oatawa/iStock via Getty Images

Investment Thesis

AppLovin (NASDAQ:APP) positively surprised investors with its alluring guidance for Q1. As we dig through, there are some negative and positive elements that investors should be mindful about.

On balance, there are more positives than negatives and I’m inclined to be bullish on AppLovin at a $5 billion market cap.

Navigating This Challenging Environment

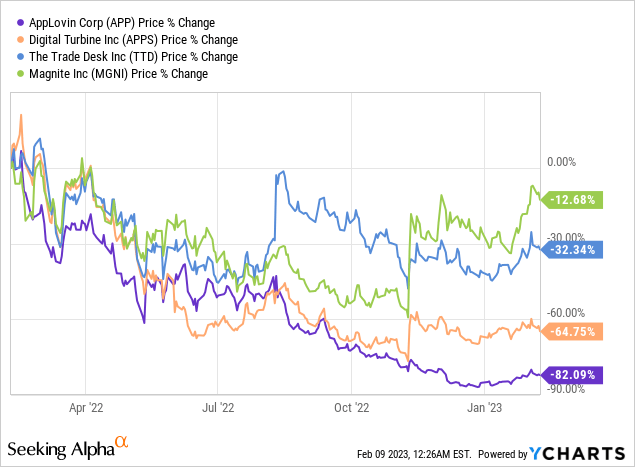

AppLovin has seen its stock get crushed in the past year. It’s not only down, but it’s down significantly more than a randomly selected group of peers. Put simply, expectations were incredibly low for AppLovin as it headed for this quarterly report.

Recall, AppLovin has two segments:

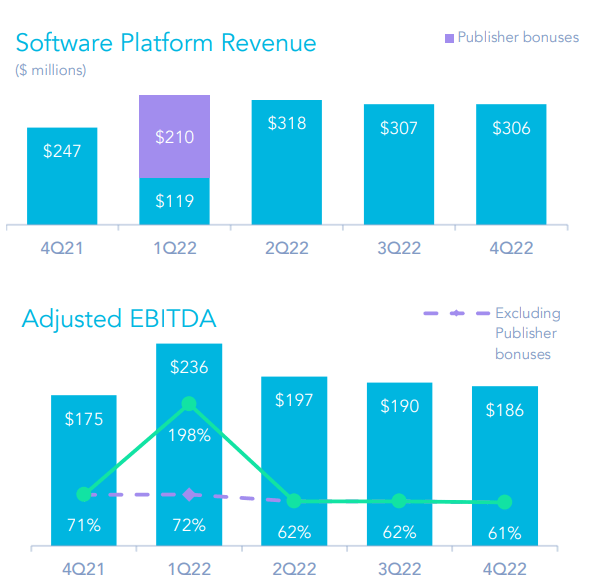

APP segment Q4 2022

AppLovin’s Software Platform is the crown jewel within its business. It’s not only growing significantly faster than its Apps Segment, with the Software Segment increasing 24% y/y compared with a decline of 28% for its Apps segment.

But also, the Software Platform has impressive EBITDA margins.

APP Q4 2022

As you can see here, even now, the Software segment reports more than 60% EBITDA margins.

I suspect that either this quarter or the next, its Software Segment will be the bigger unit within AppLovin. And given that its growing faster than the underlying business, this could see AppLovin’s overall growth rates picking up momentum.

And this leads me to discuss AppLovin’s financials.

