jetcityimage

The transportation and logistics industry operates in a highly cyclical industry. Market volatility and moderating freight demand are evident. Yet, ArcBest (NASDAQ:ARCB) rises above all these challenges. Its performance shows a balance between growth and viability. Fundamental soundness is visible through its stellar Balance Sheet. As such, ARCB is well-positioned against macroeconomic disruptions.

Moreover, borrowings and dividend payouts remain well-covered by adequate cash reserves. Dividend yields may be unexciting, but security and consistency are guaranteed. Meanwhile, the stock price adheres to company fundamentals and stays fairly valued.

Company Performance

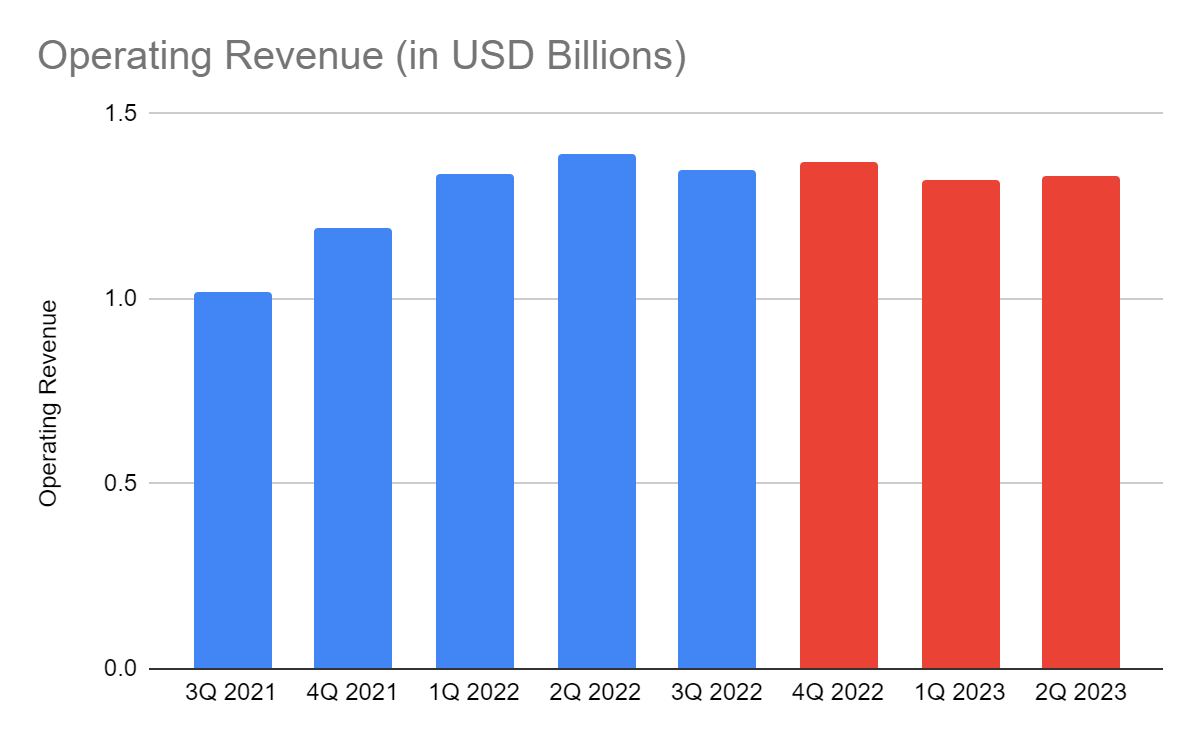

The transportation and logistics industry sees the freight demand cooldown and a potential recession. Although inflation has continuously decreased from its peak last June 2022, the purchasing power is yet to bounce back. Despite this, ArcBest Corporation demonstrates its impeccable ability to navigate the rugged market. It keeps its core operations stable as it balances revenues with margins. Currently, its operating revenue is high at $1.35 billion, a 32% year-over-year growth. This desirable outcome can be attributed to several factors.

