Antagain

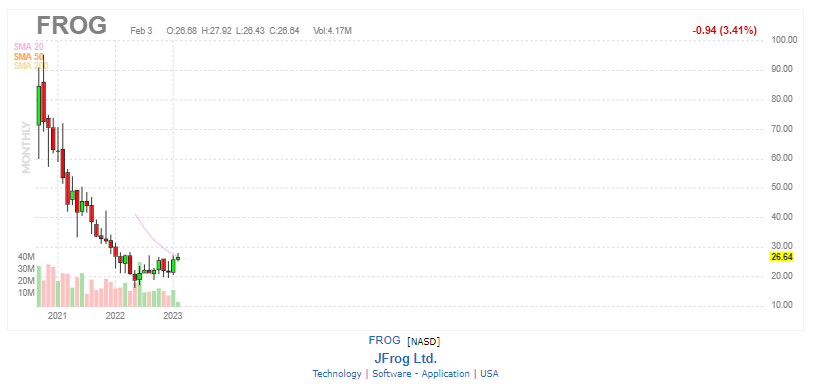

Looking across the cloud, I’ve seen JFrog (NASDAQ:FROG) come up on a number of occasions as an interesting name to consider. The company is relatively new to the scene, going public in September of 2020, right in the middle of the cloud explosion during the post-COVID tech bubble.

Finviz

The stock went gangbusters for a short time, peaking in the mid-$90’s per share before cratering into the end of last year. The company has seen some consolidation and bottoming, and maybe the dust has settled a little. Some of the B2B cloud companies can be a little dense to discuss, so I’ll include a little snippet from their S-1 here to discuss what they do:

