cemagraphics

C3.ai (NYSE:AI) has built a data science platform and a range of use case specific applications on top of that platform. The company promotes itself as the preeminent enterprise AI company, but this ignores the reality of its current capabilities and the competitive landscape. The current surge in share price is driven by hype around generative AI, rather than C3.ai’s prospects and investors should be aware of this. The stock could easily continue moving higher on the back of momentum and ignorance, or could collapse based on ongoing poor fundamentals.

C3.ai currently has 42 enterprise applications that provide predictive analytics within oil and gas, utilities, health care, manufacturing, aerospace, defense and intelligence. The company was founded in January of 2009 and since then has spent over a billion dollars developing their platform. The company’s current strategy is based around a belief that customers prefer off the shelf applications rather than building their own applications using existing tools.

A customer preference for applications is not currently borne out by C3.ai’s growth rate relative to competitors though, and if customers value AI, it is not clear why they would use off the shelf applications, as this would merely be table stakes and provide no competitive advantage.

C3.ai has pointed towards organizations like the hyperscalers, Cloudera, Apache open-source tools, Databricks and DataRobot as their primary competitors. Management has stated that they are succeeding by offering applications which reduce software development risk for customers and that no one, to C3.ai’s knowledge, has ever succeeded building their own AI applications using existing tools, which is clearly not correct. Thousands of organizations would not be spending hundreds of millions of dollars with companies like Alteryx (AYX) and Databricks if they were not realizing value.

Consumption-Based Pricing

Despite what management has stated publicly, C3.ai is obviously struggling to gain traction in the market and continues to experiment in the hopes of finding an approach that works. As part of this, C3.ai recently switched from a subscription-based model to a consumption-based one.

This appears to be in response to difficulties landing a sufficient number of customers, when trying to negotiate contracts worth tens of millions of dollars. Over around a three-year period, the new pricing model is supposed to be revenue neutral, but the far lower upfront cost should open access to significantly more customers.

