Funtap

Thesis & Introduction

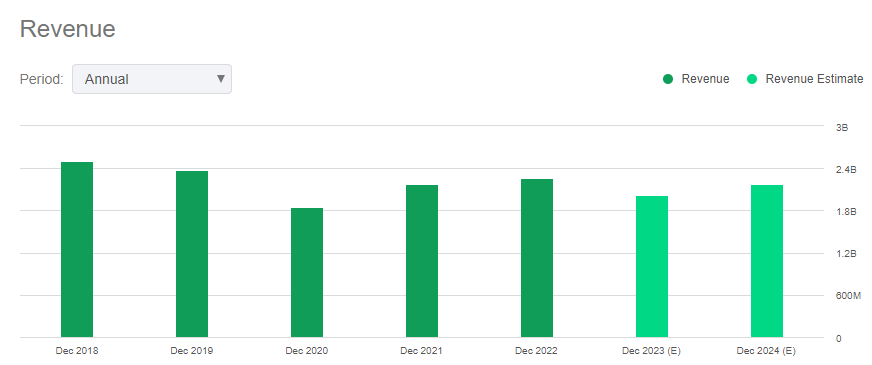

One might think that human resources and employment services companies would flourish given the unemployment rate hitting a 53-year low in the United States. Ironically, these businesses are finding it difficult to sustain their revenues and margins. TrueBlue, Inc. (NYSE:TBI) hasn’t been able to recover since the pandemic rout in 2020, even after a strong bounce back by the economy in 2021. Its sales in 2022 ($2.3B) have grown almost 17% compared to 2020 ($1.8B) but are still way below average sales of $2.5B from 2015 to 2019. This is not surprising given the declining revenues of the company since 2017, when sales hit an all-time high of $2.7B, only to come down to $2.3B in 2019. This may indicate that the company has found it difficult to acquire new clients and penetrate existing and/or new markets. With the recession still not being out of the question, 2023 is only going to get tougher for TrueBlue. Though other major companies in the industry are in a similar position, TBI has faced four down revisions in revenue as well as EPS since April 2022, further validating a difficult road ahead for the company in 2023 and 2024.

Seeking Alpha

TBI operates in three segments: PeopleReady (PR), PeopleManagement (PM), and PeopleScout (PS). PR provides staffing solutions for blue-collar industries, while PM provides contingent labor and outsourced industrial workforce solutions. PS offers permanent employee recruitment process outsourcing and manages contingent labor programs.

Industry Analysis

As companies in the staffing industry compete for distinction, they often seek to differentiate themselves through their legacy of service, sectoral expertise, investments in technology, and singular systems and protocols. As per the recent earnings presentation, the executives of TrueBlue have conveyed their intention to digitalize PeopleReady, their highest revenue-generating segment, which they believe will allow them to outperform less established rivals and lower their operational expenses. The workforce solutions sector is inherently cyclical and susceptible to shifts in demand for temporary staffing services, influenced by the fluctuations of the economy and seasonal patterns. This partly explains the downward revisions of revenue and EPS due to increasing uncertainty about economic and political outlooks since the beginning of 2022.

Debt-free with financial stability

The company, in 2022, attained a monumental feat by eradicating its debts and becoming one of the few debt-free entities in the staffing industry. This development has allowed for the redirection of its prior interest expenses, exceeding $1.5M, and with net margins as low as 2.8%, it will create more value for common stockholders. Despite abstaining from distributing dividends, the company has demonstrated its financial stability and commitment to its equity shareholders by repurchasing shares worth an average of $40M annually over the past five years. The company’s tangible book value per share stands at $11.89, resulting in a price to tangible book value ratio of 1.5, significantly below the industry average of 3.7, making it undervalued. Despite challenges with its top line, the company has maintained robust operating and overall cash flows, reflected in its current and quick ratios of 1.8 and 1.6, respectively, surpassing the industry averages of 1.5 and 1.2.