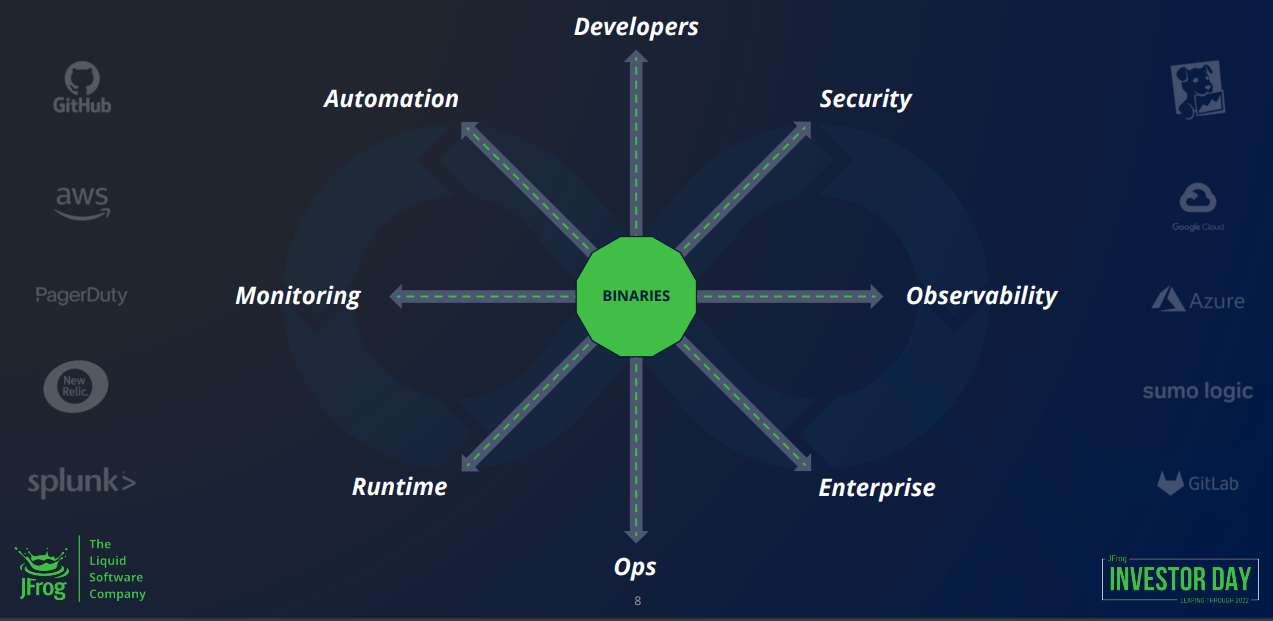

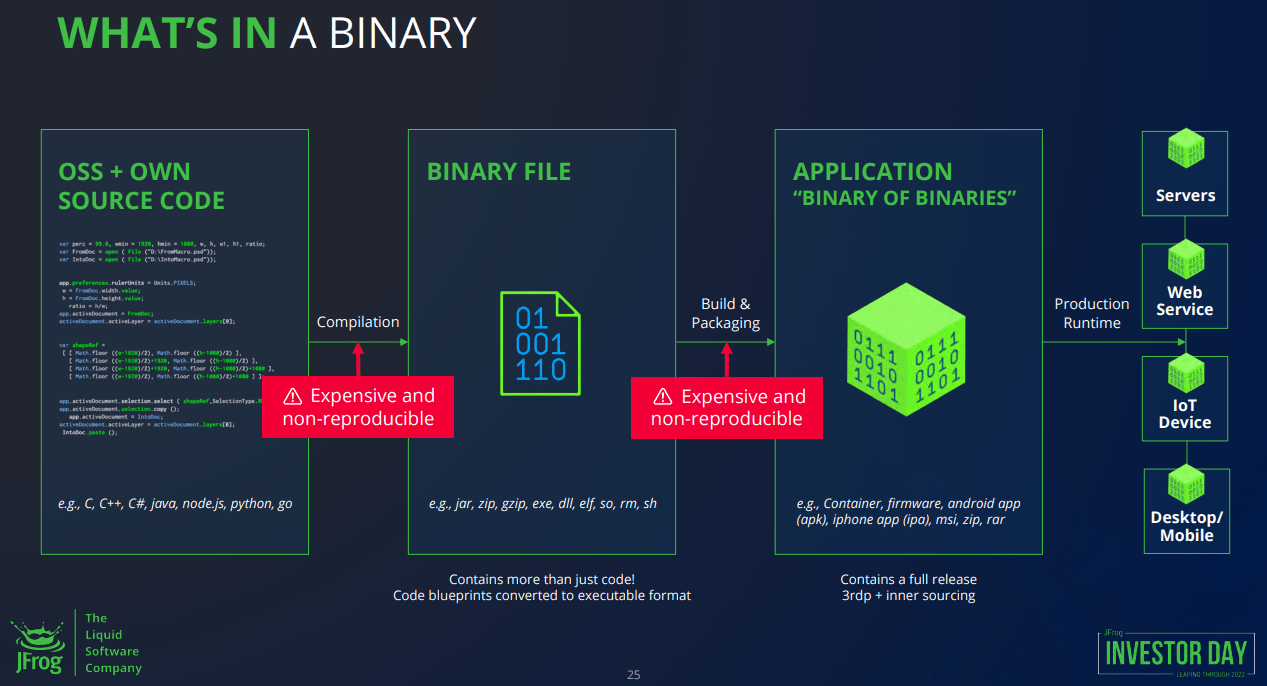

While many software development technologies today address aspects of a particular segment of DevOps, CSRM [continuous software release management], enabled by JFrog, provides the common ground for software developers and IT operators, making it integral to the DevOps workflow. Software as it is written by a developer, in source code, cannot be deployed in a runtime environment. In order for software to run in production, source code is transformed into executable binary files that can be understood by and run on a server or device. Organizations need tools that can turn source code into binary files, store and manage these binaries, and then create software packages, or combinations of one or more binary files, that can be released and deployed to runtime environments. Our platform is designed to manage and deploy all types of software packages within an organization, making it the system of record for an organization’s software, and is often called the “database of DevOps.”

Company Presentation

So, in a nutshell, FROG is offering a repository, or in their product name, an Artifactory, where source code is stored in a usable format, called binaries, for scanning and ultimate deployment to all the end use-cases. These can be as disparate as internet of things devices, cars, airplanes, computers, mobile devices, etc. In the process, the company provides security architecture for monitoring and the source code is never involved. The ultimate goal of this is a bad actor can only impact one device receiving the software from FROG, which is identified and can be quickly remedied.

