Poike

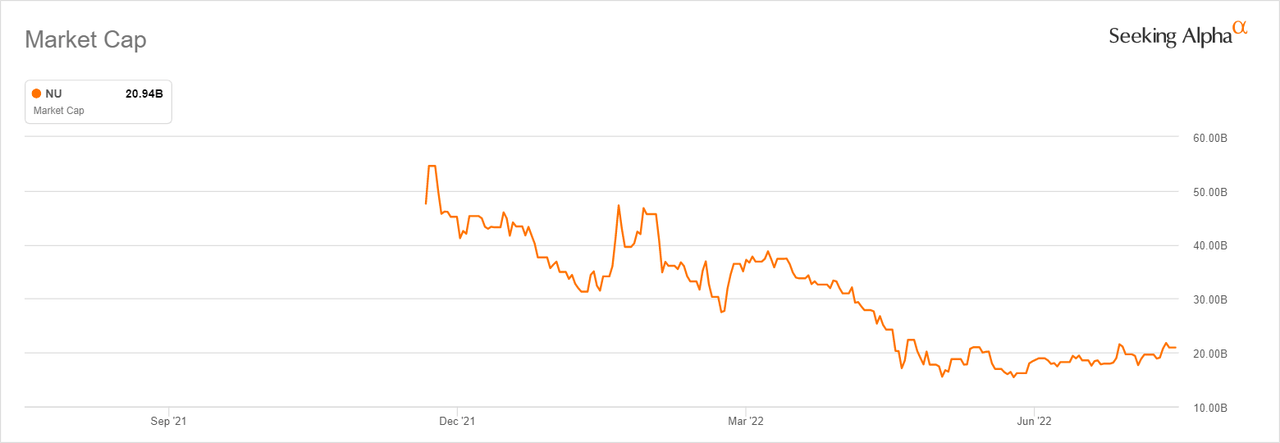

Nu Holdings Ltd. (NYSE:NU), the largest digital bank by market value and customer base in Brazil, was one of the most hyped IPOs of 2021. The stock hit a market cap of around $50 billion on December 9, 2021, its first day as a publicly traded company. It, however, tumbled in the first half of 2022 and currently has a market cap of around $20 billion, around 60% off its IPO highs.

NU market cap since IPO (Seeking Alpha)

That said, NU seems to have stabilized at the $20 billion market cap level for the past three months. This is fair grounds to speculate that the bottom is in, particularly if you consider the positive shift in market sentiment signaled by the strong rally in indices tracking the S&P 500 and Nasdaq 100 over the past two months. Tellingly, NU rallied 20% following its positive Q2 results on August 15. We see this as the beginning of a new bullish chapter for the stock and recommend accumulating it for potentially exciting returns in the long term.

Revisiting the bull case

Founded in 2013, NU is an app-based provider of credit cards (its core product), current accounts, personal loans and other financial services. It operates in the LATAM region. It primarily serves the consumer market, but in recent years, introduced offerings for small and medium-sized enterprises. NU’s main market in terms of geographic footprint is Brazil, where it launched in 2013 and as at Q2 2022 served 36% of the adult population, as per its Q2 2022 earnings presentation. In recent years, it ventured into Columbia and Mexico. Overall, it had around 65 million customers in all markets at the end of Q2 2022, majority from Brazil.

