Dragan Mihajlovic

Thesis

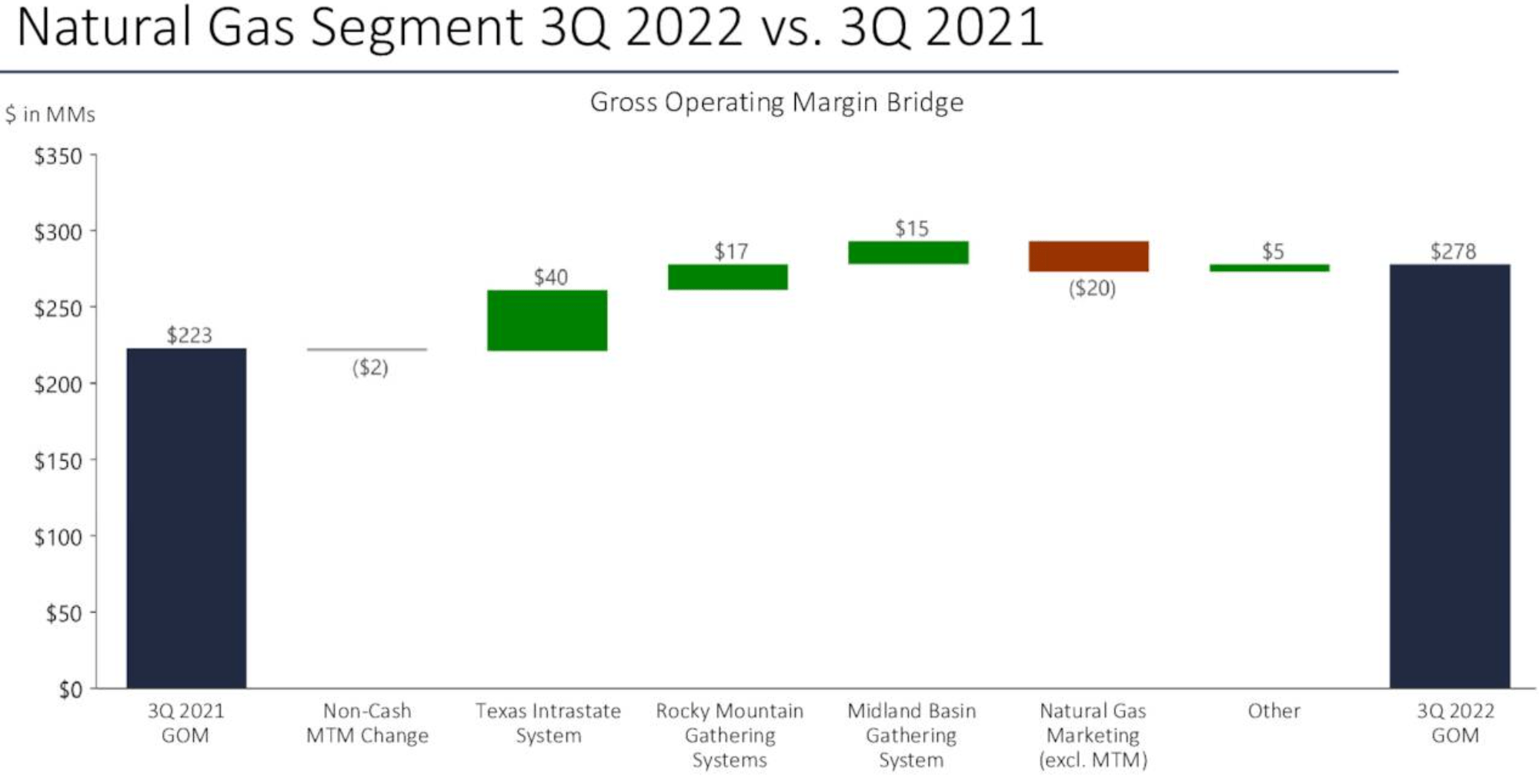

I see a divergence between the earnings prospects of Enterprise Products Partners L.P. (NYSE:EPD) and its market valuations. On the one hand, I see an encouraging earnings growth curve ahead both in the near term and also long term. In the near term, the amount of volume of all products being transported through its system of pipelines set a record in Q3 of 2022. And margins in the key NG&L Pipeline segment rose substantially, leading to a nearly 25% YOY gain in profit as seen from the chart below (from about $223 in Q3 2021 to $278 in Q3 2022).