Company Presentation

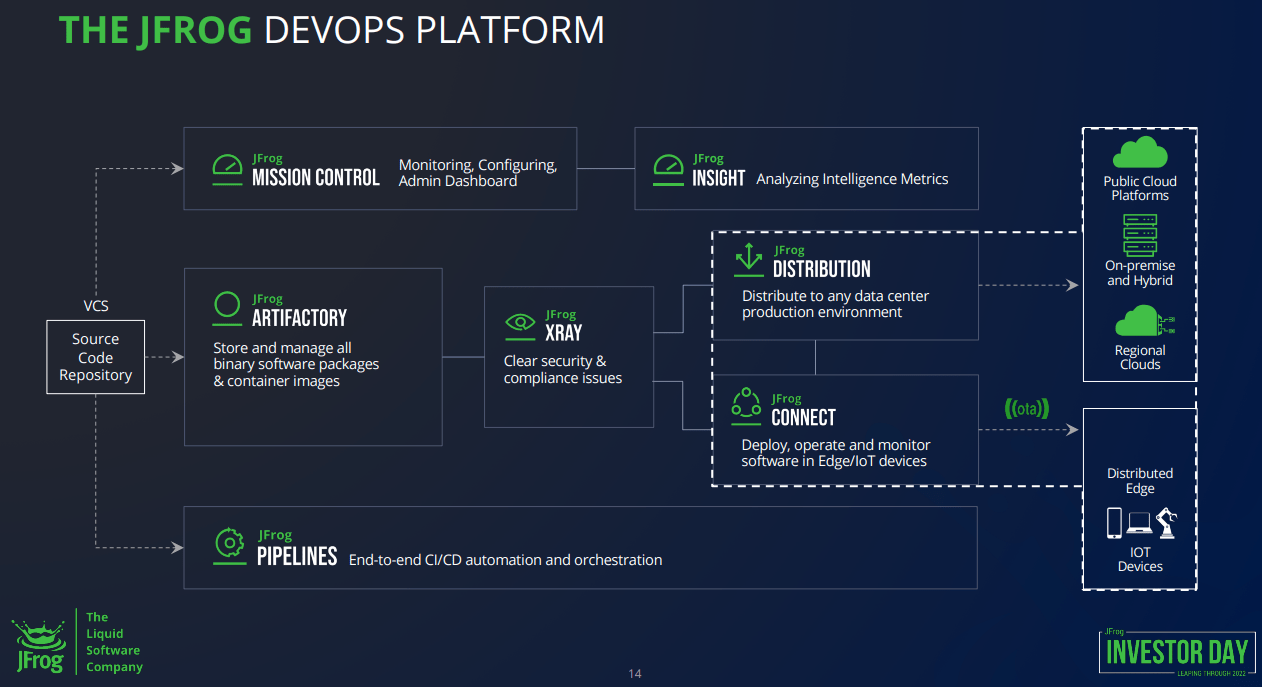

In practice, this is all very complicated, but the use case is much easier. The company gives a ton of good examples in their IR materials, and one of the best ones to think about is car manufacturers. Newer cars are running company software and often require updates. However, rather than wait for a customer to bring a car into a dealership for an important safety-related update, FROG would be used to instantly ship the update out without ever losing operability of the car. This is why the company often discusses ‘liquid software’, where there are no version numbers or long waits for software updates. Effectively, once the code is ready, the company’s products can be used to start rolling it out and maintaining one singular, “true” version across the entire software supply chain.

Company Presentation

The model has worked well for the company. FROG has continued to expand its offerings and roll out additional tiers and updates to its core Artifactory product. The company currently boasts 696 customers over $100K ARR, 18 customers over $1M ARR, and has driven strong growth since IPO. 39% of new customers have opted for the Enterprise Plus software tier, which includes all the extra offerings and leads to higher spend for each win, and the company’s gross margin looks fantastic at 84%, which is one of the main reasons to love software as an investor. On the most recent quarter, FROG drove 34% revenue growth and a net revenue retention rate of 130%, which is top tier among cloud providers. One of the use cases discussed by the CEO in the earnings call:

In Q3, one of the world’s top 3 largest automobile manufacturers joined JFrog as a new customer — this multimillion dollar deal that was completed in partnership with cloud marketplace included a full adoption of the JFrog platform and notably originated through community efforts around Konan. JFrog opens our Clas package manager, preferred by many automotive and IoT groups.

These customers look at DevOps and deep SaaS solution that can scale and centralize global development. They emphasize the need for binary management, universality, security and distribution, which was perfectly aligned with the JFrog solution. They migrated from Sonopet Nexus to the JFrog platform looking to standardize on the cloud and evolve during the era of electric vehicles.