Revenue and margins, both at risk

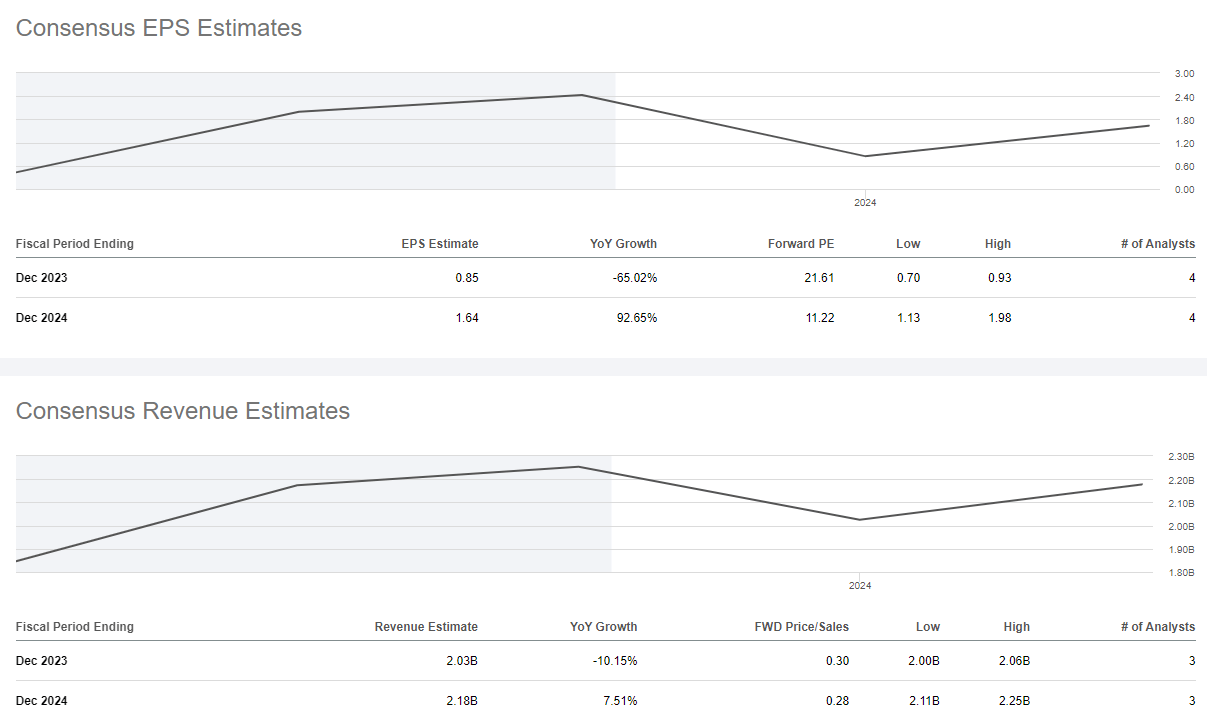

As per the latest earnings presentation, the company will have a reduction in revenue during the first and second quarters of 2023 compared to 2022, which will be roughly 7% and 4% respectively. This serves as the final piece of the puzzle that explains the downward revision of revenue from $2.51 billion in April 2022 to $2.03 billion recently, and earnings per share from $2.51 to $0.85. The shares of the company also haven’t seen much volatility in a decade where prices ranged from $13 to $31 and the current price of $18.37 is the same as it was ten years before. This is due to the fact that more than 90% of shares in the company are held by institutional investors, which usually works in favor of the company. However, low insider shareholding (1.8% only) often raises concerns about the management’s confidence in the company. As stated earlier, the company is working with very thin margins of 2.8%, which is significantly below the industry average of 9.6%. As almost 60% of revenue comes from the PR segment, which is also their second-highest profit margin segment, the chances of them shrinking further are reasonably high. Adding to that, the company also expects $3M worth of PeopleReady technology upgrade cost, further threatening their margins.

Seeking Alpha

Valuation

Companies in the human resources and employment services industry trade at a median P/E multiple of 15.1x while their average P/E is 17.2x. On the other hand, TBI is trading at a P/E multiple of only 9.8x. For valuing TBI, I will proceed with 15.1x as it is closer to its current P/E.

|

Particulars |

Value |

|

Normalized net income (TTM) |

$45.0M |

|

P/E GAAP (TTM) |

15.1x |

|

Value of equity |

$680.3M |

|

Number of outstanding shares |

32.7M |

|

Intrinsic value |

$20.8 |

The intrinsic price of the share based on P/E valuation is slightly above the current price of $18.37, making it undervalued, but a risky proposition.

Final Thoughts

Stock Tracking Opinion

TrueBlue has been in the business for more than 40 years, and they have survived obstacles including the dot-com bubble of 2000 and the great recession of 2008. Since the pandemic, the company hasn’t been able to showcase its ability to bounce back, and with macroeconomic pressure, matters are only going to get worse for a while. What I like about the company at this point is its financial position and its latest achievement of becoming debt-free, which will provide a long rope to the company for turning the tables and attaining revenue growth. Hence, I will keep this on my watchlist.

Investment Opinion

Given the disappointing outlook, I would have rated this a sell in line with its Quant rating on Seeking Alpha, but I prefer waiting to analyze its results over the next couple of quarters. Hence, my current opinion on TBI is a Hold.

Be the first to comment