z1b

The market (SPY; VNQ) has rallied over the past weeks.

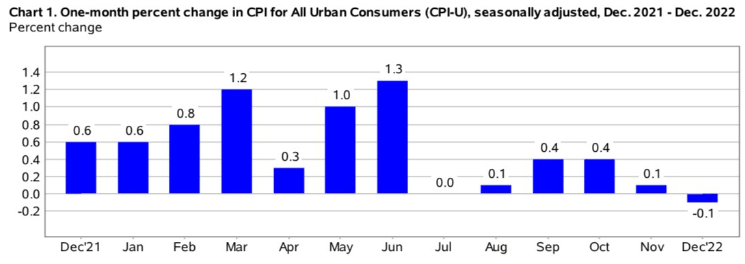

It rallied because last month’s consumer price index came in at -0.1%.

If you now annualize the consumer price index of the last 6 months, you get a 1.8% inflation rate:

Federal Reserve

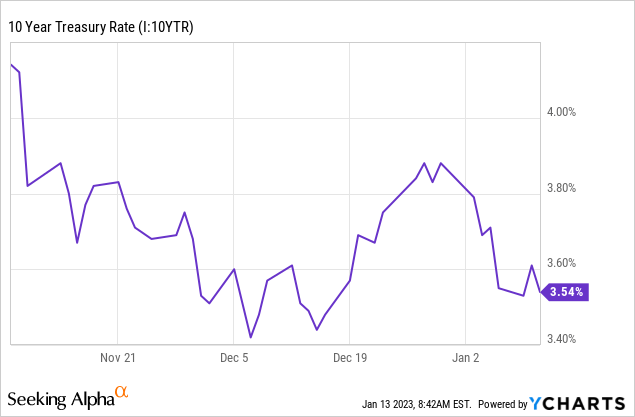

The market collapsed in 2022 because the high inflation forced the Fed to hike interest rates, but the inflation now appears to have been brought back under control, so this would suggest that interest rates would now also start to return to lower levels. This is at least what the bond market has begun to price:

YCHARTS

It will probably take some time for the Fed to cut rates because it wants to be 110% sure that we have inflation under control, but eventually as we enter a recession, I expect rates to be cut again as the Fed turns to stimulate the economy in hopes of avoiding a hard landing.

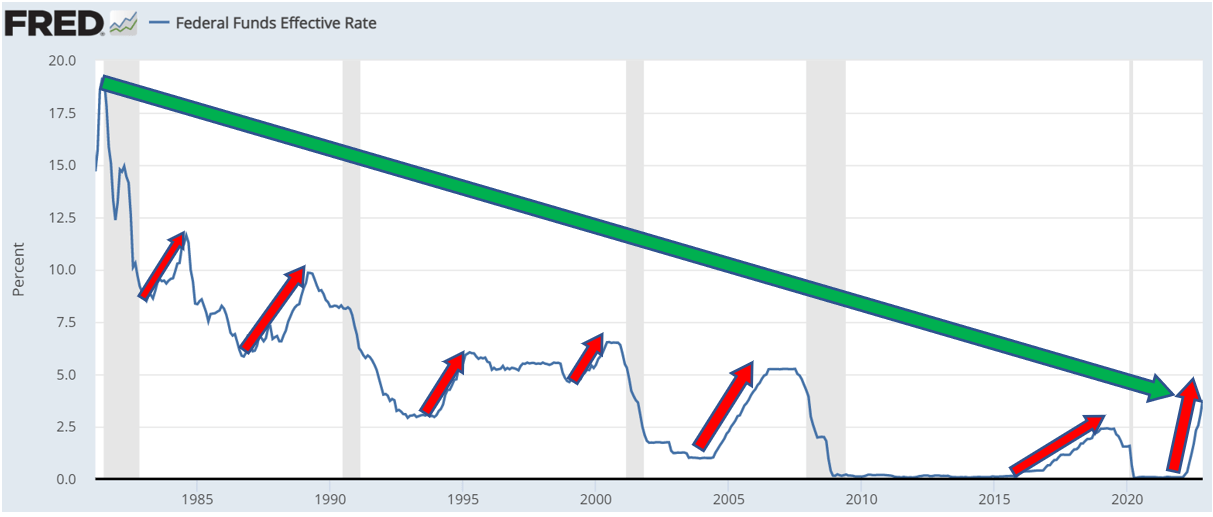

If you look at the past 40 years, we have seen this play out many times. We get occasional surges in interest rates, but shortly after, rates are cut significantly and end up lower than ever:

Federal Reserve

If you look at the past 40 years, we have seen this play out many times. We get occasional surges in interest rates, but shortly after, rates are cut significantly and end up lower than ever:

What REIT will benefit the most from this?

I believe that there are a few types of REITs that stand to benefit the most.

