DieterMeyrl/E+ via Getty Images

Magino Cost Overrun & Investment Thesis

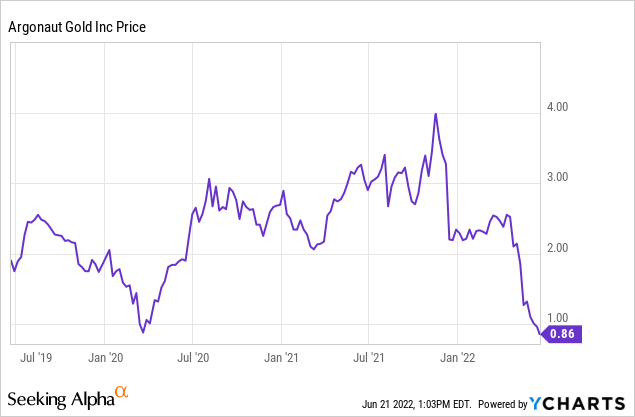

I first bought Argonaut Gold (OTCPK:ARNGF) in February of 2020, and I have covered it several times here at Seeking Alpha since then. While 2020 and much of 2021 were good to Argonaut, the stock has gotten severely punished over the last nine months.

Figure 1 – YCharts

The initial substantial decline in late 2021 was due to the very large cost overrun for the Magino build, where the estimate went from C$510M to C$800M. The second recent decline in Q2 of 2022 was related to the announcement that the second set of estimates was too low as well, and the total capital build is now estimated to be around C$920M.

While the news is very hard to swallow given that Argonaut initially highlighted that part of the project spend was fixed and because the revised estimate was made very recently and included a contingency of C$61M.

The problem is that Argonaut now needs to raise somewhere around C$400M in a depressed market with an even more depressed stock price to be able to complete the Magino build. Both a self-financing option via the debt and equity markets and strategic alternatives are being investigated, where we can expect a confirmation in the next few weeks. There is always the alternative of pushing out the Magino build as well even if it is a less desirable option due to the running costs for a half-built project.

So, with 20/20 hindsight, it would have been ideal to sell the stock in late 2021. There is also a lot of uncertainty related to how much the company can raise via debt financing, what concrete interests there are for a joint venture or outright sale of Magino or the company. However, at the current price, the long-term risk is quite low, almost regardless of the outcome.