Generative AI

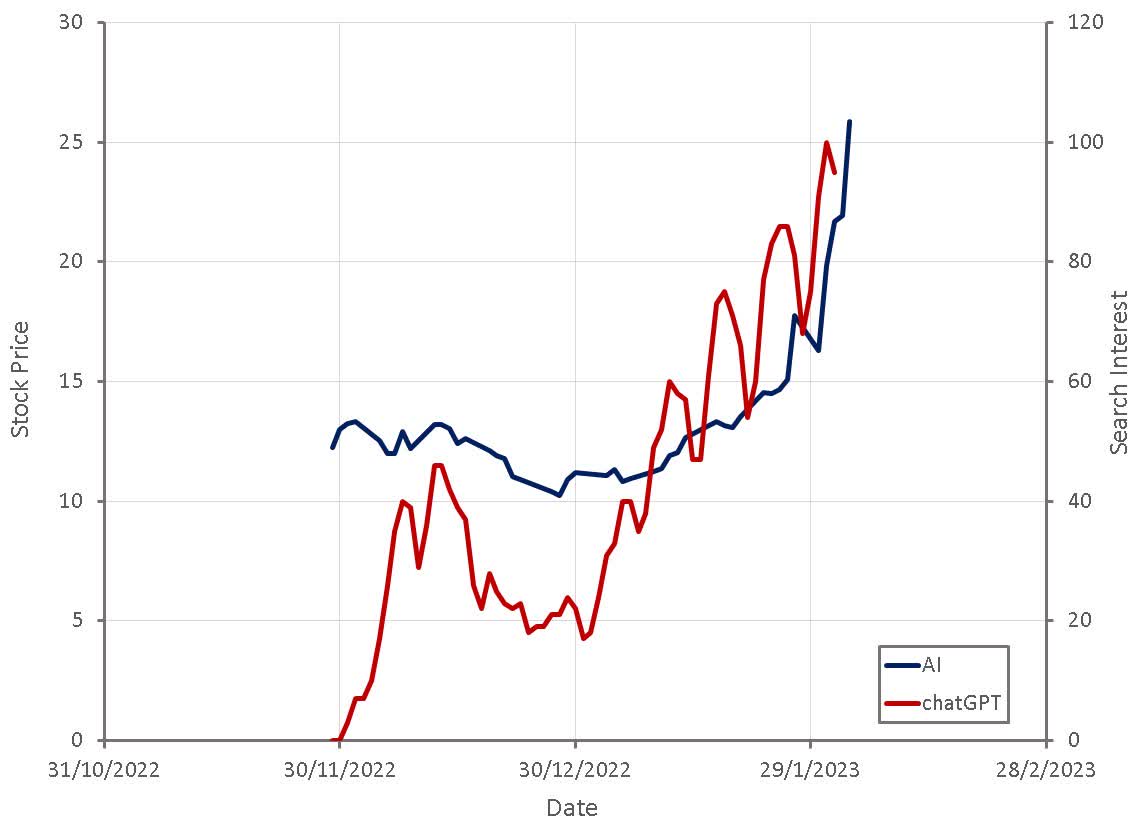

Recent movements in C3.ai’s share price appear to be largely driven by the hype around ChatGPT and the potential of large language models. Most of this is likely due to investor ignorance around artificial intelligence and what C3.ai actually does, and it is likely that C3.ai’s current stock price is primarily due to their AI ticker. ChatGPT has impressive capabilities, but those capabilities are being massively overrated by many. ChatGPT appears to optimize for plausibility rather than accuracy, and this plausibility can cause user complacency when assessing accuracy. Generative AI also appears to be a poor fit for C3.ai’s business, which has historically focused on IoT and predictive analytics use cases.

Figure 1: C3.ai Stock Price and ChatGPT Search Interest (source: Created by author using data from Google Trends and Yahoo Finance)

While there are clearly uses for ChatGPT, it will likely take time to work out where it is useful and where it is harmful. Even if models like ChatGPT find widespread adoption, it is not clear that viable businesses can be built on top of them. OpenAI / Microsoft (MSFT) will benefit from usage, although the willingness of users to pay versus the cost of delivering these services is unclear. A company building a UI on top of an API is likely to struggle with a large amount of competition and limited differentiation.

At the end of January 2023, C3.ai moved to capitalize on the generative AI hype, announcing the launch of a Generative AI Product Suite, with the first product being Generative AI for Enterprise Search. This is supposed to provide users with a natural language interface to locate relevant data from within an organization’s information systems, utilizing capabilities from models like ChatGPT and GPT-3. This appears to be a hastily thrown together product offering, with search deemed the best use of the technology in C3.ai’s business. Enterprise search tools already exist though, and they have been moving in the direction of semantic search, which helps to provide better results.

For example, Elastic (ESTC) is leveraging vector search in their enterprise search product. Vector search leverages machine learning to capture the meaning and context of unstructured data, including text and images, by transforming it into a vector representation. Vector search then finds similar data using approximate nearing neighbor algorithms. In comparison, traditional search relies on keywords, lexical similarity, and the frequency of word occurrences. Compared to traditional keyword search, vector search yields more relevant results and executes faster. While these types of tools may not allow users to interact with the search tool in a conversational style, they are more likely to provide reliable information.

C3.ai has a history of chasing trends to generate interest in the company and has no problem marketing itself aggressively. This is illustrated by a comment the CEO recently made at a conference:

Marc Benioff, a guy who I hired at Oracle, okay, out of USC, studied business administration, okay, and have never seen a computer in his life.

This statement was obviously meant to illustrate how experienced Siebel is, but given that Benioff actually founded a software company in high school and was an intern at Apple (AAPL) before joining Oracle (ORCL) , it sends a very different message to the one intended.