Operating Revenue (MarketWatch And Author Estimation)

One of the primary driving forces is its capitalization on expansion to increase its market presence. Its acquisition of Molo in 2021 continues to pay off amidst the crowded freight brokerage market. It secures its place in the market, given its access to over 70,000 carrier partners. A higher network capacity is also one of the things it enjoys. It is a crucial aspect to keep up with supply chain changes and cater to more customers. Also, its strategic pricing allows it to offset the impact of the elevated fuel and equipment prices. Although customer demand softens, it stays at a manageable level. Sequential values may not be too impressive, but the absolute strength in Q3 is undeniable. Higher shipments and tonnage, matched with solid pricing and fuel surcharges are other growth drivers. Also, LTL like ArcBest has a relatively shorter distance than larger carriers. Hence, it is easier for them to maximize the advantages of fuel surcharges.

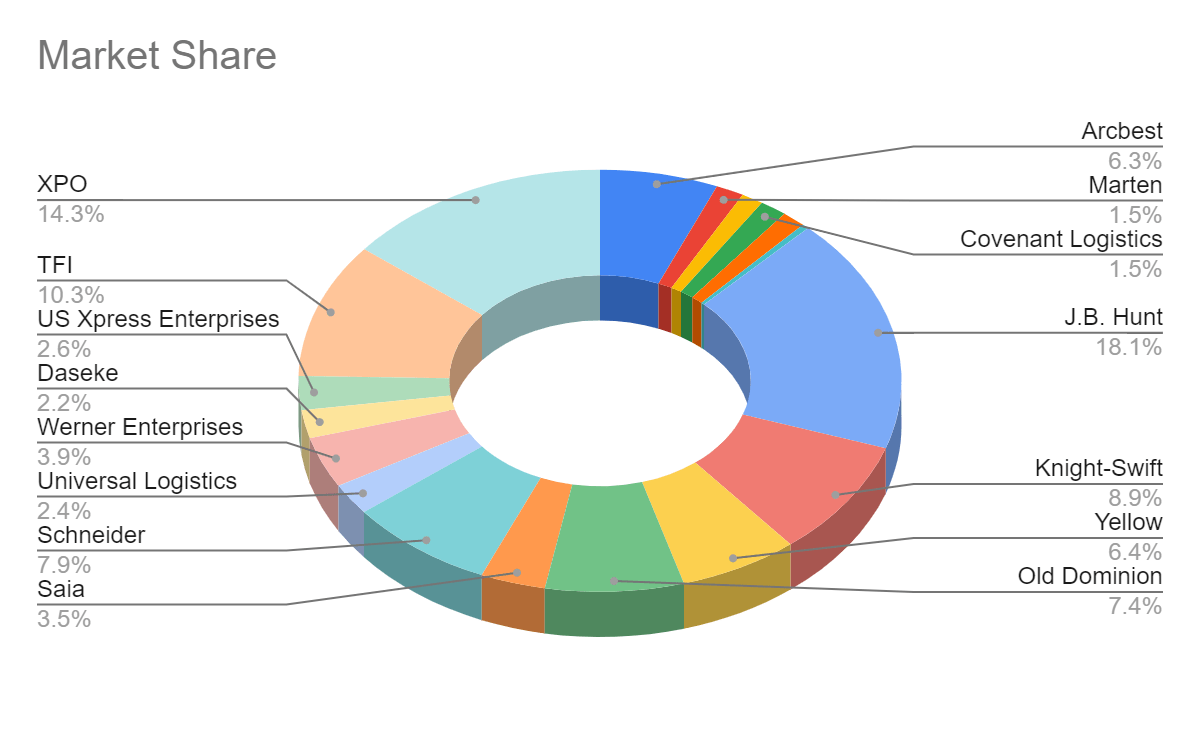

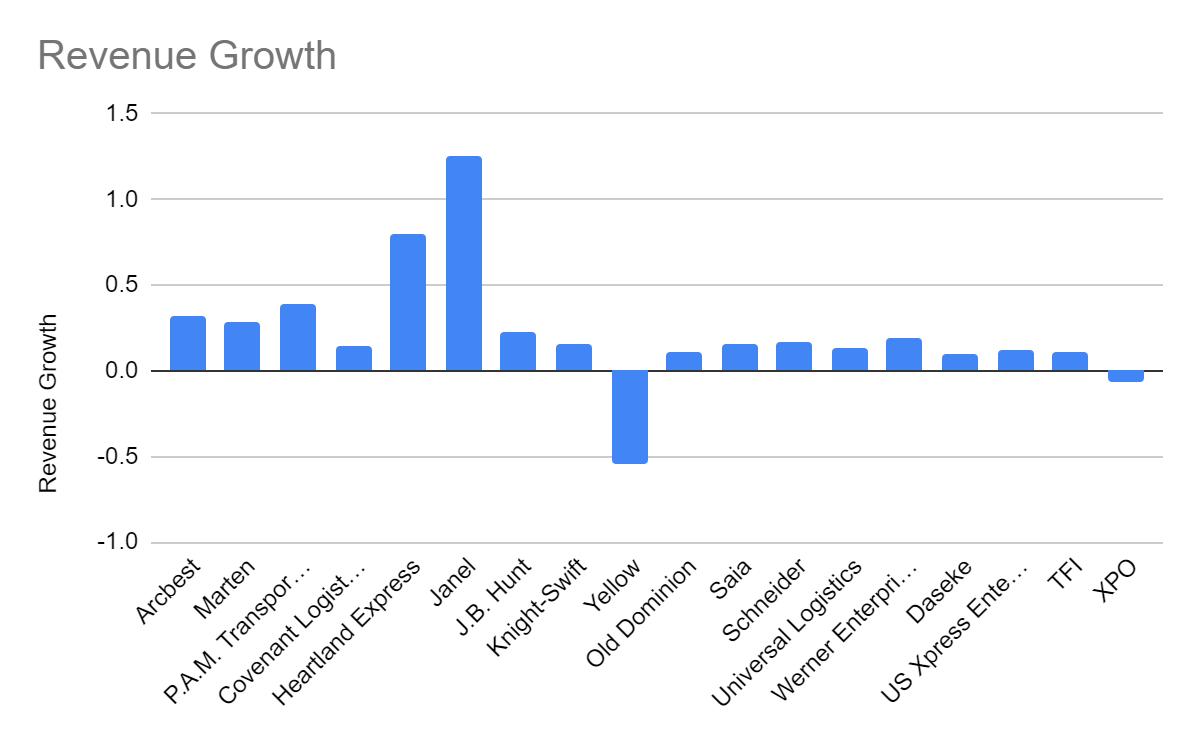

Concerning its peers, ArcBest remains relatively smaller than some truckload and LTL giants. But it holds a considerable portion of the market. Its market share of 6.3% is a substantial improvement from 4.9% in the comparative quarter. It should not be surprising, given its impeccable revenue growth, exceeding the market average of 22%. ARCB even exceeds many popular peers, such as Old Dominion Freight Line (ODFL), Yellow Corporation (YELL), Knight-Swift (KNX), and Saia (SAIA).

Market Share (MarketWatch) Revenue Growth (MarketWatch)

