ipopba

Introduction

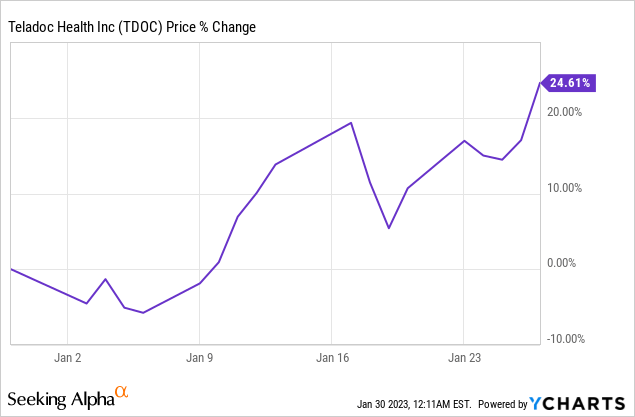

After hitting its peak in early 2021 (along with many other high-growth tech names), Teladoc’s (NYSE:TDOC) stock has undergone a spectacular crash. The COVID-19 pandemic and easy money policies from central banks propelled telehealth stocks to incredible levels, and a reversal in these drivers has led to a sharp crash in this sector. However, Teladoc’s stock is off to a flying start in the new year:

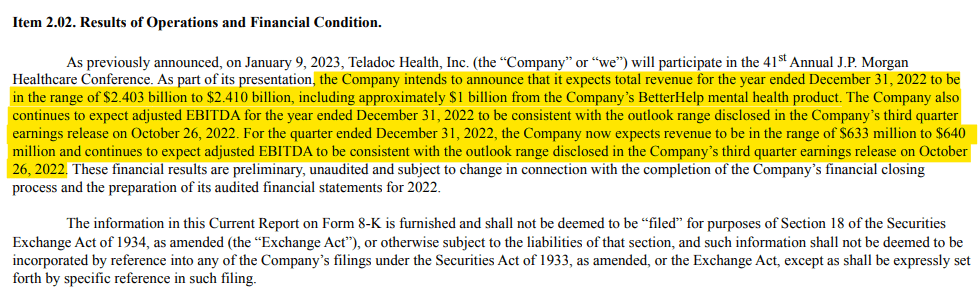

While many high-beta tech stocks rallied in early 2023, Teladoc’s strong performance (or at least a part of it) can be attributed to recent business updates from the company. In one of its recent 8-Ks (8th January 2023), Teladoc’s management updated its Q4 revenue outlook to $633-640M (the upper end of the original guidance) and maintained the adj. EBITDA guide of $88-98M.

