Leonid Ikan

Canadian Natural Resources (NYSE:CNQ) is a very popular name in the Oil & Gas space. Especially amongst institutions. 70% of the float is currently owned by institutions while only 30% is owned by the general public. Part of this is due to the volume that trades in a given day, but the company has solid fundamentals and pays out a stable dividend which should be attractive to everyone. While you may not see much appreciation on the share price, I do fully expect to see new all-time highs in 2023 which would take us north of $70 per share.

What’s Driving CNQ?

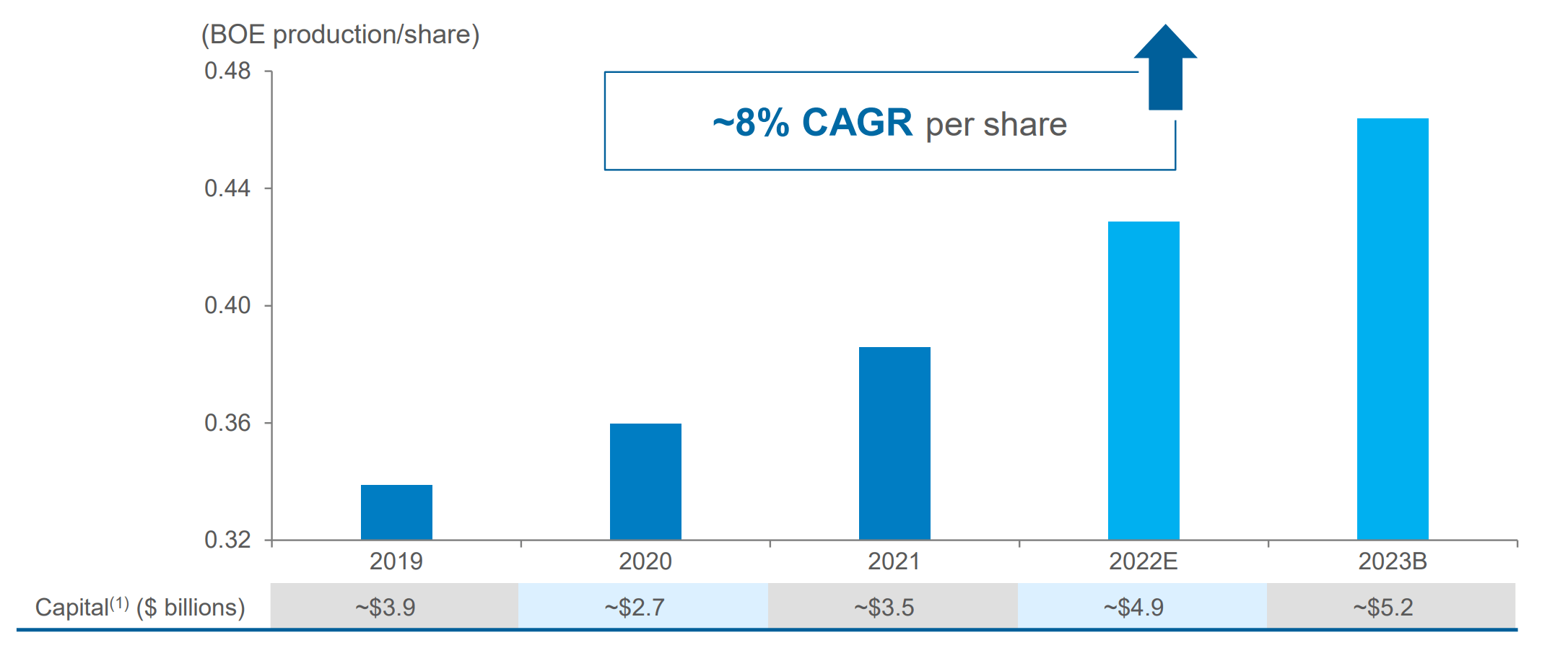

This will shock you, but it’s Cash Flow. (I really hope that didn’t shock you). The company has solid fundamentals and the price of oil over the last couple of years has really helped CNQ strengthen the balance sheet and set itself up for the long term. Besides that, the company is applying capital in the right places over the last few years. Looking below we can see the barrel per day growth since 2019, and it’s impressive when you think about what the world has gone through.

