peepo/E+ via Getty Images

This is my first take on BioXcel (NASDAQ:BTAI). In Q2, 2022, it prepared for the launch of its IGALMI (dexmedetomidine, BXCL501) sublingual film for the acute treatment of agitation associated with schizophrenia or bipolar I or II disorder in adults. As discussed in its Q3, 2022 earnings call (the “Call”), its trade launch started on 07/2022.

In this article written during the last days of 01/2023, I assess BioXcel’s near term investment merits as it pursues its launch and develops its late stage pipeline.

IGALMI’s launch which is underway will likely disappoint over the near term.

I have long characterized the fraught and often drawn out period, between a pharma product’s launch and its commercial success, as the danger zone. I anticipate that IGALMI is setting up for a particularly exasperating such period.

IGALMI’s label is broad. It is indicated for the acute treatment of agitation associated with schizophrenia or bipolar I or II disorder in adults. It is free of black box warnings. It includes several warnings and precautions including ones for hypotension and somnolence. Somnolence is called out as one of its most common adverse reactions.

I assess the label as described above as all for the good. However, there are two aspects of the label which merit attention. Most significantly in connection with its administration it provides:

2.1 Important Recommendations Prior to Initiating IGALMI and During Therapy IGALMI should be administered under the supervision of a healthcare provider. A healthcare provider should monitor vital signs and alertness after IGALMI administration to prevent falls and syncope.

The label also includes a post-marketing mandate; such requirements are not unusual. Indeed they are quite routine in the abstract. IGALMI’s particular post-marketing requirement strikes me as considerably more rigorous than is the norm for such mandates as discussed below.

Unlike the post-marketing proviso, the label’s supervision requirement just about guarantees that IGALMI’s 2023 revenues will be modest.

Two IGALMI requirements for investors to evaluate.

Supervision

IGALMI’s supervision label requirement has resulted in BioXcel’s decision to launch IGALMI in a hospital setting. In response to an analyst question as to whether anything precluded a physician from sending a patient home with an IGALMI scrip, CEO Mehta blithely responded:

…wherever there is a supervision available, IGALMI we believe can be used. We’re just focusing in the hospital setting because two-thirds of the patient out of 25 million episode comes to the hospital market. It’s a very well defined and focused approach, how physicians will use it, once they develop experience, all of that will unfold in next six to 12 months.

I do not share his attitude here. From my point of view this encumbers IGANDI’s launch with a troublesome overlay of bureaucracy, red tape, and delay. Hospitals, particularly the most significant, are vast institutions, with a variety of competing constituencies. Once you focus your sales on this channel you are ensuring that nothing can happen quickly.

Before you can sell to a hospital you have to get on its formulary. Before that can happen you need approval from its Pharmacy and Therapeutics Committee “P&T committee”. Before the P&T committee can consider such a decision, the issue must be added to its agenda. Before it can make a decision, a quorum must attend the meeting.

How red is this red tape you might ask, I say very red. In response to analyst questions during the Call, BioXcel’s CCO Wiley filled out the time required to fulfill two revenue prerequisites:

- formulary access — the process for formulary access typically takes 6 to 12 months, noting at the time that BioXcel had a lot of activity ongoing with just 26 reps in the field.

- product uptake — it’s roughly 37-or-so percent in emergency department and site physicians expected to try IGALMI the first six months or so post formulary approval.

As regards item 1 above, it is important to understand that formula access is not some automatic process. It takes 6-12 months to get on a formulary. Wiley does not advise how much prep works or how long it takes to start the process.

We do know that BioXcel is beefing up its sales force beyond its initial 27 reps in order to kick start the process. Its initial generally successful sales efforts coupled with its market research led it to make the strategic decision “to expand our sales footprint across all major geographic markets”.

During the Call CEO Mehta described its forward initiatives to fulfill its strategy as follows:

By December 1st, we will increase our sales force and deploy a total of 70 reps to cover approximately 1,700 target hospitals. We now have fully integrated commercial and medical teams with the necessary infrastructure to cover the entire U.S. agitation market to fuel our growth.