Other Value Destruction

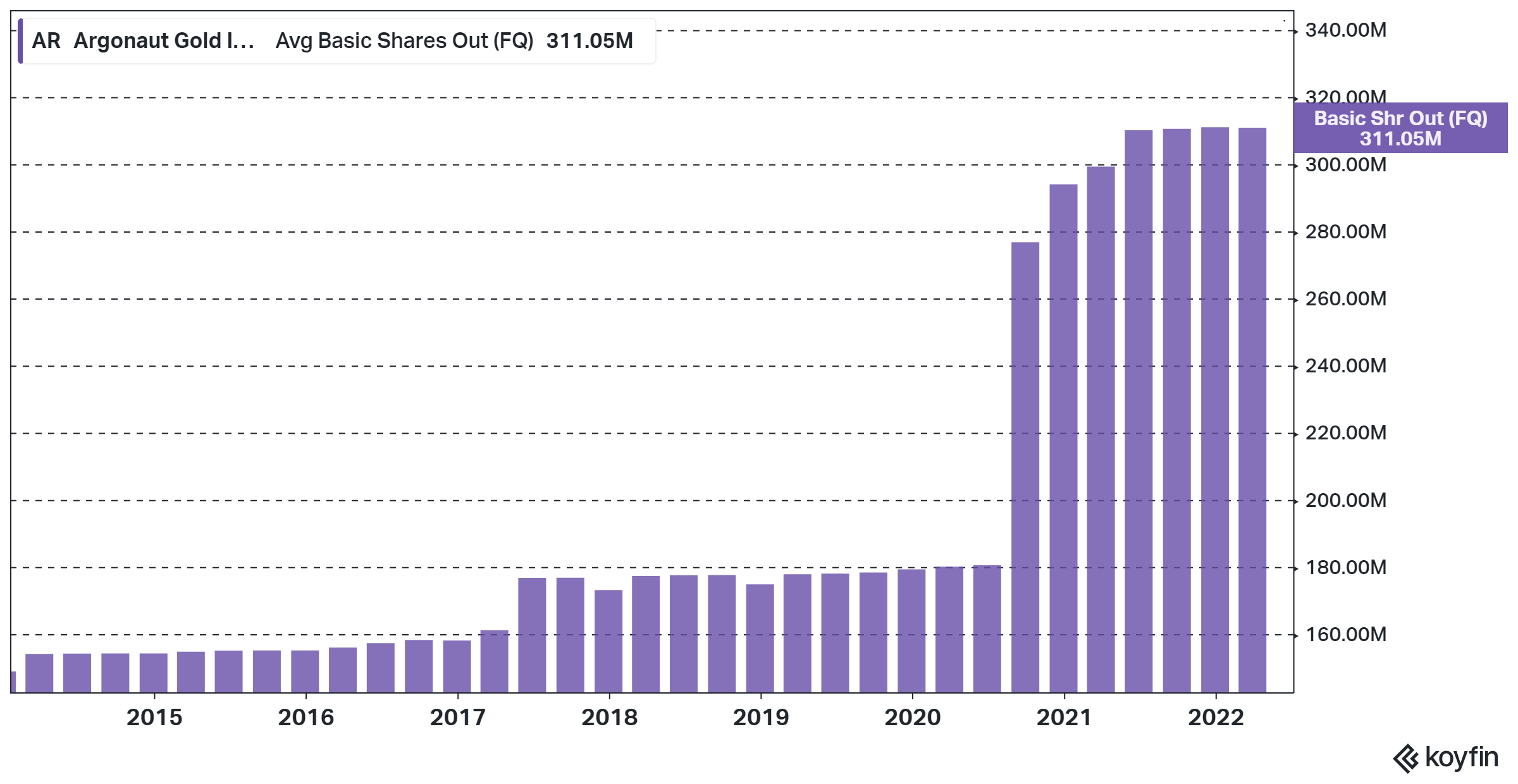

Apart from the Magino disaster, which is partly due to bad luck with the timing and inflation, even if part is certainly on management as well. Another strategic decision which has turned out very poorly is the merger with Alio Gold. While it sounded good to get an underperforming U.S. asset at a time when the market was depressed. If Argonaut would have bought Alio Gold with cash, there would have been little to object against, but Argonaut saw the share count increase by about 50% in 2020 due to the merger.

Figure 2 – Koyfin

So, what did Argonaut get for a 50% increase in the share count? Put bluntly, a development asset in Mexico that cannot be sold and Florida Canyon in the U.S., which is just barely producing positive cash flows at record gold prices. Compare this to the Mexican producing assets, which have been producing solid cash flows for quite a while.

