Tryaging

Overview

The bull case for Bentley Systems (NASDAQ:BSY) is based on the increasing demand for infrastructure investment and the need for digital infrastructure engineering to bridge funding gaps in the sector. With global infrastructure investment estimated at $3.4 trillion and projected to grow, there will be many opportunities for private capital to invest in infrastructure projects. BSY’s solution can help to fulfill the needs of private infrastructure investors by providing digital twins and reducing the risks associated with such investments. Additionally, BSY’s services cover the entire life cycle of an infrastructure project, positioning the company as a solution provider in the design and engineering industries for large-scale civil construction projects.

Business description

Bentley Systems offers software for bridge analysis, construction, simulation and analysis, modeling, and geotechnical engineering.

More infrastructure needed in the future

In my opinion, there will be a lot of opportunities around the world in the coming decades as a result of the rate of new spending needed to meet the anticipated demands for infrastructure. In 2020, global infrastructure investment was estimated at $3.4 trillion, and it is anticipated to grow at a CAGR in the mid-single digits over the next few years. Many things, in my opinion, have contributed to the surge in infrastructure needs. Examples include the persistent growth of urban areas and the increasing urgency of adapting our infrastructure to the effects of climate change.

Behind this escalating expenditure on infrastructure, substantial resources are required. Considering the compelling IRR of such infrastructure investment, I believe it will attract many private capital to bridge this. Consequently, I believe that the need for digital infrastructure engineering will increase as a result of funding gaps in the infrastructure sector. Despite the fact that a lot of money from private sources has been set aside for infrastructure investment, a lot of it is just sitting there. As a fellow investor, I can say with confidence that these parties are looking for promising ventures that provide enough early predictability and ongoing transparency to entice them to commit capital. This is especially for infrastructure assets that carry many execution risks and projects have long duration.

In my opinion, the risks associated with investments can be minimized with the help of digital twins by satisfying the requirements of investors and living up to their expectations of development in digital workflows.

Infrastructure projects going digital

Although digital technologies have steadily enhanced manufacturing economics over time, owner-operators often insist on starting from scratch when developing an engineering plan, wasting valuable time and resources that could be better spent elsewhere. As a result, there are few possibilities for breakthroughs in lifecycle costs in construction-driven and operations-driven design.

More and more businesses in the infrastructure engineering industry are realizing the importance of digitizing their operations to improve their workflow efficiencies. The “industrialization” of infrastructure design and construction is the focus of new methods. One area of the construction industry that stands to benefit greatly from the advancements in industrialization is heavy civil earthmoving, thanks to the automation facilitated by digitally controlled machinery.

The argument for and necessity of infrastructure delivery industrialization seems compelling and inexorable to me. The result will be that owner-operators use analytics gleaned from their operational assets to steer the supply chains of the projects they oversee, ensuring that digital twins are delivered alongside physical assets. For this reason, I think the success of industrialization will spur the introduction of 4D digital workflows.

Comprehensive solutions to cover the entire lifecycle

BSY’s services encompass the entirety of an infrastructure project’s life cycle. Since major infrastructure projects like airports and railroads necessitate close cooperation between specialists from various fields, this strengthens the firm’s standing as a solution provider in the design and engineering industries.

In my opinion, BSY has successfully positioned itself as the supplier of choice for engineering firms and owner-operators engaged in municipal work. Large-scale civil construction projects fall into this category. solutions share a common code base, which allows for data to flow freely between building models, simulation, and construction management tools. In doing so, it avoids the inefficiencies that arise when moving workflows between different solution sets and subsequently losing data in the process. Furthermore, BSY is well-established in the Asset Operations and Maintenance subsector of infrastructure engineering, a field in which market leaders like Autodesk (ADSK) are less well-represented. As the infrastructures in mature economies age, I believe BSY Asset Lifecycle solutions will continue to be popular among owner-operators.

