imaginima

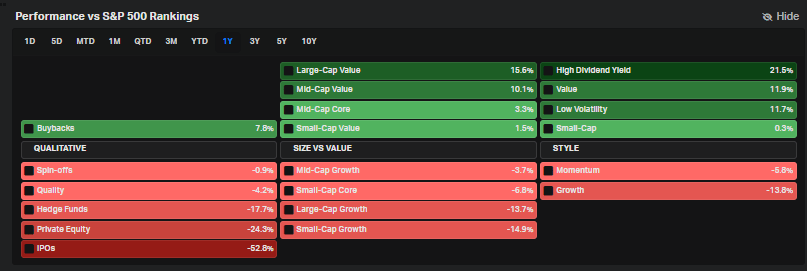

SPACs and IPOs peaked more than a year ago, but the last 52 weeks have been particularly brutal for investors in once-hot, not-freezing cold new-issue companies. The IPO factor, as measured by the Renaissance IPO ETF is down more than 50% on a relative basis to the S&P 500 since late November 2021 when interest rates were near record lows and cheap capital was everywhere. What a difference a year makes. Moreover, a popular thematic play was to own robotics companies. One such company that went public via a SPAC has seen its stock price get slaughtered. Is there a value case to be made for Berkshire Grey?

IPOs, SPACs Struggled YoY vs S&P 500

Koyfin Charts

According to Bank of America Global Research, Berkshire Grey (NASDAQ:BGRY) is an industrial robotics and artificial intelligence software company. The company was incorporated in 2013 and went public via a special purpose acquisition company (SPAC) in 2021. The company focuses on online order fulfillment and store replenishment operations across five verticals: retail, e-commerce, 3PL, parcels, and grocery.

The Massachusetts-based $239 million market cap machinery industry company within the Industrials sector has negative trailing 12-month GAAP earnings and does not pay a dividend, according to The Wall Street Journal.

Berkshire recently beat earnings estimates in its Q3 report earlier this month, but shares have not seen a recovery. Earlier this year, the firm partnered with FedEx (FDX) to expand strategic relations for robotic automation solutions. That corporate agreement was a positive, but share dilution was a key risk. More recently, an equity purchase agreement with Lincoln Park Capital improves the liquidity situation at Berkshire Grey, but financial flexibility remains a concern with this struggling Industrials stock.

BGRY could be an effective speculative way to play warehouse automation, e-commerce trends, and even onshoring via its processes and technologies in a post-COVID world. Berkshire Grey is well-positioned with technical expertise in picking & sorting automation, including software and hardware solutions. Much depends on how the firm can scale up in a quickly changing economic landscape while beating out other tech startups. A primary near-term risk is liquidity and equity-holder dilution.

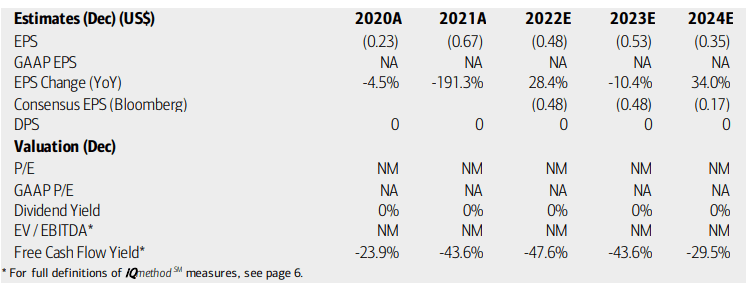

On valuation, analysts at BofA are bullish on BGRY’s prospects. They see earnings, while negative through 2024, as improving from 2021’s level. Investors and prospective owners must monitor free cash flow for signs of improvement so that the company can meet its financial obligations.

The Bloomberg consensus forecast is close to what BofA sees. BofA has a $4 price target based on an eventual 7x EV/EBITDA multiple once per-share profits turn positive by then. The firm grew sales by 26% on an annual basis in its third quarter, so there is a growth case to be made, and BofA sees BGRY turning free cash flow positive by 2025. Overall, with a forward price-to-sales ratio under 4, I think this could be worth a flyer on fundamentals.

