5./15 WEST

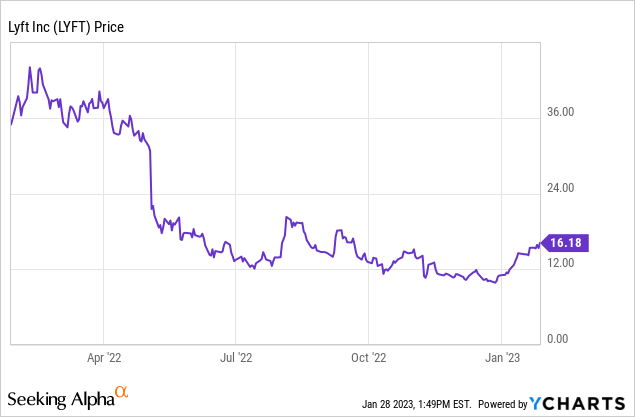

As the market continues its heady early 2023 recovery, I’m continually looking for beaten-down tech names that are well-poised for recovery. In my view, there continues to be a tremendous opportunity for long-term oriented investors to nab high-quality brands at a fraction of their former worths.

Lyft (NASDAQ:LYFT) is a name that has recently caught my eye. Long occupying the position of second fiddle to Uber (UBER), I think the ride-share company does offer several distinct advantages over its larger global cousin, namely in profitability. And in today’s more jittery market where tech bottom lines are being more closely scrutinized, I think that’s reason enough to lean in on Lyft.

Lyft is up nearly 40% in the year-to-date so far (though still down more than 50% from the past year). In spite of the furious January rebound, I still think there is plenty of opportunity for Lyft to climb higher. I am bullish on Lyft and think there is still a generous upside to go.

Here is my bullish thesis on Lyft:

- Ridership trends continue to grow. By now, we should recognize that the rideshare market is a “Coke and Pepsi” situation. Most riders don’t have a preferred app, switching between Uber and Lyft depending on wait times and prices. Lyft continues to grow active riders as well as revenue per rider; so even if its scale is dwarfed by Uber, it still has a place in the market.

- Rideshare will continue to be the way of the future as car ownership declines. I view the “sharing economy” as a trend that will continue to dominate the next several decades. Especially as supply-demand dynamics shot up the prices of cars during the late pandemic, and as the hassles of car maintenance and parking detract from the appeal of owning a car, more and more younger consumers will opt to forego car ownership and rely on transit or rideshare.

- Diversified modes of transport. Lyft also has Lyft Bikes and Lyft Scooters under its brand, as well as full-on car rentals, diversifying its revenue stream beyond simply rideshare and making Lyft a leader in last-mile transport.

- Focus on profitability. Lyft has boosted its contribution margins (it is known for often being more expensive than Uber; and that shows up in its bottom line), while a focus on opex reductions in the post-pandemic world has also led to tremendous EBITDA gains.

In my view, there’s plenty of appeal here.

Ridership trends are strong

We’ll caveat this one: Uber is showing much stronger post-pandemic rider recovery. In its most recent quarter, Uber reported >80% y/y revenue growth on >30% y/y bookings growth (with the gap explained by a favorable increase in take rates).