Canadian Natural Resources

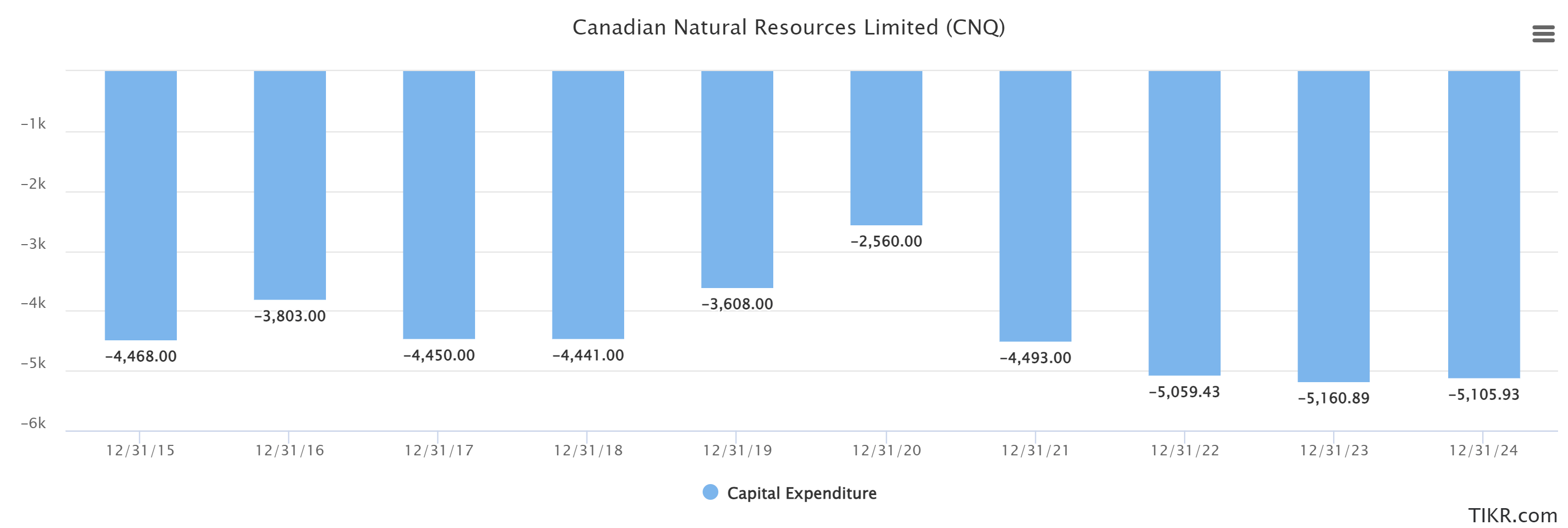

The best part of this is that they didn’t have to go crazy with CapEx to do it. We can see that they made massive cuts to CapEx in 2019 and 2020, and it has rebounded to levels similar to what we were seeing before the big oil collapse. It’s not like they have started throwing cash out the window to grow production which is great news. One thing to keep an eye on here would be a sudden surge in CapEx but based on what I can tell I don’t expect this to happen anytime soon given how well things have been going over the last couple of years.

