Prostock-Studio/iStock via Getty Images

Omega Healthcare Investors (NYSE:OHI) has been a battleground REIT for many investors, with bulls and bears making their cases on each side, and sometimes, with opinions changing back and forth.

The stock is now well off its near-term high of $32 achieved in November, with recent news pressuring the stock, while many other REITs have seen a decent bounce over the past 30 days. In this article, I highlight why now remains a good opportunity to pick up this 9.2% yield while market sentiment is working against it.

Why OHI?

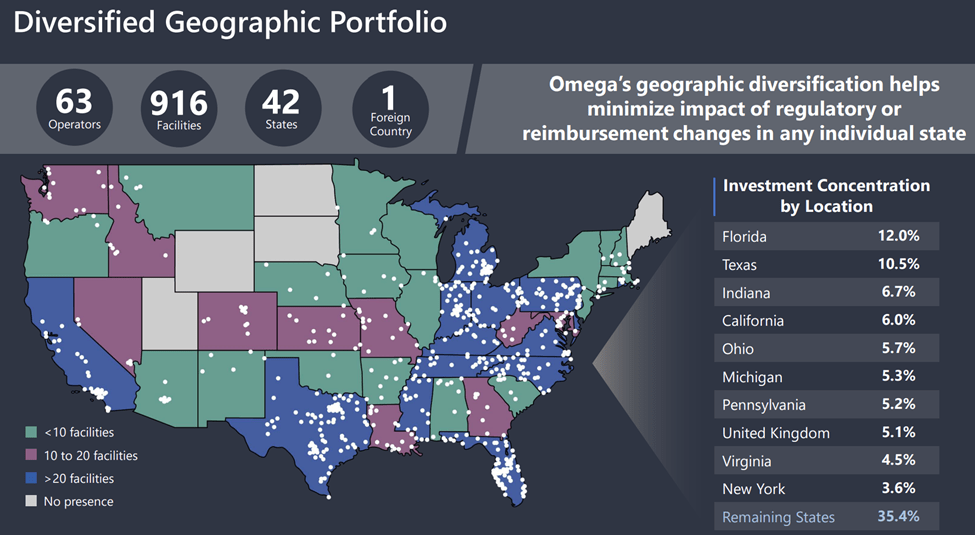

Omega Healthcare Investors is the largest publicly-traded owner of skilled nursing facilities. It has a long track record of 30 years as a public company and at present, has 916 properties spread across the US and UK, comprising 92K beds and leased to 63 operators. It’s also geographically diversified with exposure to nearly every U.S. region, and its top 3 states are Florida, Texas, and Indiana.

OHI Locations (Investor Presentation)

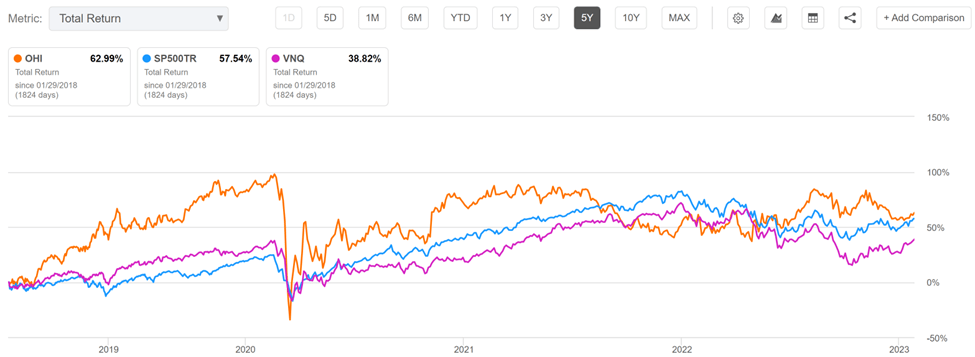

I like to think of OHI as being the “big tobacco” of REITs, as negative market sentiment pops up every now and then, and has perpetually kept its share price from rising too high. This, combined with a steady and high dividend yield and the essential nature of its properties, has produced market-beating returns. As shown below, OHI’s total return of 63% over the trailing 5 years has beaten that of the S&P 500 (SPY) and Vanguard Real Estate ETF (VNQ).

OHI Total Return (Seeking Alpha)

OHI may have spooked some investors with a recent announcement on January 9th that it expects EBITDA and FAD (funds available for distribution) to be sequentially lower in Q1 than Q4 of last year, driven by issues related to some operators’ ability to pay rent and mortgage obligations on time. As such, management believes that the leverage and dividend payout ratios will be higher than historical range.

However, dividend investors can put their minds to ease at least in the near term, as OHI declared a $0.67 dividend, which is in-line with previous, on January 26th with an ex-dividend date of February 3rd. Management also continues to believe that both its dividend payout and leverage ratio will return to its historical range upon resolution of operator issues.

Looking forward, I believe this can be reasonably achieved, as inflation is easing. That could mitigate wage inflation concerns at many of OHI’s operators, which have plagued their margins and rent coverage. Plus, operators should see some relief this year, as a Medicare rate increase of 2.7% was implemented last October, and many states have recently implemented strong Medicaid rate increases.

Moreover, a tight labor market kept occupancy levels at below average rates, and there are signs that this is easing. This helped OHI to see continued increases in occupancy during the second half of last year. Notably, Agemo, which is one of OHI’s largest operators, is scheduled to resume paying rent in the second quarter.