Teladoc 8-K

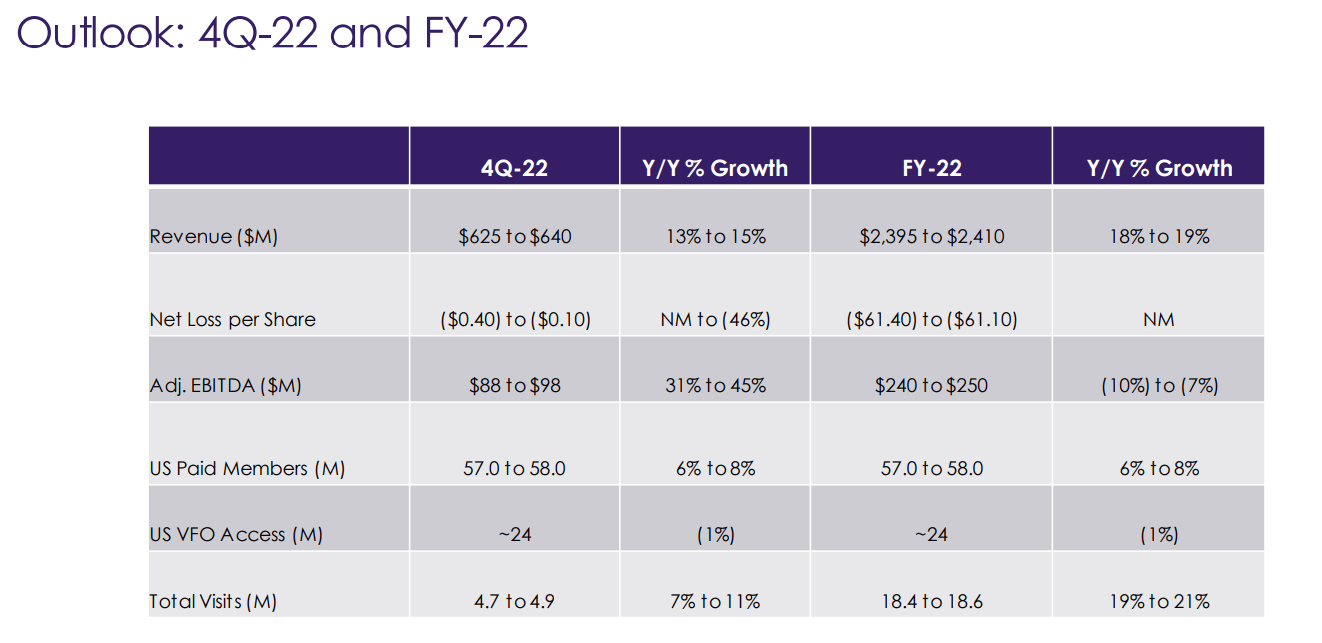

Original guidance from Q3 2022:

Teladoc Q3 2022 Earnings Presentation

In the same report, Teladoc revealed that BetterHelp (mental health platform) had generated revenue of ~$1B in 2022. With chronic and primary care numbers still looking uninspiring, I think BetterHelp is doing exceptionally well, and this product could serve as the major driver of growth for Teladoc over the next couple of years.

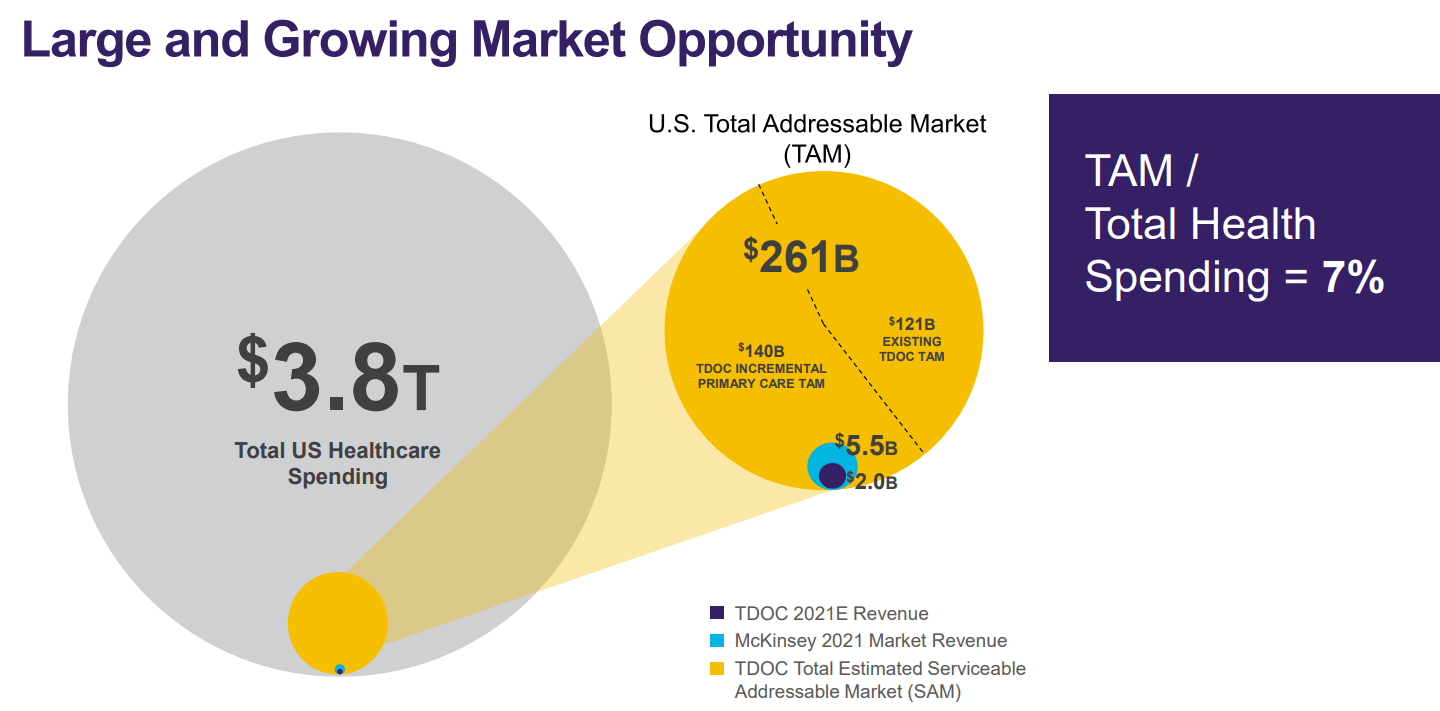

Now, as you may already know, telehealth represents a massive market opportunity; and Teladoc has a sizeable lead in this industry based on technology platform and scale. While Teladoc has been discarded by most as a COVID-only play, I believe that telehealth is not a fad, and it is here to stay.

