jaanalisette/iStock Editorial via Getty Images

Investment Thesis

We follow up on our post-earnings article on Twilio Inc. (NYSE:TWLO) stock. We highlighted in our previous article that the risk/reward profile was still unattractive, despite its massive collapse. However, there has been a material and significant development in its price action over the past month.

Our most updated price action analysis suggests that its near-term bottom has been breached and is no longer valid. Notably, we have not observed any potential double bottom bear trap that could help stanch its steep decline. Moreover, given its dominant bearish bias, we wouldn’t even be keen on a “normal” bear trap reversal price action in TWLO stock. So instead, we need a double bottom and nothing less.

Furthermore, our valuation analysis suggests it’s incredibly challenging to value TWLO stock. Its weak free cash flow (FCF) profitability is a critical concern. Therefore, we believe that the pummeling of TWLO stock is justified. Without sustainable FCF, Twilio investors need to ask themselves what they are investing in. The story is good, but the underlying metrics are terrible.

As such, we reiterate our Hold rating on TWLO stock. Moreover, we don’t think TWLO stock can recover to $200 anytime soon unless its FCF profitability improves markedly.

Is Twilio Profitable?

Twilio adjusted EBIT margins % and FCF margins % consensus estimates (S&P Cap IQ)

Street analysts and management prefer to use its adjusted profitability metrics to parse Twilio’s underlying performance. However, we urge investors to be cautious with using this approach. Because Twilio is still struggling with generating free cash flow profitability.

The consensus estimates suggest that Twilio’s FCF profitability should improve as it seeks to achieve non-GAAP operating profitability by 2023. However, having an FCF margin estimate of 1.1% in FY23 is nothing to shout about. It only emphasizes the company’s weak operating leverage, despite its story thesis. What has Twilio’s leadership in its space amounted to? If it cannot generate robust FCF with its leadership, we find it challenging to envisage how it can improve its FCF margins moving ahead.

Is Twilio Stock Overvalued?

TWLO valuation metrics (TIKR)

Using its NTM FCF yield and normalized P/E, we don’t think any rational investor can value TWLO stock accordingly. But, of course, some investors would tell us we are using the wrong metric. We should use its revenue multiples, right?

Unfortunately, we beg to differ. We have learned from our past mistakes with revenue multiples and will not repeat them. Unless a company can prove its profitability, it will be challenging to value it using a fundamental analysis framework.

| Stock | TWLO |

| Current market cap | $15.13B |

| Hurdle rate (CAGR) | 25% |

| Projection through | FQ2’26 |

| Required FCF yield in FQ2’26 | 2.5% |

| Assumed FCF margin in FQ2’26 | 2% |

| Implied TTM revenue by FQ2’26 | $46.18B |

TWLO stock reverse cash flow valuation model. Data source: S&P Cap IQ, author

Our reverse cash flow valuation model laid bare just how overvalued TWLO stock seems. We used a higher than average hurdle rate appropriate for a typical growth stock.

But, we think a 25% hurdle rate is pretty reasonable for a “high-growth” player like TWLO. Anything lesser is not worth our consideration.

We also used a reasonable FCF yield of 2.5% by FQ2’26, based on an FCF margin of 2%. However, our model indicates that Twilio needs to deliver a TTM revenue of $46.18B by FQ2’26, an “impossible” scenario.

The consensus estimates suggest that Twilio could post revenue of $5.01B in FY23. Therefore, unless Twilio can improve its FCF profitability markedly over the next four years, we think TWLO stock is still massively overvalued (based on fundamental analysis).

Will Twilio Stock Recover To $200?