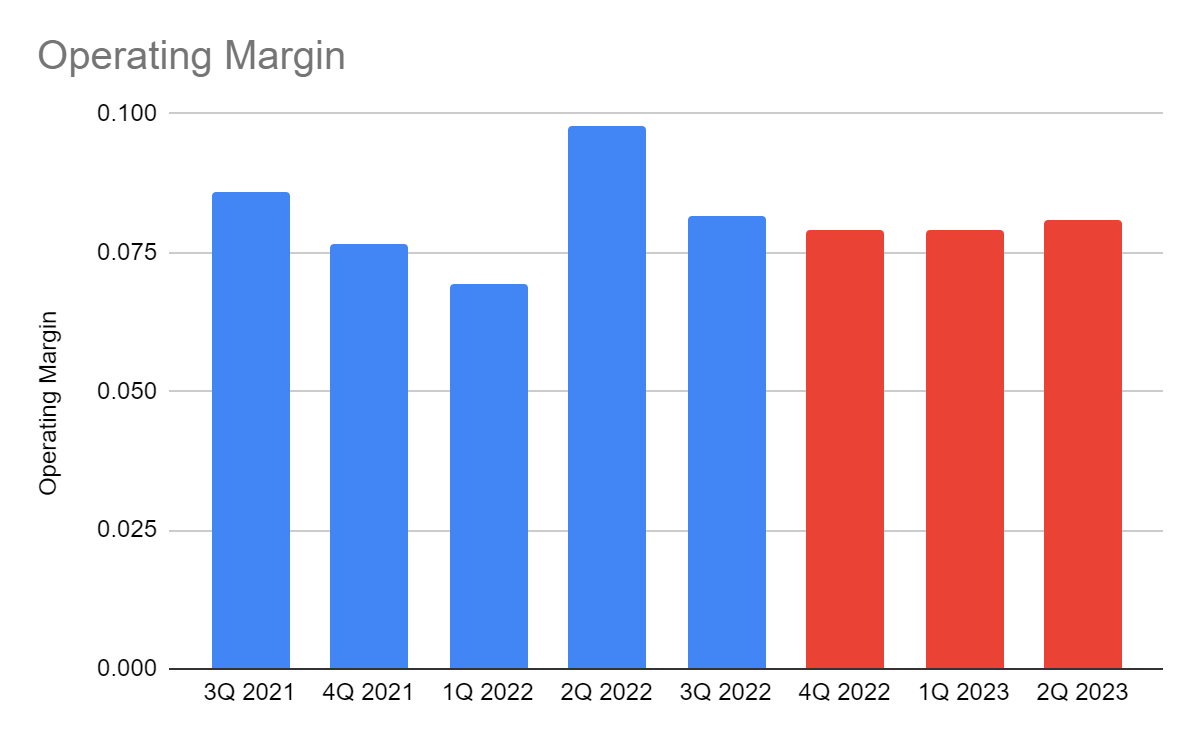

Likewise, costs and expenses are on an uptrend. Cost pressures are evident, mainly from labor-related expenses, fuel prices, and equipment. Currently, the industry navigates a tough macroeconomic environment while supply chain consistency has yet to improve. Despite this, its effort to stabilize margins remains fruitful. The increase in costs and expenses is still proportionate to revenues. This aspect can prove prudence regarding pricing and network capacity utilization. Its operating margin remains stable at 8.1%, although lower than in the comparative quarter.

This year, I expect ArcBest to balance growth with viability to maintain operational stability. There may be lower volume and pricing as demand cools down. The sequential decrease in 2022 has been observed and may continue. Even so, I don’t believe ArcBest will take a nosedive. After all, LTL is less sensitive to cyclical changes than truckloads and long-hauls. I also think the continued decrease may either imply higher normality or seasonality. With that, I expect lower but stable revenues. It may have a substantial impact on margins. But I also expect ArcBest to improve its cost-efficiency as inflation continues to lull. Crude oil and gasoline prices are more stable than in the last quarter.

Operating Margin (MarketWatch And Author Estimation)