Financial Analysis

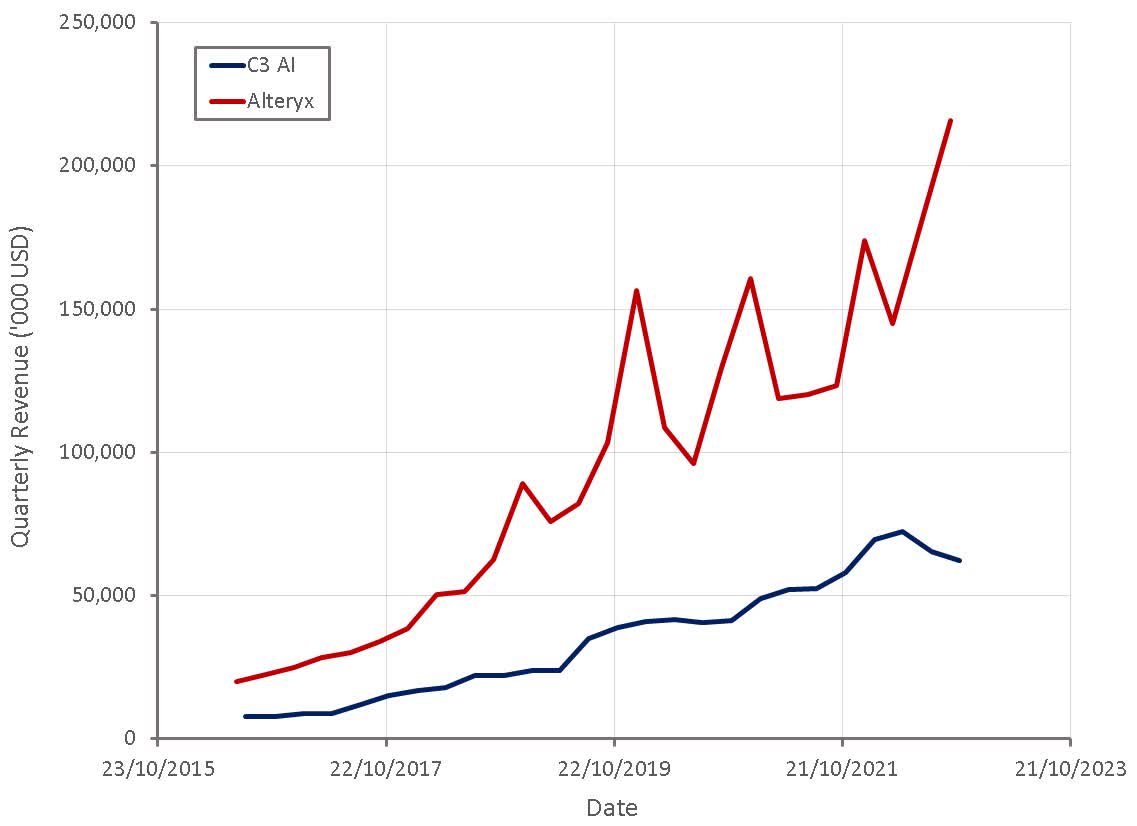

Given the macro headwinds hitting software markets at the moment and C3.ai’s shift in business model, there is considerable uncertainty regarding why the business is performing so poorly. C3.ai has been focused on landing enormous contracts with a handful of large organizations, which may have caused some deals to be delayed, but should have presented less difficulties than vendors focused on SMBs. Difficulties are certainly apparent in C3.ai’s financial performance, with revenue growth in the third quarter is expected to be approximately -8% YoY and for the full year approximately 4%.

The move to a consumption-based pricing model is expected to flatten the revenue curve in coming quarters, but by the second half of FY24, growth should begin to bounce back. The change in pricing model is revenue neutral over approximately three years, but is expected to increase C3.ai’s access to the broader market and accelerate customer acquisitions. C3.ai is not requiring existing customers to transition to the consumption model, and so far, haven’t seen customers switch. This should be helping to minimize temporary difficulties related to recognizing less upfront revenue.

Another concern for C3.ai is customer concentration, approximately 32% of subscription revenue comes from related parties, most of which is from Baker Hughes (BKR). If this relationship were to sour, or if C3.ai was to lose one of its other larger customers, it would have a material impact on the business.

For those that believe C3.ai has differentiated technology and a value proposition that appeals to customers, there is a purported 600 billion USD market opportunity that the company can capitalize on. This estimate is basically an order of magnitude larger than estimates from other companies operating in the same space though, and seems to be so broadly defined that it is meaningless.

C3.ai has also suggested that the market leader will have around a 50% market share, with number two having a 15% share, number three having a 10% share and the rest fighting for survival. While this type of share split may be accurate in some software segments, the analytics space is highly fragmented and there is no real reason to believe it will be a winner take most market. In addition, I would not count on C3.ai being one of the market leaders that actually capitalizes on the opportunity.