TIKR.com

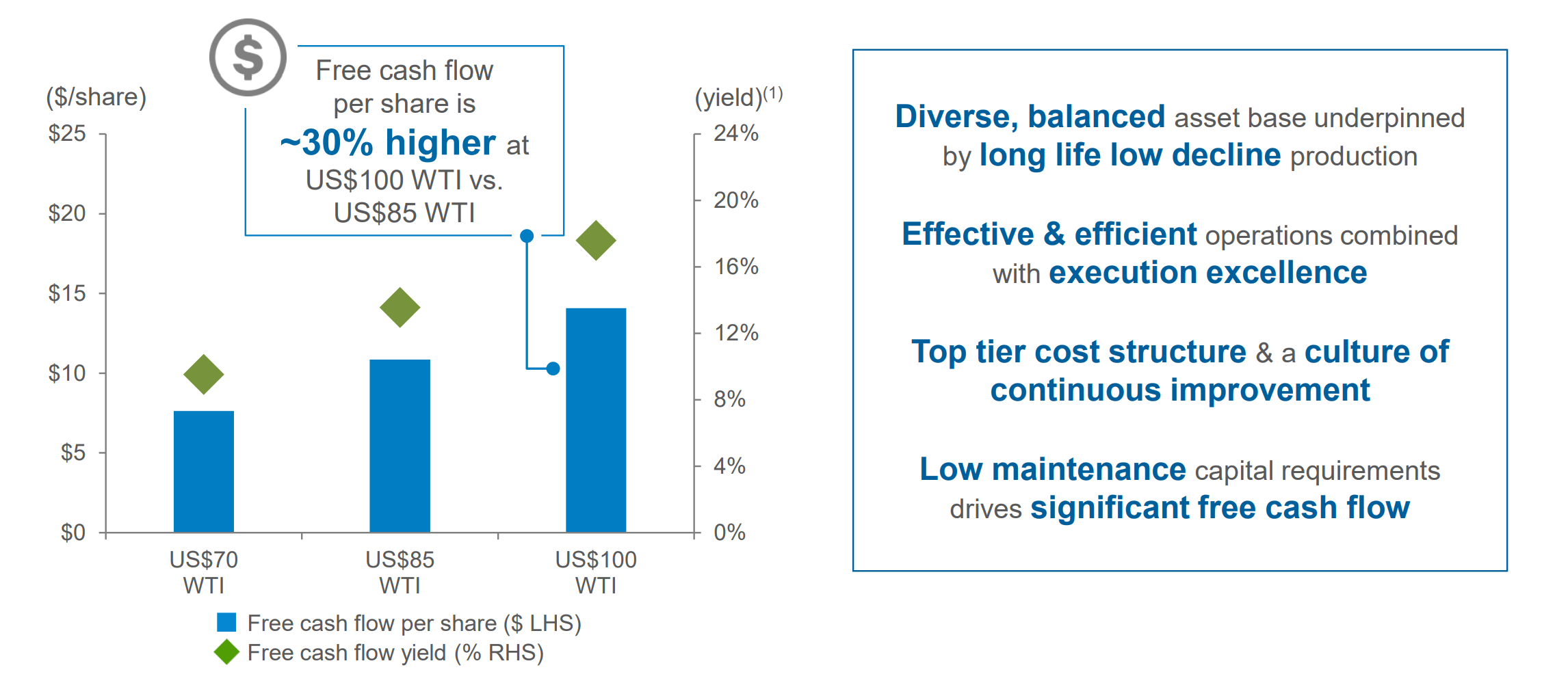

All of this, plus a bull market in Oil & Gas leads to the image below, which is Free Cash Flow. As you can see, the price of oil drastically impacts what we can expect to see from CNQ. This is good because I do believe the price of oil will remain elevated and this will only increase shareholder returns. The company doesn’t have to do anything but maintain production to capitalize on the price inflation. Mix that with growing production and it’s raining dollar bills at CNQ headquarters.

Canadian Natural Resources

Essentially, what I am saying is that CNQ has put itself in a position for long-term success regardless of the price of oil. They have slashed debt and built a sustainable business that can be maintained so long as we don’t see a big oil crash.

How’s the Dividend?