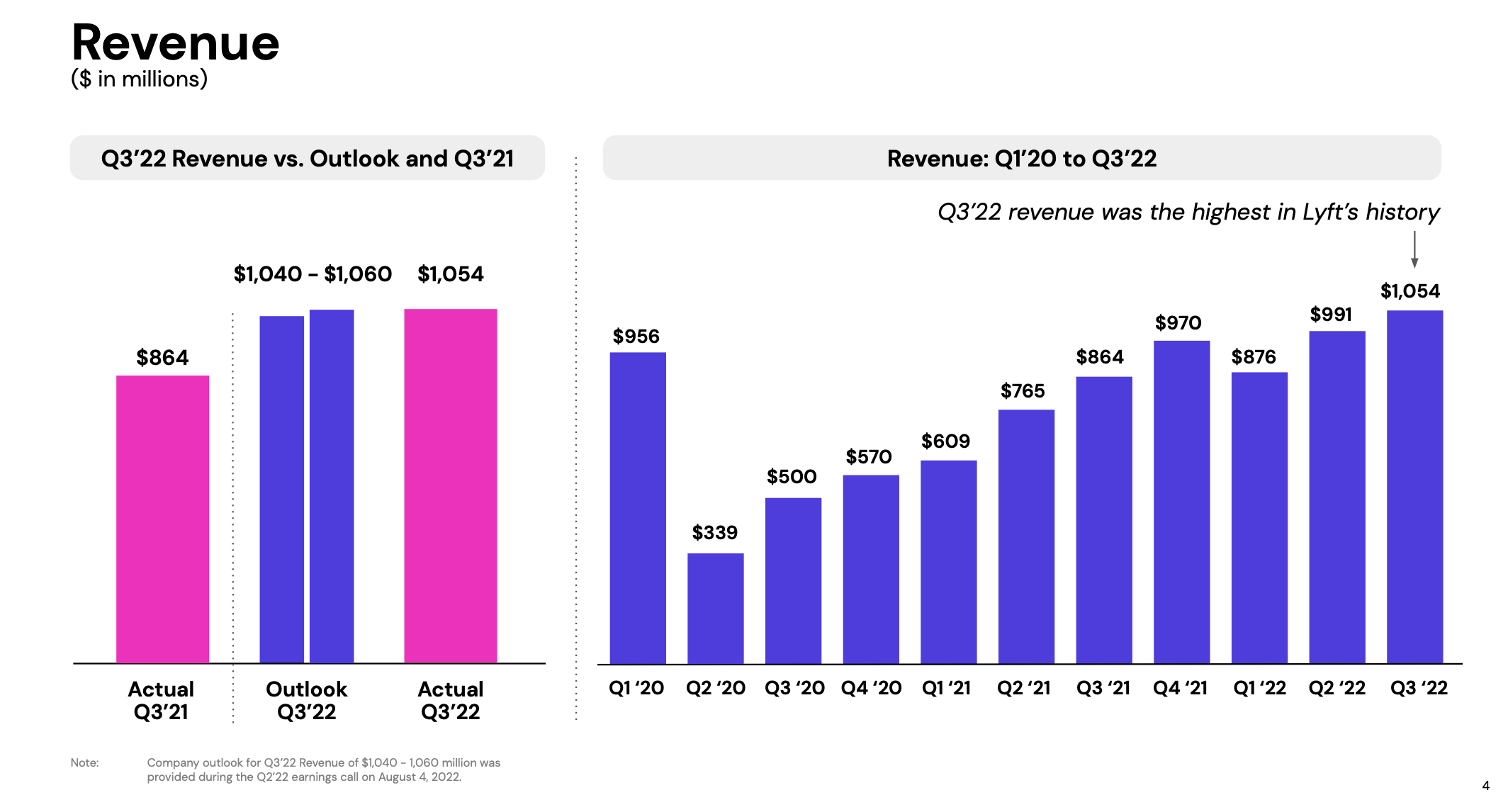

But that doesn’t mean that Lyft isn’t growing, either. In Q3, Lyft reached a record revenue of $1.05 billion, growing 22% y/y and on the high end of the company’s guidance.

Lyft revenue (Lyft Q3 shareholder deck)

