zorazhuang

Both Antero Midstream (NYSE:AM) and Energy Transfer (NYSE:ET) are midstream businesses that offer high dividend yields. ET has an investment grade balance sheet while AM issues a 1099 tax form (instead of the K-1 that ET issues) and has greater concentration in natural gas related midstream infrastructure. In this article, we will compare them side by side and offer our take on which one is a better buy.

Antero Midstream Vs. Energy Transfer – Balance Sheet

ET enjoys an investment grade credit rating (BBB-) from S&P, which is evidence that their balance sheet is quite strong at the moment. AM has a mere BB credit rating from S&P, which – though technically a junk credit rating – betrays what we believe is actually a pretty strong situation for it financially.

ET has been making impressive progress towards improving its balance sheet and even earning a credit rating upgrade in the not-too-distant future. On its latest earnings call, management stated that they expected to achieve their long-term leverage ratio target of between 4x and 4.5x by year-end 2022. Furthermore, with current liquidity of $2.32 billion and several billion dollars of free cash flow being generated each year, ET has plenty of liquidity to address upcoming debt maturities – of which it plans to pay down as much as it can – as well as pursue growth projects and growing its distribution.

AM, meanwhile, is also moving aggressively to pay down debt now that its growth CapEx is declining substantially and its new projects are coming online. As a result, it is gushing free cash flow after being free cash flow negative for a period of time and is taking advantage of this to pay down debt. Eventually it expects to achieve credit rating upgrades, and once it reaches its long-term target of 3.0x leverage (likely sometime in 2024), it hopes to potentially begin growing its dividend per share and/or buy back shares.

Moreover, with no debt maturing before 2026, AM is in excellent shape to opportunistically deleverage and position itself for long-term shareholder value creation.

Antero Midstream Vs. Energy Transfer – Business Model

ET clearly has a larger asset portfolio than AM with one of the best-diversified midstream portfolios in North America. That said, despite their size differential, both businesses are fairly resistant to commodity prices thanks to deriving the vast majority of their EBITDA from fixed-fee, take-or-pay pipeline contracts.

ET generates EBITDA from five different midstream subsectors, each of which generates less than or equal to 30% of its total EBITDA. This makes it resistant to commodity price volatility not only in the short-term, but also positions it to weather any major divergence in demand and pricing among individual energy commodities.

Furthermore, ET services every one of the United States’ major production basins, indicating the breadth of its pipeline network and the organic growth opportunities and competitive advantages that come with it.

AM, meanwhile, has a much smaller and more focused footprint with only a few hundred miles of pipelines and nearly all of its business coming from a single counterparty (Antero Resources (AR)). That said, it benefits from the stability that comes with the multi-decade production profile underpinning its assets and is well-aligned economically with AR, so shareholders can still sleep pretty well at night. AR is also deleveraging rapidly and is on the verge of achieving investment grade credit rating status from S&P, which will be a major boon to AM’s risk profile.

Antero Midstream Vs. Energy Transfer – Dividend/Distribution Outlook

ET is likely to hike its distribution substantially this next quarter – or at some point this year at the very least – to return the distribution to its $1.22 annualized rate. Beyond that, the distribution growth profile is less certain. While its distribution coverage ratio in 2023 is expected to be an impressive 2.15x – even assuming a $1.22 annualized distribution in 2023 – ET has a lot of alternative uses for that cash, including paying off debt as it matures in the coming years as well as funding numerous organic and inorganic growth opportunities.

With Kelcy Warren and his voracious appetite for empire building still looming large as the largest single unitholder and the Chairman of the Board, it is unlikely that ET will revert to aggressive unit repurchases and distribution growth moving forward. Instead, we expect modest distribution growth beyond the $1.22 annualized level and the majority of cash flow to be directed towards debt reduction and growth investments.

AM, meanwhile, has virtually assured investors that it will not grow its dividend this year and quite possibly not next year as it does not anticipate reaching its long-term leverage target until towards the end of 2024.

That said, with the dividend expected to be covered 1.69x by distributable cash flow in 2023 and DCF per share expected to increase moving forward due to a combination of interest expense reduction and organic growth in DCF per share over that span, it is very possible that the dividend will grow meaningfully once the leverage target is reached.