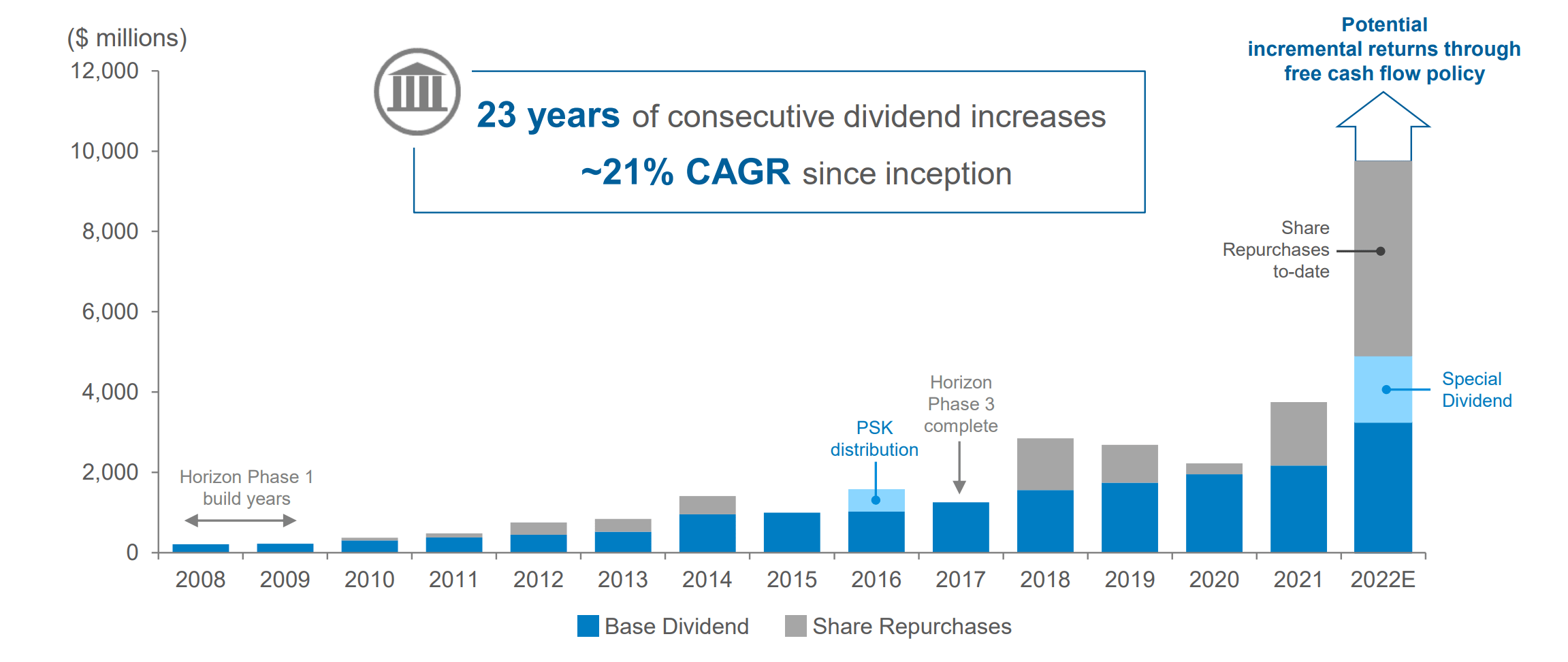

One of the big attractions of CNQ is the dividend. The company will do whatever it has to in order to avoid a cut. They have increased for the 23rd consecutive year. Which isn’t ideal when times are tough and the dividend should be sacrificed to maintain a clean balance sheet. But, when times are good, it’s great news for shareholders. This isn’t a stock that’s going to double in the next year. If you are looking for oil exposure and looking to get reliably paid to wait, CNQ is for you.

Looking below, you can see what I’m getting at. The company has made paying shareholders a priority. You can also see the large volume of share repurchases in the last two years and that is something I love to see as well. Well get the official 2022 year-end results in early March, but it’s looking like $4.33 per share will be paid out, which is good for a 7% yield on the year. Not bad!