In the longer term, as one of the world’s largest exporters of LPG (liquefied petroleum gas), I expect demand to remain robust. Demand from Europe should continue to rise as the EU intends to reduce its reliance on Russian gas going forward. And demands in the United States should remain robust, too, given the underinvestment in energy infrastructure over the past many years in the country, as I have repeatedly argued in my other articles. Last but not least, EPD is involved in just about every major shale play in its sector. It is one of the most diversified members of this industry both in terms of geographical diversity and product categories. Besides its key NG&L segment, it also transports a vast array of raw materials (ethane, propane, butane etc.). Thus, the risk to any single product line or geographical location is minimized.

Yet, its valuation is discounted heavily by the market – in the range of 20% to 35% by my estimates as to be detailed later. And in the remainder of this article, I will explain why such a divergence between its fundamentals and valuation metrics seems absurd.

A quick note before moving on, for MLPs, their “shares” should be called “units” and hence their EPS should be called earnings per unit (“EPU”). But considering that the article may be read by a range of readers, some of whom may not be particularly familiar with these terminologies, I will keep mentioning shares and EPS in the remainder of the article.

Source: EPD 2022 Q3 ER (EPD)

Robust volume and Margin

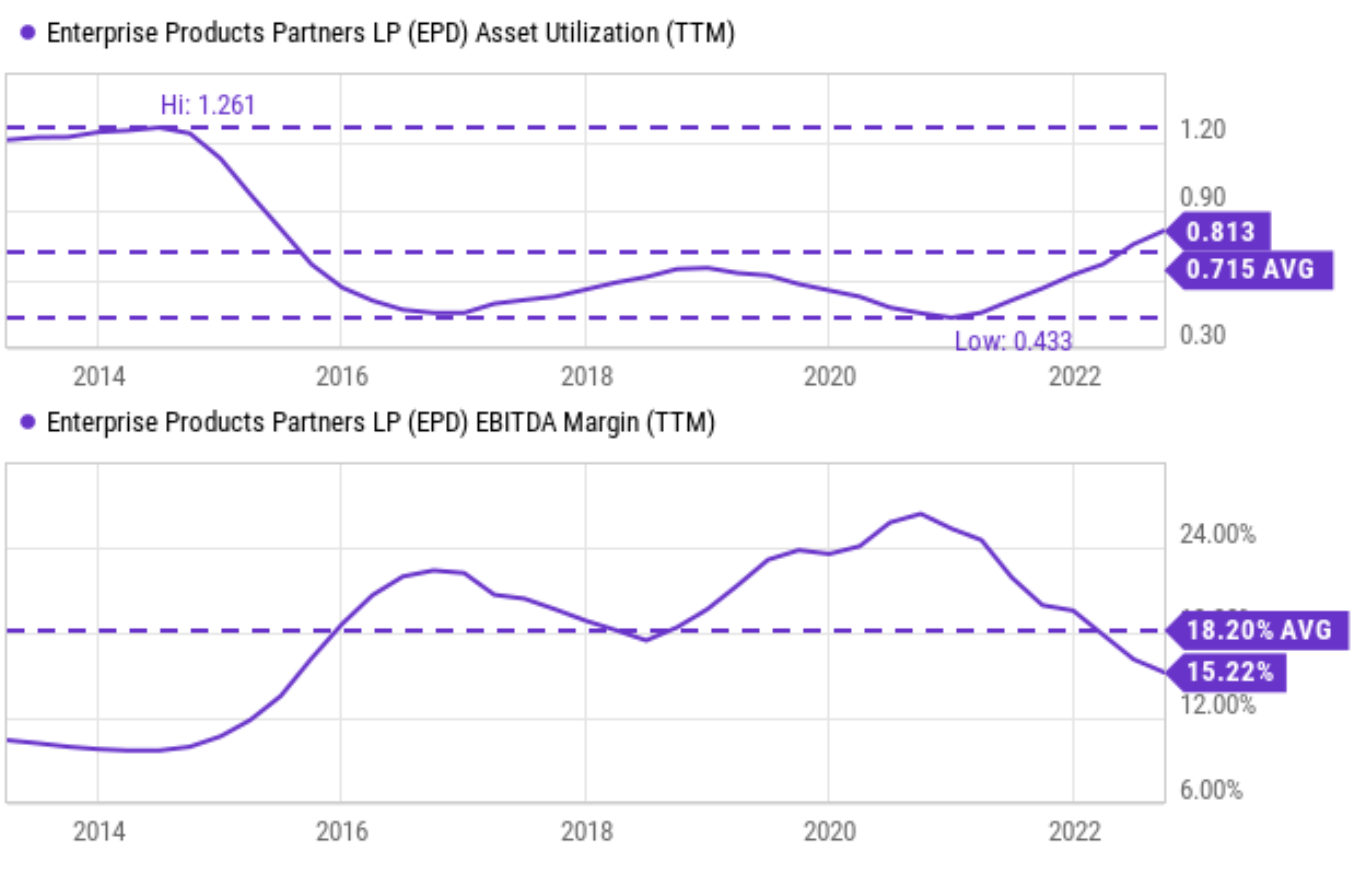

As just mentioned above, Enterprise Products Partners L.P. has been enjoying record volumes transported through its pipelines, as reflected in its asset turnover rate (aka asset utilization rate, AUR) shown in the top panel of the next chart. To wit, its AUR dialed in at 0.813x as of the most recent quarter on a TTM basis. It almost doubled from the bottom level of 0.43x during the COVID breakout and is also about 15% above its long-term average of 0.715x.

The combination of robust volume and favorable pricing environments has resulted in healthy profits and margins. As aforementioned, margins in the key NG&L pipeline segment rose almost 25% year-over-year gain in the past quarter.

The margin from the NG&L segment was partially offset by a decline in the petrochemical and refined operations. But overall, its margins are at a healthy level by historical standards as measured by its EBITDA margin (as shown in the bottom panel of the chart).

Looking forward, as aforementioned, I anticipate the demand from both Europe and the U.S. to stay robust given the geopolitical shift of the energy landscapes caused by the Russian/Ukraine war. And next, I will explain why EPD is well-positioned to benefit from this shift.

