is little room for growth in the payout due to their constraining debt load and associated debt servicing costs.

Coverage through adjusted funds from operations (“FFO”), nevertheless, appears adequate. In the current period, for example, CLPR reported AFFO of $0.12/share. The payout ratio would thus be 79%. Though above sector averages, it isn’t significantly out of line.

Additionally, they do generate sufficient operating cash flows to fully cover their payouts. It is important to note, however, that they are using more than +$30M in cash to pay interest, which is significant.

While the dividend remains fixed in its current form for now, investors should assess a higher risk premium on payout continuity.

Main Takeaways

CLPR’s local expertise in the New York metropolitan market is one competitive strength that enables the company to better navigate the complexities of the market environment. Their portfolio, though small, also has a few notable properties to their name, such as the Tribeca House and Flatbush Gardens, two prominent housing communities in the surrounding neighborhood.

The company has also capitalized on strong demand through record rental rate growth and occupancy levels. This has enabled CLPR to post solid quarterly results with regards to operating performance.

Their leasing performance and regional expertise, however, is mostly offset by their higher debt burden. Though CLPR has adequate liquidity in the form of cash on hand and through reoccurring cash flows, their debt servicing costs consume much of their outlays.

Substantially all their debt is fixed, however, and there are no material short-term maturities. These characteristics de-risks their profile in some sense but not enough to get comfortable.

Their 5.6% yielding dividend is perhaps one draw to the stock. Shares, however, don’t offer much further opportunity. At 19x forward earnings, the stock trades several notches above peers within the sector, who typically are commanding multiples in the range of 14-16x, on average.

And even though the dividend may seem attractive, it is more likely to end up on the chopping block in future periods, given their higher operating leverage. For investors seeking new opportunities, CLPR would be one to follow from afar.

Be the first to comment