Figure 2: C3.ai Revenue (source: Created by author using data from company reports)

C3.ai completed 25 contracts in the second quarter, roughly a 100% increase YoY. This is encouraging, but the average contract value in the second quarter was only 800,000 USD, down from 19 million USD a year earlier. With the switch in pricing model, the number of prospects engaged within any quarter is expected to increase by an order of magnitude. C3.ai’s sales teams are currently actively co-selling to over 300 accounts globally. Bookings diversity continues to improve, with the Federal, aerospace and defense sectors performing well.

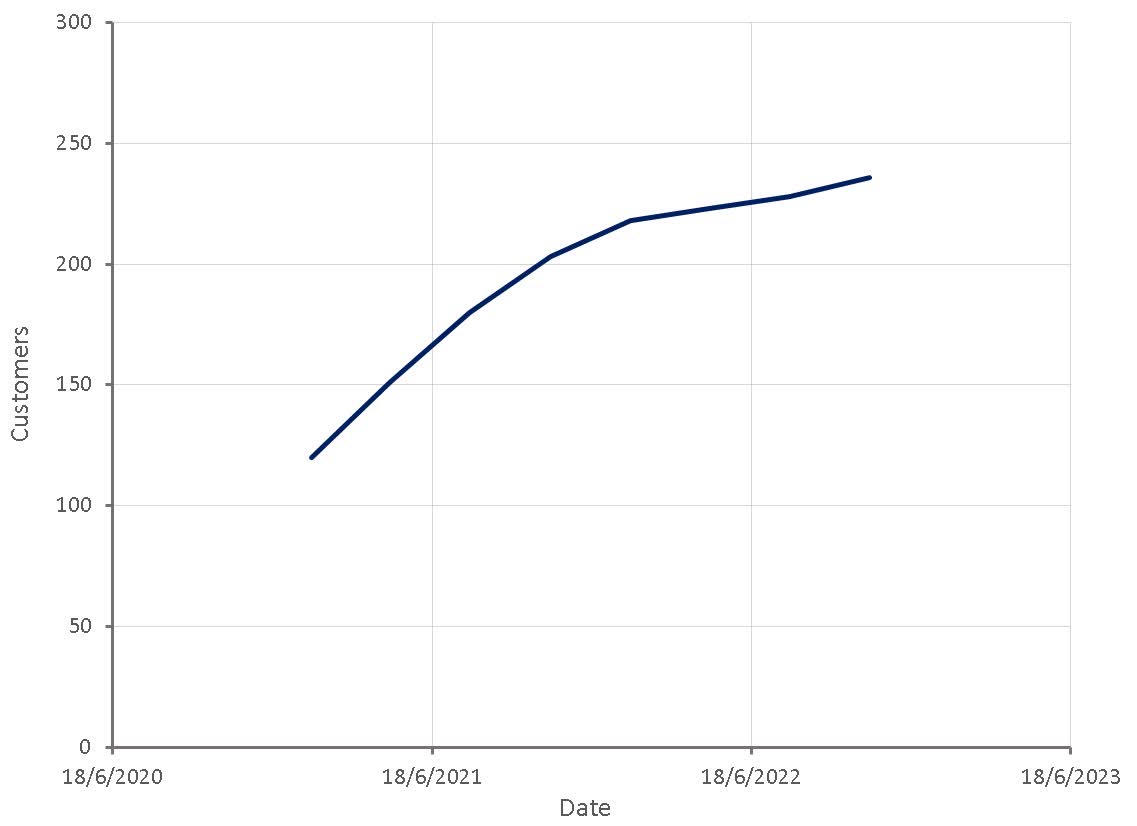

Figure 3: C3.ai Customers (source: Created by author using data from C3.ai)