Antero Midstream Vs. Energy Transfer – Track Record

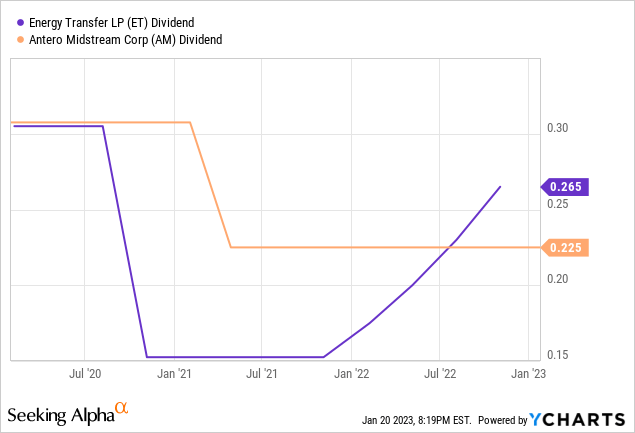

Neither business has much to brag about when it comes to track record, as ET and AM have both slashed their payouts in the not-too-distant past:

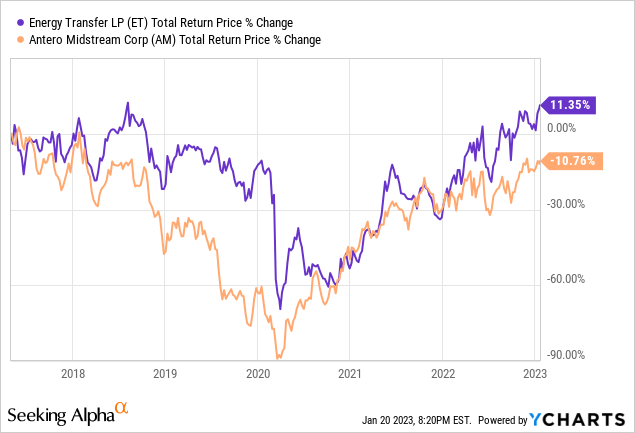

That said, ET has meaningfully outperformed AM since AM went public as its own entity:

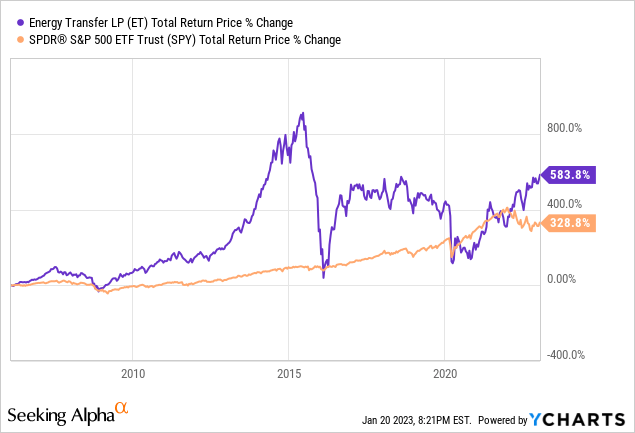

ET has also generated attractive, market-beating total returns for unitholders since going public many years ago:

Antero Midstream Vs. Energy Transfer – Risks And Catalysts

AM is a concentrated bet on a single counterparty, a single geographic region, and largely a single energy commodity (natural gas, though it also has a water business), whereas ET is more of a diversified bet on the broader midstream sector. As a result, AM’s risk profile is definitely higher than ET’s.

In the short-term, however, neither business is that risky given that they generate pretty stable energy-price resistant cash flows. However, over the medium to longer term if energy faces a sustained downturn in pricing and/or demand, both businesses would likely suffer considerably as recontracting rates would probably be weak in such an environment and some counterparties may default on their contracts.

Antero Midstream Vs. Energy Transfer – Valuation

A quick look at the valuation metrics appears to give ET the edge, as it is clearly cheaper on an EV/EBITDA and P/DCF basis and also pays out a meaningfully higher dividend yield than AM does. That said, both have similar discounts relative to their historical average EV/EBITDA multiples, with AM trading at just 83.3% of its five-year average and ET trading at 87.6% of its five-year average.

|

Valuation Metric |

AM |

ET |

|

Dividend/Distribution Yield |

8.15% |

9.64% |

|

EV/EBITDA |

9.06x |

7.72x |

|

EV/EBITDA (5-Yr Avg) |

10.87x |

8.81x |

|

P/23E DCF |

7.38x |

4.85x |

Investor Takeaway

Both AM and ET look like attractive buys at the moment, with each trading at a discount to its historical EV/EBITDA average and offering attractive and safe yields.

However, when picking between the two, we strongly favor ET given that it has greater distribution growth potential in the near term, its business model is more diversified and less dependent on another entity (like AM is with AR), and also trades at a cheaper EV/EBITDA and P/DCF multiple while also offering a higher yield. As a result, we hold ET as one of our largest positions at High Yield Investor and have high conviction in its future prospects.

The biggest reasons why someone might prefer AM over ET is simply because:

(1) It is more of a pure play on natural gas.

(2) It issues a 1099 tax form as a C-Corp, in contrast to ET’s K-1 tax form since it is an MLP.

High Yield Investor Portfolio

Be the first to comment