Canadian Natural Resources

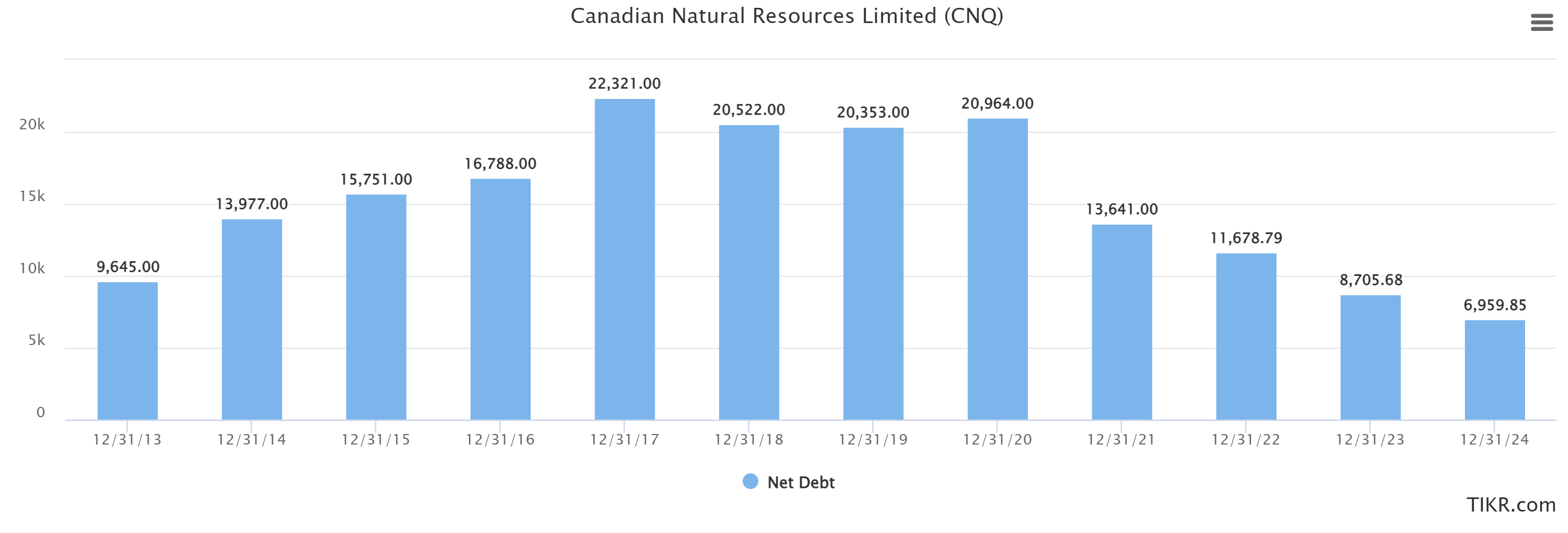

Is there more room for this to grow? Yes. Once Net Debt hits $8 billion, CNQ will allocate 80% to 100% of free cash flow as incremental returns to shareholders. Yes, you read that right, possibly 100%. The question is when. Looking below we can see analysts estimate that this will occur in 2024. I am bullish on the industry and I do think there is a chance we see this come through this year, but that really depends on what happens with the price of oil. Currently, the leverage ratio is sitting at 0.5x, which is good for a company in this industry of this size. There is no concern over the dividend at this time.

TIKR.com

CNQ is advertising a potential $16 per share dividend over 2022 and 2023 combined which would be incredible. So much of this is dependent on the price of oil over the next year, but knowing that’s even remotely possible is very encouraging for shareholders. There is nothing to worry about here so long as the price of oil remains stable. We are entering the seasonal period of strength for the industry as well. It’s been a good year to own CNQ.

What Does The Price Say?

If you are looking for crazy capital gains, this isn’t the stock for you. As mentioned, the sustainable dividend is the attractive piece here. There will not be near as much torque in a name like CNQ as there is in a Whitecap Resources (WCP.TO) for example. That said, there is still room to run here.