Teladoc Investor Relations Teladoc Investor Relations

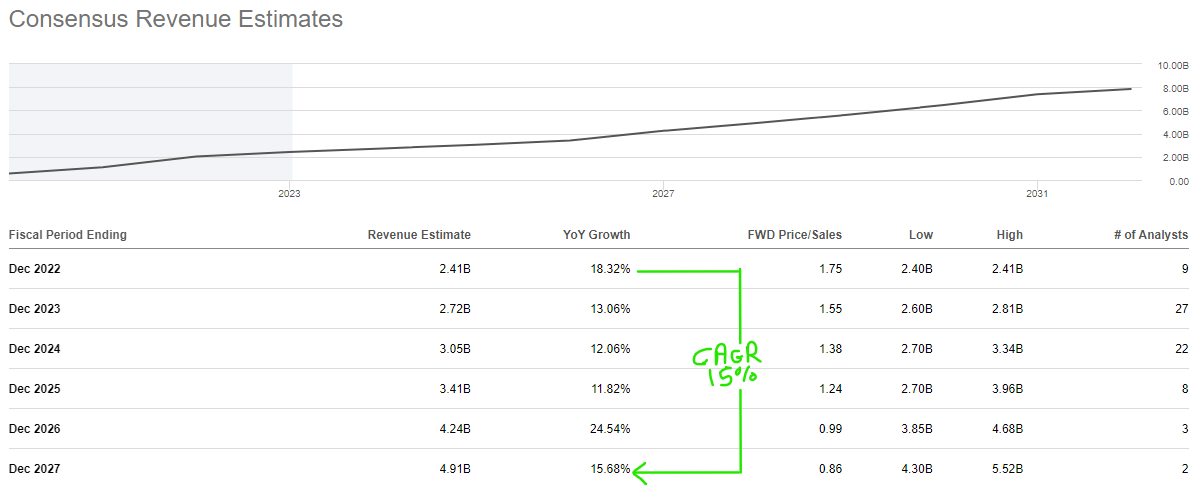

The days of hypergrowth are likely over for Teladoc; however, the growth story is far from over. According to consensus analyst estimates, Teladoc is set to grow sales at 15% CAGR over the next five years. And this figure is the same as what I had modeled for Teladoc five months ago.

SeekingAlpha

Despite having a solid growth trajectory, Teladoc announced a restructuring plan on 18th January 2023 intended to reduce operating costs. In this restructuring, Teladoc is cutting ~300 non-clinician roles (nearly 6% of the workforce), and the goal here is to strike a balance between growth and profitability! If you are looking for more details, head over to Teladoc Investor Relations. By accelerating its efforts to drive profitability, Teladoc seems to be winning investors back on its side.

In this note, we will discuss Teladoc’s recent quarter, re-run its valuation through TQI Valuation Model, and analyze TDOC’s technical charts & quant factor grades to make an informed investment decision.