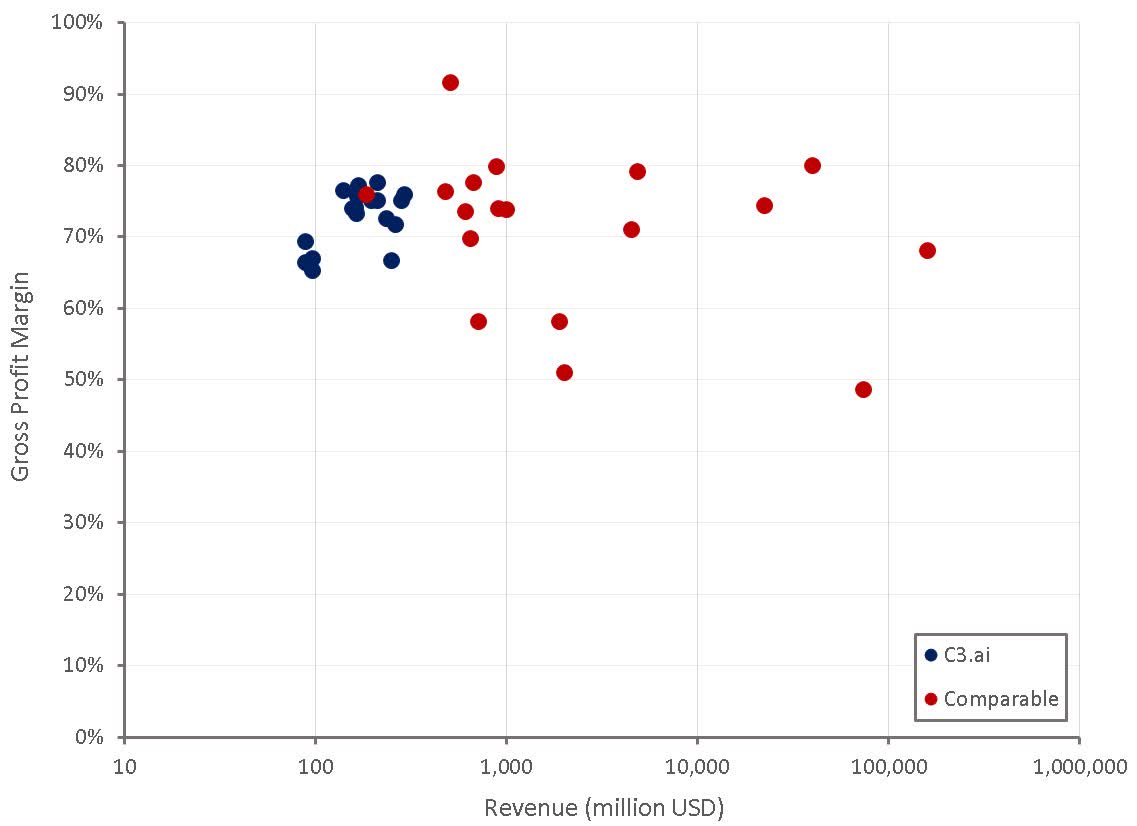

Gross profits have been declining due to a higher mix of trials and pilots, which carry a higher cost required to ensure customer success during this early phase of engagement. This trend is expected to continue in coming quarters as the proportion of revenue coming from pilots continues to increase. This hints at relatively high implementation costs and the service heavy nature of C3.ai’s business. Longer term C3.ai expects service revenue to be in the range of 10-20% of total revenue.

Figure 4: C3.ai Gross Profit Margins (source: Created by author using data from company reports)

