Peach_iStock

Introduction

The debt limit is the total amount of money that the United States government is authorized by Congress to borrow to meet its existing legal obligations, including Social Security and Medicare benefits, military salaries, interest on the national debt, tax refunds, and other payments. If the U.S. Treasury reaches its debt ceiling and runs out of cash, it would be unable to pay all its bills. A failure to pay bills would represent a default by the U.S. Government.

A government default is different from a government shutdown. The latter occurs whenever congressional appropriations bills are not passed to fund programs. The U.S. Government has not defaulted since just after the War of 1812. There have, however, been 10 shutdowns since 1980 with the most recent occurring in the 35-day shutdown of 2018-2019. That shutdown was caused by a dispute over funding for an expansion of the U.S.-Mexico barrier and is the longest shutdown in history.

My previous Seeking Alpha article noted that the U.S. Government would soon reach its debt ceiling. This article explores the behavior of stocks, gold, silver, long-term interest rates, and the U.S. dollar in 2011 following the first official warning of a debt ceiling problem until its resolution. Investors should find the information presented helpful in making investment decisions as Congress once again copes with the debt ceiling issue.

History

The first federal debt limit was set at $45 billion in 1939. Since 1960, Congress has acted 78 separate times to permanently raise, temporarily suspend, or revise the definition of the debt limit. These actions were taken to prevent the U.S. Treasury from defaulting on financial obligations. Interestingly, the debt ceiling has never been lowered!

Among all prior encounters with the debt ceiling, 2011 stands out because of its extreme bitterness and striking similarities between then and now. On January 6, 2011 Treasury Secretary Timothy Geithner sent a letter to Senate Majority Leader Harry Reid requesting an increase in the $14.294 trillion debt limit. In that letter Geithner stated the federal debt ceiling would be reached between March 31 and May 16, 2011.

Twelve years and one week later, on January 13, 2023 Treasury Secretary Janet Yellen sent a letter to House Speaker Kevin McCarthy saying that the U.S. Treasury expected it would reach the debt limit of $31.281 trillion by July 1, 2011. The debt ceiling was, therefore, raised by $16.987 trillion or $1.416 trillion per year from 2011 to 2023.

Political Control

The 2011 and 2023 debt crises emerged shortly after mid-term elections when the Republican Party re-gained control of the House of Representatives, while the Democrats retained control of the Senate. The crises also emerged during the second year of a new Democrat President’s first term in office after he replaced a Republican President. In 2010 Obama had replaced Bush, and in 2022 Biden replaced Trump.

There were 242 republican members of the House in 2011, which was the largest number of republicans since the 80th Congress (1947-1949). By contrast, the republican majority in the House is much smaller today at 222.

Chronological Events of 2011

In a February 3, 2011 letter to Senator Toomey, Treasury Secretary Geithner re-iterated the need to raise the debt ceiling. He also sent letters requesting an increase in the debt ceiling to Congress on April 4 and May 2, 2011. The April 4 letter noted the debt ceiling would be reached between April 15 and May 31, 2011.

The May 2 letter stated he would suspend any new debt issuance beginning May 16, 2011 unless Congress raised the debt ceiling. In that letter he also declared a debt issuance suspension period lasting until about August 2, 2011 and the fact that Treasury was prepared to take certain extraordinary measures. On July 1, 2011, the U.S. Treasury declared it had exhausted its borrowing capacity and on July 15, Treasury announced it suspended reinvestment in the Exchange Stabilization Fund.

Congressional Action

Despite the many warnings from Secretary Geithner, the first sign of Congressional action did not occur until May 24 when a bill (H.R. 1954) was introduced in the House to raise the debt limit. That bill was soundly defeated in the House by a vote of 37 to 318 on May 31, 2011.

On July 19, 2011 the House passed bill (H.R. 2560) that among other things increased the federal debt limit to $16.7 trillion. The House easily passed the bill by a vote of 234 to 190. The Senate, however, tabled that bill by a vote of 51 to 46 on July 22, 2011.