How ArcBest Corporation May Fare This Year

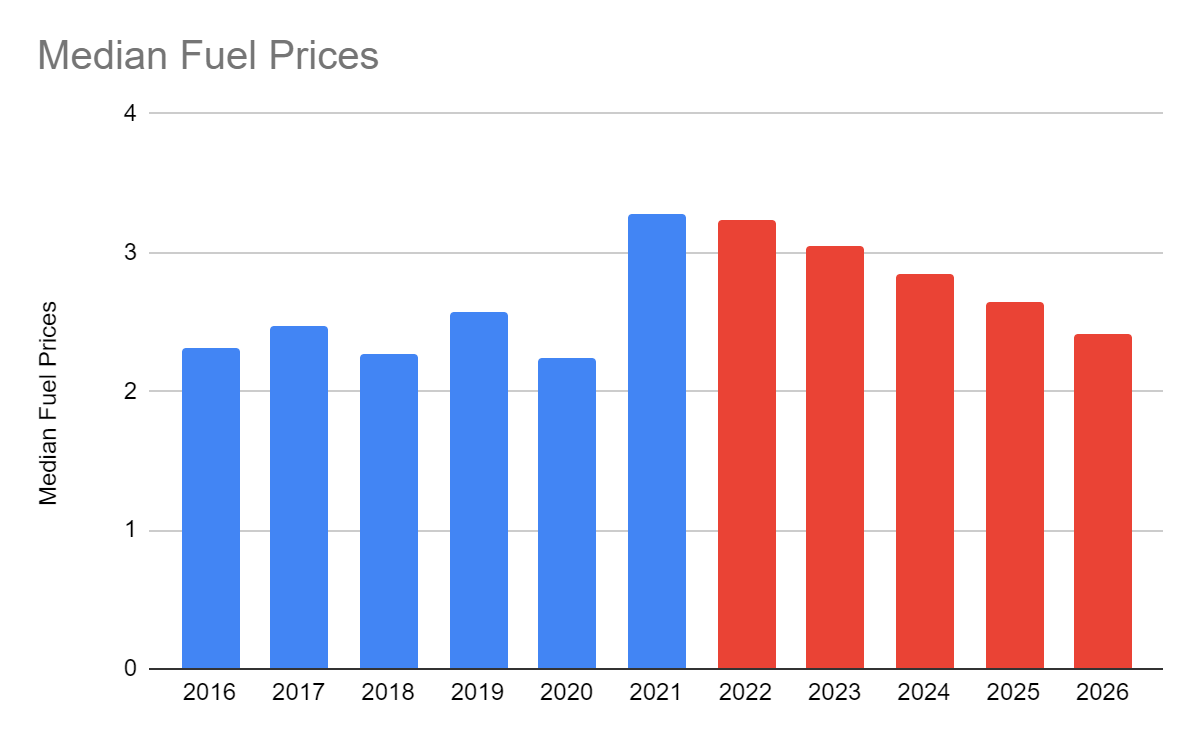

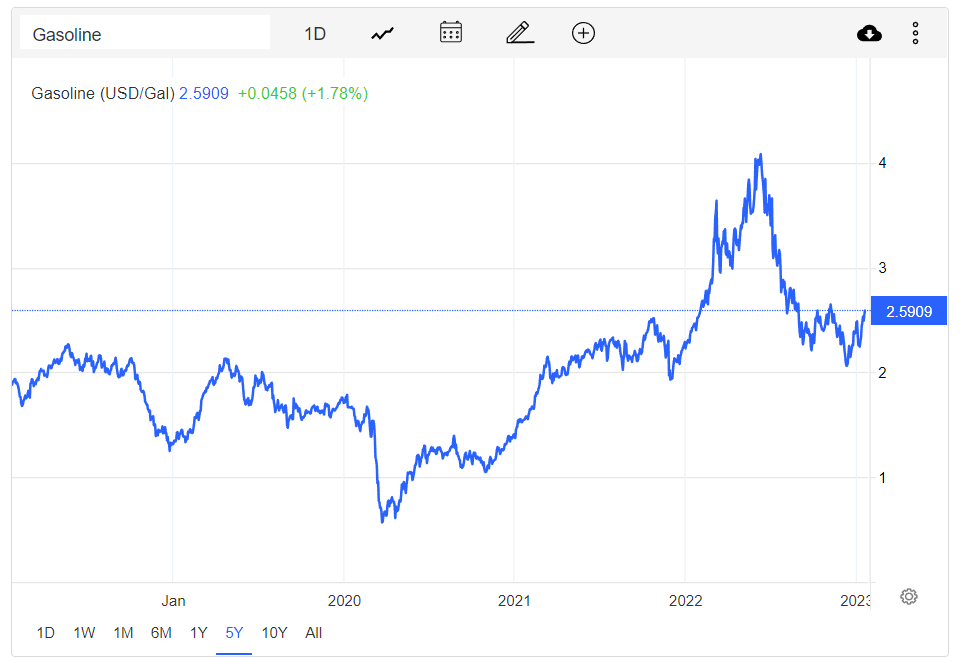

Moderating freight demand and recession fears are the top concerns of the industry this year. Even I, myself, agree with the current supposition of the industry performance. Despite all these, I am not pessimistic at all. I expect some boons to materialize and give decent prospects. First, inflation has decreased faster and further than expected. At only 6.5%, it has already dropped by 30% in six months. That is why it is not unsound to expect fuel and equipment prices to be more stable. Of course, the Russo-Ukrainian War should not be discounted. But inflation lull may start to help normalize crude oil and gasoline prices.