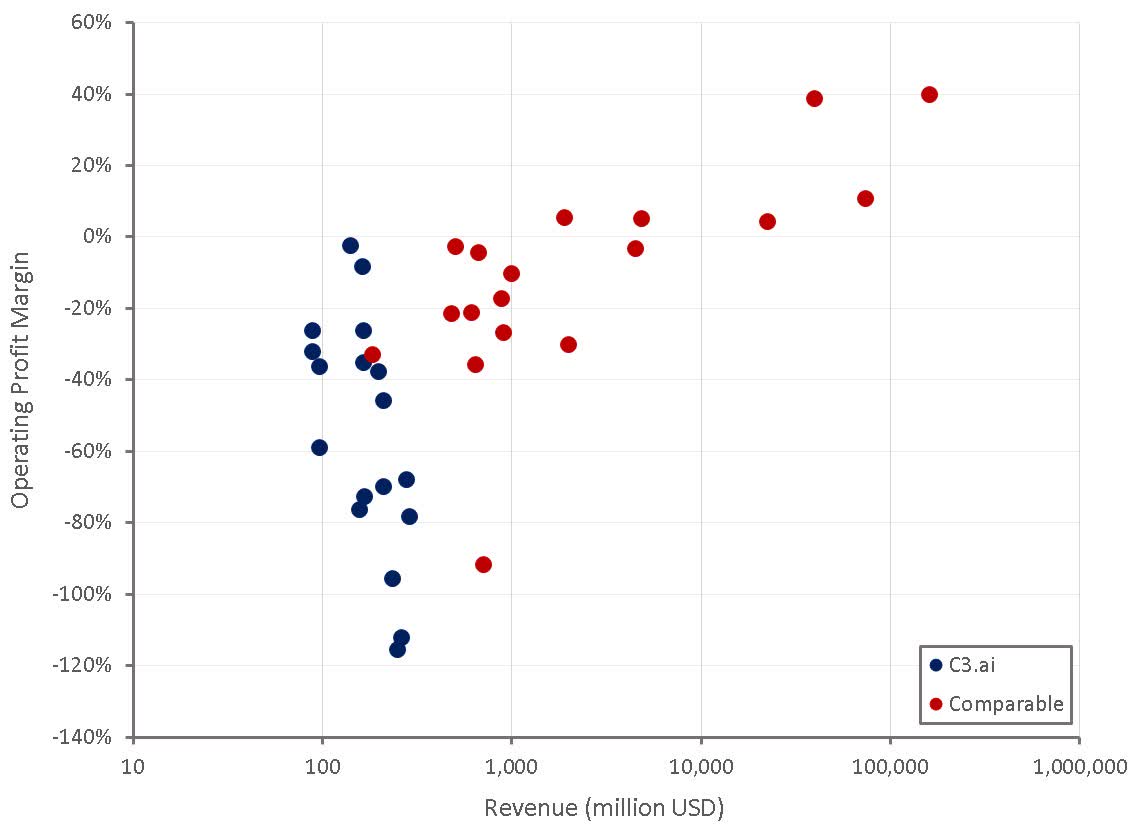

C3.ai’s operating profit margins have been extremely poor in recent quarters, some of which can be blamed on the switch in pricing model and heavy investments in their sales force. Given C3.ai’s high gross margins, 10+ year history, 1+ billion USD R&D investment in the platform, small number of customers and high contract values, the company should be a lot more profitable than they are.

Figure 5: C3.ai Operating Profit Margins (source: Created by author using data from company reports)

Operating losses are acceptable if they are efficiently generating growth in revenue that is likely to be sticky, but this is questionable for C3.ai. Last year, C3.ai’s marketing and branding spend was reportedly 29% of revenue. This seems unusual for an enterprise focused company that is likely to be more reliant on developing close relationships with potential customers than building brand awareness.

C3.ai is also still spending 46% of revenue on R&D, despite supposedly already investing over 1 billion USD in the platform and having the leading solution on the market. This may be due to the company’s focus on building industry specific turnkey applications, but this would suggest that high R&D costs are a structural feature of the business. Management believes that C3.ai will eventually be a 20% operating margin business, but this will depend on their competitive position and ability to retain customers.