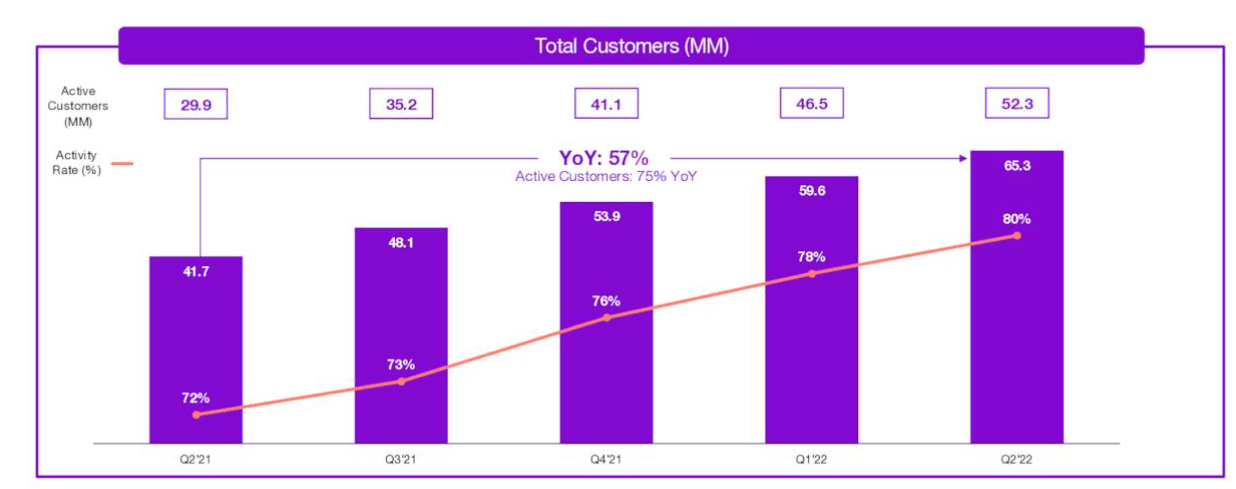

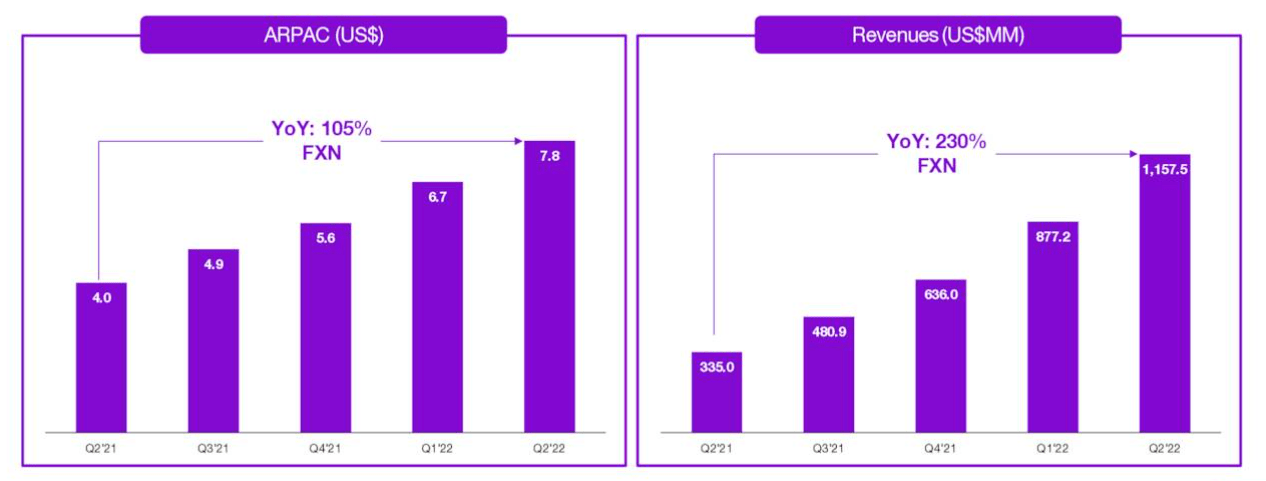

The foundation of NU’s bull case is the fact that it has been able to consistently grow both the number of customers as a whole as well as the total percentage of active users. This has translated into revenue growth and an increase in the average revenue per active user, as the below screenshots from its latest earnings presentation illustrate.

Customer growth and percentage of active users since Q2 2021 (Nubank)

Average revenue per active user and revenue have been trending up since Q2 2021 (Nubank)

Importantly, NU has been able to grow its top line while achieving greater efficiencies over time. Its average cost per active customer was $1.4 in 2019, $1.2 in 2020 and $0.80 in 2021, according to its Annual Report for 2021.

NU also has a strong brand. Its Annual Report states that it received a Net Promoter Score, or “NPS,” of 90 in Brazil and 94 in Mexico. The company claims that this score exceeds incumbent banks and all other major local financial technology companies. The company further claims to have become the primary banking relationship for over 55% of its active customers who had been with it for more than 12 months as of December 31, 2021.

