hallojulie

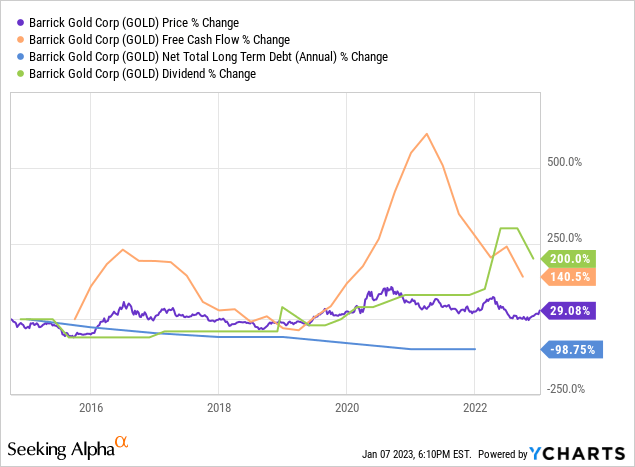

Barrick Gold (NYSE:GOLD) has executed an impressive turnaround over the past decade. As the chart below makes obvious, free cash flow (though still lumpy to some degree as it invariably is in the mining industry) has improved immensely, the variable quarterly dividend payout has increased dramatically, and the company has eliminated virtually all of its once massive debt pile over the past nine years. Yet, despite all of these fundamental improvements (which have also included fine tuning its world-class asset portfolio, bringing in one of the industry’s best leaders as CEO, buying back shares opportunistically, and building up an impressive decade plus production pipeline from high-quality gold and copper mines), the stock price has hardly moved by comparison, including floundering during 2022:

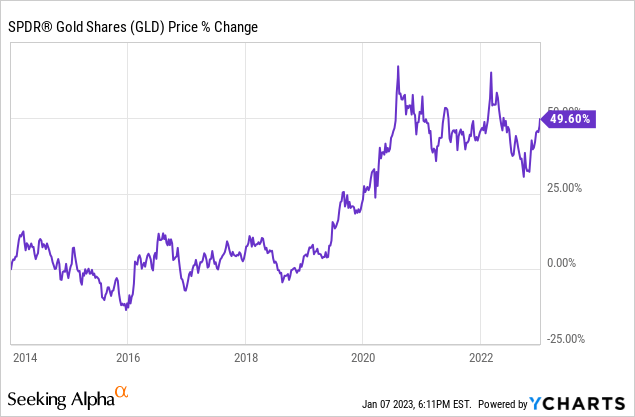

This is especially incredible given that the gold price (GLD) is up by ~50% over that same time frame:

Was GOLD overvalued back at the beginning of 2014? Perhaps, but we believe that the valuation pendulum has swung too far in the other direction and that GOLD – especially given the macroeconomic fundamentals and trends at the moment – is meaningfully undervalued right now and ready to spring higher. In this article, we share three reasons why we think 2023 might finally be GOLD’s year.

Reason #1: Gold Prices Are Likely To Shine In 2023

Gold prices have numerous tailwinds blowing behind them as we begin 2023. First and foremost, central banks are buying up the yellow metal, which serves as a ringing endorsement. In fact, 2022 central bank demand for gold was at a 55-year-high and actually accelerated over the course of the year. This signals momentum behind continued strong demand for the yellow metal in 2023.

Gold also stands out as a safe haven option for investors looking for places to hide with a recession on the horizon. While CDs currently offer attractive interest rates, if/when the Federal Reserve pivots on interest rates (which is quite possible to take place at some point in 2023), gold will stand alone as the safe-haven of choice, especially now that cryptocurrency (BTC-USD) and Ethereum (ETH-USD) have lost a lot of their luster in the wake of the FTX scandal and other negative crypto sphere developments in 2022.

Finally, geopolitical turmoil and tensions continue to drive demand for the yellow metal and black swan event such as a Russian nuclear strike or China invading Taiwan could drive gold prices much higher in 2023 as well. Not only that, but China itself appears to be hedging against such a scenario playing out by buying gold very aggressively right now (in fact, Reuters recently reported that China’s central bank plans to buy an additional $1.8 billion in the near future).

Reason #2: GOLD’s Fundamentals Have Further Upside Ahead

As much as GOLD’s fundamentals have improved over the past decade, we see further fundamental improvement in store for the company in 2023.

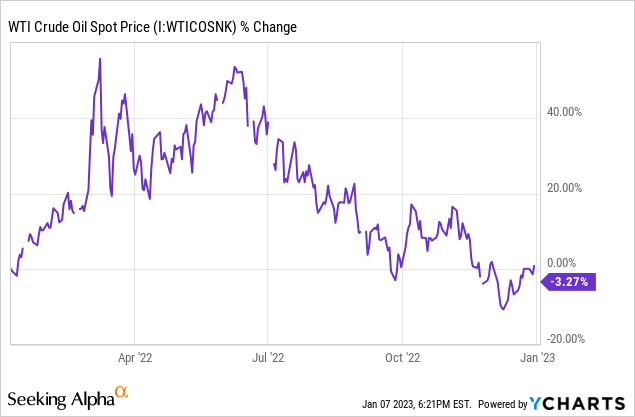

First and foremost, oil prices have pulled back sharply from their rapid rise in the wake of the outbreak of the Russia-Ukraine war in early 2022, and are in fact slightly below where they were a year ago (prior to the war breaking out):

This should alleviate one of the biggest headwinds facing GOLD last year by dramatically reducing its operating costs, combining with higher gold prices to generate fatter profit margins.

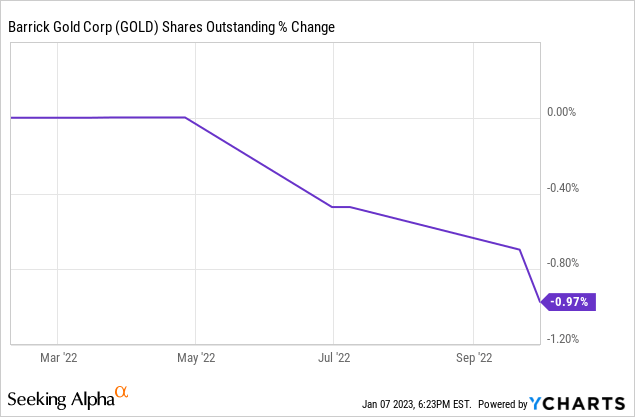

Furthermore, GOLD repurchased ~1% of its outstanding shares through the first nine months of 2022 and very possibly repurchased more in Q4 given that it still has a whopping $670 million left on its buyback authorization and certainly has the financial capacity to do so:

While not a huge tailwind, this is not unmeaningful either and will also help boost per share results in 2023.

Another reason we are bullish is simply that we expect production to only increase moving forward. Its Nevada joint venture is firing on all cylinders and is poised to enjoy new production from mines like Goldrush, Fourmile, REN, Robertson, and North Leeville as well as increased production levels at Turquoise Ridge. Meanwhile, its Pueblo Viejo assets is on track for a major expansion of operations there.

Reason #3: GOLD’s Valuation Looks Attractive

Last, but not least, GOLD also should benefit from some multiple expansion in 2023. Based on a return to 2021 normalized earnings per share levels of $1.16 (which is not too much of a stretch given the aforementioned factors), GOLD’s forward P/E ratio is 16.4x. In contrast, its five-year average normalized P/E ratio is 22.3x. Furthermore, with the company generating significant free cash flow and returning a lot of it to shareholders via dividends and buybacks, it is not unreasonable to expect a 4-5% shareholder capital return yield on current cost in 2023. Assuming the ~36% multiple expansion occurs over a three-year period and combining it with the 4-5% capital return yield alone and not accounting for any increase in the gold price or other growth for the company, we see ~15% annualized total returns over the next three years for GOLD shares, though it will obviously be meaningfully higher if gold prices move higher like we think they will.

Investor Takeaway

We are very bullish on gold prices heading into 2023 and are even more bullish on the price of GOLD shares. Between the bullish fundamentals for its main product, production and operation efficiency upside for the company in 2023, a shrinking share count, and valuation multiple expansion potential in combination with its attractive dividend yield, GOLD is poised to deliver outsized returns in 2023. After doing due diligence on the company including interviewing its CFO, we are very bullish on its prospects in 2023 and beyond. As a result, we have allocated ~10% of our portfolio to gold miners at High Yield Investor with a substantial portion of that being invested in GOLD shares.

HYI Portfolio

Be the first to comment