Company Presentation

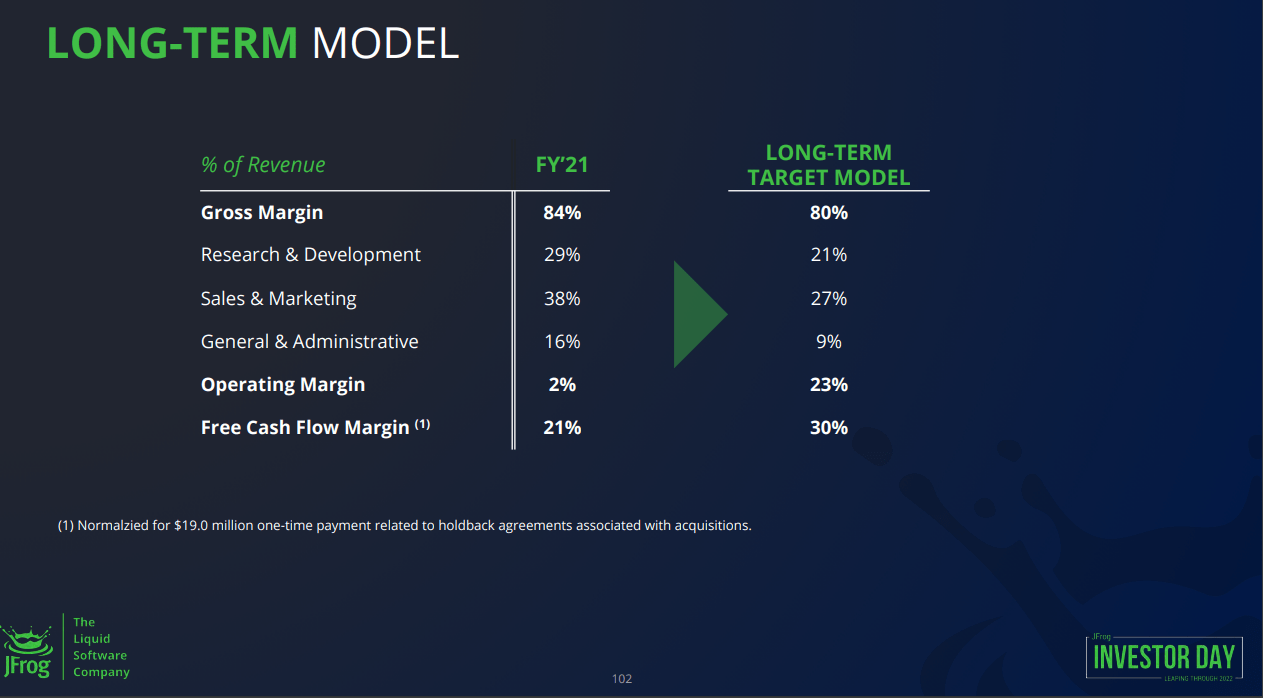

Looking at the longer term projections from management, they are obviously looking for significant operating margin expansion. The company expects to break-even for the first time this year, and investors should look for some significant growth in profitability from the company as they continue to scale. The model is out there with other cloud providers, and generally a lack of expense management is a good reason to stay away if these companies can’t grow profitably.

Management has projected for R&D, S&M, and G&A costs to come down materially as a percentage of revenues, which could just as easily be based on revenues growing faster than expenses versus any actual cost-cutting, which should help fuel that significant increase in operating margin.

Although the above slide is useful, management declined to provide any 2023 guidance on the most recent call, so there is no useful timeline for the company to reach any of these figures.

