Natali_Mis

A good market drubbing can be great for income investors, especially when it comes to high yielding names. That’s because a price drop on a high yield stock does more to push up the dividend yield.

For example, a stock yielding 2% that goes down by 10% would still yield just 2.2%, whereas with the same drop, a stock yielding 10% would jump to an 11% yield.

This brings me to Ares Commercial (NYSE:ACRE), which has seen its yield jump past 11% on recent share price weakness. Let’s see why this presents a solid opportunity for value and income investors.

Why ACRE?

Ares Commercial Real Estate is a large commercial mortgage REIT that’s externally managed by the alternative investment juggernaut, Ares Management (ARES), a well-known asset manager that also happens to manage Ares Capital (ARCC), the largest BDC by asset size.

ACRE benefits from its affiliation Ares Management, as the latter has over $50 billion in real estate assets under management. This affiliation is valuable for ACRE, as it benefits from an experienced management team that’s in the know about real estate deal flows.

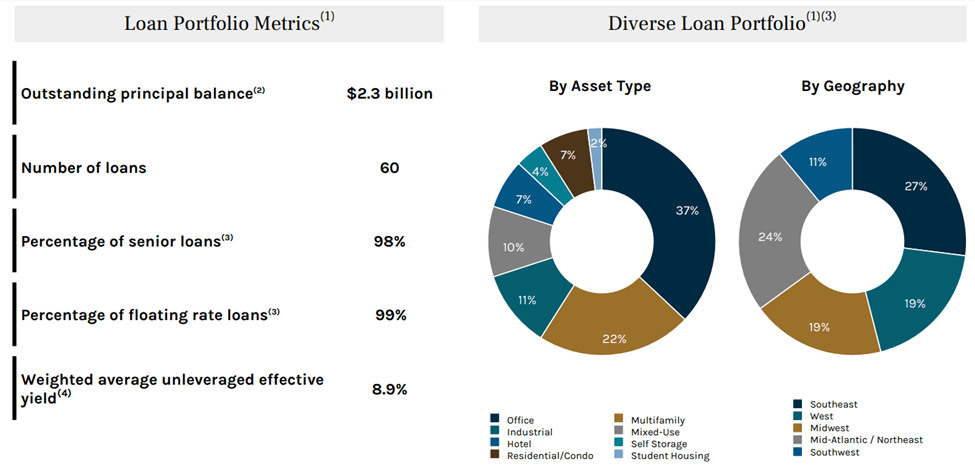

Meanwhile, ACRE carries a strong $2.3 billion loan investment portfolio with 98% senior loans that are spread across 60 underlying property assets. Commercial mortgage REITs such as ACRE also benefit from being able to pivot its investments rather quickly due to relatively short duration of loans that generally last for just a few years.

This is reflected by ACRE’s pivot towards loans to multifamily properties, which is a better positioned asset class in an inflationary environment. Since the end of 2021, ACRE’s allocation towards multifamily loans has grown from 13% to 22%, while hotel decreased from 10% to 7%. As shown below, ACRE is also well-diversified by geography, with office, multifamily, and industrial assets being the top 3 property types secured by underlying loans.

Investor Presentation

Moreover, ACRE originated $56 million in new commitments during the fourth quarter, bringing total FY 2022 commitments to $753 million, equating to over one-third of its total current portfolio. Funding was supported by $823 million in loan repayments over the same time period.

While ACRE collected 99% of its interest payments from its borrowers during Q4, it’s worth noting, that ACRE’s portfolio quality has declined since the end of Q3, with the percentage of loans rated 3 or higher declining from 90% to 80% as of year end 2022. Management highlighted during the recent conference call the reasoning behind the change as well as the successful resolution of a loan on no-accrual after recovering 98% of its original investment

This change primarily reflects the negative migration of one office property loan and one mixed-used proper loan, which were downgraded from three to four due to our outlook on their respective business plans and our macroeconomic view of their respective submarkets. As it relates to CECL, we increased our total reserve by $19.4 million during the fourth quarter of 2022 and our total CECL reserve stands at $71.3 million or about 3% of our total loan commitments at year-end 2022.