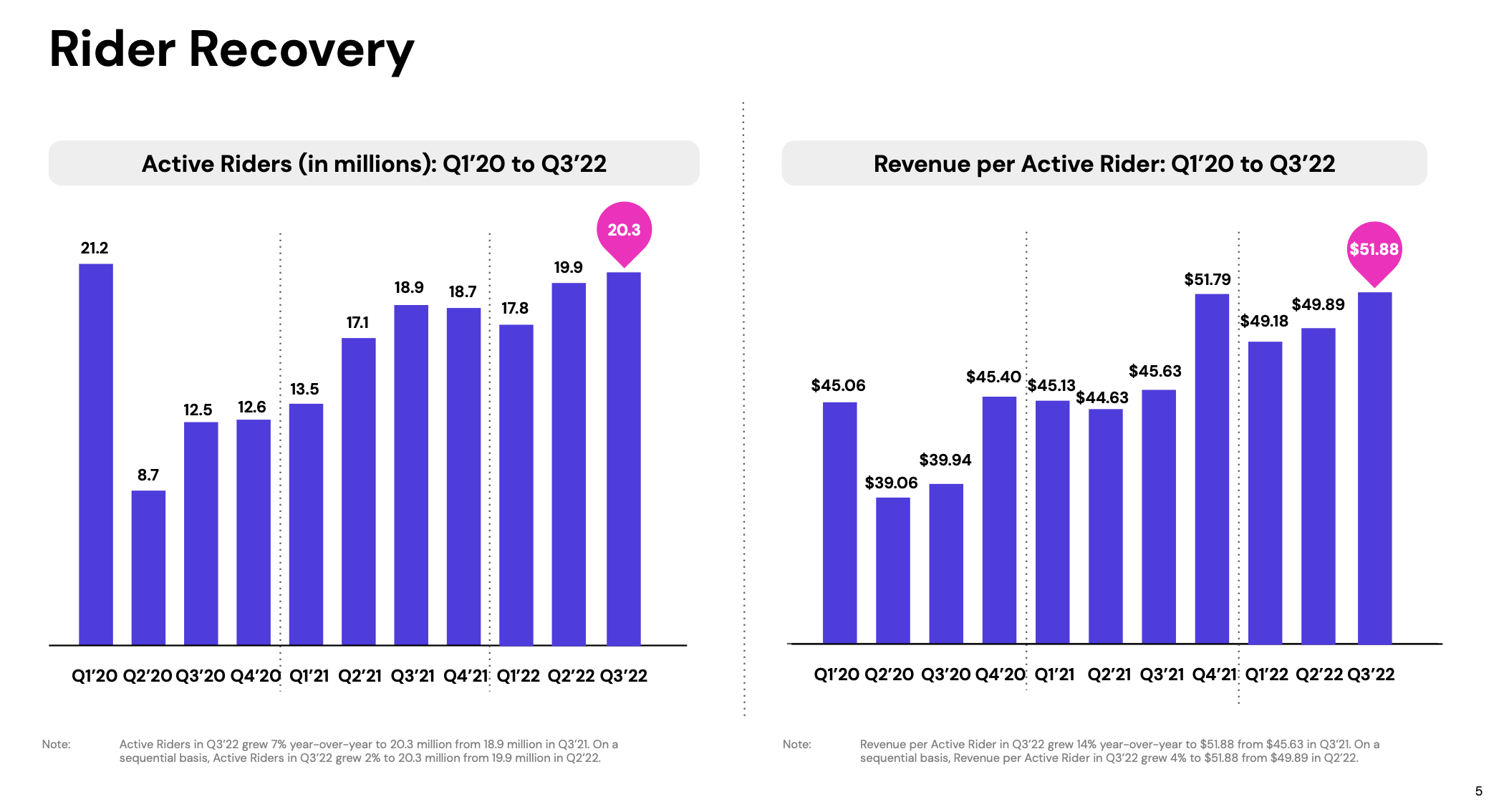

Active riders grew to 20.3 million, the highest since the pandemic began, and revenue per active rider also grew to a record of $51.88, driven by rate increases. The company has also done a good job at increasing service levels and driver availability, reducing wait times. The incentives for drivers to join the Lyft network have also gotten sweeter, and Lyft reported that average driver earnings per hour, including tips and bonuses, is up 7% y/y.

Lyft rider recovery (Lyft Q3 shareholder deck)