These are those REITs that:

- Own long-duration assets like triple net leases or ground leases

- Own low cap rate assets and are priced for cap rate expansion

- Have heavily leveraged balance sheets

Below we highlight a few REITs that could present significant upside potential as long-term rates return to lower levels:

iStar (STAR) & Safehold (SAFE)

I believe that iStar and Safehold, which will soon become one company as they merge together, will benefit a lot from lower interest rates.

They specialize in ground leases, which are incredibly sensitive to interest rates due to their ultra-long duration. You can learn more about ground lease investments by watching the video below:

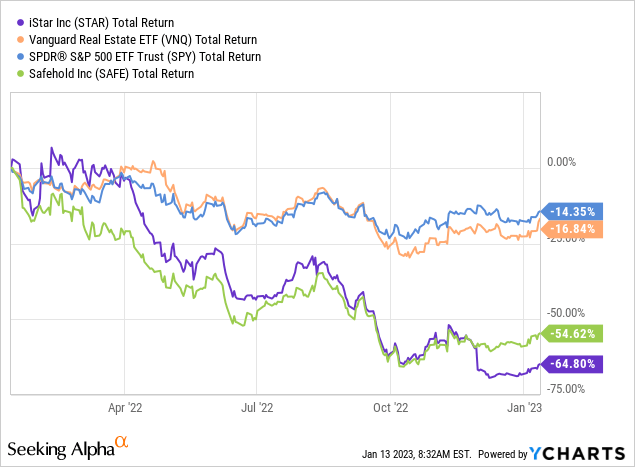

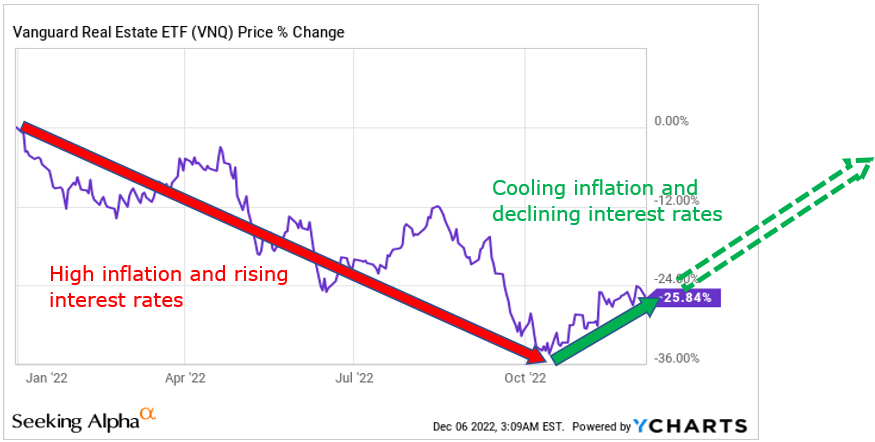

The news of lower inflation caused STAR’s share price to surge, but it remains down very significantly over the past year when compared to the rest of the market:

YCHARTS

The underlying businesses kept performing just fine in 2022, but their share price collapsed because of the high inflation and the surge in interest rates

Therefore, simple logic would tell you that a return to lower inflation and lower interest rates would be a very significant tailwind for the market sentiment of the company:

YCHARTS

All REITs will benefit from this, but STAR and SAFE are poised to rise the most because ground leases are the most sensitive to interest rates of all commercial properties.

To recover to where it was at its peak, the company’s share price would need to roughly double, but the company has also created a lot of value since then so theoretically, it would need to rise even higher to return to the same valuation. We expect 70%+ upside.

BSR REIT ([[HOM.U:CA]] / OTCPK:BSRTF)

BSR is another REIT that should benefit a lot. It is an apartment REIT that owns properties mainly in the Texan triangle (Austin, Dallas, and Houston) and it is priced at a 35% discount to its net asset value, despite growing its same property NOI by nearly 10% in the last quarter.

BSR REIT

It is priced so cheaply because these are low cap rate assets and the market fears that the recent surge in interest rates will cause the cap rates of its assets to rise, and its NAV per share to decline.

So the market priced it at a 35% discount, expecting a significant drop in its NAV, but this appears unlikely to us.

The bond market is already starting to price lower interest rates and the type of investors who buy these properties are long-term oriented. Sure, cap rates may expand a bit, but rents are also growing rapidly, which compensates for the cap rate expansion. Moreover, the company is also actively buying back shares, creating value for shareholders.

I suspect that as interest rates return to lower levels, BSR’s share price will rapidly recover. You are today buying shares at $14, but the latest NAV is $22.35, and you earn a near 4% dividend yield while you wait for the recovery.

This is quite exceptional when you consider the assets that we are talking about. We are not talking about Class B office buildings here. We are talking about rapidly growing apartment communities that are located in the famous Texas triangle: Austin, Dallas, and Houston.

We believe that BSR has about 50% upside and we expect to earn double-digit total returns from the near 4% yield and the growth while we wait.

Finally, DIC Asset could also benefit significantly from lower interest rates because it is heavily leveraged.