Median Fuel Prices (ST. LOUIS FED And Author Estimation) Crude Oil Price (Trading Economics) Gasoline Price (Trading Economics)

Meanwhile, recession fears are present, given the persistent interest rate hikes. But I am not buying the over0pessimistic sentiment due to several reasons. First, the inflation lull may help stabilize interest rate changes. The interest rate may keep increasing since the Fed must stay conservative. Despite this, increments may slow down. Also, I set its peak at 4.5-4.8% compared to the 5-5.25% consensus estimates. Second, the labor market conditions are stable, even better than in the Great Recession. The unemployment rate remains low with increased wages. Third, business activities may increase as pandemic restrictions continue to ease. Fourth, tourism and e-commerce may play a vital role in an economic rebound. Lastly, there is anticipated spending on infrastructure, given the infrastructure law’s investment program. There may be more movements of construction materials, which may stimulate growth in the transportation and logistics industry. Also, the long-run advantage of shorter travel time and distance may help the company.

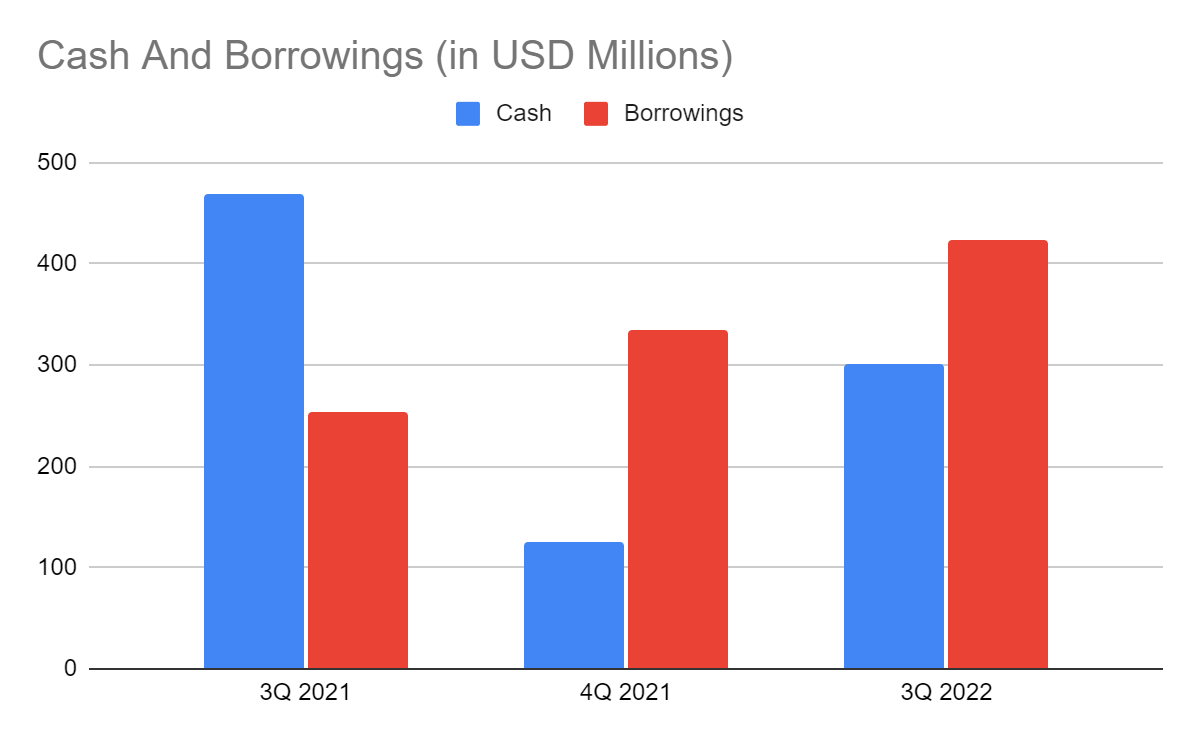

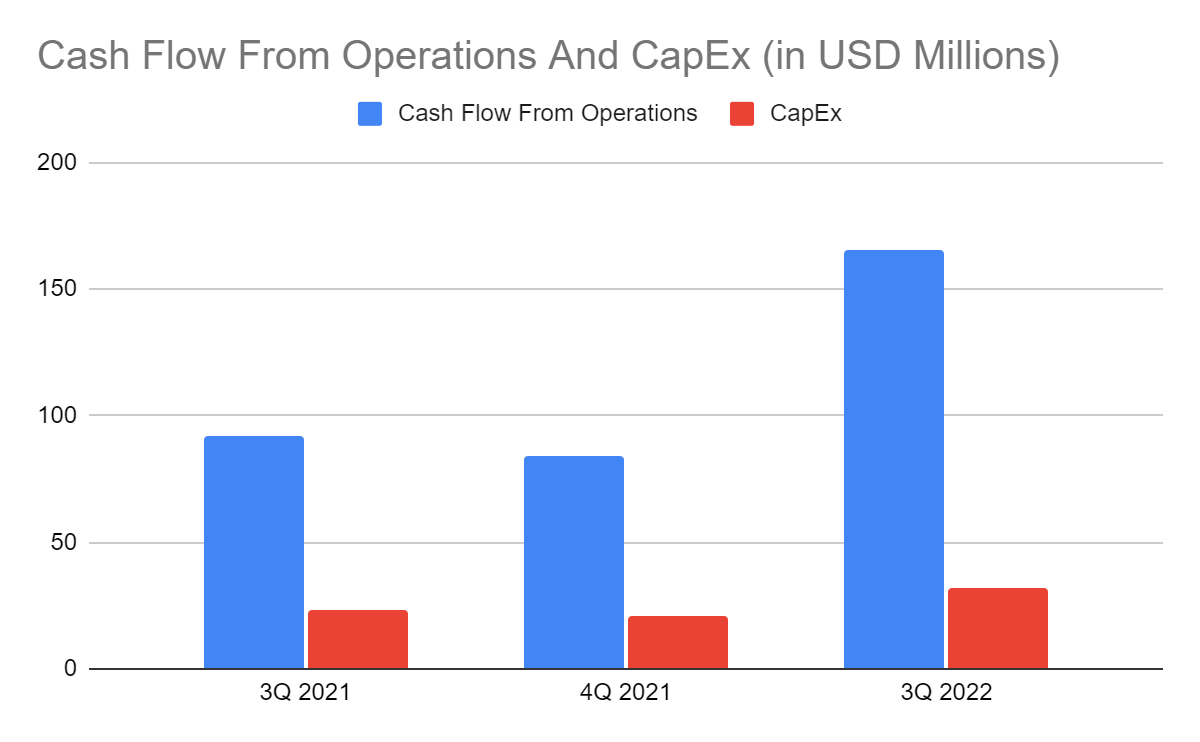

Currently, what’s certain is that ArcBest remains well-positioned against market disruptions. It demonstrates fundamental stability and high liquidity to sustain its operating capacity. Cash reserves are adequate, given their substantial increase. Borrowings also show a massive increase, which can be attributed to the increase in LTL and equipment. Although it is already higher than cash, liquidity remains high. The Net Debt/EBITDA Ratio of 0.34x shows that ArcBest earns enough to cover borrowings. Even