Profitability story is even better

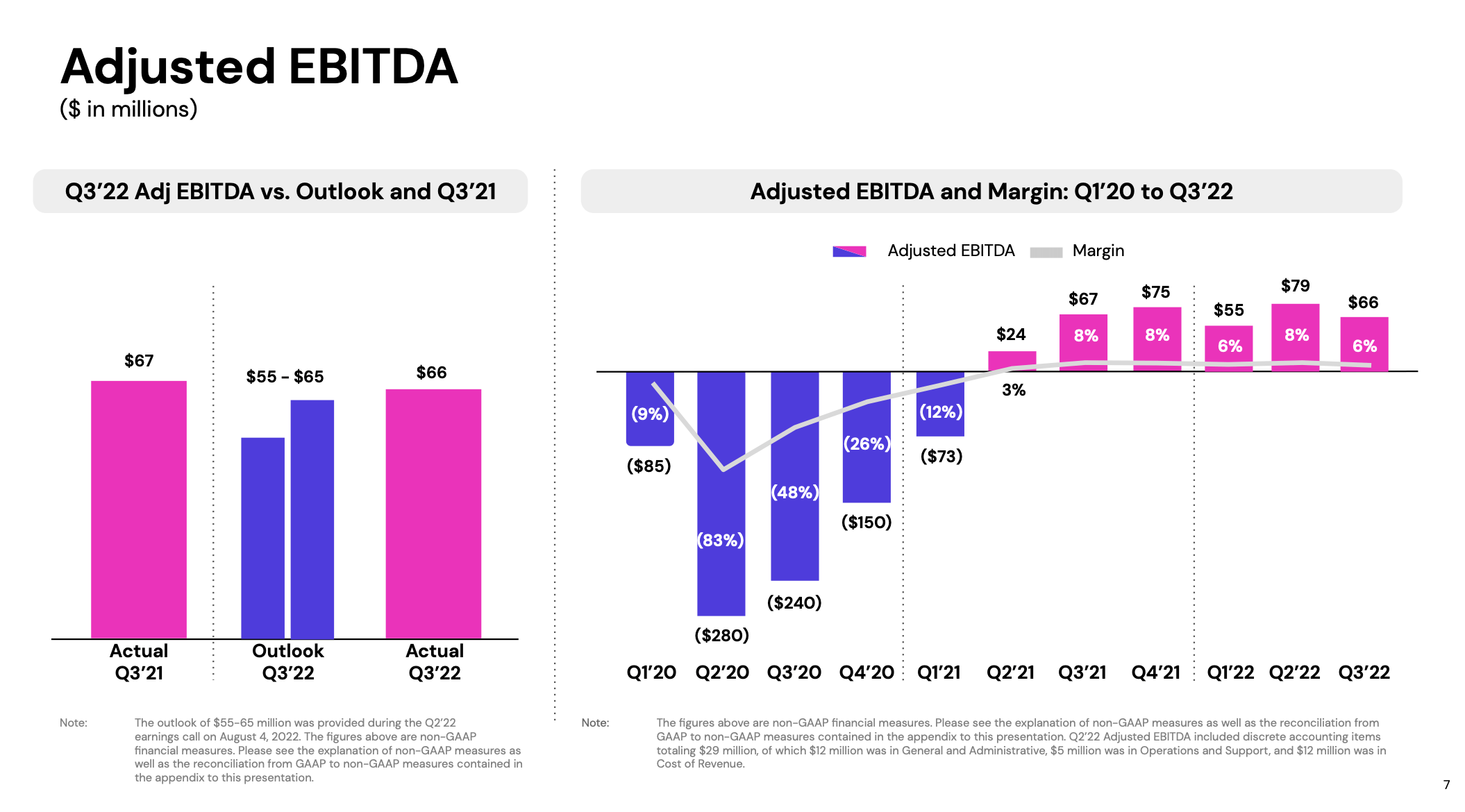

But here’s where, in my view, Lyft differentiates itself even more strongly than Uber: in profitability. Lyft notched a 6% adjusted EBITDA margin in Q3, hitting $66 million in adjusted EBITDA. While this represented two points of margin headwind y/y versus 8% in Q2, note that Uber only achieved a 2% margin in the same quarter.

Lyft adjusted EBITDA (Lyft Q3 shareholder deck)

The way we should think about it is this: Uber is more diversified in its growth efforts, leaning in on UberEats and (even more forward looking), Uber Freight. But Lyft has consolidated around its core rideshare business, which is throwing off generous amounts of EBITDA.

Macro headwinds have also driven Uber to review its expense portfolio, similar to other tech companies. Per CEO Logan Green’s remarks on the Q3 earnings call:

First, on headcount. Earlier this year, we significantly slowed and then froze new hiring. Last week’s action reflected a continuation of our commitment to carefully manage our team size and expenses in this environment. One focus was to remove management layers to accelerate decision-making and execution. It was a hard decision, but we’re confident that it’s the right step for the business.

Second, operating expenses. Starting in Q2, we reduced various operating expenses, inclusive of professional services and limited discretionary spending, particularly related to marketing. Third, our real estate. Since many team members now enjoy working remotely, we are reducing our office footprint and cutting related real estate costs by approximately half. These actions go hand in hand with the continued prioritization and streamlining of our highest ROI initiatives that will further enable greater operational efficiency and speed.”

