StudioEasy/iStock via Getty Images

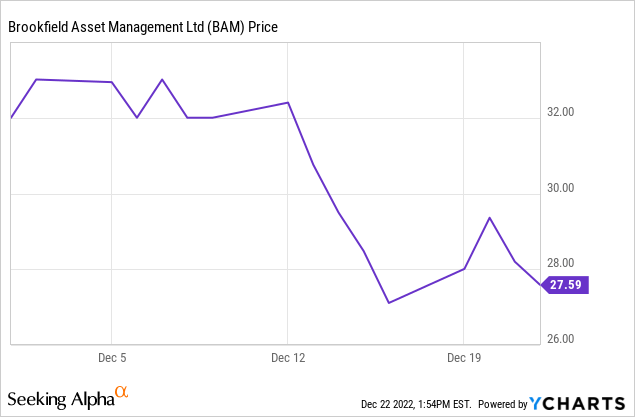

The Brookfield name draws praise from all corners of the investing sphere. We should know as simply putting the idea out there that you won’t make money by buying Brookfield entities at silly valuations tends to get hostile comments. That same love for the Brookfield name was on display as the asset management side got spun out from Brookfield Corporation (BN) in the form of Brookfield Asset Management (NYSE:BAM). There was no shortage of bullish sentiment and aggressive price targets. Yet, the newly listed entity has struggled to get a boost.

What’s wrong? Well, let us give you the other side of the story.

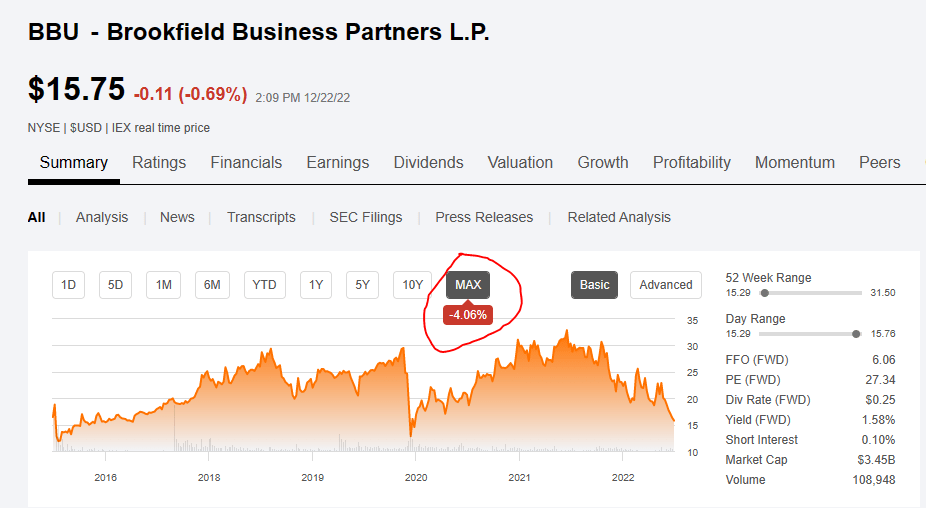

Brookfield Business Partners (NYSE:BBU)

The company came about as a spin-off from Brookfield Corporation on May 16, 2016.

BBP will be the primary vehicle through which Brookfield will own and operate the business services and industrial operations of its private equity business group on a global basis.

“Brookfield Business Partners will complete the fourth pillar of our strategy to consolidate Brookfield’s major business units into public market affiliates, and will appeal to investors looking for long-term growth and direct access to many of the businesses within Brookfield’s private equity group,” said Cyrus Madon, the CEO of BBP and a Senior Managing Partner of Brookfield.

Source: Brookfield

That sounded fantastic. Getting into the Brookfield prime time where the gloves come off and Brookfield uses its maximum leverage and expertise to give you returns. What actually happened was a bit of a let down. The stock is down 4% since the spin-off.

Seeking Alpha

6.5 years of zero returns shows what can go wrong with the best managers. Let us add to that the fact that 5.5 of those years were during an extremely benign Federal Reserve priming the pump and whispering sweet nothings every time the market fell. BBU has still trailed the S&P 500 (SPY) by 98% in total returns over this time frame. What went wrong?

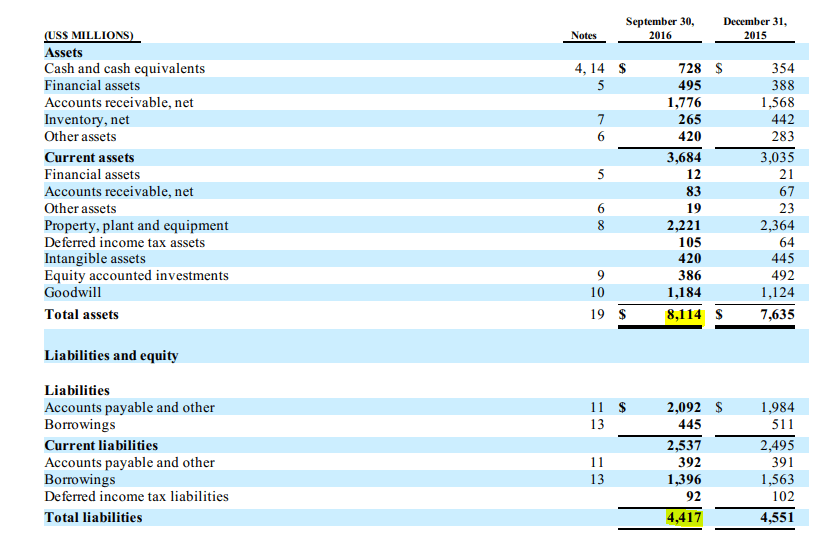

BBU’s failures were certainly not for a lack of trying. Here “trying” refers to the sheer amount of deals they have done to move the needle. We can show you that by demonstrating the delta in the balance sheet over time. One of the earliest quarterly results after listing showed the balance sheet as follows.

BBU Q3-2022

We had $8.1 billion of assets and $4.4 billion of liabilities. Considering the stock has gone nowhere, make a wild guess where these two stand today before seeing the next picture.

Ready?

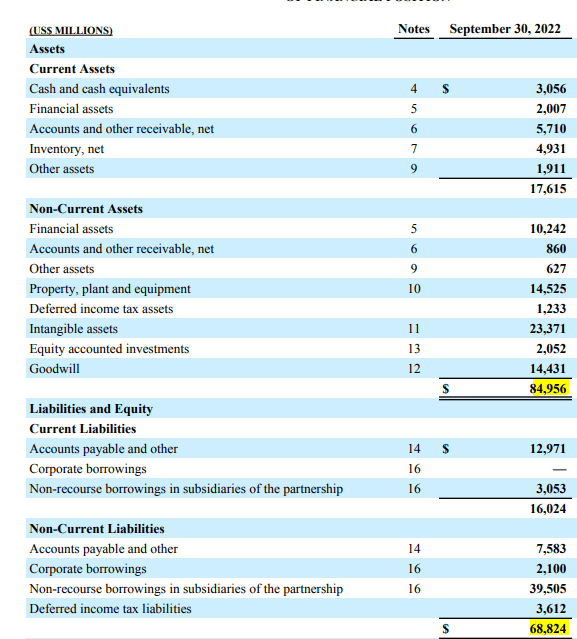

BBU Q3-2022

That’s right. Assets are up 9 fold, liabilities up by 15 fold since 2016. Anytime we have pointed that out on BBU, the bulls come out swinging. We get to hear “It is all non-recourse”, “exit multiples are amazing”, “the dog ate their homework”. Defend it all you like, but the fact remains that BBU’s extreme leverage has not produced any returns that we can see. Analysts have often touted the funds from operations (FFO) as an indication of how “cheap” the company has become. Considering that BBU owns non-REIT businesses, that number is about the most useless metric one can find in our opinion. What BBU has done is taken the maximum amounts of non-recourse leverage in order to maximize returns. That has meant that there are no real GAAP earnings and the only executable idea is to sell the asset at a higher price. Obviously they have done some impressive turnarounds and the recent sale to Cameco Corporation (CCJ) was one of the better successes. But overall this strategy has failed and it has failed while there was sunshine and rainbows across the Brookfield empire. Looking ahead, those heavily leveraged entities will all struggle as rates rise and BBU will have a tough time exiting these investments.

Brookfield Asset Management

BBU’s miss is not on anyone’s mind with bullish ratings dominating the BAM stock. Here is one as an example.

“We view BAM as one of the largest global Alternative Asset Managers ($400B in fee-paying AUM), with an outsized exposure to some of the fastest growing parts of the market, including Infrastructure, Clean Energy, and Credit – collectively 63% of 2022E management fees,” Blostein wrote in a note to clients.