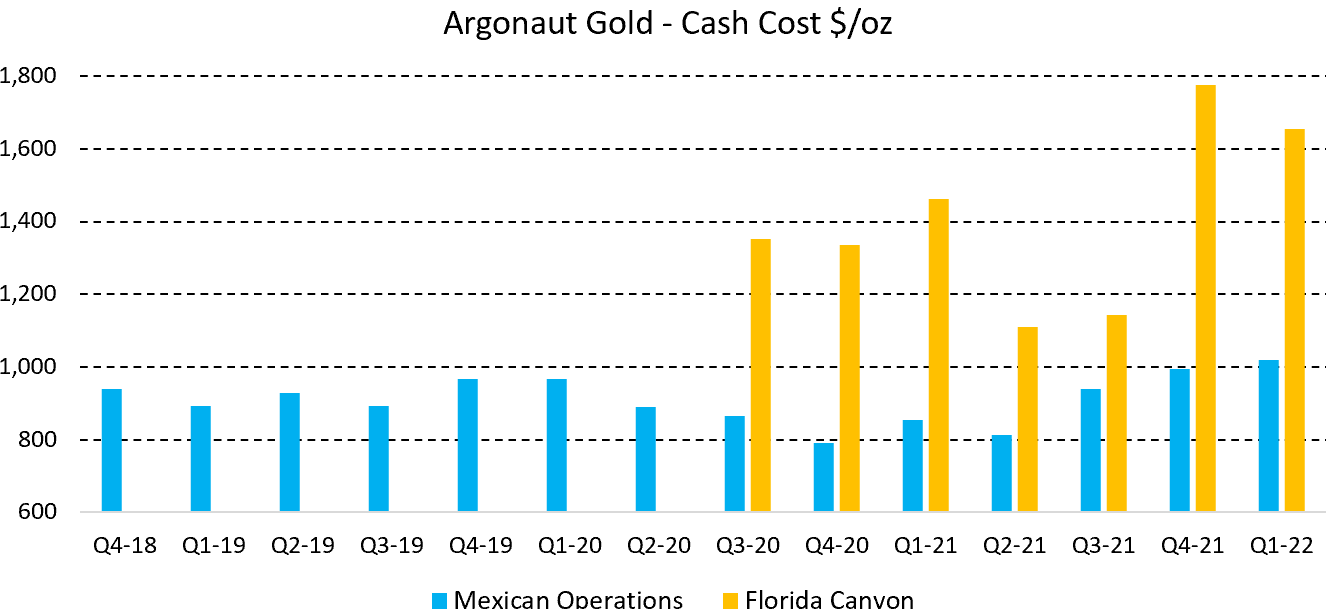

Figure 3 – Quarterly Reports

Note that this is even though Argonaut has invested heavily in Florida Canyon over the last 18 months, the asset had $10M in capital expenditures in 2020 and $29M in 2021. In Q4-21, both the development asset Ana Paula and Florida Canyon that came with the merger were partly written down. This has likely not been positive for the share price as well.

Valuation

Using the latest share price and financials from Q1-22, we are currently looking at a market cap of only $215M and an enterprise value of $186M for Argonaut Gold. Note that the enterprise value will increase just to cover contract commitment when the cash position is drawn down regardless of the scenario.

Figure 4 – TradingView & Q1-22 Financials

Provided Magino moves forward within Argonaut, there will be further dilution if equity is used to partly finance the project. Alternatively, the ownership in Magino will be diluted in a joint venture scenario.