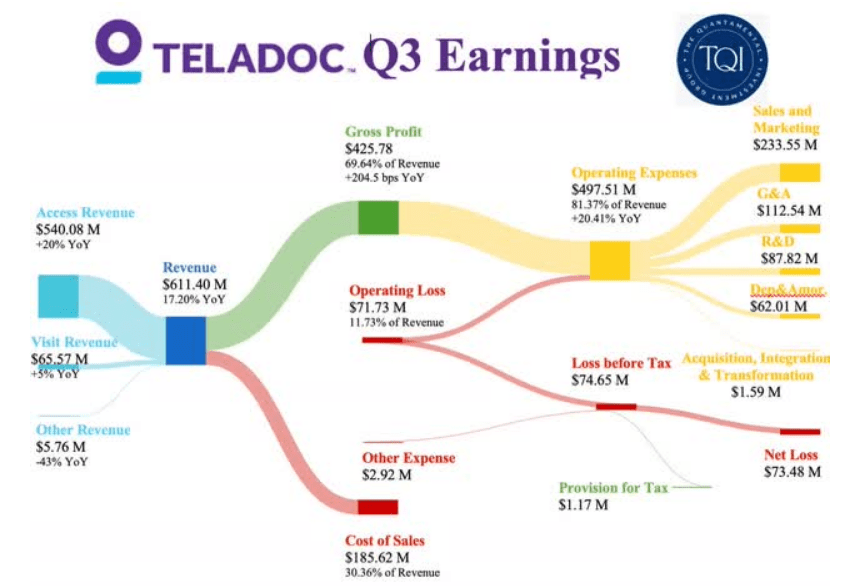

Brief Review of Teladoc Q3 Earnings

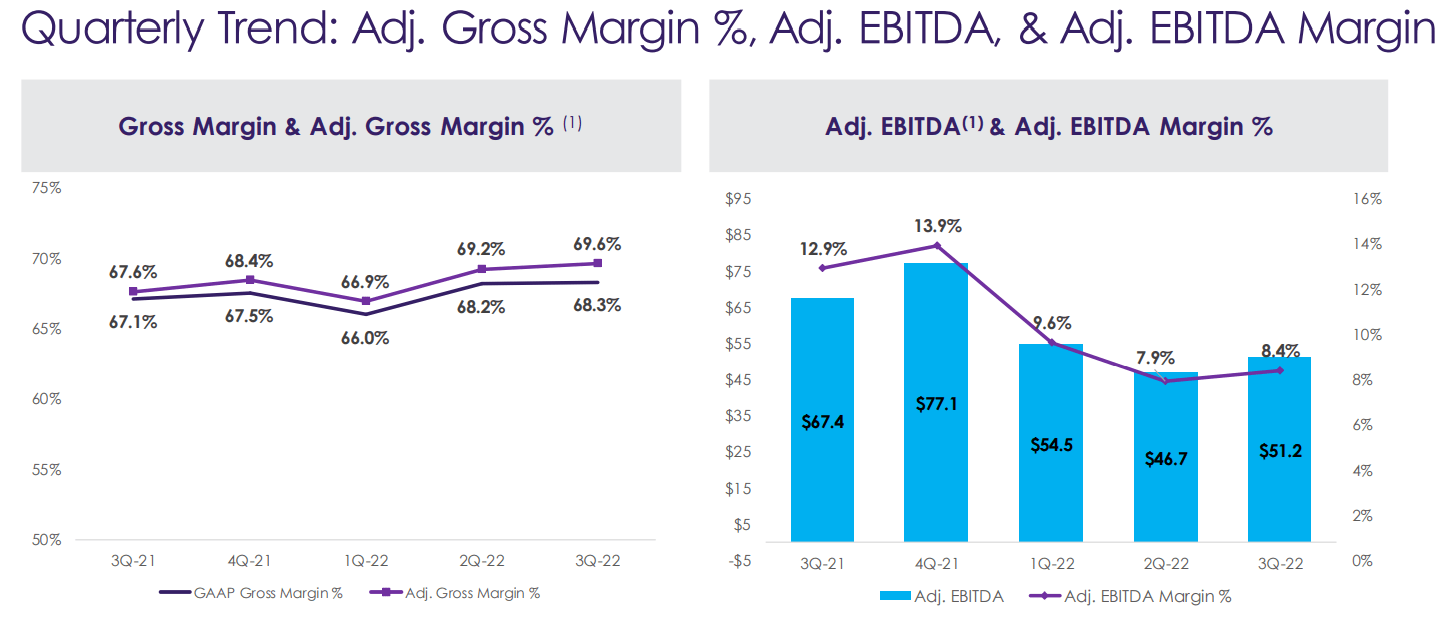

In Q3 2022, Teladoc’s revenues came in at $611.40M (up 17.2% y/y), whilst non-GAAP gross margins rose to ~70%. Despite a stronger-than-expected top line, Teladoc’s adjusted EBITDA contracted -24% y/y to come in at $51.2M. The good thing here is that Teladoc is growing adj. EBITDA once again.

Author

Management Commentary on Q3 results:

Teladoc Health delivered strong third quarter results, including robust revenue growth, and adjusted EBITDA above the high end of expectations. During the quarter we continued to make progress against our whole person care strategy as the market evolves towards integrated virtual and digital health solutions.