Source: Seeking Alpha data

Growth potential

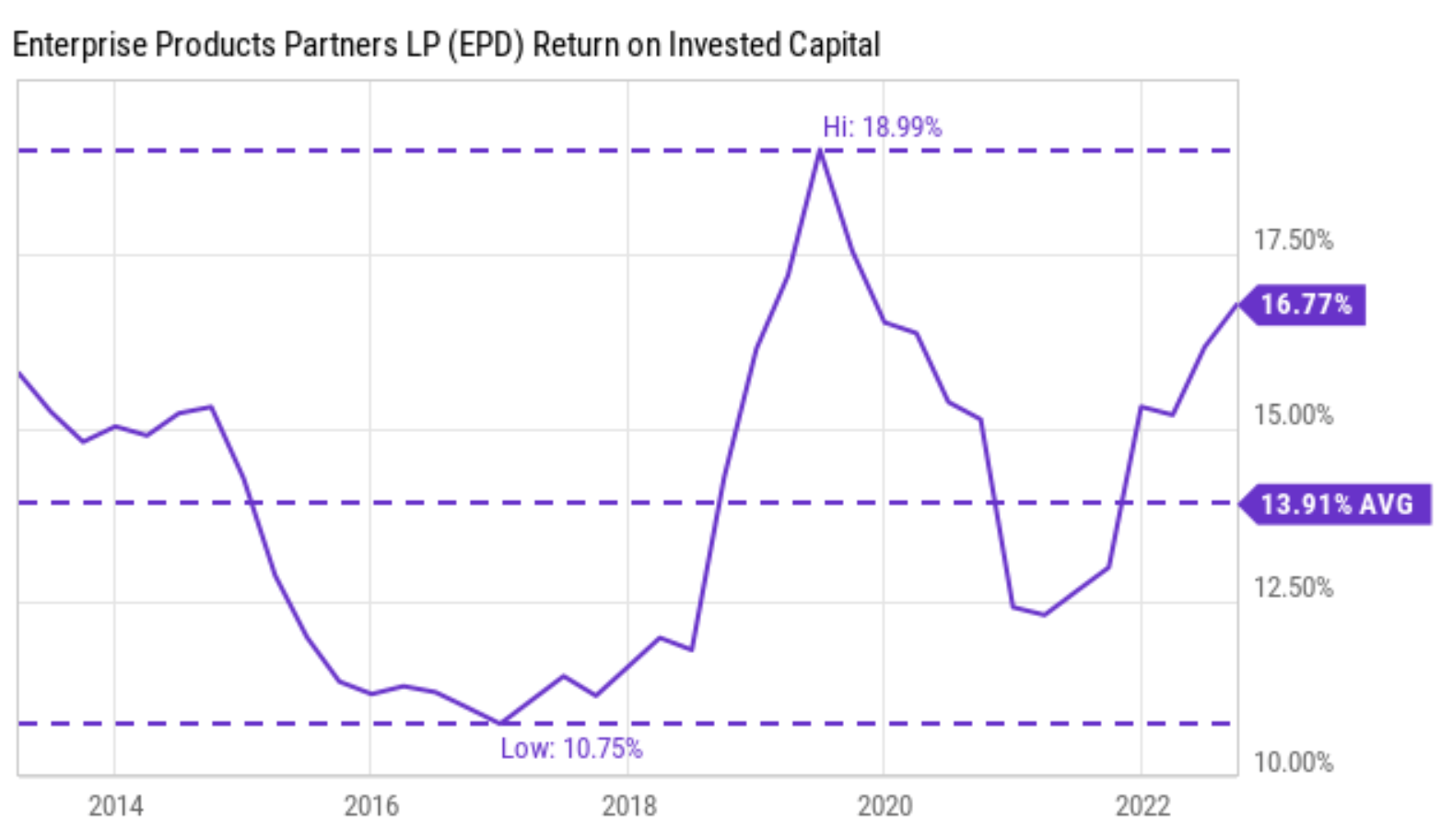

In the long term, the growth potential of any firm is governed by two factors ultimately, the return on invested capital (“ROIC”) and the reinvestment rates (“RR”). And EPD enjoys healthy metrics in both areas. In terms of ROIC, the chart below shows its current ROIC hovers around 17%, far above its historical average of ~14%. In terms of reinvestment, the company has been maintaining a plowback ratio in the range of 20% to 25% in recent years.

An ROIC of 17% and an RR of 20% could lead to 3.4% of organic real growth. And given the long-term pricing power EPD boasts, adding a conservative inflation escalator of 2.5% can push the growth rate to about 6%.

And next, I will show that a 6% growth rate, when coupled with its current valuation discount, already offers an extremely favorable return profile in the years to come.

Source: Seeking Alpha data

Yet valuation is discounted

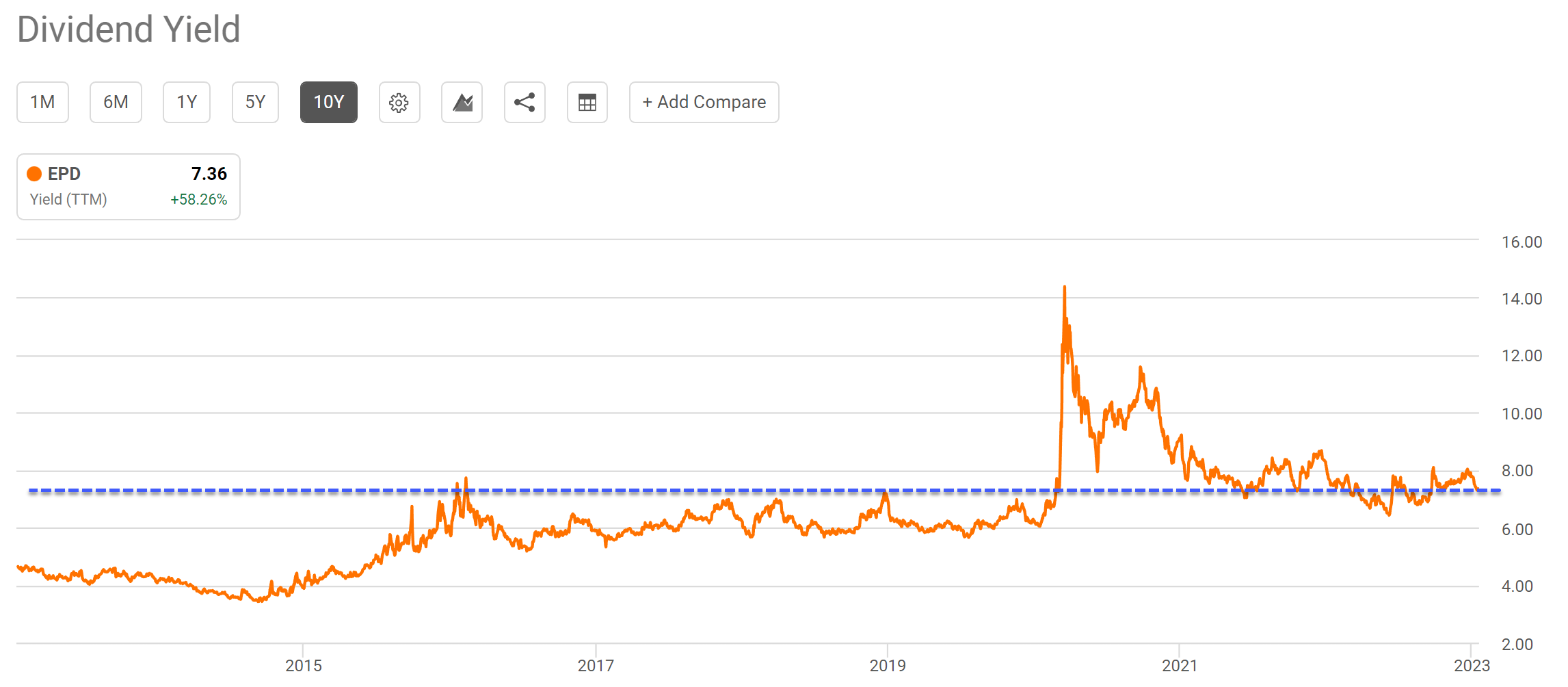

Enterprise Products Partners L.P. is currently priced at a discounted valuation based on the metrics I’ve examined. As a reliable dividend stock (a dividend champ actually), dividend yield should be the most reliable valuation metric here. As seen from the chart below, its current yield of 7.36% is near the highest level in a decade. It is above its historical average of 6% by 22%, signaling a 22% valuation discount.

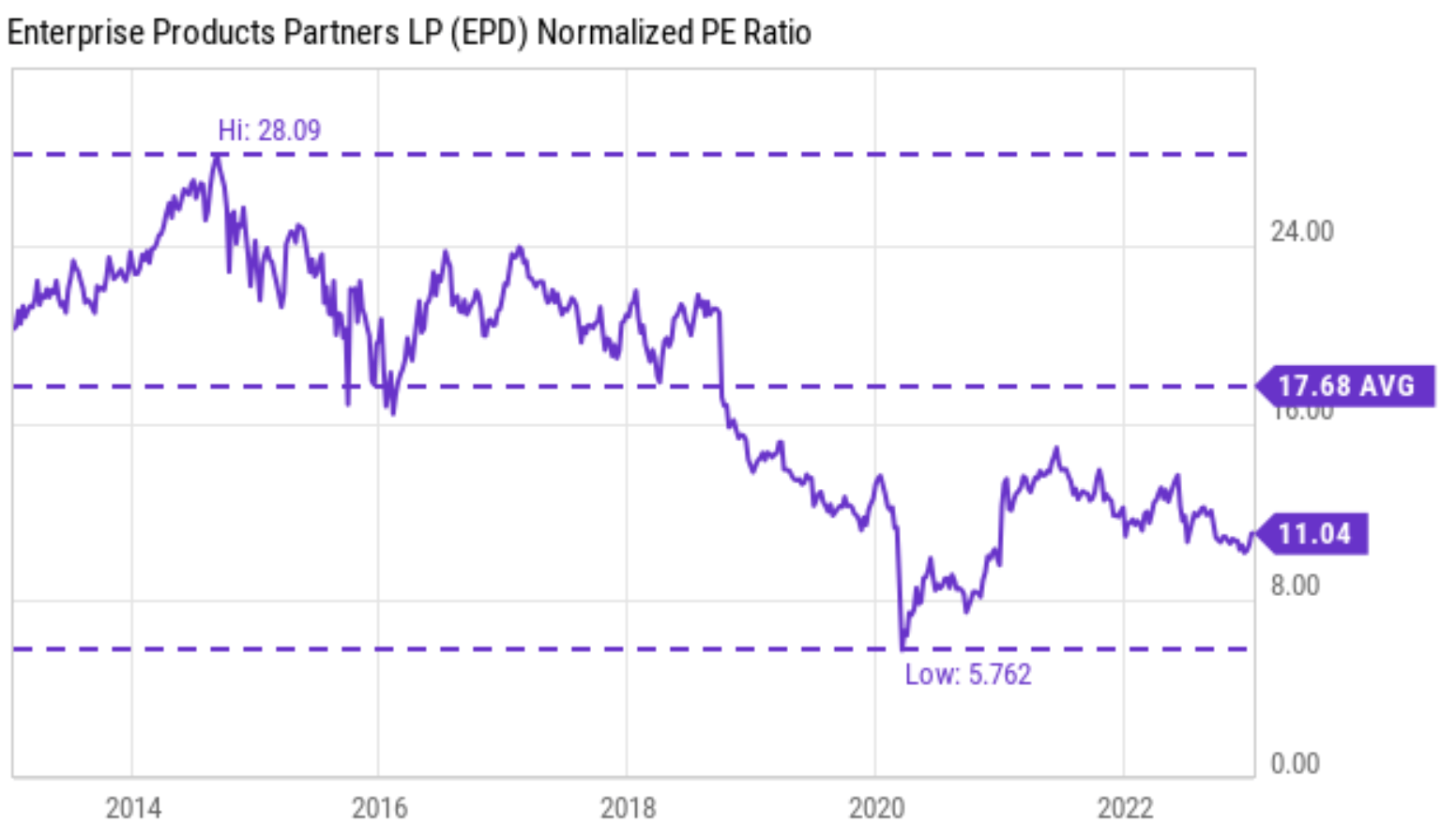

The second chart below shows its P/E ratios, which suggests an even larger discount. Its P/E sits around 11x currently. Compared to its historical average of 17.68x, it is discounted by about 35%.

