fizkes/iStock via Getty Images

By Rob Isbitts

Strategy

Invesco Senior Loan ETF (NYSEARCA:BKLN) is among the largest and longest-tenured of a class of ETFs that invest in a portfolio of “Senior Loans.” These are short-term loans made to corporations. They are debt of the company, and collateralized against assets of that company. BKLN invests in a basket of these loans, which themselves are not publicly traded securities. BKLN aims to track the Morningstar LSTA US Leveraged Loan 100 Index.

Proprietary ETF Grades

-

Offense/Defense: Offense

-

Segment:Bonds

-

Sub-Segment:Senior Loans

-

Correlation (vs. S&P 500):Very Low

-

Expected Volatility (vs. S&P 500):Very Low

Holding Analysis

BKLN holds more than 100 loans, more than the target index. The entire portfolio matures in between one year and seven years. 85% of the ETF’s exposure is to loans backed by US companies, while the other 15% are from the UK and European issuers. Only 8% of the loan holdings are rated BBB, which is the highest rating of any security in the ETF. BB-rated loans comprise another 24%, and B-rated loans make up 63% of the fund. The rest (5%) of the portfolio is invested in loans rated below B or not rated.

Strengths

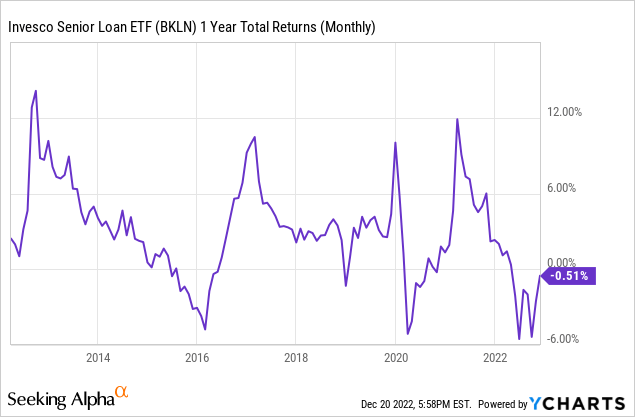

Under normal circumstances, BKLN could be viewed as a nice reward/risk tradeoff. As this chart shows, its 1-year total return since its 2011 inception have ranged from as high as 13% and as low as -6%. That is a very solid range for any ETF, and can provide peace of mind versus the regular gyrations of the stock market.

In addition, Senior Loans have some distinct competitive advantages over some other types of corporate debt, which Invesco, the ETF’s issuer, touts strongly in its marketing materials for BKLN. Senior secured loans rank above traditional bonds, preferred stock and common stock in the capital structure. In other words, when the company has limited assets to pay out debtors, Senior loan holders get paid first among those groups. That’s because they are “securitized” in that their pay back to the debtor is tied to specific company assets, such as inventory, property, plants and equipment. Senior loans have also traditionally offered a notable yield advantage over other types of bonds of similar maturities.

Weaknesses

Now, for the bad news. What makes Senior loans, and BKLN as a leader in that space, attractive is also what can make it very risky. As noted in the holdings section, this is about as “junky” a collection of securities you will find in an ETF. More than 2/3 of the portfolio are rated below BB, which is typically where many high-yield funds crowd into, as it is the “highest quality junk” so to speak. But here, the average rating of a loan is B. So that makes BKLN more like a regulated, tamer version of a loan shark. The companies borrowing in this manner are often those who are the opposite of pristine quality. None of this mattered when interest rates were low and money was free and easy. In fact, these types of corporate borrowers made extensive use of the market, and BKLN did its job in buying them up for shareholders. But as of 2022, the climate has shifted.

We also cannot forget the 5-alarm fire that was BKLN’s price crash during the onset of the pandemic in 2020. If that was just a drill, with the price dropping about 25% in about a month, then recovering over the last 9 months of the year, we don’t want to be around the next time that happens.

Opportunities

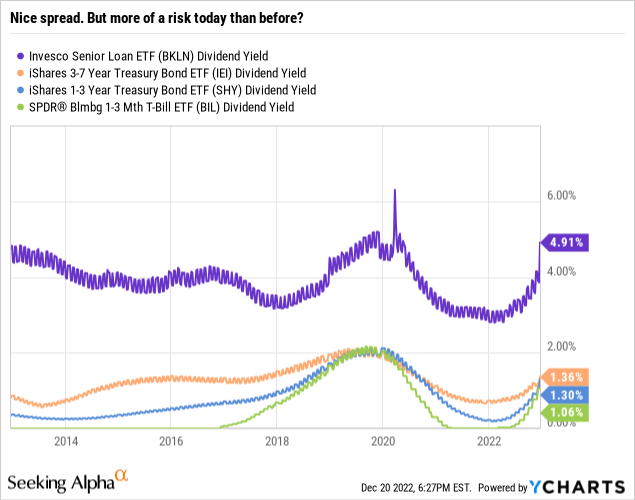

As shown in the chart below, BKLN delivers a consistently higher yield as compared to US Treasuries. In fact, it’s not even close. Even the orange line, which represents Treasury Notes of similar maturity to BKLN’s holdings is more than 300 basis points behind on a 12-month trailing basis. So if credit conditions do not become impaired during the next year or two, BKLN stands to deliver a big yield pickup, with its historically-low level of volatility. Note that these are 12-month trailing yields, so Treasuries have caught up somewhat, but BKLN still paid out an annualized rate of 6.4% on 12/14/22.

Threats

Pardon our skepticism, but if our bull case laid out in the Opportunities section above actually plays out, we will be as surprised as anyone. That will be good news for current BKLN holders. But we think it that’s a moonshot, As we have noted in many bond ETF profiles recently, the credit markets are unstable at best, and dangerous at worst. It is already been seen in price slippage among high yield and corporate ETFs. And the fact is, even during a period of lower but stable interest rates, BKLN did not generate enough positive return to offset the risk that is now being realized. The fund earned a total return of between 9-10% in 2016 and 2019, but every other calendar year produced returns of between roughly +2% and -3%. Consistent, but not worth the risk, now that T-Bills represent new, stiffer competition for the first time in a long time.

Proprietary Technical Ratings

-

Short-Term Rating (next 3 months): Sell

-

Long-Term Rating (next 12 months): Hold

Conclusions

ETF Quality Opinion

BKLN is a $4 Billion ETF with plenty of history behind it, and it trades about $175 million in a day. It represents a sizable part of the Senior Loan market. That’s all positive, until the next credit crunch occurs. Then, the opposite happens. Investors try to get out the door, and there are not enough diverse players to accommodate demand for those sales without marking down prices sharply (see 2020). This is the same disease that could potentially infect corporate and high yield bonds. So BKLN is a solid ETF, but only as solid as the market segment it represents.

ETF Investment Opinion

BKLN is a Sell for the reasons above, but the real bottom-line is this. A repeat of 2020’s price action is a bigger risk than at any time we know of. That does not mean it will happen, but only that conditions are in place that something of that sort could happen. Credit markets are cracking, so only the most risk-tolerant investors would consider trading off a bit more yield for the possibility of being caught in period when liquidity in this market dries up quickly, prices plunge and this time around, the recovery could take much longer.

Be the first to comment