imaginima

Antero Midstream (NYSE:AM) has finally headed towards the midstream “promised land” where free cash flow increases for the foreseeable future. An acquisition of some assets from Crestwood Equity Partners (CEQP) even brightened the free cash flow outlook. After markets doubts about the dividend that have lasted for more than a year, the market finally sees that the dividend will be maintained.

Next up will be the decrease of debt to management goals before there is any talk of a dividend increase. Still, the relaxation of worries about the dividend will likely lead to a higher stock price on average because the market will no longer worry about a dividend cut. That alone makes this issue enticing. There are likely to be further price increases as idle capacity fills up in the future to slowly increase earnings and cash flow.

Free Cash Flow Increase

Antero Midstream is one of the few companies that subtracts the whole capital budget in the calculation of free cash flow. Therefore, the acquisition that was made required no new cash from the company as the conservative financial strategy allowed for quite a bit of flexibility in paying for the acquisition.

As long as the acquisition earns a return greater than the interest rate, then the acquisition will be accretive. Management has felt that the potential savings plus established cash flow (and earnings) meant that the company paid 4.5 times adjusted EBITDA. That means it is a foregone conclusion that this acquisition will be accretive.

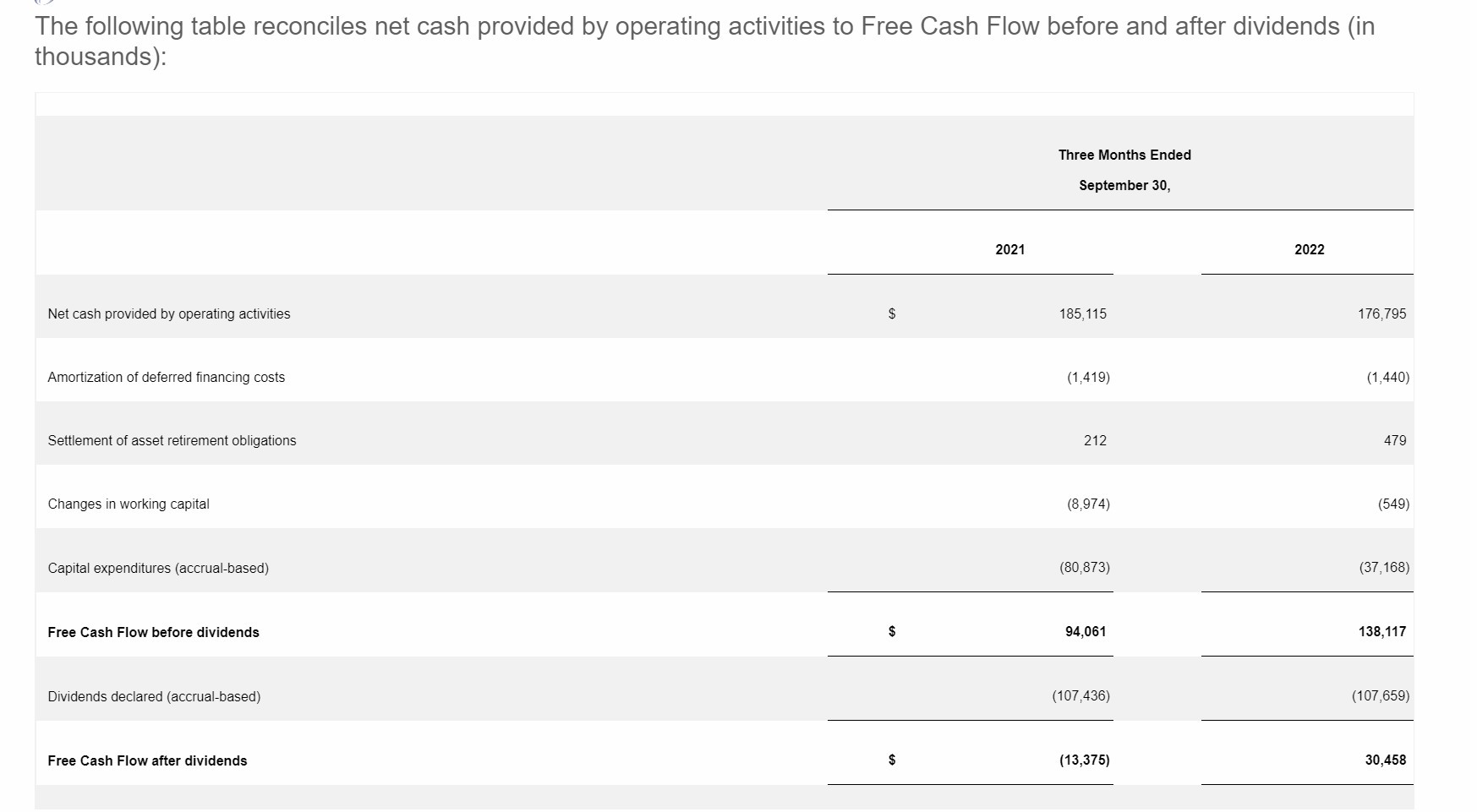

Antero Midstream Free Cash Flow Calculation (Antero Midstream Third Quarter 2022, Earnings Press Release)

Management had long forecast that the capital budget would decline enough to generate free cash flow after dividends were paid. Of course, Mr. Market had his doubts until of course it actually happened. So, the stock was caught in a trading range until the current report. This kind of cash flow progress is likely to be a stock price boost.