To drive additional awareness and understanding of IGALMI, our medical affairs teams have been actively engaging with the medical community and P&T committee members in addition to participating in leading industry conferences across the country.

Post-marketing

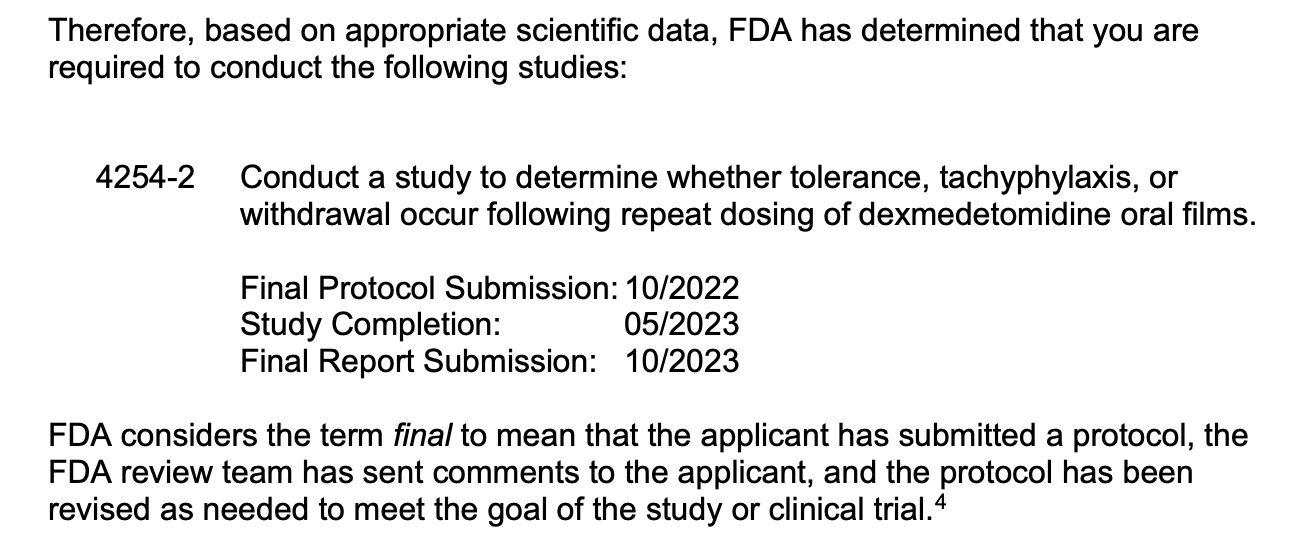

Of less immediate impact than the above described supervision mandate, but nonetheless important is its post-marketing requirement in its approval letter. Post-marketing requirements are an essential often routine part of the FDA’s drug approval process.

The actual requirement listed in the FDA’s 04/2022 NDA approval letter is rigorous and unforgiving. It notes that typical postmarketing adverse events reports would be insufficient to identify serious risks of tachyphylaxis, or withdrawal accordingly its approval letter includes the following:

accessdata.fda.gov

My research has not encountered any references to such a study being considered by BioXcel. I do not expect this to become an issue, however I am alert to the issue and will be following it.

BioXcel has an intriguing late stage pipeline with several near term catalysts.