– Jason Gorevic, CEO of Teladoc Health

While Teladoc’s management was pleased with the Q3 performance, I think there’s still a lot of room for improvement, especially with regard to the integration of Livongo (chronic care business) and the go-to-market strategy and/or sales motion for Teladoc’s whole-person care solution.

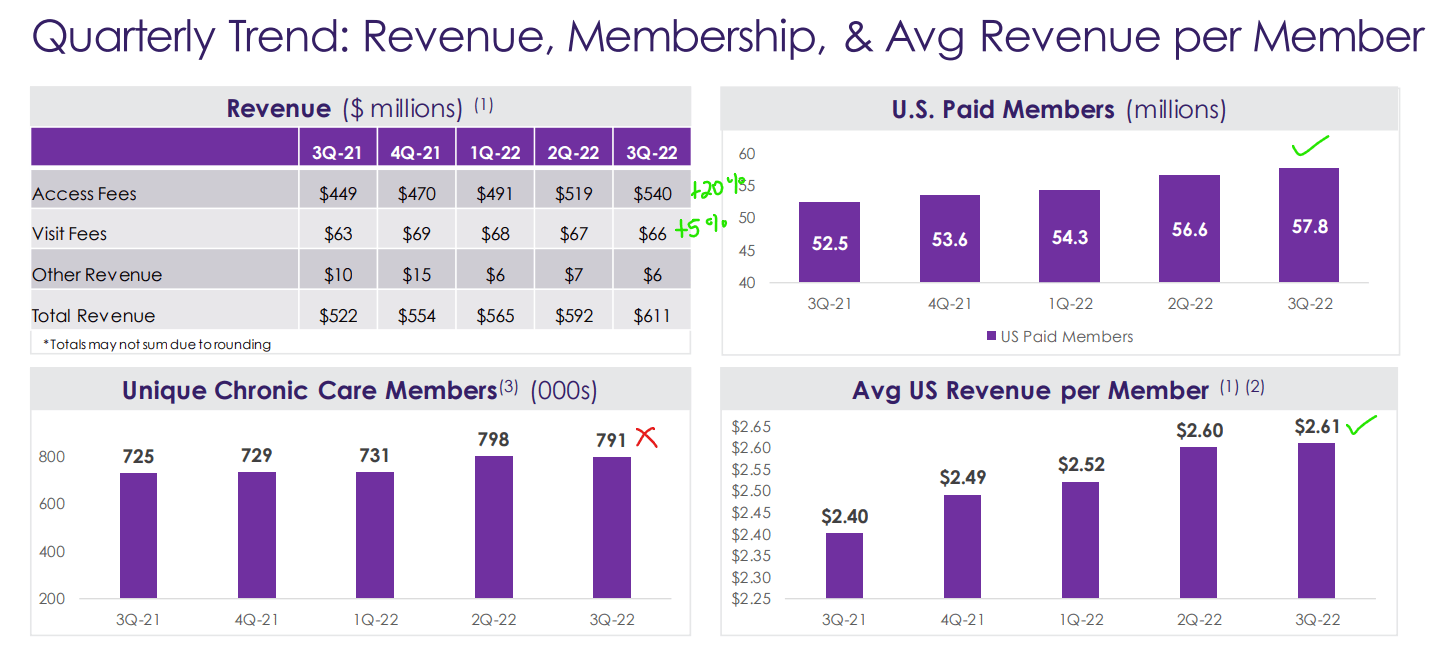

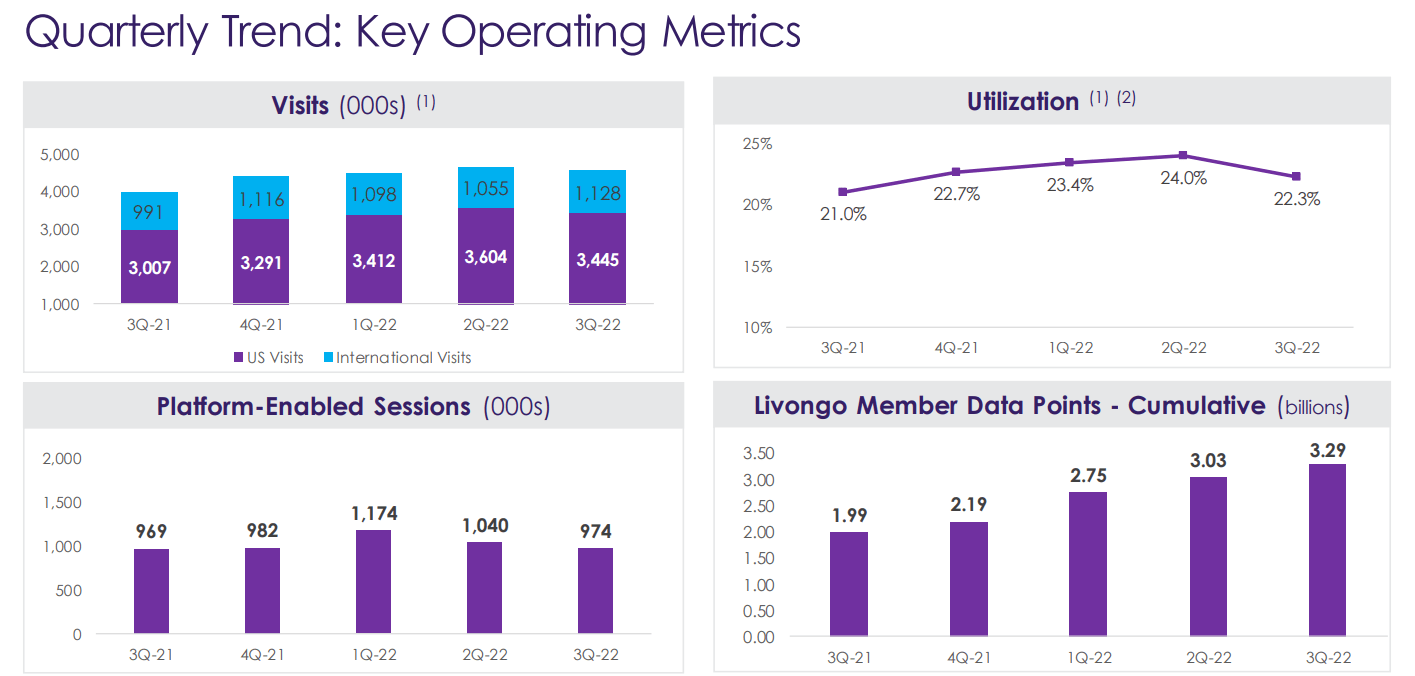

Despite a noticeable slowdown in the telehealth industry in the post-pandemic world, Teladoc is still growing its Paid Members (access fees) and Visit Fees. That said, Teladoc’s platform utilization and platform-enabled sessions count ticked down in Q3.

Teladoc Q3 2022 Earnings Presentation Teladoc Q3 2022 Earnings Presentation

As you can see above, the drop in US Visits was more or less offset by the tick-up in International Visits. In Q3, Teladoc’s gross margins improved further, leading to a tick-up in adj. EBITDA margin.

