diego_cervo/iStock via Getty Images

BTI logo (British American Tobacco)

Investment thesis

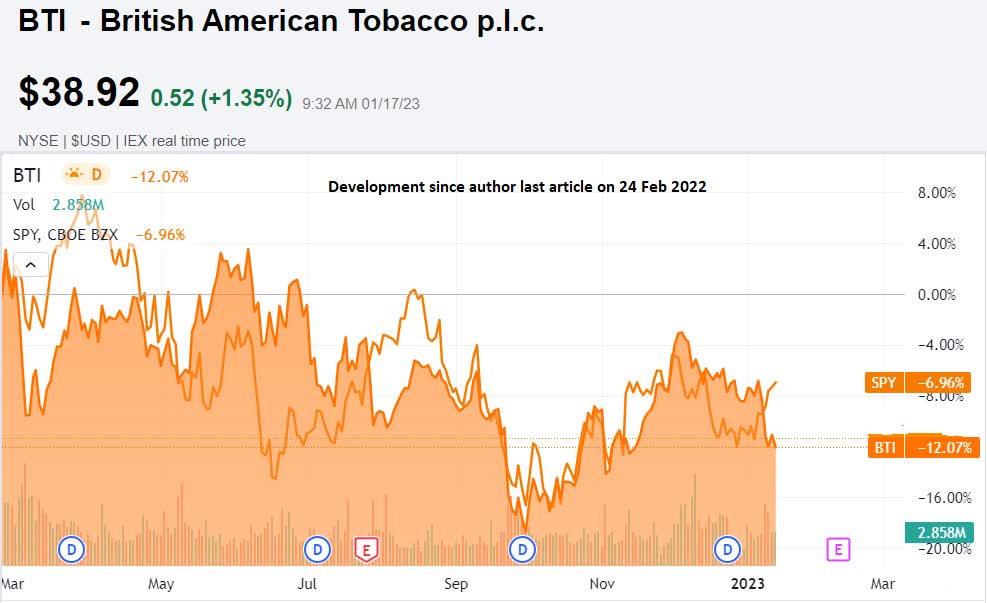

It is almost a year since we last covered British American Tobacco (NYSE:BTI) here in SA. At that time, we gave it a Buy stance. The share price is down 12.4% since that time. This surprised us somewhat, as throughout 2022 it felt like it held up well as we watched the general market fall. After all, people don’t stop smoking.

BTI share price since 24 February 2022 (SA)

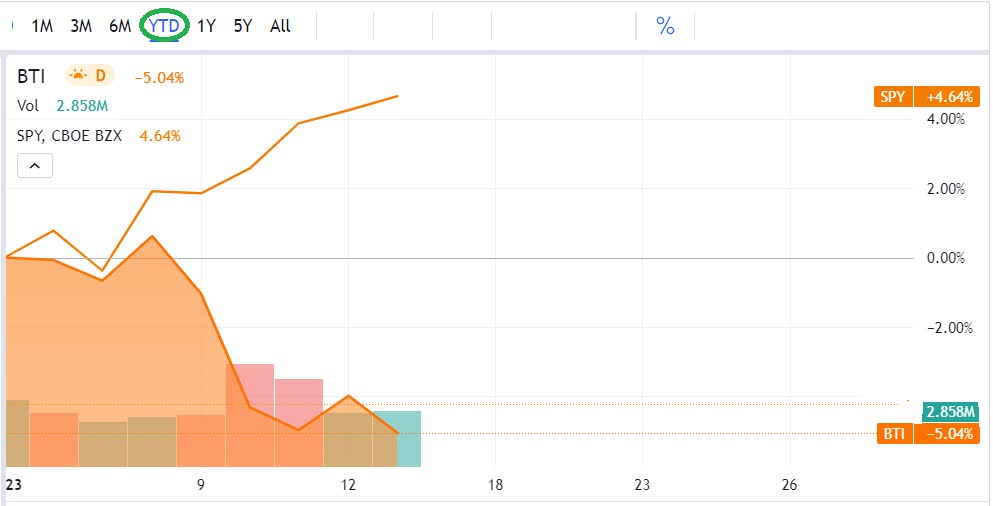

It is during the few trading days of 2023 that we have seen BTI go in the opposite direction to the S&P 500.

BTI share price development YTD (SA)

Perhaps investors interested in BTI are reevaluating the risks of owning it.

Let us talk numbers

When FY 2021 came out, management guided for an increase to EPS of high single-digit for 2022.

When they came out with their FH 2022, their revenue was up 5.7% and the profit from operation came in at GBP 5.65 billion, which was 7.8% higher than the year before.

Diluted EPS was 167.4 pence.

On the 8th of December last year, BTI came out with an update on their operation. From this, we learned that they expected the EPS for 2022 FY to increase by roughly 5% from the year before.