On July 25, 2011, legislation entitled the Budget Control Act was introduced in the House and Senate. Among other things, this legislation provided for an increase in the debt ceiling. A compromised version of this legislation (BCA; P.L. 112-125) was approved in the House by a vote of 269 to161 and in the Senate by a vote of 74-26. President Obama signed this legislation into law (BCA; P.L. 112-125) on August 2, 2011.

Under the new law, the debt limit was raised in three-steps. It was raised by $400 billion to $14.694 trillion on the date of signing. The ceiling was raised another $500 billion on September 22, 2011 bring the ceiling up to $15.194 trillion. A third and final increase of $1.2 trillion in the debt ceiling occurred in late December 2011 and brought the debt ceiling to $16.394 trillion.

Impact on Financial Markets

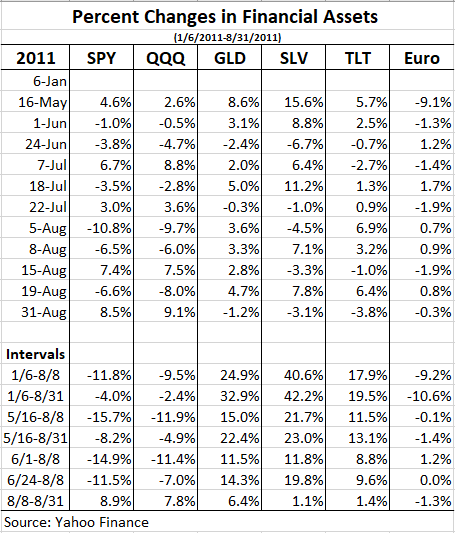

The impact that the 2011 debt ceiling drama had on the financial markets is shown in following exhibit. It shows the percentage changes in the prices of stocks, precious metals, bonds, and the U.S. dollar over various time intervals.

Yahoo Finance

Stocks are represented by SPY, which is the symbol for the S&P 500 ETF, and QQQ, which is the Invesco NASDAQ-100 Trust. Precious metals are represented in the exhibit by GLD, which is the symbol for SPDR Gold Shares, and by SLV, which is the symbol for iShares Silver Trust. Long-term bonds are represented in the exhibit by the symbol TLT, which is the iShares 20+ Year Treasury Bond ETF. The U.S. dollar measure used in the exhibit shows the amount of U.S. dollars required to buy one (1) euro.

Dates and intervals in the exhibit were selected based on volatility observed in charts and identifiable events that triggered movement in stocks. For example, one such event occurred on January 6 when Secretary Geithner sent his first letter to Congress alerting Speaker Reid about the debt ceiling problem. A second event occurred on May 16, which was the date Secretary Geithner set for issue suspension. A third event occurred on August 5 when Standard & Poor’s lowered the credit rating of U.S. Government debt from AAA to AA-.

Stock Performance in 2011

Data in the exhibit show that stocks began 2011 on a positive note. From the date of Geithner’s original warning letter (1/6/2011) until May 16 (the date the U.S. Treasury suspended new debt issuance, the S&P was up 4.6% and QQQ was up 2.6%.

Stocks then came under significant pressure as contention about the debt ceiling grew in Congress. From May 16 to August 8, the first trading day after the S&P lowered its Unites States credit rating, the S&P fell 15.7% and QQQ fell 11.9%.

Following the S&P down grade and the statutory increase in the debt ceiling, the stock market recovered. From August 8 to August 31 SPY rose 8.9% and QQQ rose 7.8%.

U.S. Treasury Bond Performance in 2011

Long-term interest rate headed lower at the start of 2011. From January 6 to May 16, 2011 the TLT rose 5.7%. That equated to an increase in price of ~$4 and a decline in the rate on U.S. Treasury bonds of about 20 basis points “BPS.” Bond yields continued to decline and bond prices rose in the immediate aftermath of the Treasury suspending issuance of new securities. In fact, TLT rose ~$2 from May 16 to June 1, 2011.