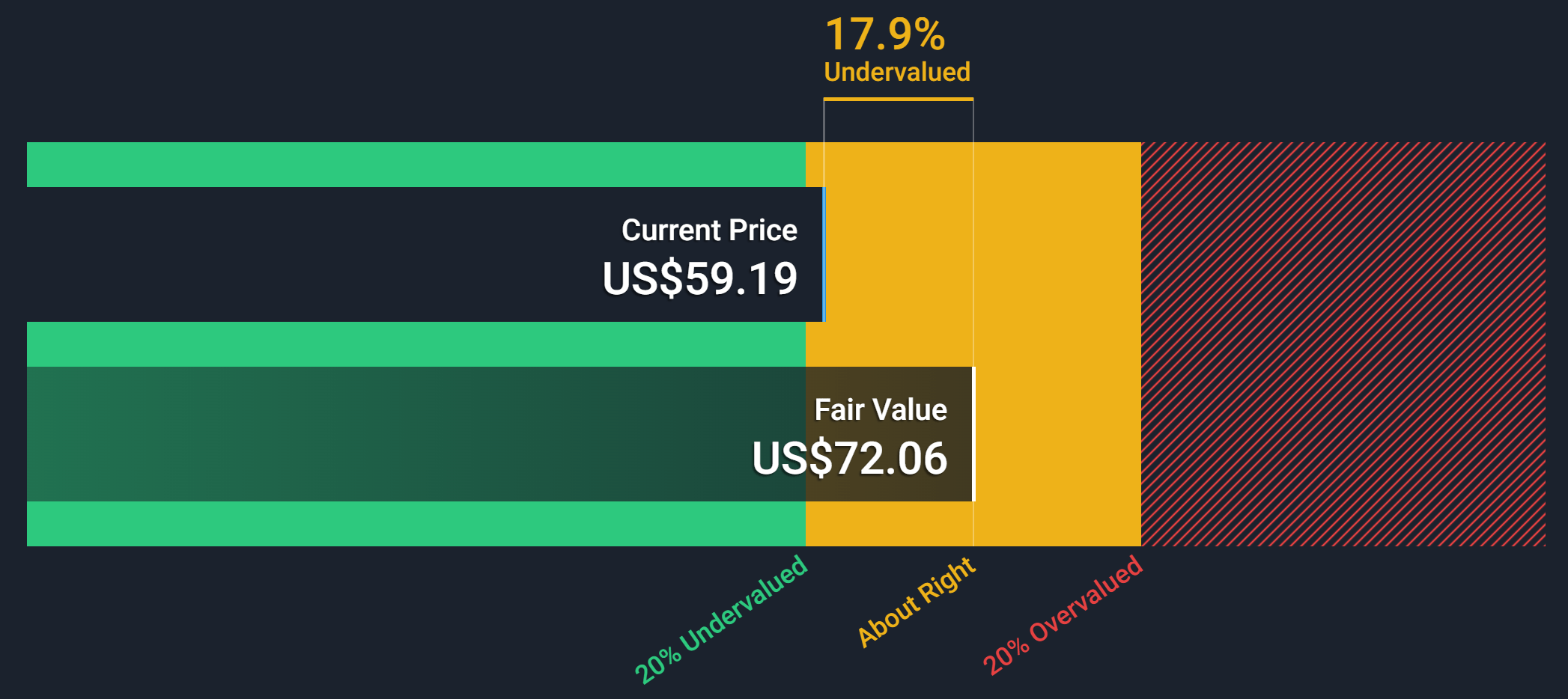

Looking below, we can see that the current price of $62.00 falls right into the “about right” part of the valuation chart. This chart is based on levered future cash flows. Does that mean that the stock isn’t going to improve? No. But it does mean that there likely isn’t as much room to run compared to other names. But that’s why it’s a large cap!