Clouded Judgement Substack

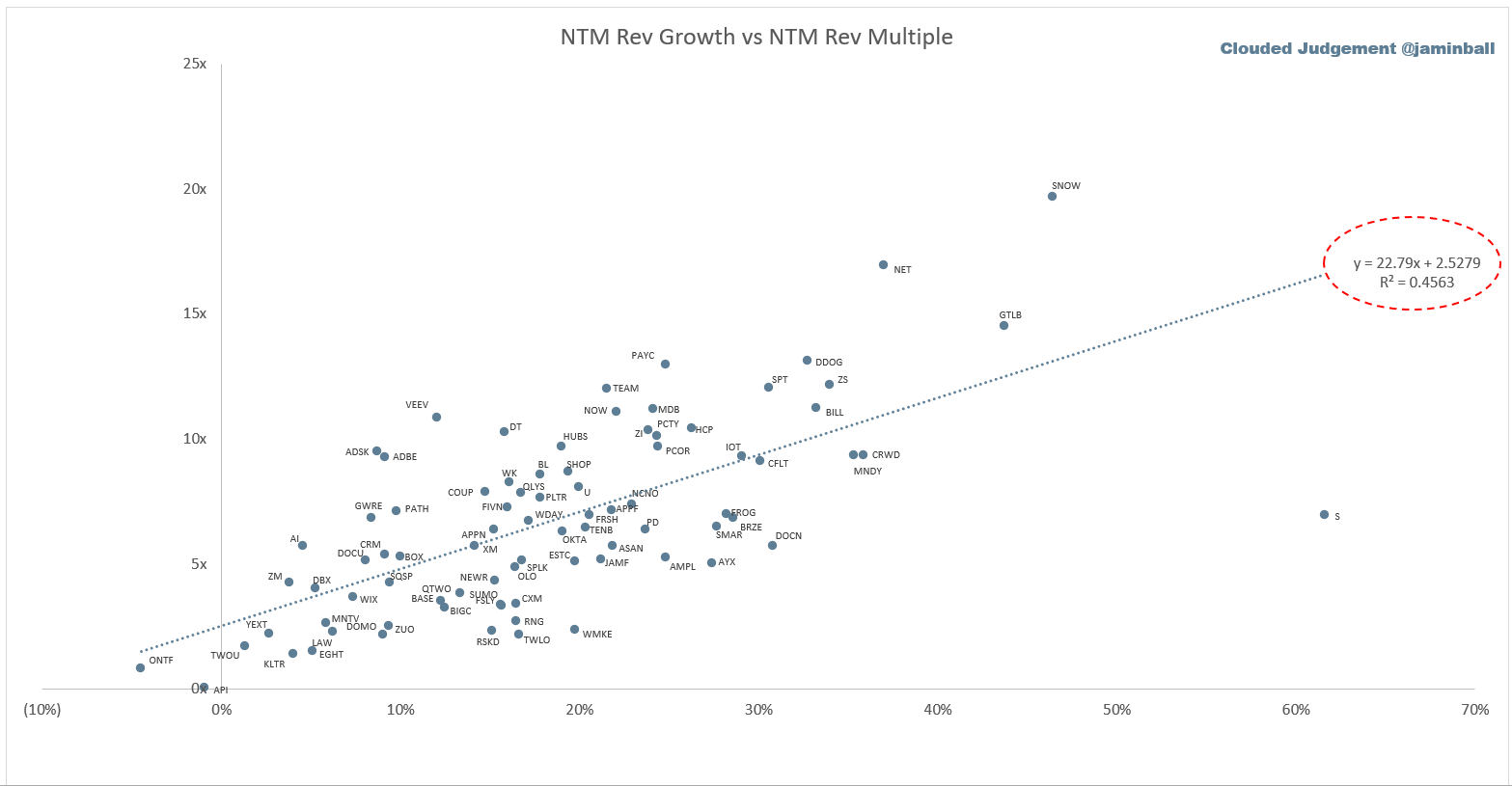

Looking at the graph above, the various cloud providers are shown on a sliding scale of valuation on the y-axis as a multiple of sales, and revenue growth rates on the x-axis. It can be a useful way to see how companies line up against peers. FROG is relatively cheaper than the average for its growth rates, which are relatively in-line with a company I recently covered, Paycom Software (NYSE:PAYC). However, the operating metrics of the 2 companies could hardly be more different the second you look away from revenue growth, which paints an easy picture of why there’s a valuation gap.

Clouded Judgement Substack

Looking at some other key metrics, and of course the first one that stands out to me is my least favorite. Stock-based compensation came in at 24% of revenues. This is right around the mean across the sector, and FROG’s actual $ amount of revenues are low compared to some of the companies I’ve covered, but it still isn’t ideal. It shouldn’t be a surprise at this point, but be ready for some dilution as a shareholder in FROG, and this will be something I keep an eye on as the company scales to see if they continue diluting the share base.

Outside of that, the only other thing worth noting that I haven’t covered already is the company’s Rule of 40, or revenue growth added to EBITDA margin, which sits at a comfortable 49%.

FROG has a lot of potential. The company’s use case is a strong one, and the revenue growth and customer count show it. There’s a few things I want to see before entering a full position. I’d like to see the company execute on its claims this next year and achieve a semblance of profitability. It’s possible, as expense growth slowed to at least not outpace revenue growth this past year. I’d like to see SBC slow down as revenues grow and the company brings on more employees. Lastly, I want to see the number of customers over $1M ARR start to grow. FROG is in a pond with a number of big tech companies likely eyeing the same $50B opportunity. As the company scales its offerings, strong future growth will come from increasing spend as much as it does from new customers. I have a starter position open coming off what looks like a pretty hard bottom for the stock, and I’m rating it as a hold. I’ll update after the next earnings announcement.

Be the first to comment