Brett_Hondow/iStock Editorial via Getty Images

Introduction

Cadence Bank (NYSE:CADE) is one of the very few banks on my shortlist that actually saw its share price increase in the past few months. I wanted to have a closer look at its financial performance to see if there’s a good reason for Cadence to go against the tide.

The Q2 results were okay, but what about the increasing interest rates?

Banks tend to be in an excellent position to take advantage of increasing interest rates but in the current economic environment it will be important to make sure it doesn’t also result in a sharp increase in defaults and loans past due.

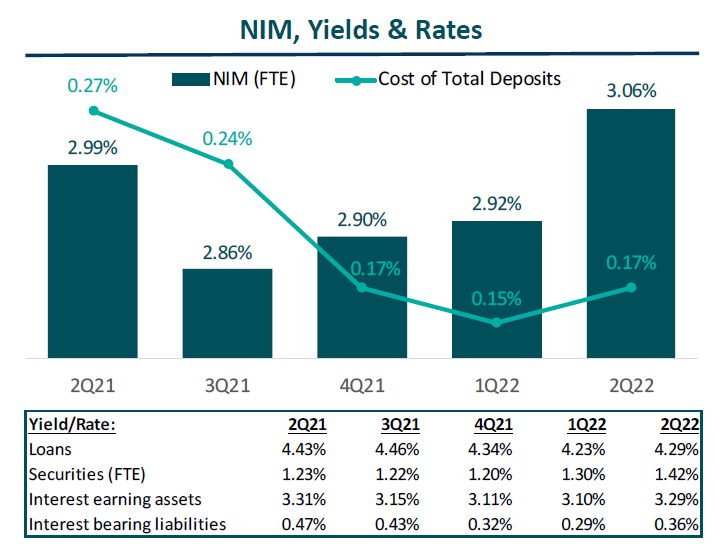

Cadence Bank saw its net interest income increase by approximately 4% in the second quarter compared to the performance in the first quarter thanks to a higher net interest margin and a slightly higher asset base.

Cadence Bank Investor Relations

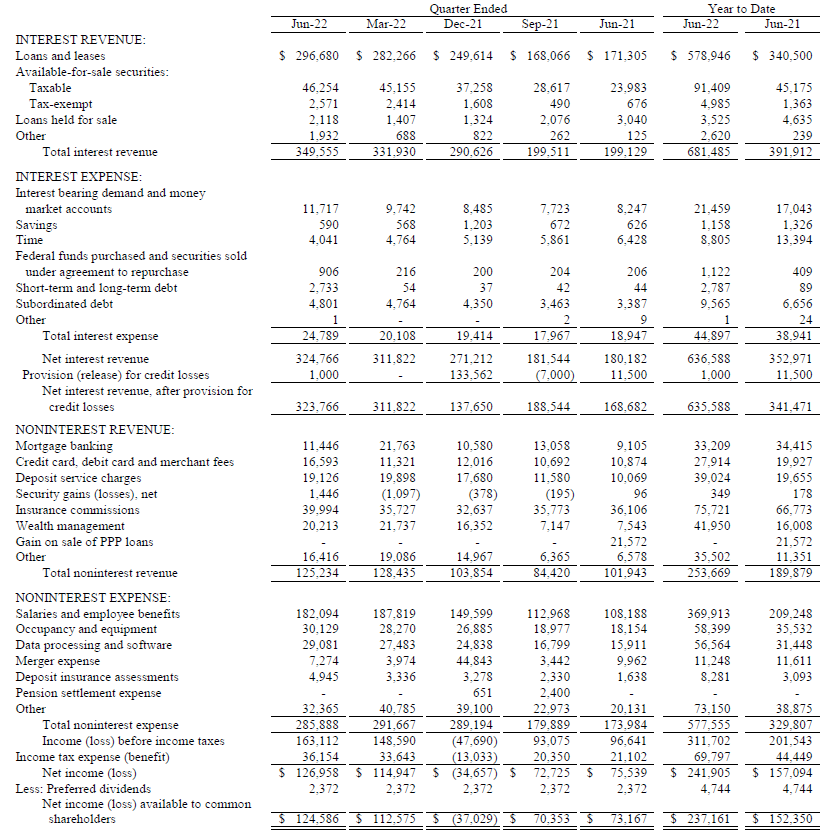

The net interest income came in at just under $325M which is the highest level ever (although it is difficult to compare it with the period before the acquisition which was completed in the second half of last year). The bank also reported just over $125M in non-interest income and about $286M in non-interest expenses resulting in a $164M pre-tax and pre loan loss provision income.