BSY homepage

Strong customer relationships

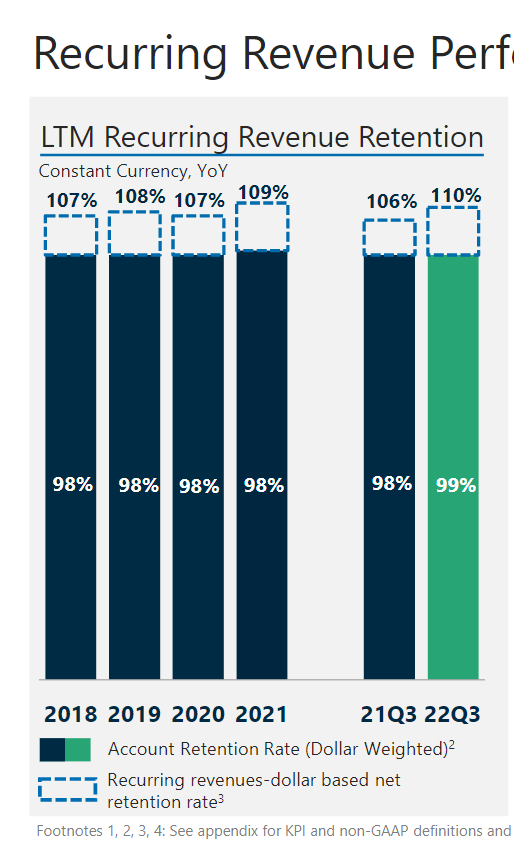

A large portion of BSY’s income comes from its most reliable customers. Strong customer relationships have been a hallmark of BSY, as evidenced by high account retention rates and steadily rising net revenue retention rates, both of which point to increased spending across the board with existing customers. BSY’s flexible platform and its ability to meet a wide variety of infrastructure engineering needs are likely major contributors to its high customer retention rate (a bullish point that I have stated above regarding a comprehensive product portfolio). Another reason, I believe, would be BSY customer service. Customers are also able to get the most out of BSY products thanks to the company’s dedication to providing first-rate service and support. The BSY Success Plan offerings supplement this with a higher tier of subscription service than what is included in the base SELECT or Enterprise technical support package.

3Q22 presentation

This solid foundation of trust with the customer base will allow BSY to eventually increase prices. When compared to rivals, BSY’s pricing strategy has traditionally been more conservative. The company has been focusing on annual inflation-rated pricing escalations of around 1%-2% above inflation, with the precise amount varying according to the functionality and additional services the company offers against incremental pricing. As a result of providing sticky solutions and maintaining strong connections with its clientele, I think BSY can command a premium price without losing any of its clientele.

3Q22 presentation

Solid 3Q results

In my opinion, BSY’s third-quarter results have given shareholders a clearer picture of the company’s preparedness to succeed in a more uncertain economic climate. BSY’s year-over-year ARR growth was 14%-16% at a constant currency rate, with 99% account retention and 110% net retention. Not only has BSY performed admirably, but it has also shown strong momentum in other leading indicators, such as increased engineering backlogs and organic ARR growth of 11.5%. I attribute this 11.5% ARR growth to solid new business conditions and steady increases in E365 consumption. Furthermore, BSY’s ability to consistently drive operating margin accretion is a key consideration.

Forecast

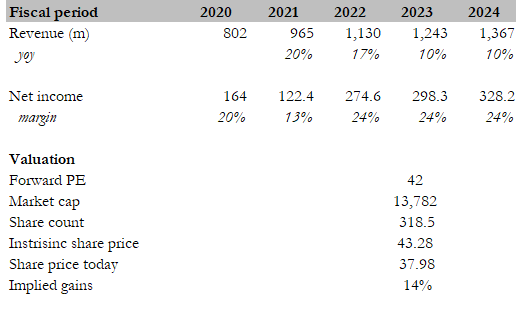

I believe BSY has 14% upside. My model indicates that it is worth $43.28 in FY23. It is very clear to me that BSY is well-positioned to benefit from the large and growing spending on infrastructure – which will have a positive impact on the demand for its services. If we were to look into BSY fundamental performance, it is clear that they have been executing well and customers love their services (high retention rate).

Based on my estimates, BSY should generate around $328 million in net income in FY24 suppose it continues to grow topline at a stable pace and maintain margins (note that margin could expand further but I am being conservative here). If we assume BSY to trade at the same forward PE multiple, BSY is worth $43.28 in FY23, or 14% more.

Author’s estimates

Key risks

Major recession

Weaker expansion rates due to potential churn and increased competition would be bad for the business and stock narrative. Bentley has maintained a 98% account retention rate, but if we enter a severe recession or competition ramps up from engineering peers like Autodesk, the company may experience higher logo churn and lose customers.

Exposure to cyclical industries

Approximately 10% of BSY’s revenue comes from the Commercial and Facilities end-market, which has cyclical industry exposure. Customers are reevaluating their need for a fixed workplace in the wake of COVID, and this segment of revenue may suffer as a result of the rise of telecommuting and other flexible work arrangements. Further, Commercial relies heavily on non-public sources of funding for its endeavors. Their access to capital will be constrained as interest rates rise.

Conclusion

BSY is well positioned to ride on the long-term secular uptrend of digitization in infrastructure spend. I believe this growth is inevitable as human civilization evolves and requires better living standards. The immediate concern is the near-term uncertainties in the macro-environment, which BSY has clearly demonstrated it can navigate through it.

Be the first to comment