Teladoc Q3 2022 Earnings Presentation Teladoc Q3 2022 Earnings Presentation

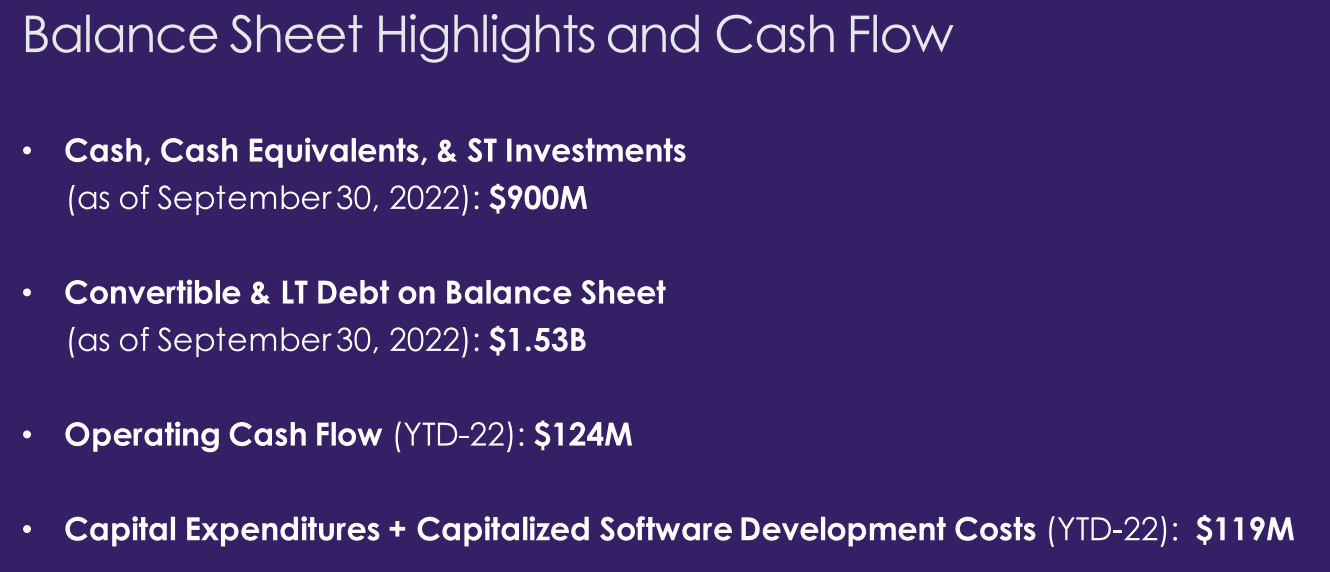

After going through a problematic digestion period post-acquiring Livongo, Teladoc is probably done with goodwill write-offs for the foreseeable future. Also, I expect Teladoc to remain a cash-flow generative business going forward. From a liquidity perspective, Teladoc has $900M in cash & short-term investment and $1.53B in convertible & long-term debt. In my view, Teladoc is well-capitalized to weather out an economic hurricane!

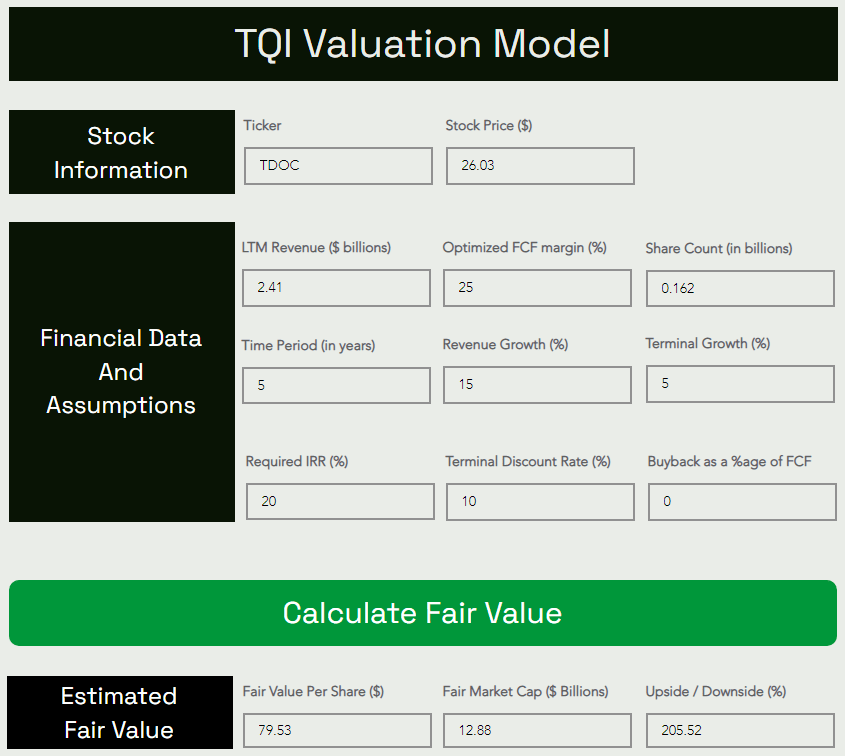

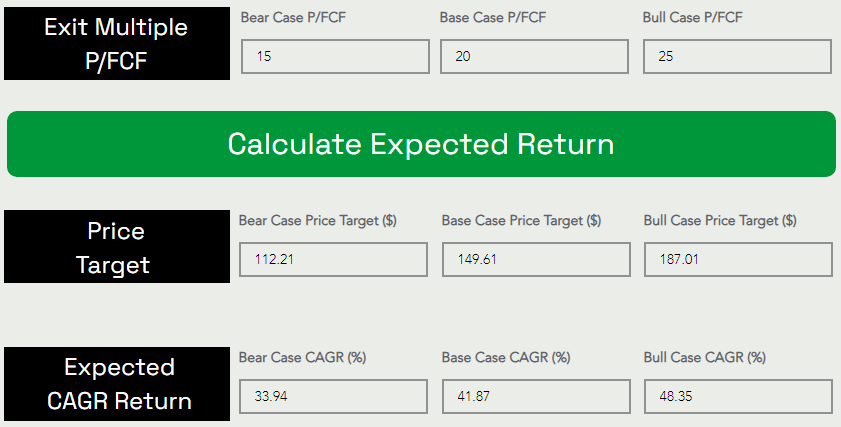

So, where do Teladoc’s fair value and expected CAGR returns stand today?