Shifting to post quarter end activity in January 2023, we successfully resolved a senior loan backed by a residential property located in California. Through our structuring capabilities and the experience of our asset management team, we were able to recover approximately 98% of our cumulative cash investment in this loan.

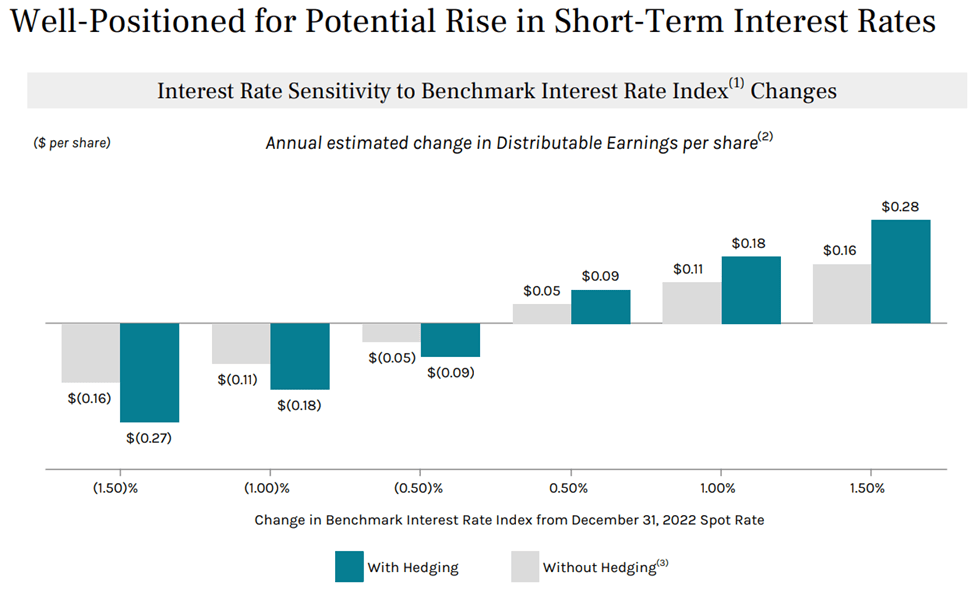

Looking forward, ACRE stock is well-positioned from a balance sheet standpoint as it carries a reasonably low debt to equity ratio of 2.1x and has $216 million in available capital. It’s also benefitting from high interest rates as 99% of its loan portfolio is floating rate. As shown below, ACRE could see up to $0.09 annual distributable EPS benefit from every 50 basis point increase in the benchmark interest rate.

Investor Presentation

ACRE is already reaping the benefits from higher rates, as it generated $0.44 in distributable EPS during the fourth quarter, resulting in 1.33x coverage on its regular dividend of $0.33, and giving it plenty of room to pay a $0.02 supplemental dividend this quarter.

Lastly, I see plenty of value in ACRE at the current price of $11.73 with a price to book value of 0.85x. As shown below, this sits on the low end of ACRE’s trading range over the past 5 years outside of the 2020 timeframe. Analysts also have a Buy rating on the stock with an average price target of $12.86. This is still below ACRE’s book value and could translate to a potential one-year 21% total return including dividends.

ACRE Price-to-Book (Seeking Alpha)

Investor Takeaway

Ares Commercial continues to see strong interest collection and is benefitting from higher rates. It maintains a solid balance sheet for a commercial mortgage REIT and the portfolio is well diversified with higher exposure to multifamily assets compared to the end of 2021.

Recent price dislocation has pushed the dividend yield past 11% and it has plenty of wiggle room to continue declaring supplemental distributions. As such, income investors may want to take advantage of the recent discount in share price.

Be the first to comment