Cadence Bank Investor Relations

The loan loss provision was low, very low: Cadence Bank had to set aside just $1M after not having to record a single dollar in additional provisions in the previous quarter.

This eventually resulted in a pre-tax income of $163M and a net income of just under $127M. As the bank also has preferred shares outstanding (see later), the net income attributable to the common shareholders of Cadence was approximately $124.6M which represents an EPS of $0.68. A strong increase compared to the $0.60 EPS in the first quarter of the year as the higher net interest expenses provided a nice boost to the earnings.

The main issue when it comes to Cadence Bank is the impact of the increasing market interest rates on the value of the securities available for sale. Unfortunately this had a negative impact in the past few quarters and after recording a $525M loss on these securities in the first quarter of this year, on the comprehensive income statement, it looks like an additional $400M evaporated. As long as the interest rates continue to increase, the value of the securities available for sale will continue to be impacted.

The preferred shares are still attractive

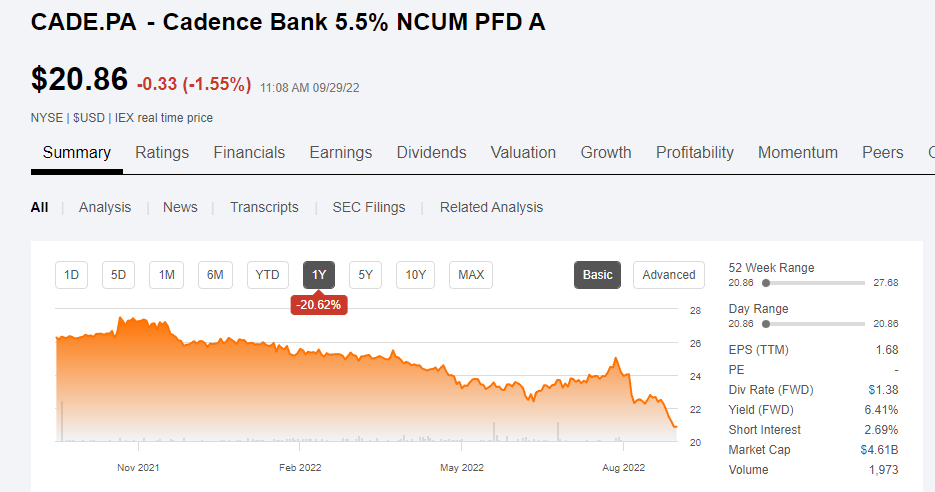

In the previous article, I also briefly discussed the bank’s preferred shares as Cadence Bank also has a non-cumulative preferred share outstanding trading as (NYSE:CADE.PA). This preferred share has a 5.50% preferred dividend yield. Considering the preferred dividends require less than 2% of the net income and the $172M of preferred stock outstanding (6.9M shares) ranks senior to the $3B in tangible common equity, the preferred share could be a good option for an income-focused investor.

While the share price of the common shares went up in the past 2.5 months, the preferred share price actually went down as the interest rates are increasing (thus putting pressure on fixed income securities). In the past 10 weeks or so, the preferred share price fell by in excess of 10% to the current level of $20.86.

Seeking Alpha

The preferred dividends obviously remain unchanged at 5.50% based on the principal amount of $25 which means the $1.375 in annual preferred dividends resulting in a current yield of approximately 6.6%. Not the highest in the banking sector but considering Cadence Bank needs less than 1.5% of its net earnings to cover the preferred dividend payments and considering there’s in excess of $2.5B in tangible equity ranked junior to the preferred shares, an investment in the preferred shares could be an option for investors primarily looking for income.

Investment thesis

Despite reporting decent profits, Cadence Bank saw its equity value decrease by about $600M in the first half of the year. This caused an erosion of the book value from $26.98 to $23.41 per share and the tangible book value dropped from $18.45 to $14.73. That’s hardly something to get really excited about but fortunately the bank’s earnings profile remain strong as it reported earnings totaling $1.28/share in the first semester and on an adjusted basis the EPS was $1.38 which is obviously pretty good (and the sole reason why the [tangible] book value per share didn’t drop even further than that).

I think the worst may be behind us when it comes to the erosion of the book value (although I do expect Q3 to show additional weakness) but I’m not sure I’m willing to pay almost 2 times the tangible book value at this point. While it is encouraging the TBV will be built at a rate of $1.5-1.75/share per year (the difference between the earnings and dividends paid), it would take the company approximately 6 years to close the gap between the TBV and the current share price.

Income-focused investors may be interested in the 6.6% yielding preferred shares but one will miss out on potential capital gains in the common share price. I currently have no position in either.

Be the first to comment