Here’s my recent valuation for Teladoc (including Q4 2022):

TQI Valuation Model (TQIG.org) TQI Valuation Model (TQIG.org)

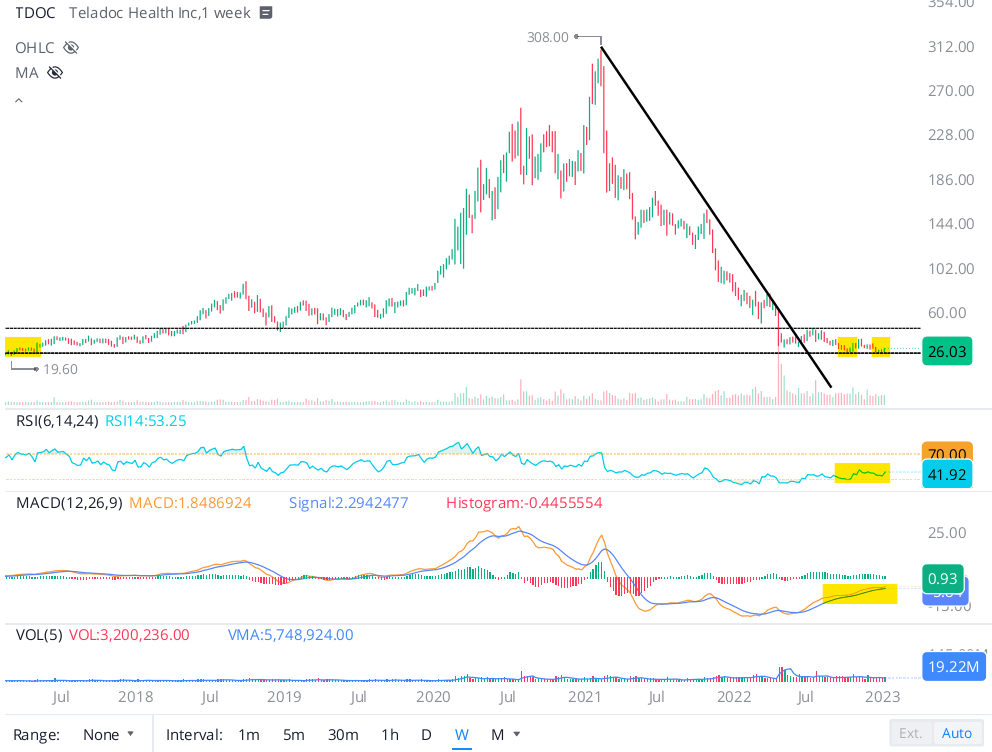

A Look At TDOC’s Technical Chart

Teladoc’s chart exemplifies the boom and bust cycles we have gotten accustomed to over the past two decades. A big boom in 2020-21 was followed by an epic bust in 2021-22. Since May of 2022, Teladoc’s stock has been forming a Stage-1 base pattern in the range of $20-40 per share.

WeBull Desktop

With Teladoc currently trading closer to the low end of this base, I think a long-term investment here is fine. However, a breakdown of this base could send the stock into a tailspin. In my opinion, such a breakdown is very unlikely; however, given the current macroeconomic environment, I can’t rule it out for now.

Concluding Thoughts

Telehealth is not a fad, as evidenced by continued sales growth at Teladoc. As we saw earlier in this note, Teladoc is expected to generate an adj. EBITDA of $88-98M next quarter, which means it is back to producing ~$400M per year in operational cash flow. As of today, Teladoc has a market cap of $4.77B and an enterprise value of roughly $5.4B. This pegs Teladoc’s valuation at ~13.5x adj. EBITDA. That’s cheap for a business growing at a healthy clip whilst improving margins. Teladoc is not out of the woods yet, and its future growth trajectory remains uncertain as the telehealth giant tries to create a paradigm shift in the industry by selling its whole-person care solutions as a bundle to clients. Considering the risk/reward on offer, I like the idea of staggered accumulation in Teladoc in the $20s (and even $30s).

Key Takeaway: I rate Teladoc a “Strong Buy” at $29.

Thank you for reading. If you have any thoughts, questions, and/or concerns, please share them below.

Be the first to comment