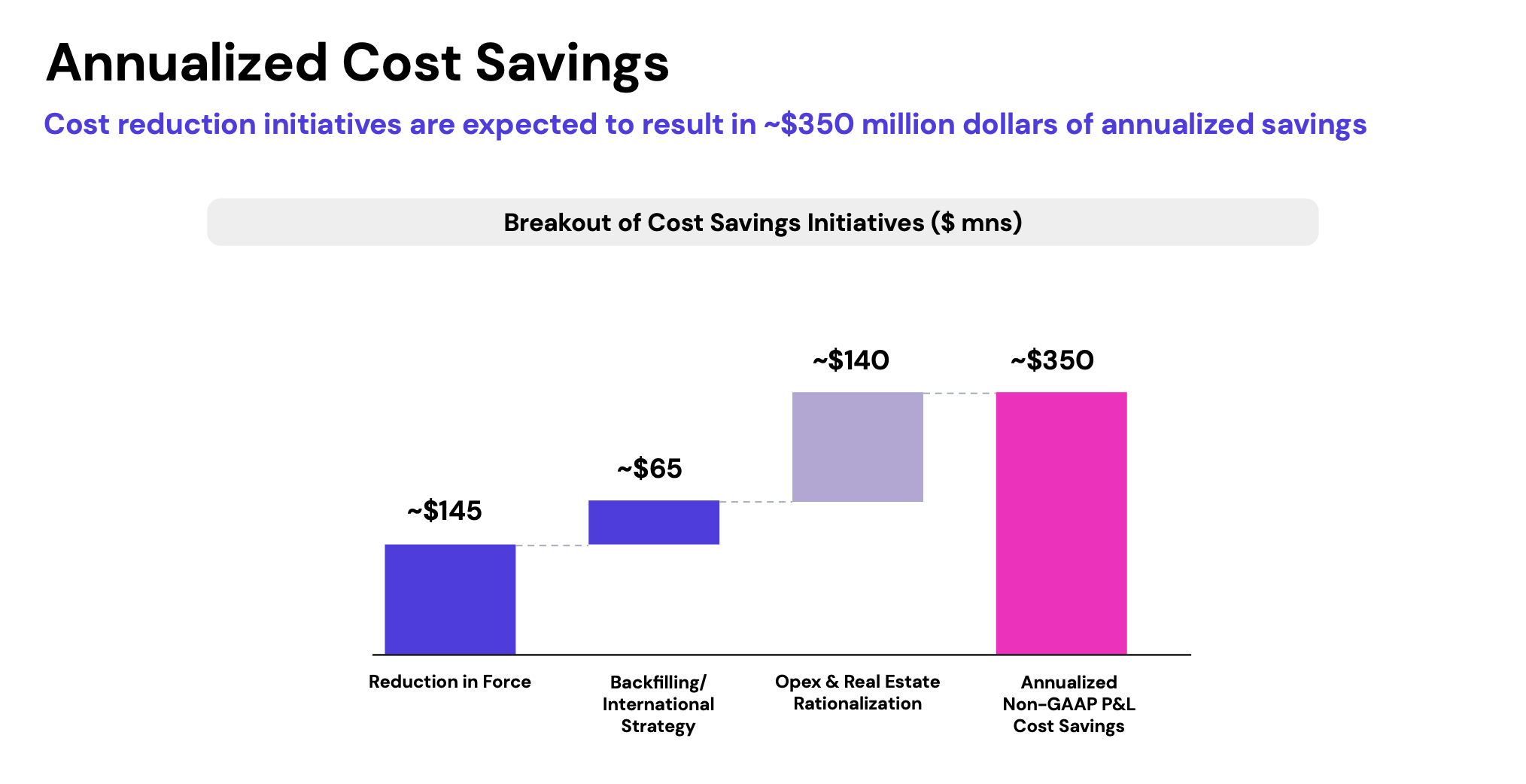

Overall, the company has eliminated $350 million in annualized run rate savings:

Lyft cost savings (Lyft Q3 shareholder deck)