DIC is our second-largest German real estate investment at High Yield Landlord. It is a higher risk / higher (potential) reward type of investment because it uses more leverage than average and invests mainly in industrial and office buildings.

It also runs an asset management business, which is growing nicely, but its earnings are more cyclical since it will earn lower transaction and incentives fees during the tough years.

DIC Asset

The market is pricing DIC at a deeply discounted valuation because its loan-to-value is high in this environment at around 55% and its refinancing rates would be materially higher than its current cost of debt.

Understandably, it worries the market.

But here’s the important context that the market appears to be missing.

DIC just recently closed a massive deal, buying VIB Vermögen, a large industrial portfolio that increased its leverage. The increase in leverage is temporary and it will now be worked back down as DIC sells some assets and structures JVs to start earning interest income. The higher leverage level was never intended to be permanent, although DIC got very unlucky with the timing of this deal.

DIC is not a traditional REIT. It is an asset management firm and so it is in the business of creating funds, raising capital from institutional investors, and then earning fees for managing it all.

Some of the assets that DIC acquired as part of the VIB transaction can now be used to structure such funds, raise equity and pay some of that debt to reduce risk. DIC made this clear in a recent statement:

“The thing that has made DIC Asset unique and strong for many years is its innovative business model comprising two pillars: portfolio properties owned by the Company and management of properties for institutional investors. This model has evolved into a success factor, safeguarding the reputation of DIC Asset AG in the market. No other company is able to make attractive assets available for institutional investments as fast as we can… This two-pillar model will now be applied to VIB Vermögen AG as well. Going forward, we will also increasingly use it to operate a platform for logistics properties. Here, too, we guarantee our tenants and investors high availability of prime properties. And we guarantee our shareholders a stable cash flow. Our product pipeline here is well filled – several new funds are currently being launched.“

The industrial property market remains exceptionally strong in Europe and most of these assets happen to be located in strong, highly desirable markets of Southern Germany that are experiencing rapid rent growth.

I contacted DIC’s investor relations and they confirmed that they plan to sell some of these assets to pay off debt:

“Yes, indeed, disposals are part of our plannings to refinance existing debt in addition to the available liquidity we have to payback maturities in 2023 ff.”

So that’s an important context to consider. Moreover, most of the debt won’t mature for years to come, leaving ample time for the market conditions to stabilize. By then, rents will also have risen for these industrial assets, which now represent the largest chunk of DIC’s portfolio, and interest rates will likely have come back down to lower levels.

So yes, debt is high and it presents risks, but I think that with this context in mind, the risks are not as great as what’s implied by the market.

DIC’s NAV per share is nearly €25 and you can today buy shares at just €8.8, representing a 65% discount to NAV. Put differently, you get to buy these assets at 35 cents on the dollar, and I also want to remind you that prior to this crisis, DIC was a rapidly growing asset management company.

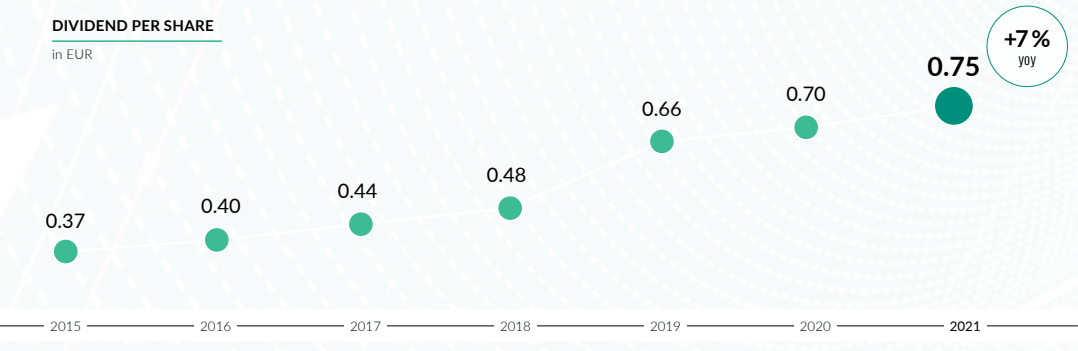

Its assets under management have more than tripled since 2017 and a lot of this is external capital that earns them fees. This has allowed them to more than double their dividend since 2015:

DIC Asset

There is elevated risk right now, but overall, this is a strong company with rapid growth prospects, and its steep discount to NAV won’t make any sense in a few years from now if they can get through this crisis (which we think that they will).

Even if the share price doubled, they would still trade at a relatively large discount to NAV. Today, the dividend yield is 8% and it is easily covered by cash flow, but we would actually welcome a cut if it allowed them to accelerate the deleveraging and push for some more buybacks.

Bottom Line

Many REITs are currently priced at huge discounts as if interest rates would remain high for a very long time to come. But the bond market is already starting to price lower rates, which makes sense given that inflation is now getting back under control, and the Fed will likely need to stimulate the economy in a future recession.

Historically, rate hikes are rapidly followed by rate cuts and this time probably won’t be different.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment