ronniechua/iStock via Getty Images

Introduction

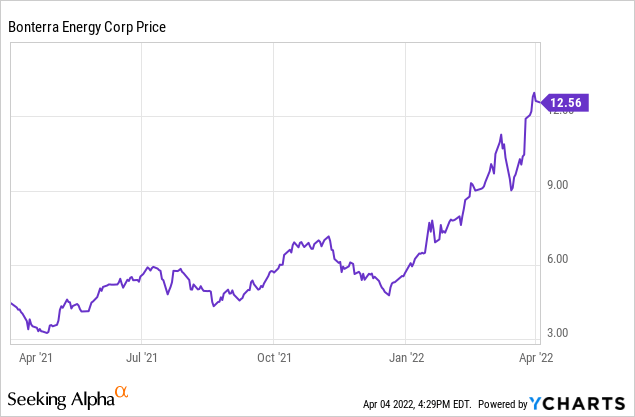

It has only been about three months since I last discussed Bonterra Energy (OTCPK:BNEFF) but the company’s share price has done exceptionally well with a share price appreciation of approximately 150% as the stock is currently trading over C$12/share compared to the C$5.25 when my December article was published. Time to update my view!

I would recommend to trade in Bonterra stock on the Toronto Stock Exchange where Bonterra Energy is trading with BNE as its ticker symbol. The average daily volume in Toronto exceeds 150,000 shares per day, clearly making it the most liquid listing for this company. The current market capitalization is approximately C$440M.

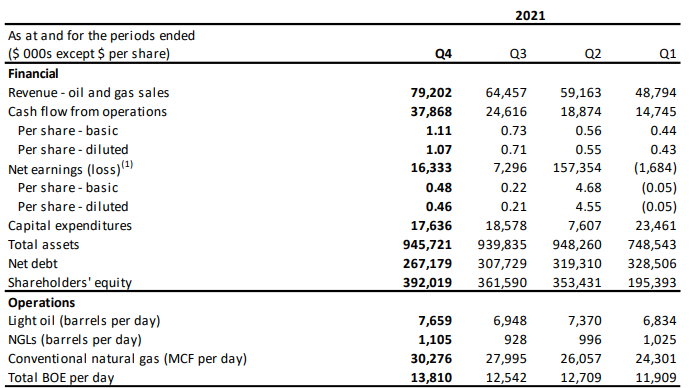

The final quarter of 2021 shows the cash flow potential of Bonterra Energy

Bonterra’s oil-equivalent production rate increased throughout the year (but was flat in Q3 compared to Q2) and the company was able to produce a total of 13,810 barrels of oil equivalent in the final quarter of the year. Approximately 55% of the oil-equivalent output consisted of light oil with natural gas liquids representing just under 10% of the production mix with the remainder coming from the production of natural gas.

Bonterra Investor Relations

As the realized natural gas price increased to almost C$5/MCF in the fourth quarter (up from for instance C$3.02 in the final quarter of 2020 and up from C$3.94 in the third quarter of 2021), the revenue from natural gas provided a nice additional boost.

And as you can see in the image above, the company generated almost C$38M in operating cash flow while it spent just C$17.6M on capital expenditures resulting in a free cash flow result of around C$20M. Divided over 35M shares outstanding, represents a free cash flow of C$0.57 per share. Not bad at all.

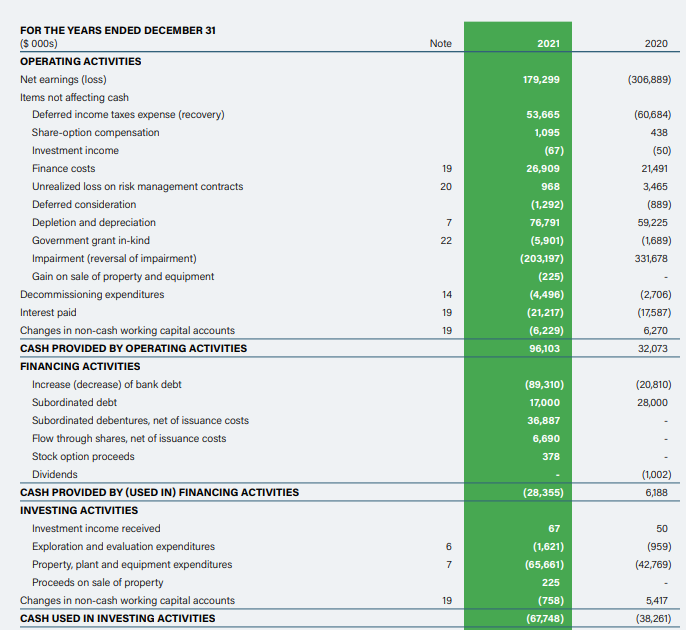

Looking at the company’s cash flow results on a full-year basis, Bonterra reported an operating cash flow of C$96M. This includes a C$6.2M investment in the working capital position so on an underlying basis the adjusted operating cash flow was C$102.3M and after deducting the C$67M in capex, Bonterra generated approximately C$35M or C$1/share in free cash flow.

Bonterra Investor Relations

With an average realized price of C$75/barrel of oil, C$44 per barrel of NGL and less than C$4 per MCF natural gas, it is clear Bonterra Energy is on the right track.

The company’s main issue was the high net debt position on the balance sheet. Not only because it makes the equity of the company more risky, but also because the high interest expenses had a profound negative impact on the cash flows. In FY 2021, Bonterra Energy paid in excess of C$23M in interest expenses. That’s approximately C$5 per barrel of oil-equivalent that was produced in 2021. Reducing the net debt will reduce the interest expenses and further boost the cash flows.

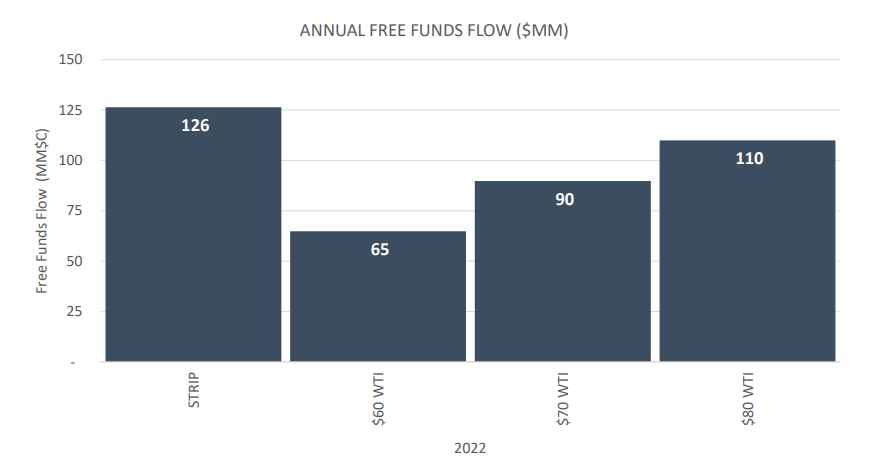

That’s why the guidance for 2022 is focusing on keeping the production unchanged and instead focus on generating free cash flow. Bonterra now expects to produce 13,300-13,700 boe/day in 2022 and as it will spend just C$55-65M on capital expenditures to keep the production rate stable, it anticipates to generate C$90M in free cash flow using a WTI oil price of US$70 in the base case scenario while the natural gas price used in the guidance is just C$3.50/mcf. With WTI at $100 and AECO natural gas prices above C$5, it looks like Bonterra Energy may surprise friend and foe this year and I expect to see an excellent Q1 result.

Bonterra Investor Relations

So using $75 WTI and a free cash flow result of C$100M, Bonterra Energy will make close to C$3/share in free cash flow this year, which makes the share price of C$12.50 not outrageously high.

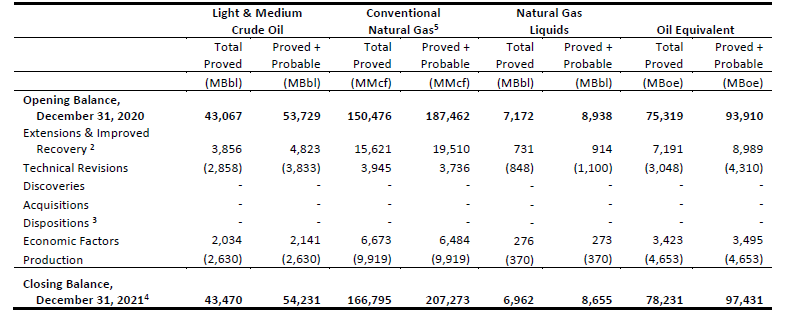

The reserve estimate has been updated, underpinning a long reserve life

Bonterra also released an updated reserves estimate and the total amount of barrels of oil equivalent in the proved and probable categories increased from just under 94 million to 97.4 million barrels. This means the company mitigated the impact from the depletion in 2021 and replaced almost 175% of the barrels it actually produced.

Bonterra Investor Relations

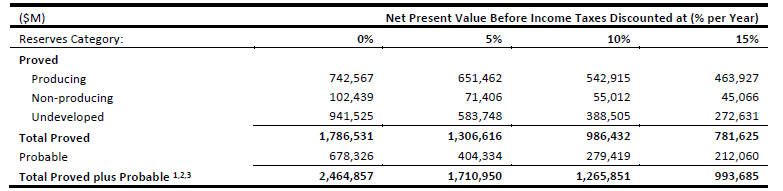

Based on the anticipated output of 13,500 barrels of oil-equivalent per day, Bonterra’s 2P reserves underpin a useful reserve life of just under 20 years which isn’t bad at all. The independent consultants also calculated the PV10 value of the updated reserve estimate and on a pre-tax basis, the PV10 of the 2P reserves comes in at C$1.27B.

Bonterra Investor Relations

With a total deficit of in excess of C$400M on the balance sheet, Bonterra should be able to keep the tax pressure rather limited, and although no after-tax calculation was provided, I think it will be somewhere between C$900M and C$1B.

With a net debt of just under C$270M as of the end of 2021 (including C$10M in contingent consideration payable), the PV10 value of the equity on an after-tax basis will likely be just over C$600M.

Investment thesis

That would be just over C$17/share indicating additional upside, but keep in mind we should be mindful of interest expenses and G&A expenses which will weigh on that theoretical “fair value” of the stock. We shouldn’t discard Bonterra at all as the PV10 value was based on an oil price trading at just around C$80/barrel in 2023-2025. So if the current high oil prices are maintained for a bit longer, the PV10 value will increase even if not a single additional barrel of oil-equivalent would be discovered.

2022 will likely provide a boost as the company is in an excellent position to rapidly reduce its net debt to less than C$200M which will provide more room to breathe on the interest expense front.

That all sounds great but as I’m looking to reduce my exposure to some oil names, Bonterra isn’t on my buy list and I will likely sell the (very small) position I currently have.

Be the first to comment