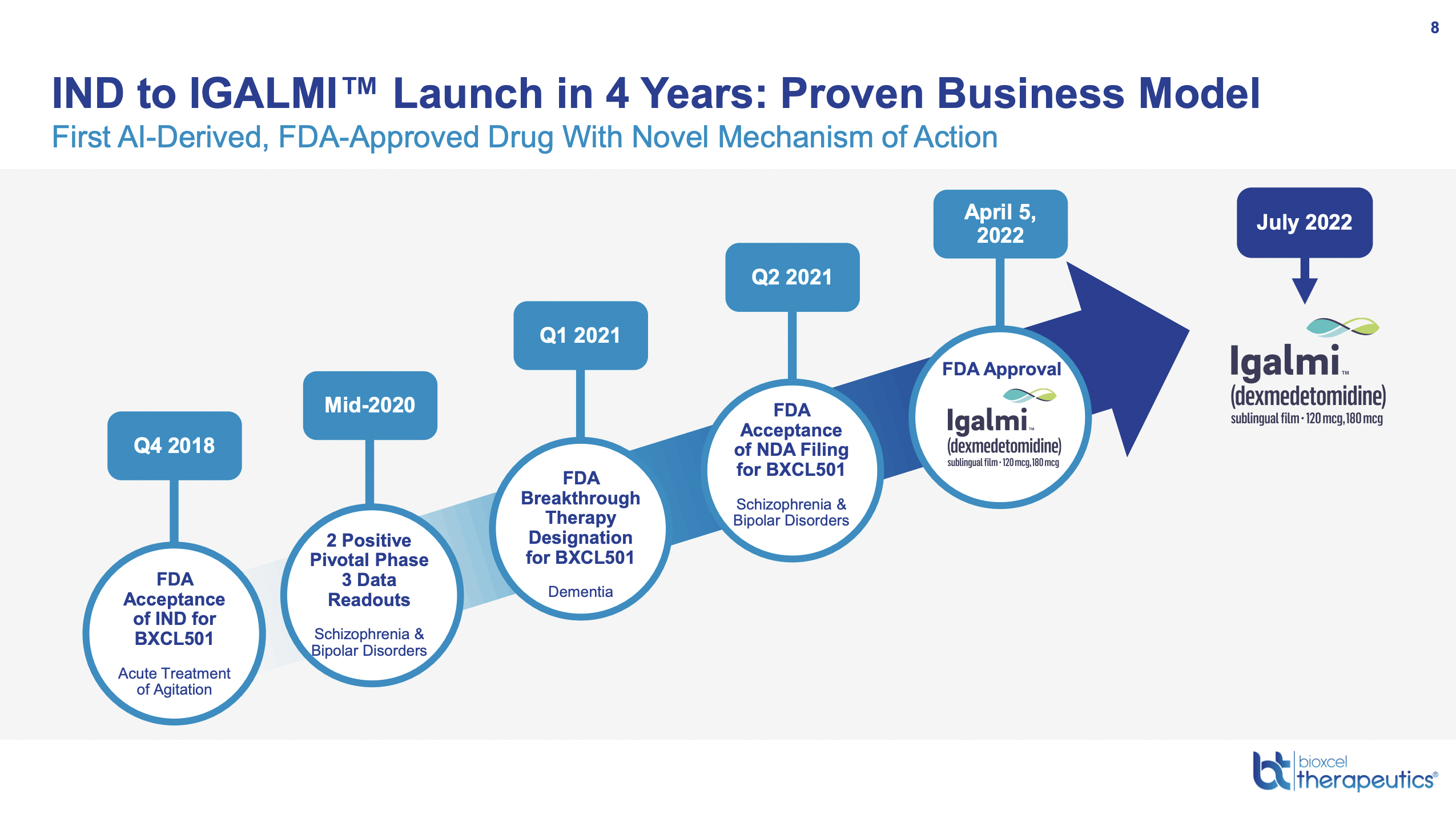

BioXcel’s recent 01/11/2023 presentation (the “Presentation“) at the 41st Annual J.P. Morgan Healthcare Conference provide late insights on its prospects. The Presentation’s title “AI-Driven Transformative Medicines in Neuroscience and Immuno-oncology” shows its focus on the current hot ticket “AI”.

The most impressive of its several AI focused slides is its slide 8 below:

ir.bioxceltherapeutics.com

Hype aside, IND to IGALMI launch in four years is impressive. No doubt the fact that dexmedetomidine had previously been approved in another indication played a part. It was approved as an injectable for sedation of non-intubated patients prior to and/or during surgical and other procedures in 1999.