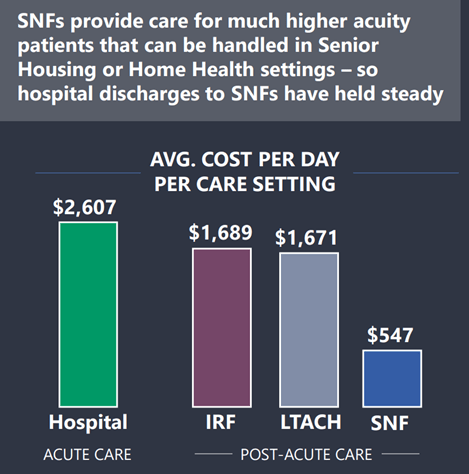

While I expect operator restructuring to remain as an overhang for the stock in the near term, the long-term thesis should remain intact. This is considering that skilled nursing facilities remain the lowest cost of care setting amongst other patient options.

SNF Cost Comparison (Investor Presentation)

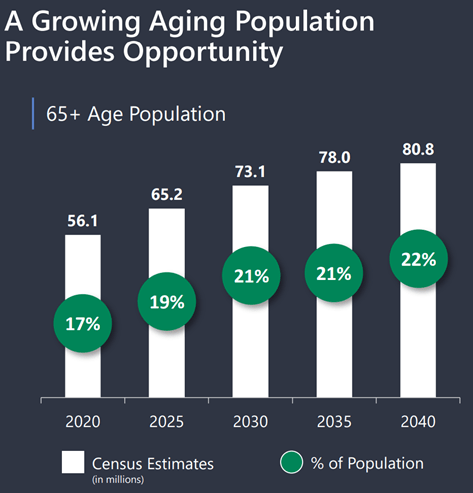

Plus, while most people would prefer home healthcare, it’s simply not realistic in most cases, and hence why hospital discharges to SNFs have remained steady. It also shouldn’t be ignored that the U.S. remains on the cusp of an aging baby boomer population, with the 65+ age cohort expected to grow significantly over the next 2 decades, as shown below.

Age 65+ Cohort Growth (Investor Presentation)

Lastly, this isn’t management’s first rodeo, as they seen the company through trying times before. This is reflected by the nature of leases, which are triple-net, resulting in higher margins due to the tenant being responsible for paying property maintenance, insurance, and tax. 97% of OHI’s revenues are tied to master leases, making it less likely for a tenant to “hand over the keys” on any single property, and 95% of revenues are tied to fixed-rate escalators at an average 2.3% weighted average escalator.

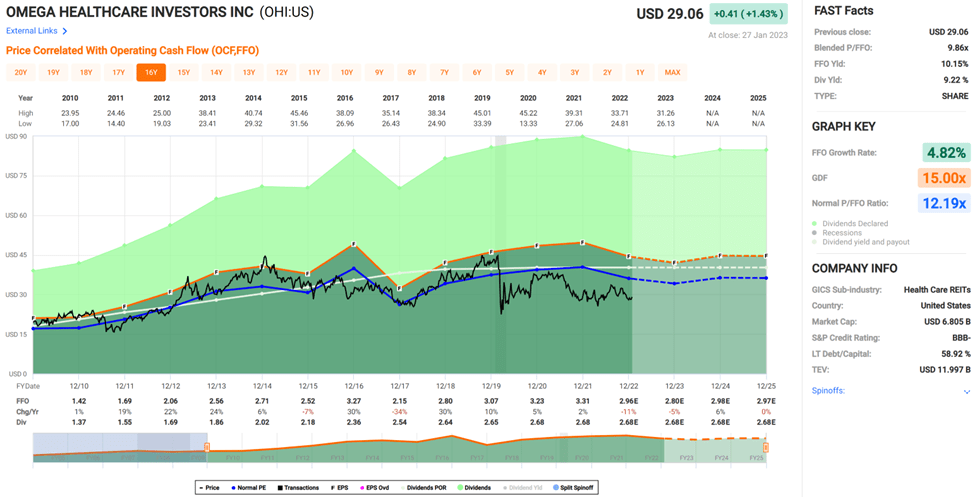

Turning to valuation, OHI is currently in value territory at the price of $29 with a forward P/FFO of 10.0, sitting meaningfully below its normal P/FFO of 12.2. Would I be interested in OHI at present at $35 per share? No, I would not. But given that present challenges appear to be baked into the current share price, I believe it’s worth a shot at present. Analysts have an average price target of $29.77, which could still translate into a near-term total return in the low-teens including the dividend.

OHI Valuation (FAST Graphs)

Investor Takeaway

Omega Healthcare Investors has seen share price underperformance as of late, driven by operator issues and rent coverage concerns. While these may remain an overhang in the near term, I believe that first half 2023 should represent a trough for these concerns, with potential for a rebound in the second half of the year.

Moreover, increases to Medicare and state Medicaid reimbursement rates should help with operator profitability in the near term, and the long-term thesis should be intact. Lastly, it appears that headwinds have already been baked into the share price, and management has telegraphed their intention to keep the dividend in-line with the recent dividend declaration. As such, I find OHI to be a high-yielding Buy for risk tolerant investors in a diversified portfolio.

Be the first to comment