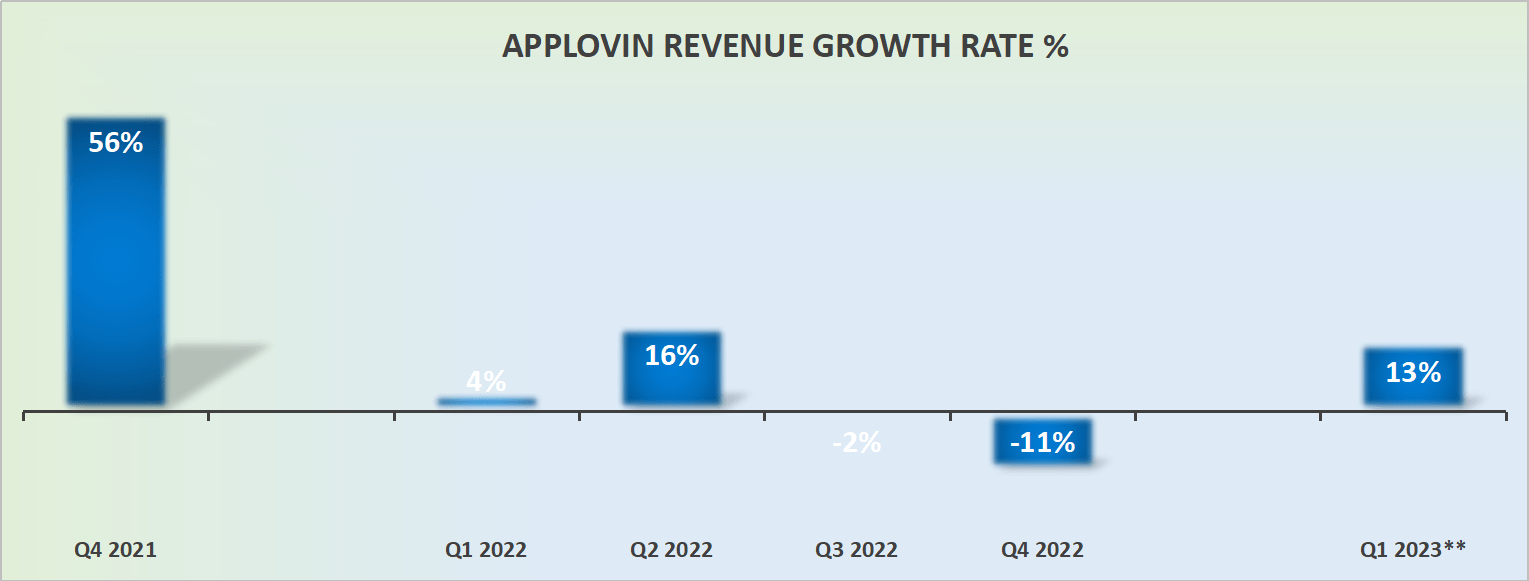

Revenue Growth Rates Reaccelerate

AAP revenue growth rates

AppLovin has seen its revenue growth rates trend lower for several quarters, ultimately reporting double-digit negative growth rates.

Looking ahead, given that many advertising companies are struggling to guide for anything higher than 10% topline growth, AppLovin’s guidance certainly is attractive.

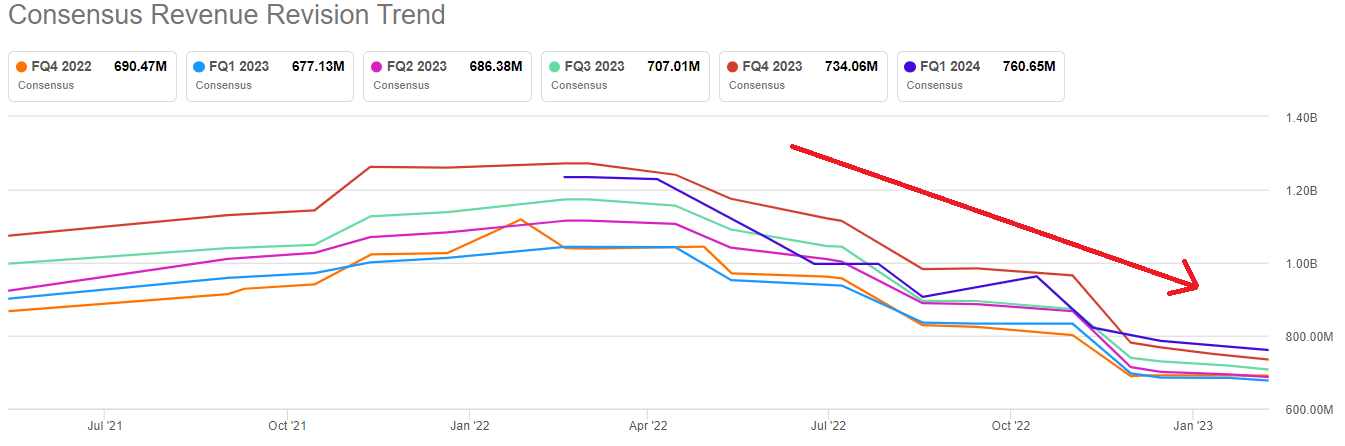

SA premium

Particularly given how negative analysts have been towards AppLovin.

Companies Focus on Executive Compensation

The reverberation coming out of this earnings season is how do companies retain executive talent?

Previously, when share prices were substantially higher, you could just pay them with SBC and everyone was happy. Executives were happy that their SBC was becoming worth more and shareholders didn’t mind because share prices only went up.

Now, companies have to provide much more SBC to incentivize management to stay. Case in point, in 2022, AppLovin saw its SBC rise 44%, even as its revenue growth for the year was flat.

Next, even though AppLovin has a considerable amount of adjustments to its adjusted EBITDA line, for instance, $100 million set aside as a loss for dispositions, the business as a whole is reasonably free cash flow positive.

More specifically, even though its Q4 GAAP net income was negative $80 million, as the business recognized several impairment charges, loss on debt, and management’s SBC, the fact remains that Q4 2022 saw AppLovin report $132 million of free cash flow.

Indeed, AppLovin’s free cash flow in 2022 is slightly over $350 million, a figure that’s very consistent with the prior year.

Of course, we must keep in mind that AppLovin acquired the widely reported MoPub from Twitter for $1 billion as well as the less reported Wurl for just under $400 million. Essentially, yes, the business makes strong free cash flows, but those cash flows are being supplemented through large and expensive acquisitions.

With this consideration in mind, let’s now turn to discuss its valuation.

APP Stock Valuation – 14x Trailing Free Cash Flow

AppLovin’s problems do not stem from an inability to report strong free cash flows. On the contrary, this is a business that throughout this most challenging environment manages to report $350 million of free cash flow (with SBC added back), clearly it’s doing many of the right moves.

The problem for AppLovin is that the business has had to lean meaningfully on an M&A strategy to grow these cash flows.

Now that AppLovin’s balance sheet carries a net debt position of $2 billion, and its share price isn’t worth all that much, I have to wonder whether that particular avenue may have closed.

The Bottom Line

I believe that it’s not an exaggeration AppLovin stock has been a disaster investment this past year. I find it difficult to imagine that at one point this stock was priced at more than $110 per share and that within 12 months it ended up trading for sub $10 per share.

On the other hand, keep in mind that AppLovin has made several big acquisitions in the past year, and those acquisitions appear from the outside to have provided no growth at all to the business.

But yet again, with the stock trading at approximately 14x free cash flows, I suspect that much negativity has already been priced in here.

Be the first to comment