Bond rates rose and TLT fell in price as the debt ceiling debate heated up in Congress during June and July. As it became clear that any default was off the table, the decline in long-term interest rates accelerated and the price of TLT rose dramatically. From July 22 to August 19 TLT rose $11.75 or 16.2% and the long-term U.S. Government bond yield fell by ~ 30 basis points. By the end of 2011, TLT was trading at $93.38 and was up 37.3% from the date of Geithner’s original warning letter. The yield on long-term U.S. Government bonds declined in 2011 by ~70 basis points from 2.90 at the beginning of the year to 2.25% at the end of the year.

Gold and Silver Prices in 2011

Precious metal investors tend to prosper during troublesome times. It is, therefore, not surprising that gold and silver investors got excited and started buying when talk began about the U.S. Government defaulting on its debt.

In the time between Geithner’s original warning letter, January 6, and the actual suspension of debt issuance, May 16, GLD rose 8.6% and SLV rose 15.6%. From May 16 to August 31 GLD rose another 22.4% and SLV rose 23%. From the January 6 to the end of the month that the debt ceiling issue was laid to rest, August 31, GLD rose 32.9% and SLV rose 42.2%.

U.S. Dollar Performance in 2011

The U.S. dollar was under pressure early in 2011 versus the euro. In fact, it went from $1.298 USD per euro on January 6 to $1.4345 on June 1, 2011, representing a decline of 10.5% in the value of the dollar relative to the euro. Currency traders were either early in recognizing the severity of the debt ceiling Congressional crisis or they dismissed any chance of the U.S. defaulting on its debt, because after falling significantly in early 2011, the dollar mostly traded sideways as debate occurred in Congress.

On May 16 it took $1.4158 to buy one Eurodollar, and on August 8 it took $1.4171. From May 16 to August 8 the U.S. dollar, therefore, declined by only 0.1% versus the euro.

Conclusion

George Santayana, a Spanish philosopher, is credited with the aphorism, “Those who cannot remember the past are condemned to repeat it.” If the 2023 debt ceiling crisis is a repeat of the 2011 crisis then the price action of stocks, bonds, gold, silver, and the dollar observed in 2011 might serve as a road map for investors in 2023.

Based on the 2011 events, Secretary Yellen’s January 13, 2023 letter to Speaker McCarthy is a wake-up call for what is likely to be an extremely contentious period in Congressional history. Investors should expect the debt ceiling issue to remain unresolved until at least the third quarter of 2023.

The inability of the U.S. Treasury to issue debt will weigh on the economy. Treasury will be unable to fund new legislative programs and will also have to prioritize payments.

Consumer confidence is likely to diminish with the increasing level of acrimony in Congress. At this moment, relatively few people are either aware of or concerned about the debt ceiling issue. By spring the seriousness of the debt ceiling issue should capture the attention of the media and the electorate and be front page news. If 2023 is a repeat of 2011, Congress will start seriously addressing the debt ceiling in May and will spend at least two months before resolving the issue.

From the date in 2011 that Treasury Secretary Geithner alerted Congress to the debt ceiling problem (January 6) until shortly after the issue was resolved (August 8), silver offered the highest return with SLV up 40.6%. The second highest return was recorded by gold (GLD), which was up 24.9%. Long-bonds had the third highest return during that period as reflected by TLT being up 17.9%.

During that same period of time, stocks and the U.S. dollar suffered. Spy fell 11.8% from January 6 to August 8, 2011, while QQQ fell 9.5% and the U.S. dollar fell 9.2%.

Based on actual 2011 results, gold, silver, and bond prices should increase in 2023 while Congress contends with the debt ceiling issue. On the other hand, stocks and the U.S. dollar are likely to decline.

Be the first to comment