Simplywall.st

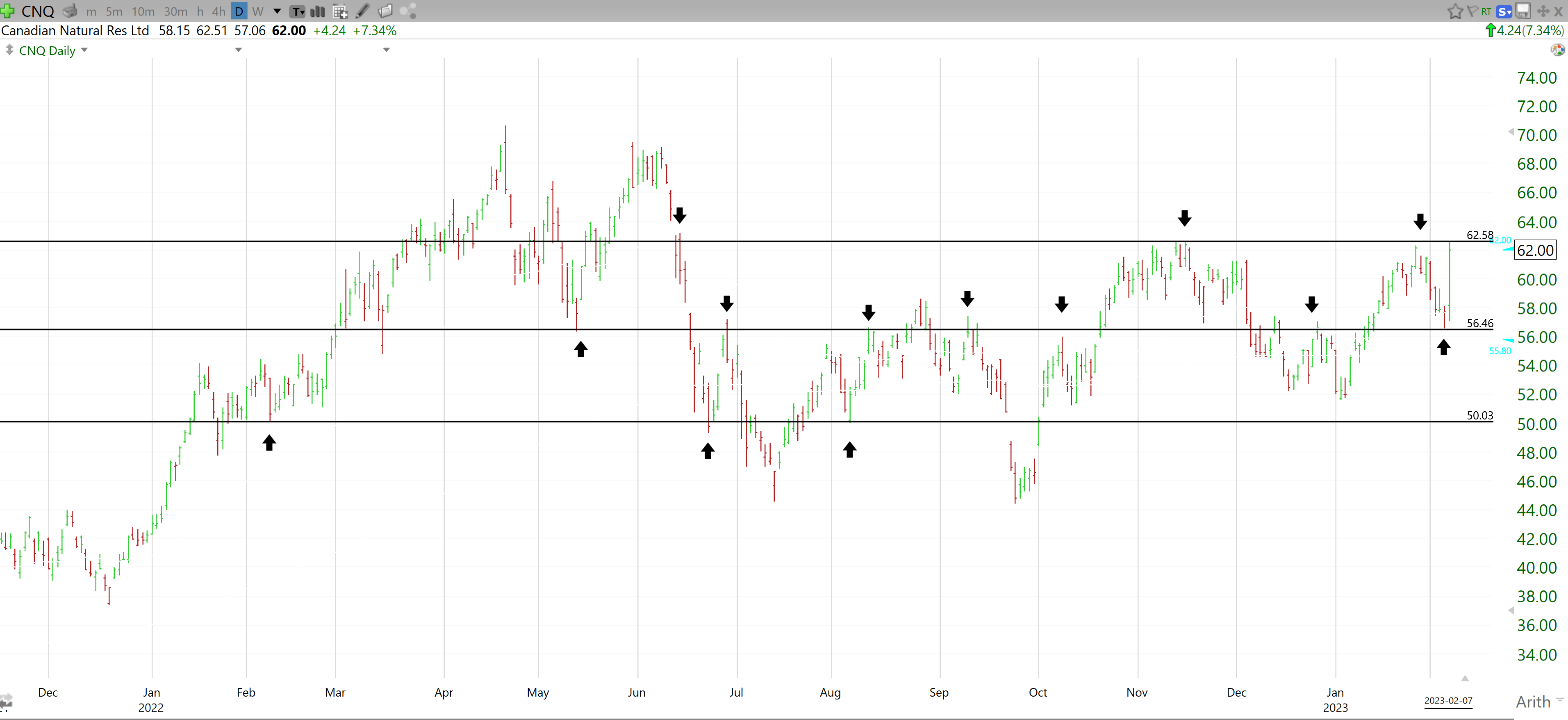

After the huge 7% day on Tuesday, the stock is quickly approaching the buy point with respect to a breakout move. Looking below, you can see three lines. The top line is where we are about to test previous highs. Right around $62.50 which is basically where the stock maxed out today. If we can see a good follow-through day, I would feel comfortable buying above this level as the $62.50 should then act as support. Obviously, this isn’t guaranteed, but it’s a nice thought.

TC2000.com

The next two lines are where you could place potential stops. Given the lower risk profile, a name like CNQ carries, I would look at a 50% stop and a 100% stop versus the all-out sell. The 50% stop would be at $56.46. Looking above, we can see that this has been a point of resistance and support recently, and was the most recent “bottom”. A break of this would be a bearish signal. Below that, you can see $50.00. I wouldn’t want anything to do with this stock below $50 for fear of what would happen next. It’s been a good point of support, but below it could quickly free-fall. I would be looking for a bounce and a higher high before jumping back in if we see the $50 mark.