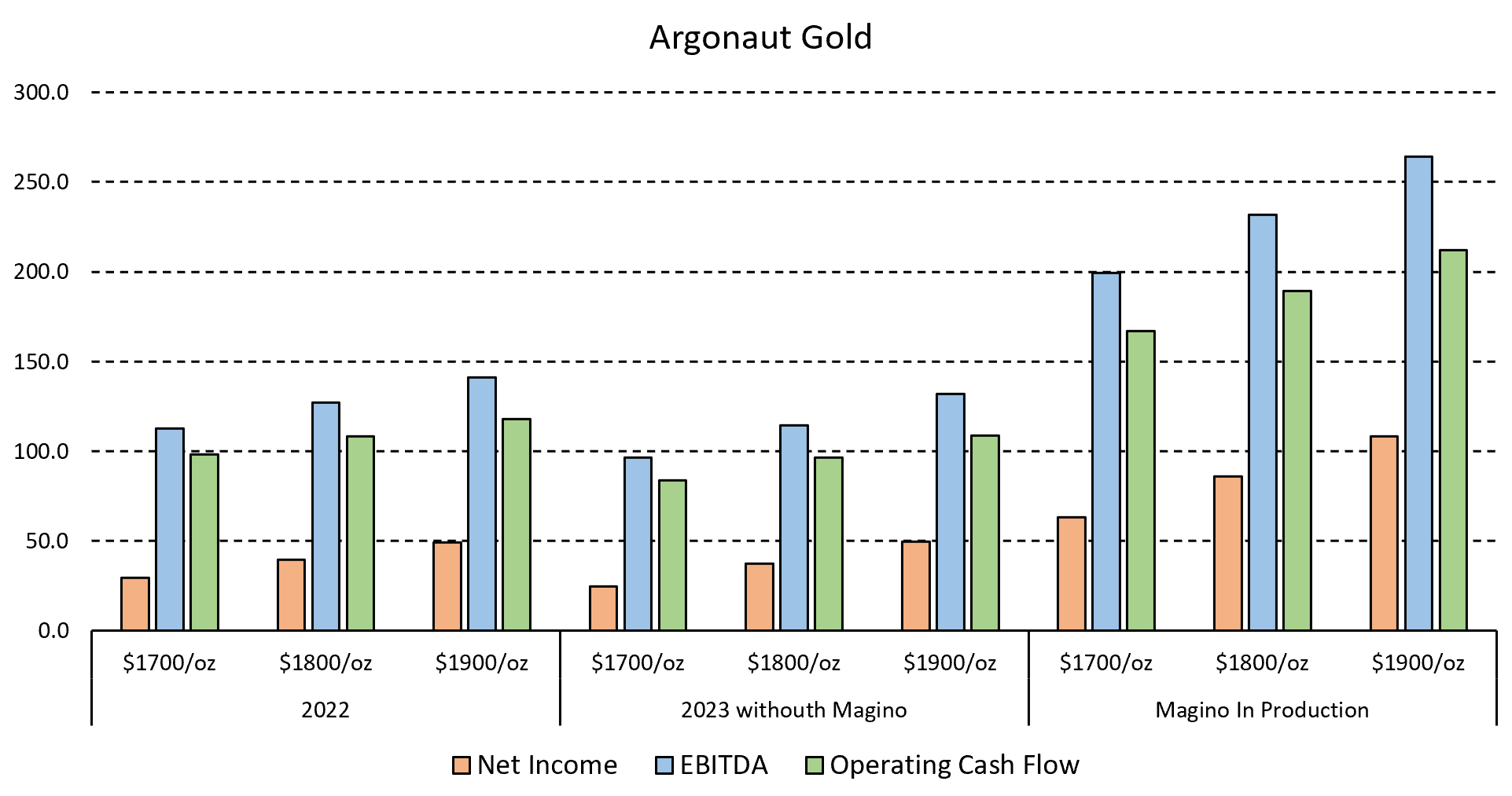

In the below chart you can see my Argonaut estimates for the years 2022, 2023 without Magino, and once Magino is in production, which would likely be from H2 2023 the earliest. I would highlight that there will be more dilution in the later scenario.

We are looking at a company with a $215M market cap, that will be producing operating cash flow around $100M in 2022 and 2023 at the current gold price without Magino. The company would very likely get a few hundred million U.S. Dollars for Magino if it ended up being sold as well.

Figure 5 – My Estimates

I certainly hope the company can keep any equity dilution to a minimum at this very depressed share price. However, even with a $100M-$150M bought deal and the rest in the debt market, the future looks quite bright for Argonaut Gold which with Magino would be producing around $200M in operating cash flow per year.

Conclusion

Argonaut Gold has ended up in a very precarious situation, and management should rightly get some criticism for this situation. I also got this story very wrong as I could not imagine cost overruns of this magnitude when part of the costs was fixed. I have consequently seen large unrealized losses in 2022 even if I have continued to buy in the recent weakness.

The market always detests uncertainty, and there is certainly a lot of that with Argonaut at the moment. However, I would argue much, if not most, of the downside appears to be priced in at this level.

It is important to remember that Argonaut Gold is still a producer with solid cash flows and I think the likelihood is very high that the share price is substantially higher in 12-18 months from here, regardless of how management chooses to move forward with Magino.

Be the first to comment