zorazhuang

Targa Resources Corp. (NYSE:TRGP) is a natural gas liquids-focused midstream corporation that primarily operates in the state of Texas. The midstream sector in general has long been among the favorite areas for income-focused investors to be due to the fact that most of these companies enjoy remarkably stable cash flows and high dividend yields. Targa Resources is something of an exception to this as it does have cash flow stability but it falls somewhat short in terms of yield. In fact, the company only yields 1.92% at the current price, which is due to a dividend cut back in 2020 that was then partially reversed last year. The company will likely increase its dividend at some time in the future, which we will see over the course of this article. Although Targa Resources does not enjoy the high yield that we typically like to see here at Energy Profits in Dividends, it has in the past and may once again. This is why I continue to discuss this company on my service. Overall, there are quite a few reasons to invest in this company today as it has made great progress in overcoming a few of the problems that it had in recent years and is thus positioning itself fairly well for the future.

About Targa Resources

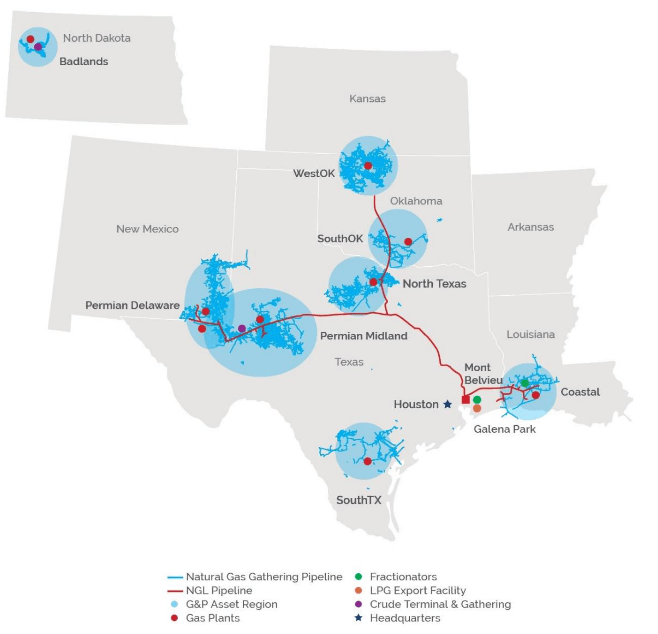

As stated in the introduction, Targa Resources is a natural gas liquids-focused midstream corporation that primarily operates in the state of Texas, although it does have some operations in North Dakota’s Williston Basin:

Targa Resources

Unlike many of its peers, though, we can see that the company’s pipeline infrastructure is fairly small. This is a bit misleading however as Targa Resources actually has a fairly substantial gathering and processing infrastructure network. A gathering pipeline is somewhat different from the large long-haul pipelines that carry resources across a state or a country. Rather, these pipelines are fairly short and low-capacity pipelines that simply grab the resources from the well that extracts them from the ground. The pipeline will then take the resources to the first stop on their journey, which is usually either a much larger long-haul pipeline or a processing facility. Targa Resources does have a fairly substantial natural gas processing capacity as it is capable of handling a total of eleven billion cubic feet of natural gas per day across its 53 processing plants. The processing of natural gas is critical because natural gas contains a number of impurities and pollutants when it is removed from the ground, such as water and sulfur. The processing plant removes these impurities and converts the natural gas into a state that can be used by the end user. The company also owns 960,000 barrels per day of natural gas liquids fractionation capacity. A natural gas liquids fractionator splits the resources into the various natural gas liquids that we use in our everyday lives, such as propane, butane, and ethane. Overall, then, Targa Resources is a fairly major player in the midstream space, even though it does not have substantial long-haul pipeline assets.

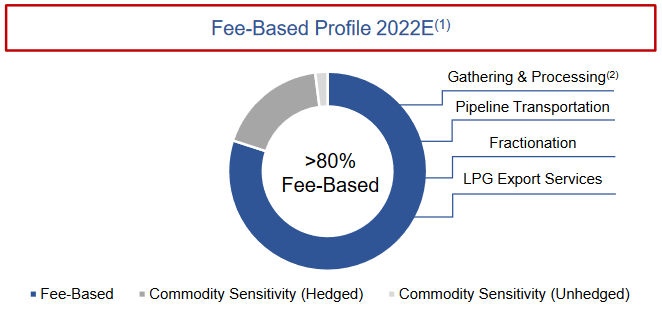

In the introduction, I stated that Targa Resources tends to enjoy remarkably stable cash flows regardless of conditions in the broader economy. This is due to the business model that the company utilizes. In short, Targa Resources enters into long-term (usually five to ten years in length) contracts with its customers. Under these contracts, the customers send resources through Targa Resources’ infrastructure and compensate the company based on the volume of resources handled. This provides the company with a surprising amount of insulation against fluctuations in commodity prices. At this point, some readers might point out that upstream resource producers tend to reduce their output when energy prices decrease. This happened back in 2020 when the COVID-19 pandemic broke out and caused the demand for crude oil to plummet. Although Targa Resources does not own any crude oil infrastructure, natural gas and natural gas liquids are often produced by the same wells so the company would still be affected. Fortunately, the company has a way to protect itself against this. The contracts that it has with its customers contain what are known as minimum volume commitments, which specify a certain minimum volume of resources that the customer must send through Targa Resources’ infrastructure or pay for anyway. Thus, it has a certain portion of its cash flow that is generally unaffected by either energy prices or resource production. In fact, 80% of the company’s operating margin (a proxy for operating profit) comes from these recession-resistant contracts:

Targa Resources

This is something that is certain to be attractive right now as nearly all economists agree that the American economy will enter into a recession sometime in 2023. One of the characteristics of recessions is that the demand for energy resources declines, which could have an effect on the output of upstream producers much as it did back in 2020. The fact that more than 80% of Targa Resources’ cash flows are protected by this provides a great deal of support for the company’s dividend and by extension our incomes.

We can see evidence of this general stability simply by looking at the company’s operating cash flows over time. Here they are over the past eleven quarters:

Seeking Alpha

This provides even further evidence that the company should be able to handle any imminent recession with ease. After all, while its cash flows did decline somewhat in 2020, they still remained much more stable than might be expected considering what happened to energy prices during that year. It is all but certain that any recession that occurs in 2023 will not be nearly as severe as it is very unlikely that the government will once again attempt to lock us all down at home and forbid us from unnecessary traveling. Thus, energy demand should not drop as much and we will likely not see nearly as big of a shock to the industry.

Growth Prospects

Naturally, as investors, we want to see more than simple stability. We like to see growth. Fortunately, Targa Resources is quite well-positioned to deliver in this area. As midstream infrastructure such as natural gas gathering pipelines, processing plants, and fractionators only have a limited quantity of resources that they handle, and the company’s cash flow depends on the volume of resources that move through its infrastructure, the normal way for Targa Resources to generate growth is to construct new infrastructure. This is exactly what the company is doing, although it admittedly does not have as many growth projects in the works as some peers such as Enbridge (ENB) or Kinder Morgan (KMI). One of the company’s major projects is the Daytona NGL Pipeline. The Daytona NGL Pipeline was announced in November of 2022 and has an estimated cost of $650 million. This project was originally envisioned as a joint venture with Blackstone Energy Partners, although Targa Resources bought out Blackstone’s stake last week. The Daytona NGL Pipeline is intended as an expansion to the Grand Prix NGL system that constitutes one of the largest natural gas liquids pipeline networks in Texas. The Grand Prix NGL system is capable of carrying 550,000 barrels of natural gas liquids per day but the Daytona NGL Pipeline is somewhat less than that because it is not the only pipeline that is feeding the entire system. During its third-quarter conference call, Targa Resources stated that the Daytona NGL Pipeline will be capable of carrying 400,000 barrels of natural gas liquids per day when it begins operating, although the company will be able to expand its capacity if needed. This sort of expandable capacity is quite common as it helps to save on construction costs and future-proofs the project. Obviously, these are things that we should appreciate as investors.

Targa Resources is also working to expand its natural gas processing capacity. Also in November 2022, the company announced that it will begin construction of a new natural gas processing plant to serve the Permian Basin. This new plant, dubbed Wildcat II, will be capable of processing approximately 275 million cubic feet of natural gas when it begins operation in early 2024. As the Daytona NGL Pipeline is expected to come online in late 2024, Targa Resources will thus be bringing a few new projects online during that year.

The nice thing about these projects is that Targa Resources has already obtained contracts for their use from its customers. This serves two purposes, both of which are beneficial for the company. The first of these purposes is obviously that we can be assured that the company is not spending an enormous amount of money to construct infrastructure that nobody wants to use. In addition, we can be certain that each of these projects will begin generating money as soon as they become operational in 2024 so we can expect steady growth over the course of that year from these two projects coming online. The second purpose is that the company knows in advance exactly how profitable the projects will be so it knows that each project will be able to generate a sufficient return to justify the investment. Unfortunately, Targa Resources has not specified exactly how profitable they will be so we cannot perform an in-depth financial analysis at this time. Kinder Morgan’s projects usually pay for themselves in four years while The Williams Companies (WMB) has about a six-year payback so it is likely that Targa Resources’ projects are in that same ballpark but this is by no means certain. Regardless, we can be certain that they will provide a very noticeable boost to the company’s cash flow.

Financial Considerations

It is always critical that we look at the way that a company is financing itself before we make an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. As few companies have sufficient cash on hand to completely pay off their debt as it matures, this is typically accomplished by issuing new debt and using the proceeds to pay off the maturing debt. This can cause a company’s interest expenses to increase following the rollover depending on the conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline may push it into financial distress if it has too much debt. Although Targa Resources has remarkably stable cash flows, we should not ignore this risk as bankruptcies have occurred in the midstream sector.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. In addition, the ratio tells us how well the company’s equity will cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of September 30, 2022, Targa Resources had a net debt of $11.0646 billion compared to $4.7314 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 2.34. At first glance, this ratio seems incredibly high for any company but let us compare it to some of the company’s peers to get a better idea of whether this is correct:

|

Company |

Net Debt-to-Equity |

|

Targa Resources |

2.34 |

|

Kinder Morgan |

0.98 |

|

The Williams Companies |

1.62 |

|

MPLX (MPLX) |

1.50 |

|

Crestwood Equity Partners (CEQP) |

1.51 |

As we can clearly see, Targa Resources is relying considerably more on debt to finance its operations than any of its peers. This is a clear sign that the company is using too much leverage and thus may have greater risks of financial distress than many of its peers. This is, in fact, one of the concerns that we have had with respect to this company. I have discussed this in many previous articles here at Energy Profits in Dividends.

Ultimately though, the company’s ability to carry its debt is more important than the sheer amount of debt. The usual way that we judge this is by looking at the leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us how many years it will take for the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. In the third quarter of 2022, Targa Resources reported an adjusted EBITDA of $768.6 million, which works out to $3.0744 billion annually. This gives the company a leverage ratio of 3.60x, which is quite reasonable. As I have pointed out in various previous articles, analysts generally consider anything under 5.0x to be reasonable but I am more conservative and like to see this ratio under 4.0x in order to add a margin of safety to the investment. All of the recommended companies here at Energy Profits in Dividends are well under this 4.0x threshold but historically Targa Resources has not been. The company now appears to be, which is actually nice to see. The biggest reason why Targa Resources cut its dividend back in 2020 was to repay its debt and it has seemingly enjoyed a great deal of success at this task. This is therefore quite nice to see.

Dividend Analysis

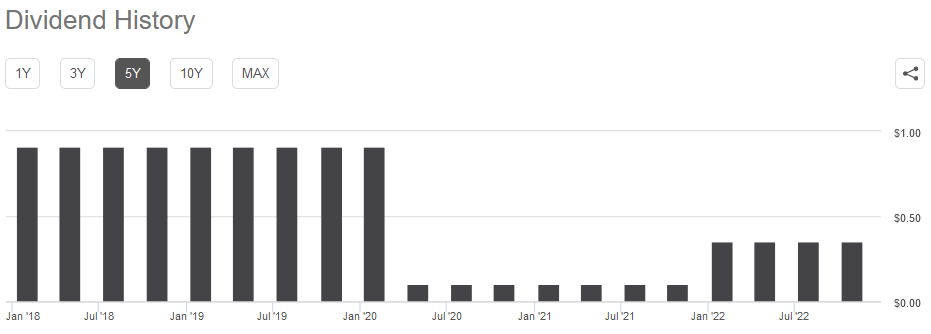

One of the biggest reasons why we invest in midstream companies is the high dividend yields that these companies tend to pay out. Targa Resources is unfortunately a notable exception to this rule as the company only yields 1.92% at its current price. This is because the company cut its dividend back in 2020 and, while it did increase it in early 2022, it still remains well below its peak:

Seeking Alpha

In addition to this, the company’s stock has appreciated by 28.31% over the past twelve months, which has also suppressed the yield somewhat. The fact that the company did cut its dividend in 2020 is likely to be a bit of a turn-off, especially since there are many other midstream companies that did not need to cut their payout. However, it is important to keep in mind that anyone purchasing the company’s shares today will receive the current dividend at the current yield and so does not really need to worry about the company’s disappointing past. Therefore, the important thing for our purposes is how well the company can maintain its current dividend. After all, we do not want to find ourselves the victims of another dividend cut since that would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we judge a midstream company’s ability to pay its dividend is by looking at its distributable cash flow. Distributable cash flow is a non-GAAP figure that theoretically tells us the amount of cash that was generated by the company’s ordinary operations and is available to be distributed to the common stockholders. In the third quarter of 2022, Targa Resources reported a distributable cash flow of $594.9 million but only paid $81.0 million in dividends. This gives the company a distribution coverage ratio of 7.34x, which is far above the 1.20x that analysts typically consider reasonable and sustainable. It is also well above the usual 1.30x that we like to see from a company that we are invested in. This incredibly high coverage ratio is one of the reasons why I suggested earlier in this article that Targa Resources may increase its dividend at some point since it can clearly afford to and seems to have gotten its debt somewhat under control. We should overall not have to worry at all about a cut here.

Conclusion

In conclusion, Targa Resources could certainly have potential despite no longer being a high-yielding stock. The company has made great strides at addressing the debt concerns that we have had about the company in the past, although the debt-to-equity ratio is definitely still a bit high. The company also has some significant growth prospects that are likely to play out over the next two years. When we combine this with a real likelihood of a dividend increase, we can see some real reasons to purchase the company today.

Be the first to comment