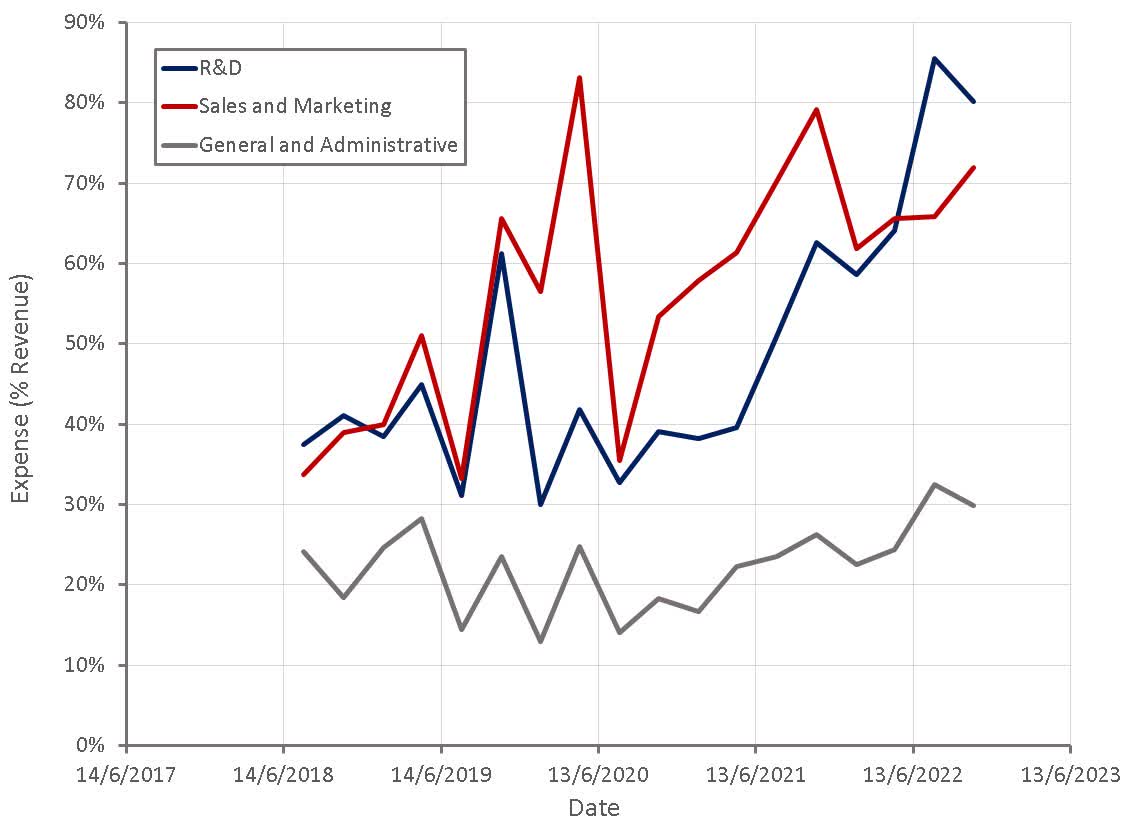

Figure 6: C3.ai Operating Expenses (source: Created by author using data from C3.ai)

Stock-based compensation as a percentage of sales is currently around 85%, which has been blamed on the vagaries of GAAP accounting. SBC expenses will come down, and the accounting cost is not really relevant to investors, but this does not mean that SBC is not a problem. Shareholders are currently being heavily diluted, and even if the company is successful, this level of dilution undermines the investment case to a large extent.

Table 1: C3.ai Share Count (source: Created by author using data from C3.ai)

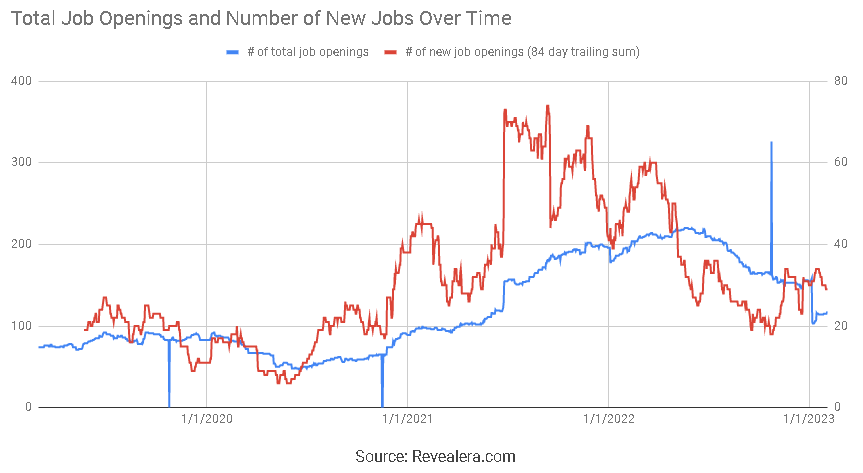

C3.ai now employees around 900 people, and continues to hire engineers, data scientists and sales professionals. The pace of hiring has moderated significantly over the past 12 months, which should help to contain growth in operating expenses going forward.

Figure 7: C3.ai Job Openings (source: Revealera.com)

Valuation

In March 2022 C3.ai repurchased approximately 0.7 million shares for 15 million USD (average price of approximately 21 USD per share). This could suggest that management believes that the stock is undervalued at this level. Given that the company had authorization to repurchase an additional 85 million USD worth of stock, and failed to do so at far lower prices, this is not clear though.

While C3.ai may not be trading on a particularly high revenue multiple, there are a number of peer SaaS companies with better prospects and lower valuations. Given highly uncertain growth and profitability prospects, it is difficult to value C3.ai, but based on a discounted cash flow analysis, a share price closer to 14 USD seems more reasonable. C3.ai’s stock price is currently divorced from fundamentals and near-term returns are more likely to be driven to the stock’s meme status.

Be the first to comment