TC2000.com

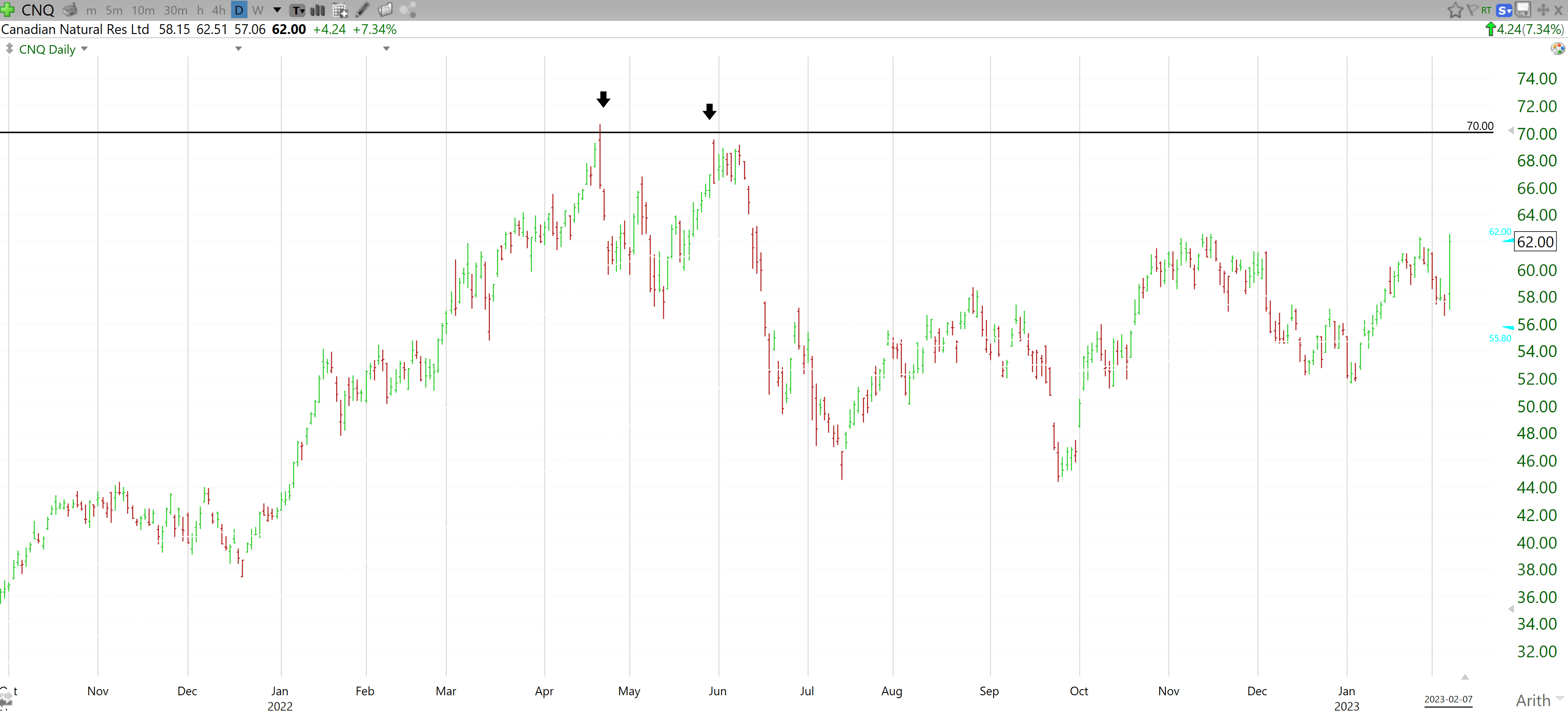

Finally, a price target. Because I am bullish on the sector, I am shooting for an all-time high test of $70. We saw this number get touched in the spring and summer of 2022, and I’d love to see it again this summer. This is only 12% above current levels though, so it’s not super ambitious. Which is one of the reasons I don’t own the name personally. The stock does chart well and trades strongly off of key support. Keep an eye on your levels and always set stops and you will be just fine in the long run with CNQ.

Wrap-Up

As you can see, CNQ seems like a no-brainer if you are looking for a safe place to park some cash and get Oil & Gas exposure. They are going to continue to reward shareholders and they are focused on reducing debt even further while growing production. If you are looking strictly for capital appreciation this might not be the name for you, but I would recommend it to someone looking to increase their oil exposure as we head into a season of strength. As always, set your stops and there won’t be anything to worry about in the long run.

Be the first to comment