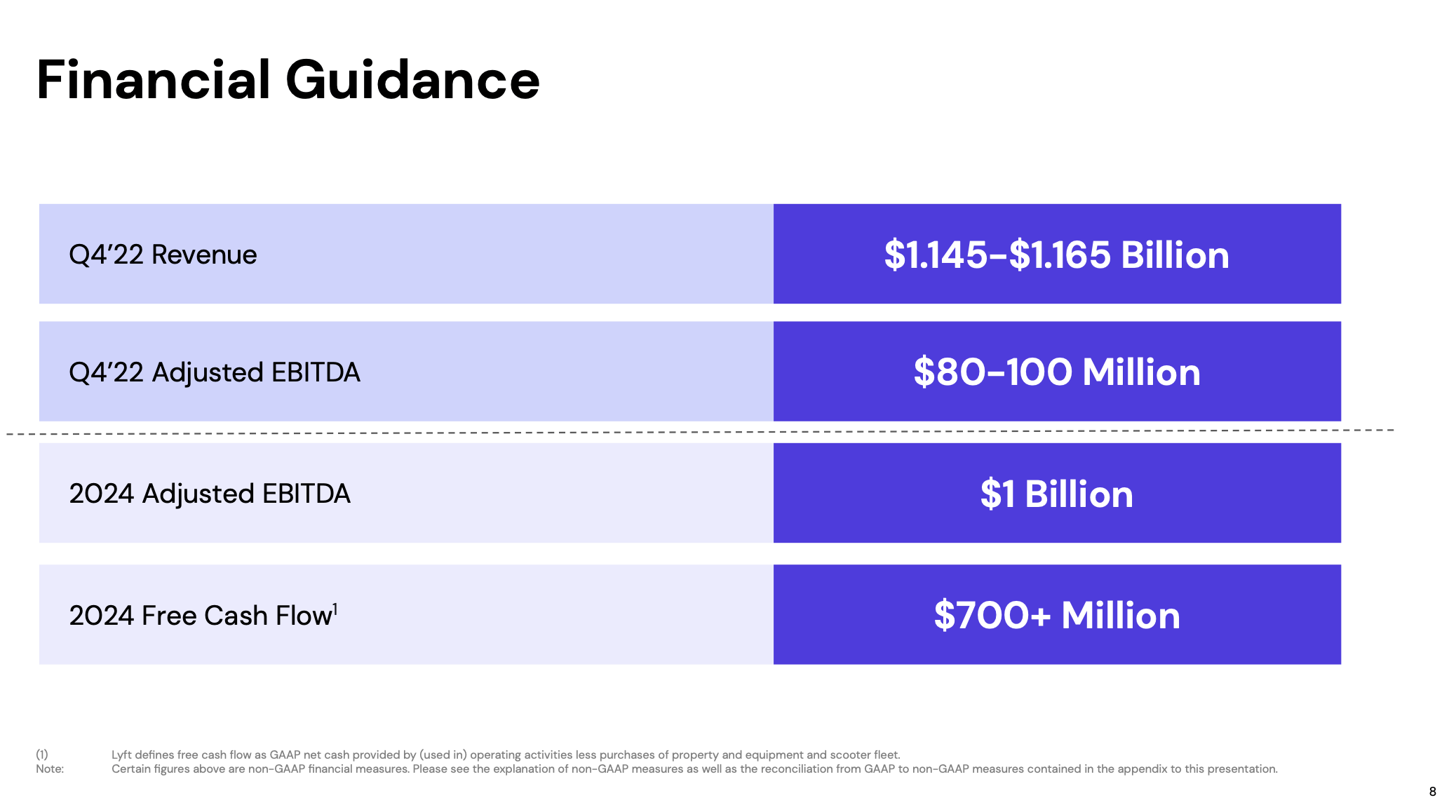

And looking ahead to 2024, Lyft is pointing to $1 billion in adjusted EBITDA and $700 million in free cash flow.

Lyft guidance (Lyft Q3 shareholder deck)

Valuation and key takeaways

The main draw to Lyft: the company can be quite reasonably valued on its bottom-line metrics. At current share prices near $16, Lyft trades at a market cap of $5.84 billion (Uber, by the way, is currently trading north of $60 billion). After $1.78 billion of cash and $814.7 million of debt on Lyft’s most recent balance sheet, the company’s resulting enterprise value is $4.88 billion.

This puts Lyft at incredibly modest multiples of:

- 4.9x EV/FY24 adjusted EBITDA

- 7.0x EV/FY24 free cash flow

As has often been the case in last year’s market downturn, overwrought pessimism has taken Lyft’s valuation down to unreasonably low levels. As long as we believe that Lyft will continue to gain its share of growth in the rideshare market, and as long as the company continues the opex discipline that it kicked off this year, I see a tremendous opportunity for Lyft to climb.

Be the first to comment