Source: Seeking Alpha data Source: Seeking Alpha data

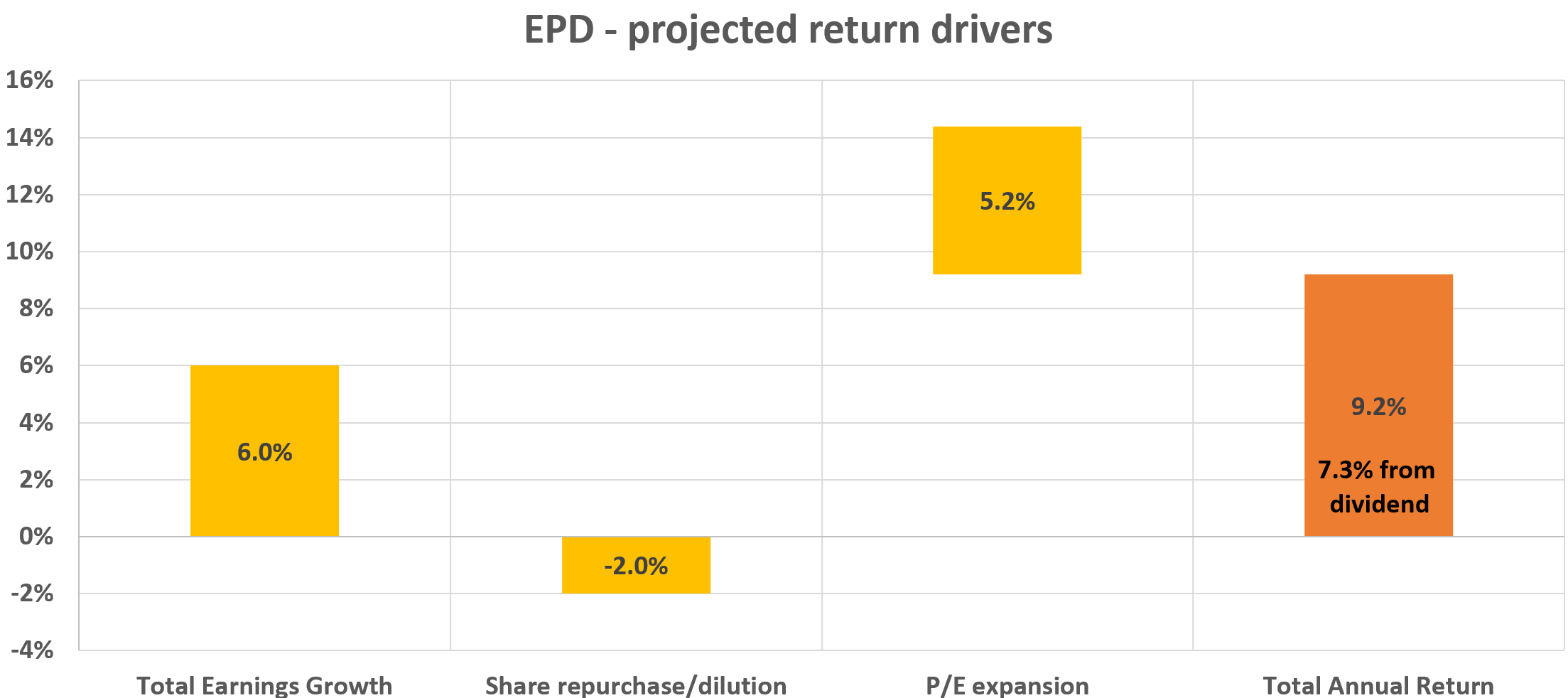

The combination of a healthy growth curve and the large valuation discount offers an appealing return profile as summarized in the waterfall chart below. Specifically, I am projecting a 9.2% total annual return in the next 3~5 years, consisting of:

- 6% annual growth in its total earnings as analyzed above.

- A 2% share dilution, which is in line with its recent year level. As a result, EPS (or earnings per unit) is projected to grow at 4%.

- And finally, a valuation expansion of 5.2% a year (obtained by annualizing the 22% valuation discount based on its dividend yield as analyzed above).

Source: Author based on Seeking Alpha data

Risks and final thoughts

Enterprise Products Partners L.P. faces both specific and macroeconomic risks though. In terms of macroeconomic risks, inflation is an ongoing concern. Or more precisely, the interest rate increases triggered by inflation are an ongoing concern. As a typical pipeline player, EPD is quite leveraged and therefore sensitive to higher borrowing costs. In terms of its own specific risks, as mentioned above, it is currently facing some headwinds in its petrochemical and refined operations. Also, the potential for its growth in the United States or overseas would also require the construction of more terminals and therefore substantial CAPEX expenditures.

All told, the divergence between Enterprise Products Partners L.P.’s fundamentals and valuation metrics seems absurd to me. And absurdity in the stock market often signals outsized return potentials. And indeed, in this case, I am seeing an annual return potential for Enterprise Products Partners L.P. close to double-digits (9.2% based on my projection). And lastly, note out of the 9.2% projected returns, 7.3% would come from its dividends – adding another layer of safety considering its dividend champ status.

Be the first to comment