The main risk with NU is profitability. Its retained earnings at the end of Dec 2021 stood at negative $336.5 million. That said, NU Brazil reported positive adjusted net income (non-GAAP measure) of $56.5 million in 2021. For a business at the relatively early stage of growth NU is in (and in a young industry), adjusted net income and other non-GAAP variants may be acceptable for some time. However, they are not sustainable measures of success in the long term.

Positive net income is the best indicator that a business model is successful over time. It’s, therefore, encouraging that, moving into 2022, NU’s Brazil unit has become profitable on a net income basis. Its latest earnings show that for the first half of 2022 its net income on a GAAP basis was $13 million for the Brazilian unit. This is certainly the beginning of a new chapter for the business. What NU now needs to do is ensure it sustains its topline growth and maintains efficiency to grow its net income even further.

Sustaining positive net income

NU has historically grown revenues and users rapidly. We believe it can sustain this strong growth and maintain its positive net income. Its credit card customers are highly engaged and, even in a macroeconomic environment characterized by inflation and recessionary risks, spent more in the first two quarters of 2022.

Purchase volumes on NU credit cards have been rising (Nubank)

In Mexico and Columbia, where NU has been aggressively expanding, the company has now emerged as the number one issuer of new cards in both countries. This is according to its latest earnings presentation.

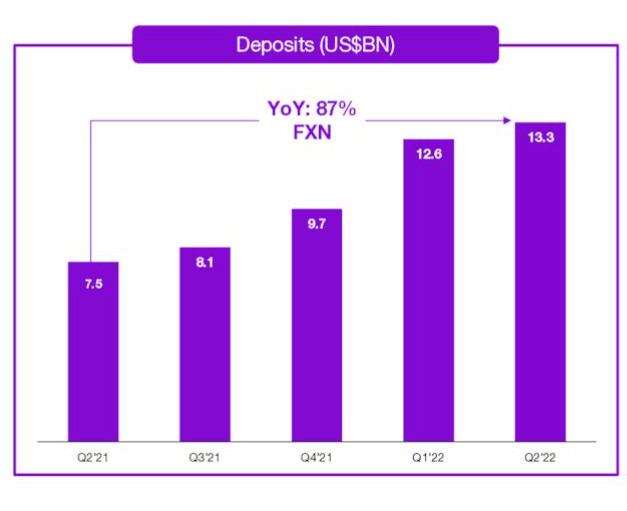

NU has equally been successful in other verticals, including personal loans, savings and insurance. Personal loans, for example, accounted for $2.1 billion or 23% of its total loan book in Q2 2022 versus $600 million or 13% of its loan book in Q2 2021. This rapid growth in the space of just one year demonstrates just how effective NU is at bringing new products to market at scale. Another pointer to this key management strength is the pace at which NU has been able to mobilize customer deposits.

NU customer deposits have increased 87% year on year as at Q2 2022 (Nubank)

Key risks

NU is a good investment, but it’s important to be aware of the risks. The first is that the fintech sector in Brazil and LATAM generally is drawing closer regulatory scrutiny because of the record level of household debt. As one of the largest fintechs in the LATAM region, it goes without saying that regulatory action in Brazil, Mexico or Columbia will necessarily target NU. Much of what could or could not happen when it comes to action by regulators is the subject of speculation. However, from an investment standpoint, increased regulatory scrutiny normally puts downward pressure on valuations in the targeted sector.

The second risk worth elaborating on is the fiercely competitive LATAM fintech market. Fintech startups in the LATAM region attracted over $13.2 billion in venture capital in 2021 compared to $2.3 billion in 2020, a report on Tech Crunch notes. Even Big Tech firms like Meta Platforms (META) are moving into the LATAM fintech market, a further indication of how crowded the market is getting. In March, Brazil’s central bank cleared WhatsApp to start transfers between Visa and Mastercard cardholders under the Facebook Pay Program.

There’s no denying that there is a huge opportunity leveraging technology to bring banking and financial services to the underserved working class. But when everyone starts doing it and new investments flood the market, opportunities for sustained strong growth and meaningful profitability quickly dwindle. Against this backdrop, NU must work really hard to differentiate itself and protect its margins. This could end up draining resources and slowing the profitability journey.

All things considered, however, the opportunities outweigh the risks and NU is a good buy, particularly in view of the stock’s lackluster H1 performance and the improving overall market sentiment.

Be the first to comment