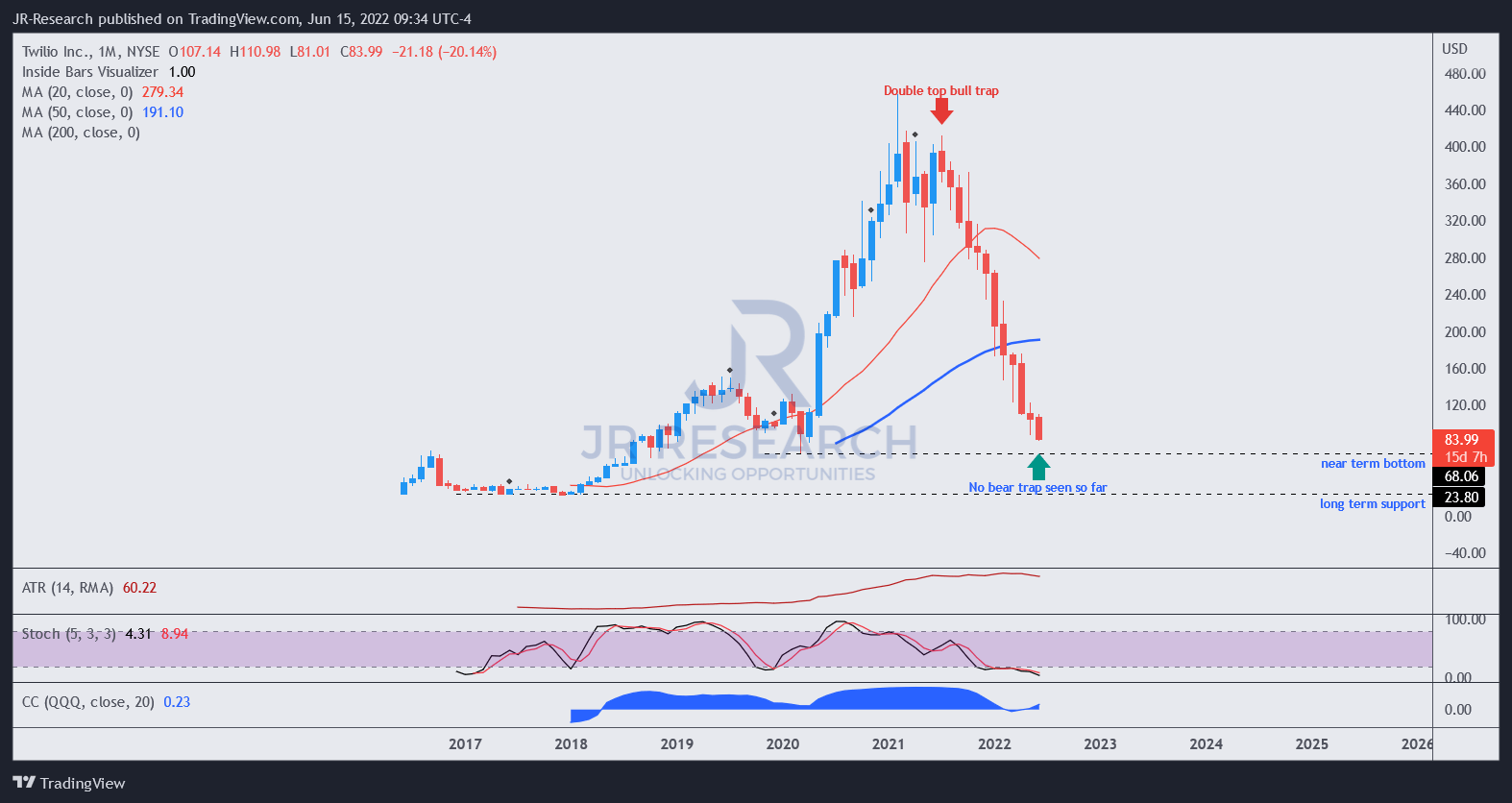

TWLO price chart (TradingView)

That’s the multi-million dollar question. Unfortunately, given its poor fundamental metrics, we don’t think it helps investors understand whether Twilio stock can retake its $200 levels.

Therefore, we believe an appropriate price action analysis can unveil critical clues. Moreover, as the market is forward-looking, TWLO investors should watch how the market intends to value TWLO stock. So, why did TWLO stock surge to a high of $457 in February 2021, despite its weak profitability metrics.

We think the market is brilliant. It drew in buyers rapidly, driven by the Fed-induced liquidity craze, putting money to work in unprofitable growth stocks. However, the mood shifted dramatically after its double top bull trap in July 2021.

Unfortunately, we had not paid sufficient attention to its price action previously. So, we will not repeat our mistakes this time. The potency of the double top is demonstrated clearly, sending TWLO stock into negative flow (decisive bearish momentum), which it has not recovered from.

Furthermore, we have not observed a double bottom bear trap that could help stanch its decline and stage a sustained bottom for a reversal in trend.

Therefore, we are watching whether TWLO can stage a double bottom at its near-term support of $68 (down 19% from the current levels). Otherwise, we cannot rule out a fall toward the gap leading to its long-term support of $23.80. Therefore, investors shouldn’t even consider whether it can hit $200 without thinking about where it would fall.

We learned that for unprofitable growth stocks, never say never.

Is TWLO Stock A Buy, Sell, Or Hold?

TWLO stock remains a Hold for now.

But, if you are not a speculative investor, then stay away from names like TWLO, as it’s massively overvalued.

But, if you have exposure for speculation, we urge you to bide your time and wait for a re-test of its near-term support before considering adding exposure.

Be the first to comment