New Category products continue to deliver growth in volume, revenue, and market share. Although it was not profitable in the past, this is changing and management said that it is now becoming a significant contributor to their performance.

In the first nine months of 2022, the new category segment delivered another 3.2 million new consumers.

With GBP 44.88 billion in debt, we should be concerned about the speed and significance of global interest rate rises. Hopefully, BTI will not be hit too hard by higher interest costs as they have a 90% fixed debt profile with an average maturity of over 10 years. The question is for how long the rates will stay elevated.

BTI will release their 2022 FY preliminary and unaudited results on the 9th of February 2023. Mark your calendar.

Returning capital to shareholders

When BTI announced their FY 2021 back in February of 2022, they communicated that their intention was to buy back shares of GBP2 billion in the calendar year of 2022.

They managed to achieve this on 15 December 2022, as they then had repurchased 59.54 million ordinary shares in 2022 at a volume-weighted average price of GBP 33.59 per ordinary share for a total consideration of GBP 2 billion.

These shares are not canceled but kept in treasury. As of 15th December, they held 221 million shares in Treasury. BTI has a total of 2,235,865,536 ordinary shares issued.

In terms of the dividend, we believe the dividend will be increased by 5%. The present TTM dividend is GBP 2.18. Therefore, if they go with a 5% increase the coming year should pay a total dividend of GBP 2.29

If they continue their dividend policy from the past, they will in February declare dividends which will be payable in four equal quarterly installments in May, August, November, and February the following year.

Are the risks going away?

Most of our fellow authors will show you beautiful slides taken from BTI on how good the growth is in the new product segments, which are mainly heated tobacco products and E-cigarettes.

Few articles discuss how BTI is going to transform and what it might mean for its profitability.

Could a global reduction of the traditional cigarette market and an increase in countries banning vaping and E-cigarette mean lower profits in the future?

Since then, World Health Organization came out with a fact sheet in May 2022. It is not pleasant reading. We urge you to read it for yourself and make your own judgment.

In November last year, South China Morning Post reported that Hong Kong’s Secretary for Health Lo Chung-mau confirmed that banning tobacco sales for future generations will be on the table in a government bid to further reduce youth smoking. They are considering a lifetime ban on anyone born in or after 2009 buying smoking products. He stated:

We should not let our guard down despite Hong Kong having one of the world’s lowest smoking rates. Let our new generations no longer be tempted and harmed by tobacco products. Gradually raising the legal age for buying tobacco products and making the next generation not able to buy tobacco products legally forever are among the options.”

The country’s parliament voted through the first draft of a bill in July 2022 that will make it illegal for people born in 2009 or after to buy tobacco. The legislation will also restrict the sale of tobacco to specialized stores with products no longer available in local shops or supermarkets. However, vaping remains untouched in the bill.

Stepping up tobacco control was also mentioned by Hong Kong’s new Chief Executive John Lee Ka-chiu during his maiden policy address in October 2022. A target has been set to reduce the smoking rate to 7.8% by 2025. In 2021, the rate was 9.5%

In 1982, when the Smoking (Public Health) Ordinance came into effect, smoking prevalence was as high as 23%.

Over in the U.S., which is a much larger market, the U.S. Food and Drug Administration has estimated that more than 2.5 million school students there use e-cigarettes, a statistic that the regulator said had left them “deeply concerned“.

What will come out of their “deep concern” is hard to tell.

Nevertheless, simply ignoring this threat does not seem to be a good strategy.

BTI’s official policy is that they want to reduce the harm. Here is what they state on their website:

We know tobacco products pose real and serious health risks and the only way to avoid these risks is not to use them. But many adults choose to smoke, so our top priority continues to be working towards reducing these risks and making available a range of less risky tobacco and nicotine-based alternatives.”

The question is whether health organizations in various countries will follow New Zealand and possibly Hong Kong, or choose to ignore the danger associated with smoking. We know that every country is struggling to try to mitigate the costs associated with health care.

If you do have a problem falling asleep one night, you might want to read BTI’s 2021 Annual Report on Form 20-F. It contains 27 full pages of present litigations concerning tobacco and other contingent liabilities.

Conclusion

In our last article, we concluded that although BTI is highly profitable and rewards its shareholders well, we needed to stay focused on the risk associated with tobacco.

Our hope was for the company to push ahead with the development of non-tobacco and non-harmful products. Not less harmful.

Here is what we said in February last year:

BTI is a buy at the present level. Having said that, I will monitor their transformation going forward to see how fast and how transformative their moves will be. The reason is that I do think it is probably more important than many investors think it is.”

There is no doubt that they are profitable and do have a generous return of capital to shareholders.

However, we are not convinced that their transformation is transformative enough.

As such, we prefer to reduce our Buy stance to that of a Hold.

Be the first to comment