Berkshire Grey: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

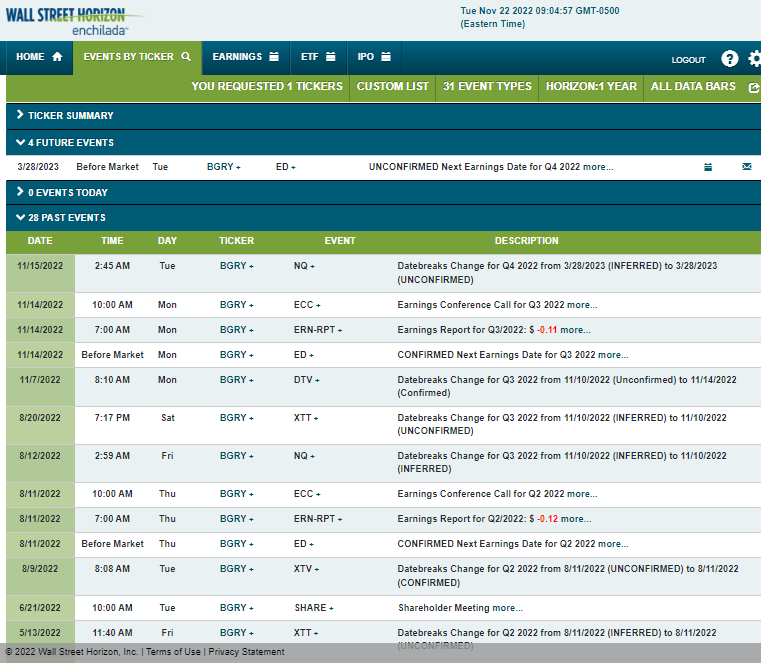

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Tuesday, March 28, before market open. The event calendar is light until then.

Corporate Event Calendar

Wall Street Horizon

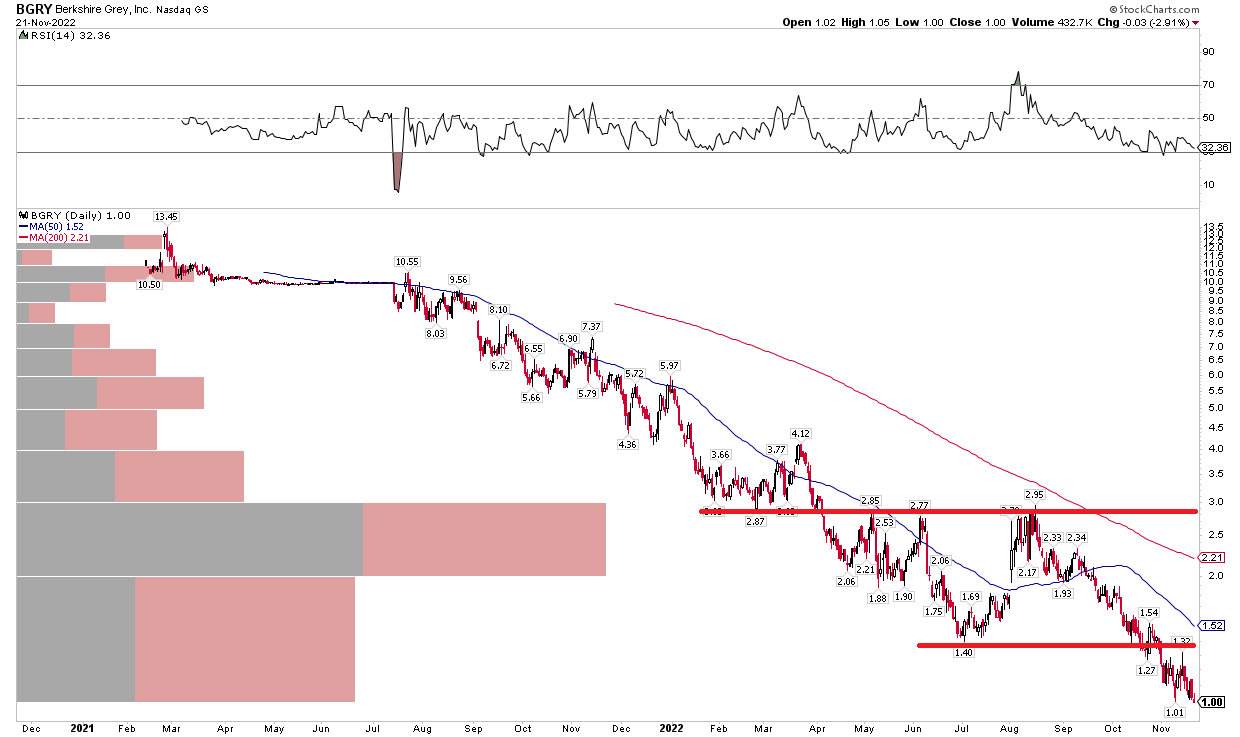

The Technical Take

BGRY is down more than 90% from its high in early 2021 shortly after the IPO. Shares rallied to near $3 following the FedEx partnership news, but it has been a brutal stretch for the bulls since then. Even the Lincoln Park partnership and decent earnings recently have done little to improve the technical picture.

The stock is near all-time lows and $1.32 to $1.40 is the first resistance. There’s more bearish resistance just below $3. Meanwhile, the long-term 200-day moving average is sharply negatively sloped and the RSI momentum reading is in bearish territory. Overall, the chart is quite poor. A move above $1.40 and eventually the 200-day moving average would help improve the risk/reward picture.

BGRY: No Let Up In the Downtrend

StockCharts.com

The Bottom Line

The growth story and broad trends support Berkshire Grey’s business, but liquidity and technicals make me cautious for now. I will look forward to revisiting this one in a few months – a move above $1.40 could warrant a bullish position. Until then, there’s just too much risk.

Be the first to comment