Not many companies disclose cash flow after the entire capital budget and dividend. It is far more likely for companies to use maintenance capital in the calculation than it is for them to put the entire capital budget as this company does. Most companies will finance at least part of the capital budget with debt. Mandatory capital expenditures for growth (for example) to prevent the loss of a customer or to keep up with changing industry conditions are rarely part of the free cash flow calculation. So, investors need to adjust free cash flow for comparability as well as to determine the real amount of free cash flow available.

Slow Growth Continues

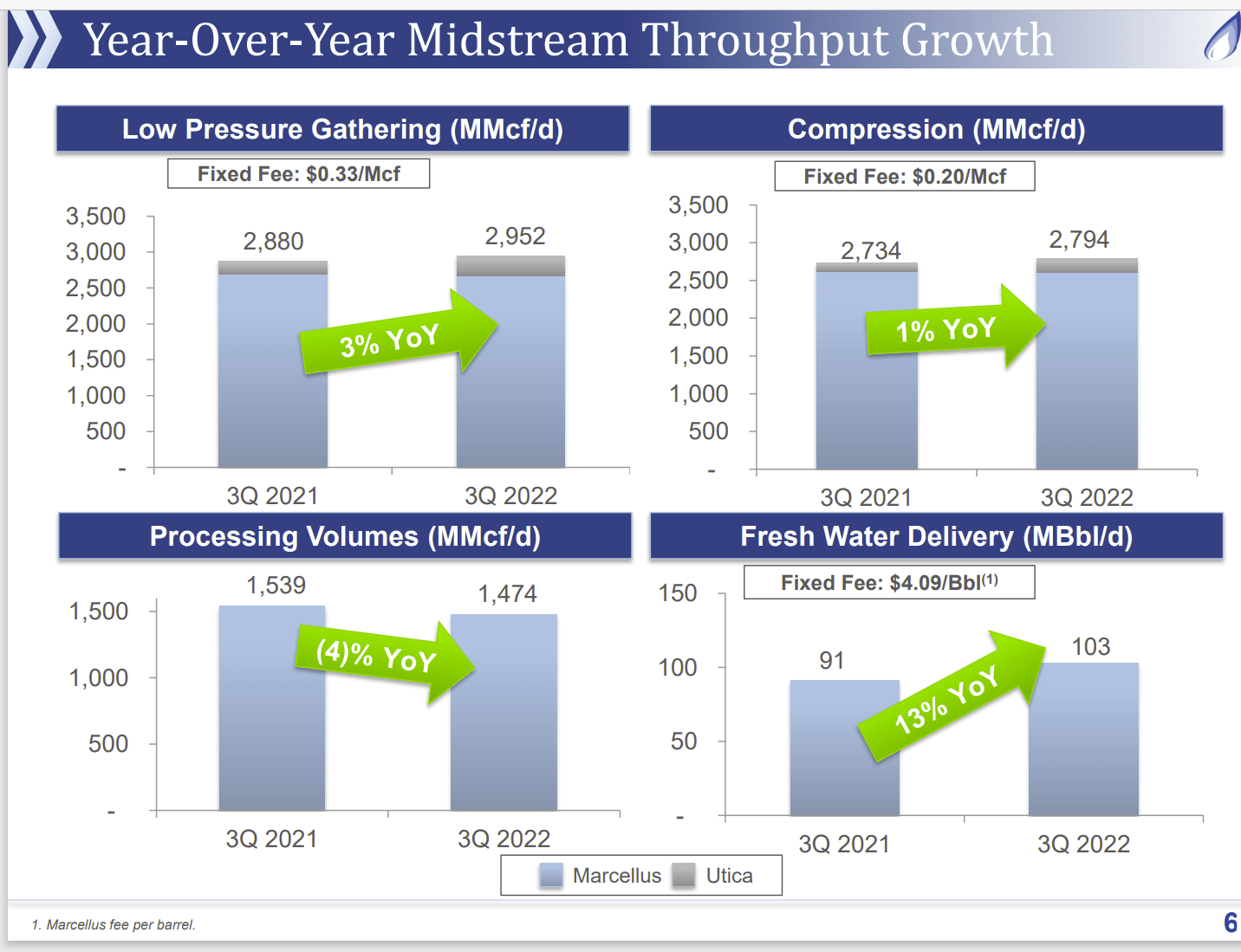

Management predicted that parent company Antero Resources (AR) would probably not grow the business. However, a joint venture was formed that will add some volume to the business of Antero Midstream. The result of this arrangement and current drilling priorities is slow overall growth of the Antero Midstream business as shown below:

Summary Of Key Antero Midstream Operating Statistics (Antero Midstream Third Quarter 2022, Earnings Conference Call Slides)

This slow growth is likely to continue. An occasional opportunistic acquisition like the most recent one should add a couple of percentage points to that slow growth. The very strong balance sheet of the midstream company minimizes the dilution possibilities for any small opportunistic acquisition.