“As a result, we expect BAM to drive a robust 20%+ earnings growth CAGR through 2024,” Blostein said. He sees that growth supported by its fundraising in real estate, transition, and infrastructure at an accelerated pace, healthy deployment and fundraising in credit, horizontal product expansion across its main asset classes, and margin expansion.

His 12-month price target of $40 implies 23X Q5-Q8 P/E and a dividend yield of 3.2%.

Source: Seeking Alpha

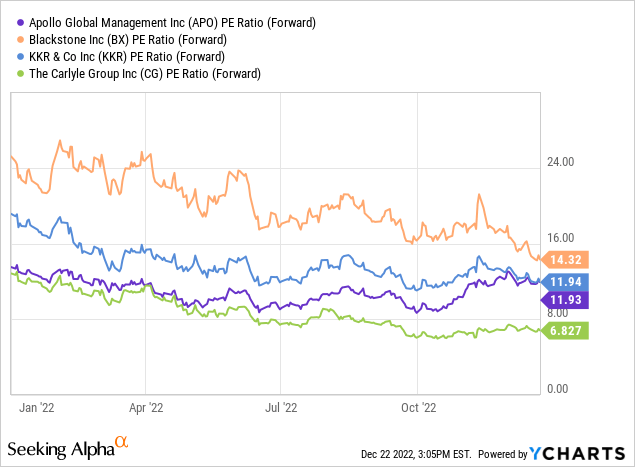

What is stunning about that 23X number is where it stands relative to other asset managers. Apollo Global Management Inc. (APO), Blackstone Inc. (BX), KKR & Company Inc. (KKR) and The Carlyle Group Inc. (CG) have all grown their fee based revenue by about 17% a year over the last 5 years. Here are their current multiples.

So if you like BAM, you should look at a lot of alternate asset managers as well.

Verdict

Our thinking here is that,

1) All asset managers will struggle in the years ahead, not just BAM.

2) Taking it for granted that the asset management business for BAM will grow so rapidly creates big downside risks.

3) Paying a huge premium here is not warranted.

4) Valuation compression is likely to give you negative returns for the next few years.

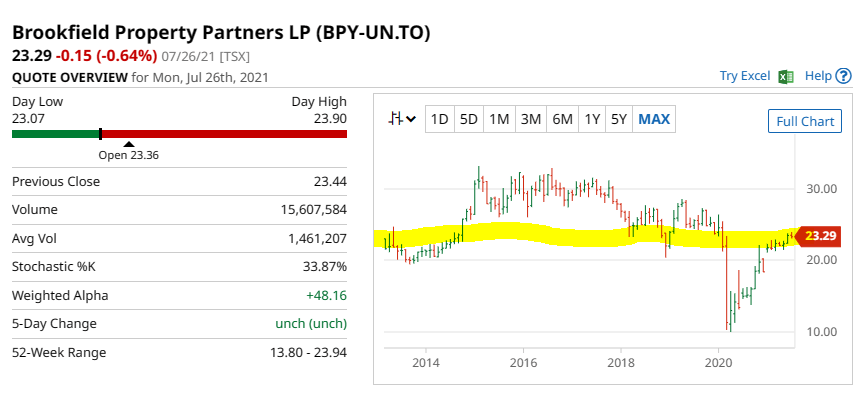

BBU is a reminder that not everything with the Brookfield name delivers. The same was the case for another forgotten Brookfield Entity, Brookfield Property Partners. This one was also run with extreme levels of leverage and ultimately was taken private well below the publicly stated NAV. The stock was flat from listing till take out on the TSX, over a period of 8 years.

Bar Chart

If we were to guess, Brookfield is probably not too happy even with the price it did pay on those assets. That is what happens when you run at 15X debt to EBITDA.

Other engines of Brookfield growth, Brookfield Renewable Partners L.P. (BEP) and Brookfield Infrastructure Partners LP (BIP) are also stuttering near 52 week lows. The real boom for the alternate asset management business was a consequence of zero interest rate policies. That has gone and unless it comes back, expect BAM to underwhelm in ways you cannot possibly imagine today. Of course the bullish crowd that touted BAM as the only place to go in an era of zero rates, now sings praises of it delivering in a high inflation era. We think that things will be very different. We have a hold rating on both BBU and BAM and would get interested in BAM under $20/share.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment