William_Potter

Investment Thesis

Axcelis Technologies, Inc. (NASDAQ:ACLS) designs, manufactures, and services ion implantation and other semiconductor chip processing equipment in the US, Europe, and Asia. Operating in the semiconductor sector, where most equities went down in 2022 owing to macroeconomic problems like FX, the company is well-positioned to benefit from the industry’s recovery.

ACLS’s stock price is up around 40% in the last year, and the company has a momentum of 38.66% compared to the industry’s -15.77%, showing that it is robust despite the market’s crushing in 2022. The balance sheet is strong, and the financials seem good, which compliments the company’s resilience ability. Although 2023 is expected to have some volatility, the long-term outlook is positive due to a growing market, so I am optimistic that the ACLS will weather the turbulence and greatly profit from the anticipated industry expansion.

2023 Outlook: Brace For Volatility

The year 2022 was filled with “Black Swans.” The conflict between Russia and Ukraine, pandemic lockdowns in China, and the US’s October 7 announcement of new export control regulations were among the unanticipated developments that caused supply chains to break down. By the end of 2023, it is projected that the Russia-Ukraine conflict will cost the global economy US$2.8 trillion in lost productivity.

The US Federal Reserve’s aggressive interest rate increases to fight inflation sparked several market stampedes, which may be compared to a grey rhino and impact consumers’ wallets since they leave them with less disposable cash to spend. The cryptocurrency market meltdown severely harmed the companies doing brisk business with bitcoin miners before the FTX bankruptcy. In 2023, the semiconductor sector will still have to worry about the flip in consumer demand for PCs and electronic gadgets and the industry-wide inventory adjustment that will accompany it.

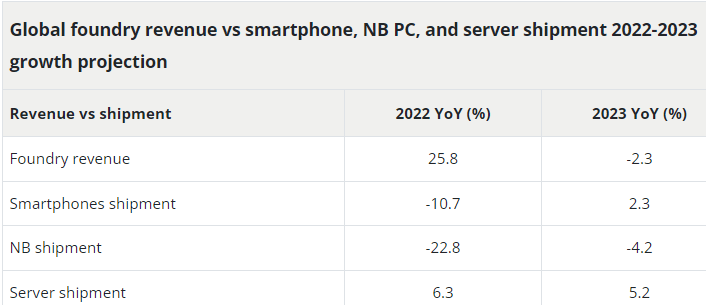

Due to the volatile nature of the global economy and the ongoing technological war between the United States and China, worldwide foundry maker revenues are expected to decline by 2-3% in 2023. Most semiconductor businesses’ revenues come from cellphones, notebook PCs, and other consumer electronics; thus, industry players want to know how 2023 will affect their business. Below are some projections regarding the same.

DIGITIMES Research

Despite the temporary setback, Chen asserts that there are patterns that create the demand to enable sustainable growth over the next five years. According to projections made by DIGITIMES Research, worldwide income from foundries will increase at a CAGR of 8.3% between 2022 and 2027, reaching US$204.7 billion.

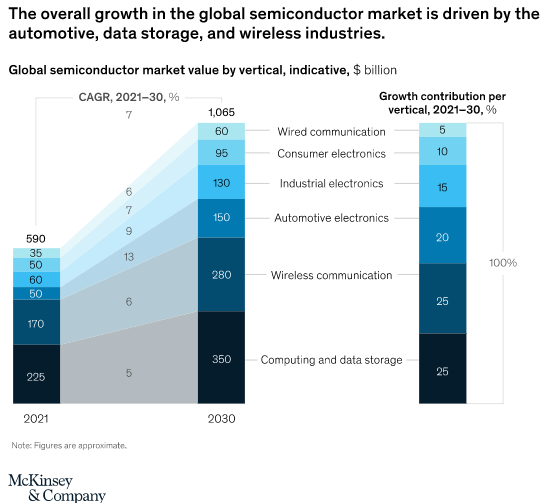

The Long-term View: A Trillion-dollar Industry By 2030

Semiconductor markets have grown, with revenues rising by almost 20% to $600 billion in 2021. Under various macroeconomic scenarios, McKinsey predicts that the industry will grow between 6% and 8% per year through 2030. By the end of the decade, the industry will be worth $1 trillion, based on the assumption that prices would increase by around 2% annually and that supply and demand will stabilize following the current instability, according to the estimations.

Manufacturers and designers should immediately assess the situation and ensure they are best positioned to benefit from the megatrends, including remote working, AI development, and the surge in demand for electric vehicles.

According to the research of 48 listed businesses, present stock valuations allow industry-wide average revenue growth of 6 to 10% up to 2030, assuming that EBITA margins range from 25 to 30 percent. However, some businesses are in a better position than others, and growth in a given subsegment may be anywhere from 5% to 15%.

McKinsey& Company

Financials

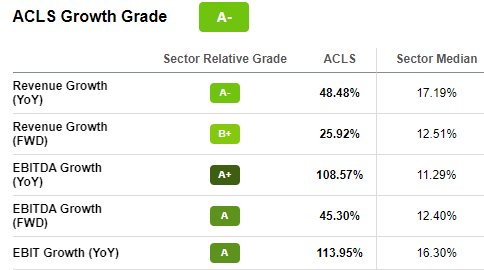

Despite a challenging 2020, the company’s finances look very good in absolute and relative terms. To begin with, the company has a YoY revenue growth rate of 48.48%, an EBITDA growth rate of 108.57%, and an EBIT growth of 113.95%. These figures are well above the industry average, demonstrating the company’s resilience in the face of a challenging macroeconomic environment and its ability to outperform its competitors.

Seeking Alpha

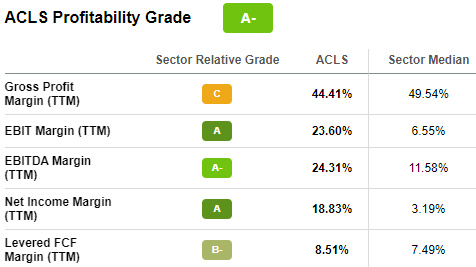

The company’s profitability is enticing, especially when viewed in relative terms, and it follows the fantastic growth data presented above.

Seeking Alpha

Other than the gross profit margin, the company’s profitability metrics are above the industry median. For example, the company’s net income is about 490% higher than the industry median. These enticing profit margins place the competition in the position of being the profitability underdogs.

Additionally, the company’s balance sheet is solid; they have a debt of $58.55M which is 0.019X its market cap of $3.14B. The low debt ratio shows the company is almost wholly deleveraged, which is very assuring, especially when the economic climate is harsh. In terms of liquidity, it has a current ratio of 3.73X and a cash balance of $342.13M, which is enough to cover its TTM total operating expense of $178.9 1.9X; its liquidity is complimented by the company’s ability to generate cash exhibited by its cash flows from operations of $131.33M.

Risks: Escalating US-China Tech War

Over the past decade, US officials have viewed their country’s technological dependency on China as a security risk. They have worked to reduce the flow of technology products, services, and inputs to and from China. The United States began a new phase of industrial policy. It escalated its tech war with China by enacting the CHIPS and Science Act of 2022 in August and the regulatory filing by the Commerce Department Bureau of Industry and Science.

The Bureau of Industry and Security of the US Department of Commerce issued a sweeping set of export restrictions on October 7 intended to impede China’s domestic advancement of crucial technologies like semiconductors. US corporations couldn’t continue to provide Chinese chipmakers semiconductor production equipment, such as SME components, that can build relatively advanced chips without a license, among other restrictions.

Uncertainty surrounding this fight presents a significant danger to the semiconductor business, and investors should be concerned. It is currently unclear how China will respond or what implications that response will have on the industry.

My Assertions

Some degree of volatility is expected to persist into 2023, but less so than in 2022. I anticipate a better performance from this company this year because it managed to survive the challenging state of 2022 and post such a stellar financial performance. The factors that will sustain growth, in the long run, are of particular importance to me. The company’s commitment to these drivers and identification of them as cornerstones of their long-term growth is encouraging in light of the robust growth potential forecast for the industry through 2030.

ACLS Q3 Transcript Presentation

In my opinion, this company’s financial health demonstrates its resilience in the face of temporary setbacks. It hints at robust, sustainable growth in the years to come thanks to its excellent position relative to the growth levers that will drive that growth. In sum, this is a prosperous time to invest in this firm, both now and in the future, but investors should be wary of the risks.

Be the first to comment