better, adequate cash levels can be proven by the increased cash inflows from operations. As such, it can cover CapEx and borrowing repayments. Its FCF/Sales Ratio of 10% shows that ARCB uses its revenues in what matters. It has an impressive capacity to turn revenues into cash.

Cash And Cash Equivalents And Borrowings (MarketWatch) Cash Flow From Operations And CapEx (MarketWatch)

Stock Price Assessment

The stock price of ArcBest Corporation has been in a series of sharp uptrends and nosedives. But the downtrend has been more noticeable. At $76.29, the stock price is 17% lower than its value last year. The price-earnings multiple of 6.03x agrees with the reasonability of the stock price. My estimated EPS of $13.43 shows a target price of $80.98. Meanwhile, the estimated EPS of NASDAQ of $13.83 has a value of $83.39. With that, there may be a 5-8% stock price upside.

-

FCFF $98,000,000

-

Cash $303,000,000

-

Borrowings $424,000,000

-

Perpetual Growth Rate 4.8%

-

WACC 9.2%

-

Common Shares Outstanding 24,417,880

-

Stock Price $76.29

-

Derived Value $79.03

The derived value agrees with our supposition of potential undervaluation, but the derived value is lower. There may be an upside of 4% in the next 12-18 months. Investors may consider this price for a buy position.

Bottomline

ArcBest Corporation proves its solid capacity to stabilize growth and margins. Projections this year may be bleak, but the company is well-positioned against disruptions. It remains liquid, allowing it to maintain its operating capacity and cover borrowings and dividends. Also, the stock price stays undervalued, although the current price is near the target value. The recommendation is that ArcBest Corporation is a buy.

Be the first to comment