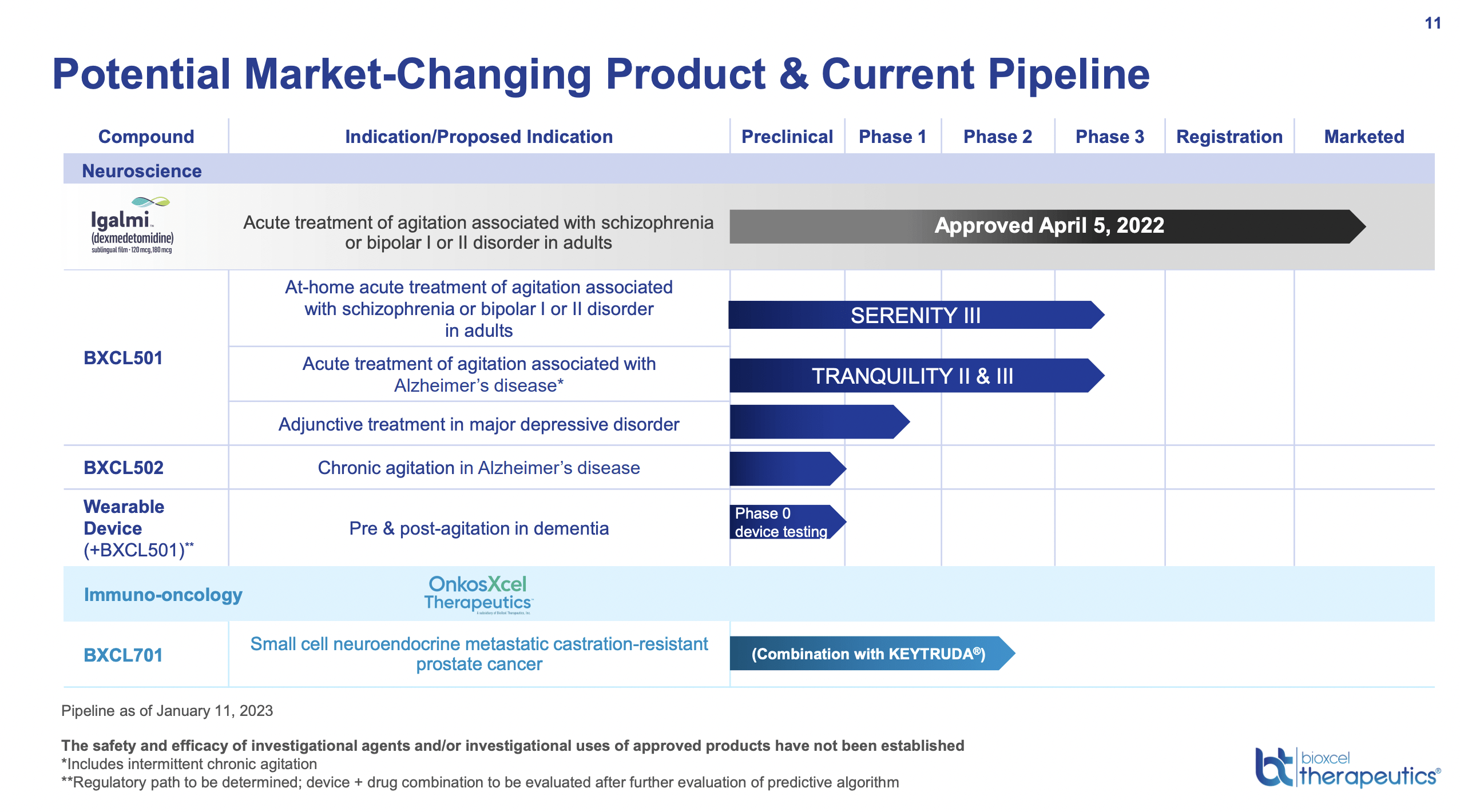

BioXcel has big plans for this molecule as reflected by its Presentation pipeline slide 11:

ir.bioxceltherapeutics.com

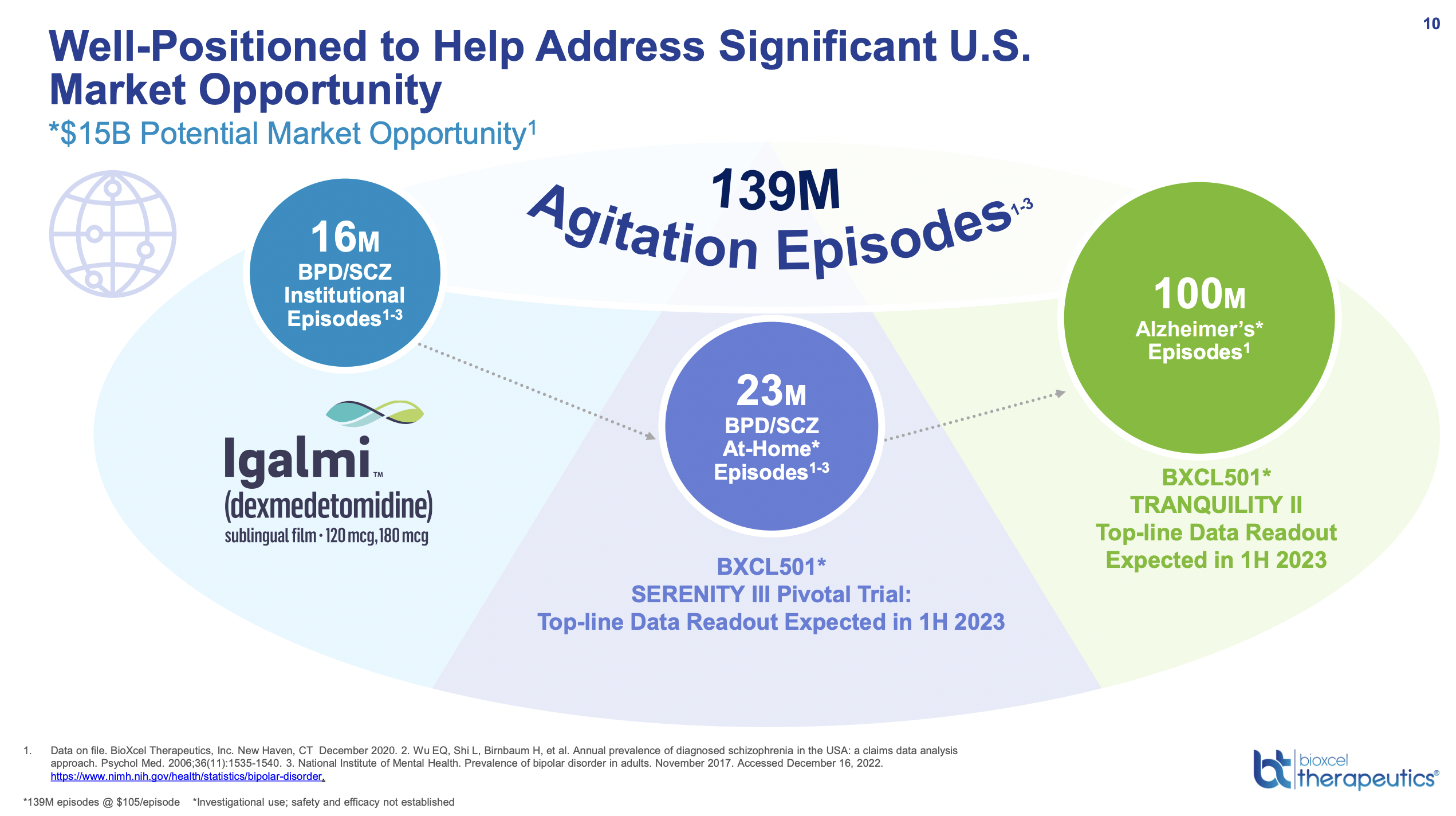

It visualizes a major market opportunity in treatment of agitation aggregating to $15 billion as reflected by its Presentation slide 10 below:

ir.bioxceltherapeutics.com

Although IGALMI’s run for the roses under its current approval faces delays as indicated above, if it can win expanded approvals things should be easier. Say for example it gets positive 1H 2023 readouts on its TRANQUILITY II and/or SERENITY III pivotal trials. It might submit its NDA’s in 2H 2023.

It would then be looking at launches in 2024. As reflected by Presentation slide 12, SERENITY III is directed at Bipolar Disorders or Schizophrenia Associated Agitation (at-home use). During the Call CEO Mehta noted that the at home market was double that currently approved.

At home use would obviate the hospital formulary issue. Instead it would need to get it approved by insurers. Assuming no unexpected hiccups develop in its hospital launch, I expect that it should be able to gear up payer approvals without undue delay.

As for TRANQUILITY II, it is the big kahuna as shown by slide 10 above. If BioXcel gets approved with a clear label to treat agitation episodes in Alzheimer’s Disease it will have succeeded in one of the tougher indications before the FDA as Biogen (BIIB) and ACADIA (ACAD) have learned to their dismay.

Not atypically BioXcel generates significant deficits however it has sufficient liquidity.

The Presentation includes no financial overview slide. It pays ever so much more attention to its bounteous blue sky potential than to its growing accumulated deficit. Per its Q3, 2022 10-Q (p. 6) the deficit grew from >$245 million at year end 2021 to >$356 million after Q3, 2022. Growing ~$111 million over 9 months puts it at an annual deficit clip approaching $150 million.

During the Call CFO Steinhardt gave the following Q3, 2022 financial rundown advising that it:

…reported a net loss of $41.8 million for the quarter — for the third quarter of 2022 compared to a net loss of $26.8 million for the same period in 2021. Cash burn for the quarter was approximately $31.5 million, which is consistent with the first two quarters of 2022. As of September 30, 2022, cash and cash equivalents totaled approximately $232.3 million.

In 04/2022 BioXcel completed a $260 million financing which it pegged as providing it a cash runway into 2025. Assuming that its cash burn continues at $31.5 million a quarter, its ~$232 million cash at close of Q3, 2022 will drop by $157.5 at close of Q4, 2024. This would leave it cash of ~$74.5 million at the start of 2025.

Conclusion

As is always true for developing biotechs that have yet to establish their commercial sea legs, there are two potential narratives for BioXcel. Bulls can seize on its multiple positive points of potential such as:

- Its rapid fire four year run from IND to launch of IGALMI;

- its growing traction in IGALMI’s launch as set out in Presentation slide 15 (“IGALMI: Poised for Success”) emphasizing why IGALMI’s 2023 results will bear no resemblance to those in 2022;

- its two new blockbuster IGALMI indications poised for 2023 NDA filings and 2024 approvals;

- Wall Street Analysts have an average price target of $46.40 — +46.56% upside.

Bears never want for ammunition; they always harken back to Wendy’s catch phrase, ‘Where’s the beef?”. Okay IGALMI has its approval. It has little in the way of revenues. Its initial approval with its supervision component carries the seeds of its downfall.

Hospitals have been dealing with challenging patients since time immemorial. They do not need to waste time and resources training staff in a whole new procedure. Late stage therapies are no more than blue sky until they are approved with a workable label and show their commercial merit.

As I write on 01/29/2023, I am conflicted on this name. It is set to trade at $31.66. It has an attractive <$1 billion market cap of ~$0.9 billion. I question whether its current approved indication will merit a significant premium to that.

However, as a speculative bet, its two phase 3 candidates are difficult to dismiss. I plan to keep this name on my watch list.

Be the first to comment