ConstantinosZ/iStock via Getty Images

Investment Overview

I last covered Bausch Health (NYSE:BHC) – the Laval, Canada based manufacturer of branded, generic, and branded generic pharmaceuticals, medical devices and over the counter (“OTC”) products – back in August, in a bearish note for Seeking Alpha.

For the full history of Bausch and the misadventures of the company under its former name Valeant, which included a spike in the share price to >$250 in mid-2015, and a subsequent collapse to <$10 per share by mid-2017 as the business model of acquiring pharmaceutical companies and hiking the prices of their commercial drugs failed and levels of debt spiralled out of control – please refer to my former note.

The focus of this article will be the prospects for Bausch Health and its recent spinoff, Bausch & Lomb Corporation, through 2023.

I was bearish on Bausch in my last note for a number of reasons. Firstly the company has been heavily loss making in recent years – net losses since 2018 have been $4.1bn, $1.8bn, $559m and $937m. Secondly, the company’s total consolidated debt stands at ~$19.6bn, which is 2.5x forecast FY22 revenues of $8bn – $8.17bn, and >6.5x forecast FY22 non-GAAP Ebitda.

Thirdly, revenue growth is somewhat flat, forecast to be up just 2% in FY22 versus FY21, having fallen in every year between 2015-2020. Fourthly, a major patent ruling that did not go in Bausch’s favour threatens to drastically reduce sales of Bausch’s best-selling drug Xifaxan, which earned $1.2bn across the first three quarters of 2022, or >20% of Bausch Health’s total consolidated revenues.

Finally, Bausch is fighting numerous court cases that involve alleged patent infringement, unpaid taxes, patent challenges, securities fraud, generic price fixing, breach of contract, and collusion with other generic drug manufacturers to delay entry of their generics into the market in exchange for payments.

With so many legacy issues affecting the company’s ability to operate successfully and drive growth across all of its business divisions, even a market cap of ~$2bn – implying a price to sales ratio of ~0.25, and a PE ratio of 9x – felt too high at the time for Bausch.

Despite my misgivings however, Bausch shares have increased in value by >35% since my note. Whether the market is simply taking a pause for breath before beginning another round of sell-offs, or whether Bausch management is finally showing signs that they can turn the business around – is open for debate.

In this post I will take a fresh look at Bausch and its prospects for 2023 through the prism of its latest earnings results and recent communications with investors and analysts, and market headwinds and tailwinds going into 2023.

Bausch Health Check After Q322 Earnings – Xifaxan Patent Dispute Still Key To Company’s Fortunes

Bausch released Q322 earnings on 3rd November. The headline figures were revenues of $2.4bn, down 3% on a reported basis but +2% on an organic basis, adjusted EBITDA of $704m – down 13% year-on-year – and adjusted net income of $277m, down from $417m in Q321.

These aren’t figures to get an investors’ pulse racing, and they also included a slight FY22 earnings downgrade to both topline revenues and EBITDA, but they were stable enough to sustain a mini-recovery in Bausch’s share price, which slipped from $22, to <$5 in mid August after management announced that the US District Court of Delaware had ruled that key patents preventing Norwich Pharmaceuticals from marketing a generic version of Xifaxan were invalid.

Bausch remains hopeful that the outcome can be reversed, announcing its intention to appeal the decision to the US Court of Appeals in August, and insisting, despite the FDA’s tentative approval of Norwich Pharma’s rifaximin 200 mg generic to Xifaxan in early September, that no generic version of its drug can be launched until Orange Book listed patents expire in 2029. A decision from the Court of Appeals is expected in 12-18 months, Bausch CEO Thomas Appio told analysts on the Q322 earnings call.

Later in November, Bausch’s share price received a mini-boost after the FDA introduced new guidance – just as Bausch had promised it would – that requires generic drugmakers to conduct four pharmacokinetic bioequivalence studies and in vitro bioequivalence studies, or four pharmacokinetic bioequivalence studies, in vitro bioequivalence studies (comparative dissolution), and two clinical endpoint bioequivalence studies, before an approval can be granted.

This seems unlikely to stop Norwich altogether, but it could cause further delays, whilst Norwich’s strategy to circumvent certain patent issues by marketing its product for Irritable Bowel Syndrome only, an indication not protected by the patents upheld by the courts in Delaware, is not guaranteed to succeed. It should not be forgotten that Bausch has successfully prevented three generics giants – Novartis (NVS), Sun Pharmaceuticals and Teva Pharmaceuticals (TEVA) – from launching generic versions of Xifaxan in recent years.

The Xifaxan patent protection issue is huge for Bausch – Xifaxan drives ~80% of the revenues of its Salix division, which itself earned ~48% of the $1.1bn revenues generated by Bausch Health in Q322.

23% of these revenues were driven by international sales, 7% by the Solta Medical division, comprised of aesthetic medical devices, and 22% by its diversified Products division, which includes generic products, ortho dermatologics, and dentistry products.

In Q322, Salix, Solta Medical, and International grew revenues organically by 3%, 10%, and 4%, but the diversified products division revenues fell by 18%, as legacy products such as antidepressant Wellbutrin contributed lower sales volumes, more than offsetting growth from newer products such as Aplenzin and Arestin.

Presently, given the market is clearly valuing sales of Xifaxan as if they will decline in the face of new generic market entrants, there may be an upside opportunity in play should Norwich be unable to secure an approval from the FDA in the near-term, and even if Xifaxan revenues were to decline by ~25% per annum from next year, as the revenues relating to drugs going off-patent typically do, its contribution would likely still be >$1bn in 2023 and 2024.

As such, Bausch stock – from that perspective at least – looks like a good value while its price to sales ratio remains <1x, and the business is profitable, as it was in Q322, with GAAP income reported at $399m on a GAAP basis, and $277m on an adjusted basis.

When completing a valuation of Bausch however, it is impossible to overlook the debt burden and ongoing litigation, and the implications these issues have on the company’s ability to generate cash to fund growth in the business.

Before discussing debt repayment and litigation, however, it is worth touching on the role Bausch’s spinoff of its eye care division into a new entity, Bausch + Lomb, will play in 2023 and beyond.

Bausch + Lomb Becomes Separate Entity But Solta Spinoff Postponed

As part of its quest to complete a strategic overhaul of the company and ease its debt burden, Bausch’s longstanding intention has been to split the company into three by spinning off its eye care and Solta Health divisions.

The eye care division was spun off successfully this May, completing its IPO by raising ~$630m at $18 per share. At the time of the IPO Bausch the original company announced that it held ~90% of the common shares of the new entity, called Bausch + Lomb (BLCO). Bausch + Lomb shares are currently trading at a price of $15, with the business being valued at $5.25bn.

The spinoff enabled Bausch to complete some debt restructuring, securing a new term loan facility worth $2.5bn, and a revolving credit facility of $975m, whilst Bausch + Lomb also secured a five-year term loan facility worth $2.5bn, and a five-year revolving credit facility worth $500m.

In Q322, Bausch + Lomb accounted for $942m – or 48% of the $2.04bn revenues generated by the two entities, its revenues increasing by 5% year-on-year on an organic basis. CEO Appio insisted on the earnings call that:

We continue to believe that the separation of Bausch + Lomb makes strategic sense and we will thoughtfully evaluate all factors related to the B&L separation

It’s possible that, had management known in advance about the patent issues around Xifaxan, or the difficult bear market for biotech stocks in 2022, it would not have gone ahead with the business separation. Bausch filed for an IPO of its Solta Medical division – which generated just $72m of revenues in Q322 – in February, but that IPO has now been abandoned, with CEO Appio adding some colour on the Q322 earnings call:

Of course, the Solta franchise, I believe is, again, another great asset that we have…I think this is an asset that we can continue to grow, continue to invest in, but keep all options open…any type of actions that we would take with our assets would have to be especially an asset like Solta at a premium price. So, again, we always – we are open to looking at different things, but we believe this asset can really grow for us and really be part of the Bausch Health family.

In other words, management sensed that the conditions were not right for Solta’s IPO, and the spinoff would presumably not have enabled management to restructure debt or raise the level of funding it wished from an IPO.

It is an unsatisfactory situation in some ways, given that Bausch might have expected to be split into three in 2022, with all three companies handling appropriate levels of debt and fresh funding raised to give all three companies momentum. In fact, given Bausch owns nearly all of the stock of Bausch + Lomb, and Solta remains part of Bausch, these goals are yet to be achieved.

I would expect to see management attempt to offload shares of Bausch + Lomb in 2023, and perhaps make another attempt to spinoff Solta – or better still, sell that business to the highest bidder.

Debt Repayment Progresses But Long Term Outlook Still Looks Tough

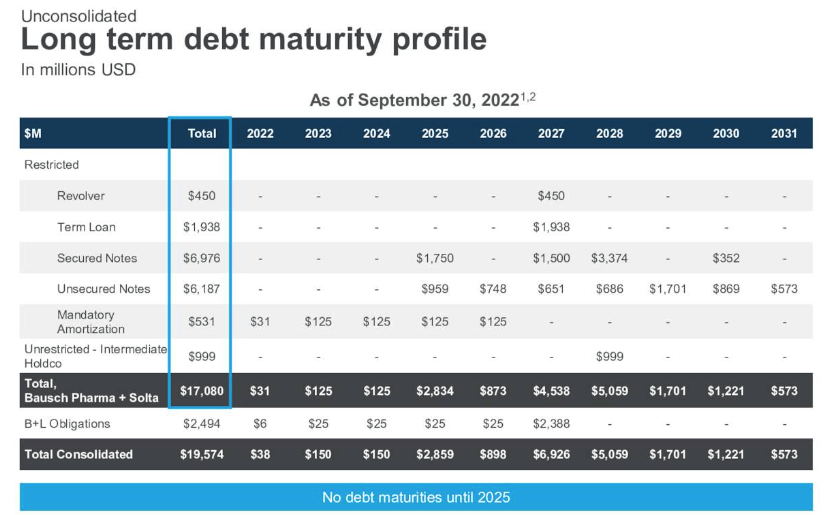

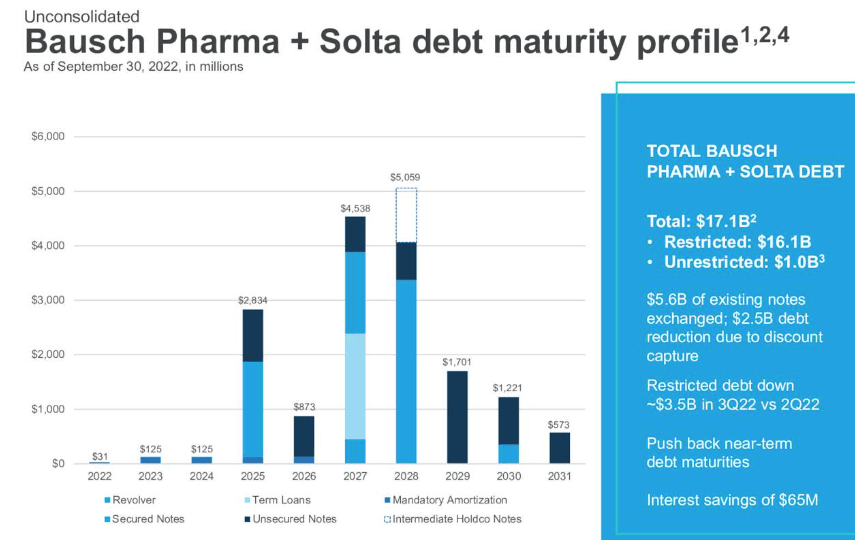

Bausch broke down its latest debt position for shareholders and analysts in its Q322 earnings presentation, as follows:

Bausch debt maturity profile (Q322 earnings presentation)

As we can see, $2.5bn has been offloaded onto Bausch + Lomb, and the near term repayment schedule is not onerous, which is good news for shareholders as revenues can be invested into growing the business.

Bausch debt maturity profile (Q322 earnings presentation)

Looking further ahead at just Bausch and Solta, however, we can see the repayment schedule gets very tough from 2025 until the end of the decade.

Bausch could raise nearly $5bn by selling its entire holding in Bausch + Lomb, if it can find institutional investors willing to pay the current share price, but with revenues at the company likely to fall to ~$4.5bn in 2023, or worse, if a Xifixan generic is launched next year, Bausch will surely struggle to meet its obligations in 2025 and beyond.

Conclusion: Bausch Can Continue to Restructure in 2023 Under New Management, But It’s Long Term Future Looks Shaky

Another troubling aspect of Bausch’ business is the turnover of senior management. Joe Papa resigned from his positions of CEO and Chair at Bausch – which he had held since 2016 – in June this year, to be replaced by billionaire fund manager John Paulson, whose investment firm had been building a position in Bausch, and who had served on the Board of Bausch between 2016 and 2022, plus new CEO Appio.

Papa has also stepped down from his role as CEO of Bausch + Lomb, although he remains at the company until the search for a new CEO is complete. Papa has helped Bausch deal with the fallout from the Valeant era, and shave >$10bn off of the company’s debt pile, which could not have been easy, although many market watchers have been critical of his time in charge.

His departure leaves a role to be filled that many qualified CEO’s may feel is tainted, while the challenge of filleting up the separate businesses, and selling what they can may not appeal to those best qualified for the job.

To summarise the state of play as Bausch enters 2023 is not an easy task. On the negative side of the ledger you have the threat of generic competition for Xifaxan reducing revenues at Bausch by >25% per annum, perhaps to <$4bn per annum in 2023 and <$3.5bn in 2024, and so on.

Meanwhile, there is still >$17bn of debt to repay, and although management announced it had “reduced debt principal by $2.5bn through a very successful debt exchange offer” in Q322, it is extremely difficult to grow a company and its valuation when all cash generated by the business goes into servicing the debt.

On top of that, management is actually attempting to shrink, not grow, the company, via spinoffs of its business divisions. We will have to wait and see how Bausch + Lomb fares as a standalone company, but without a CEO in place and with its own onerous debt covenants, the outlook here does not look especially bright.

Then there are multiple legal cases to fund, unpaid tax demands that may run into the billions, and at an even more basic level, few new product launches to get excited about, since there are limited funds available for R&D and M&A spending.

Looking at the positives, the Bausch + Lomb spinoff has been completed, and could become a positive. The debt schedule in 2023 and 2024 is not onerous. The challenge of turning the business around may appeal to a hungry new management team, especially if the Xifaxan patent dispute is settled in Bausch’s favour, and there is even ~$500m of cash to spend should the right M&A opportunity present itself.

When I weigh the pros and cons I still find it hard to escape the conclusion that Bausch is a very troubled company, that simply ran up too much debt during the Valeant era, and made too many bad investments for the company to be salvageable.

With that said, most businesses in Bausch’s sector – Perrigo (PRGO), Viatris (VTRS), Organon (OGN), Teva Pharmaceuticals (TEVA) wrestle with similar problems to Bausch – high levels of debt, flat growth, and attempts to break up the company with strategic sales of certain divisions. As I mentioned in my last note, upon changing its name to Bausch, the company’s press release stated:

The Bausch name has long been a highly respected name in the health care space, synonymous for 165 years with innovation and an unwavering dedication to improving people’s lives.

It may seem to defy all logic, but Bausch’ reputation for longevity- even if the company is unrecognisable from its previous iterations – likely helps it appeal to venture capital, hedge funds, and mavericks like Paulson.

These characters may see Bausch as not much more than some “skin in the game”, but they may also represent the business’ best chance of recovery, and since there is nothing hedge funds like more than a rising share price, as an “un-calculated gamble”, it is worth at least considering the idea that Bausch stock could stage a comeback in 2023. All things considered however, most risk averse investors would do well to steer clear, given there are dividend paying Pharmas out there with future-proofed product pipelines, strong organic and inorganic growth, and steadily growing share prices.

Be the first to comment