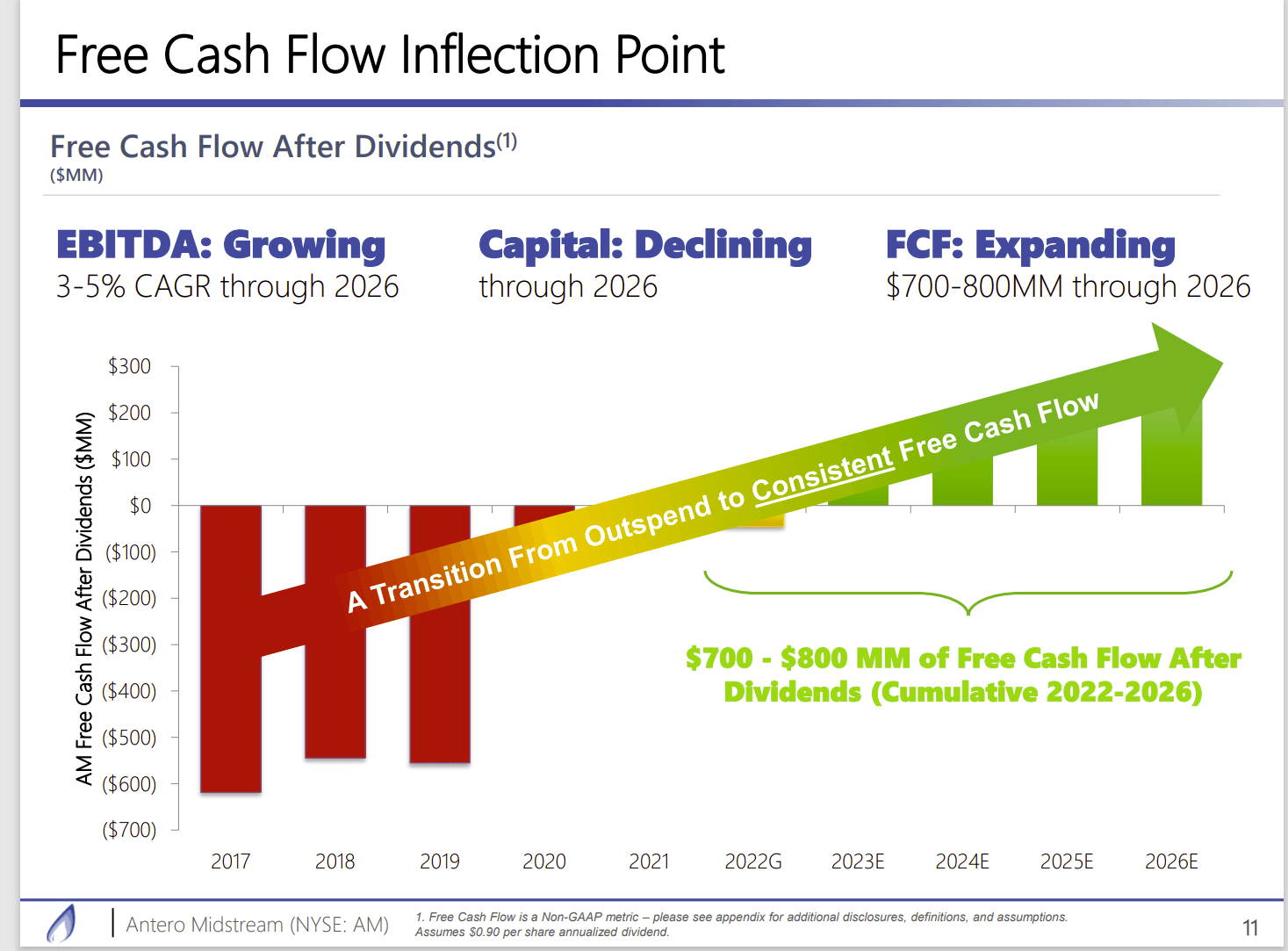

What this means is that free cash flow is likely to first be used to reduce debt to management’s original goal. After that, the free cash flow will likely be redirected towards share repurchases (when advantageous) and gradual dividend increases.

Antero Midstream Free Cash Flow Projection Schedule (Antero Midstream December 2022, Corporate Presentation)

One of the results of the acquisition is an increasingly bullish view of the free cash flow future. What could change this would be a material acquisition by Antero Resources that would demand a lot more supporting infrastructure or an indication of Antero Resources management that the company would return to a history of faster growth. Either decision would be bullish for the midstream business at the expense of either current dividends or future dividend increases (or both).

Unlike Antero Resources which has very volatile results as commodity prices fluctuate, this company has relatively steady returns from long-term contracts with take-or-pay provisions that provide a minimum amount of income. That makes future results very predictable as long as nothing catastrophic happens to the parent company.

Takeaways

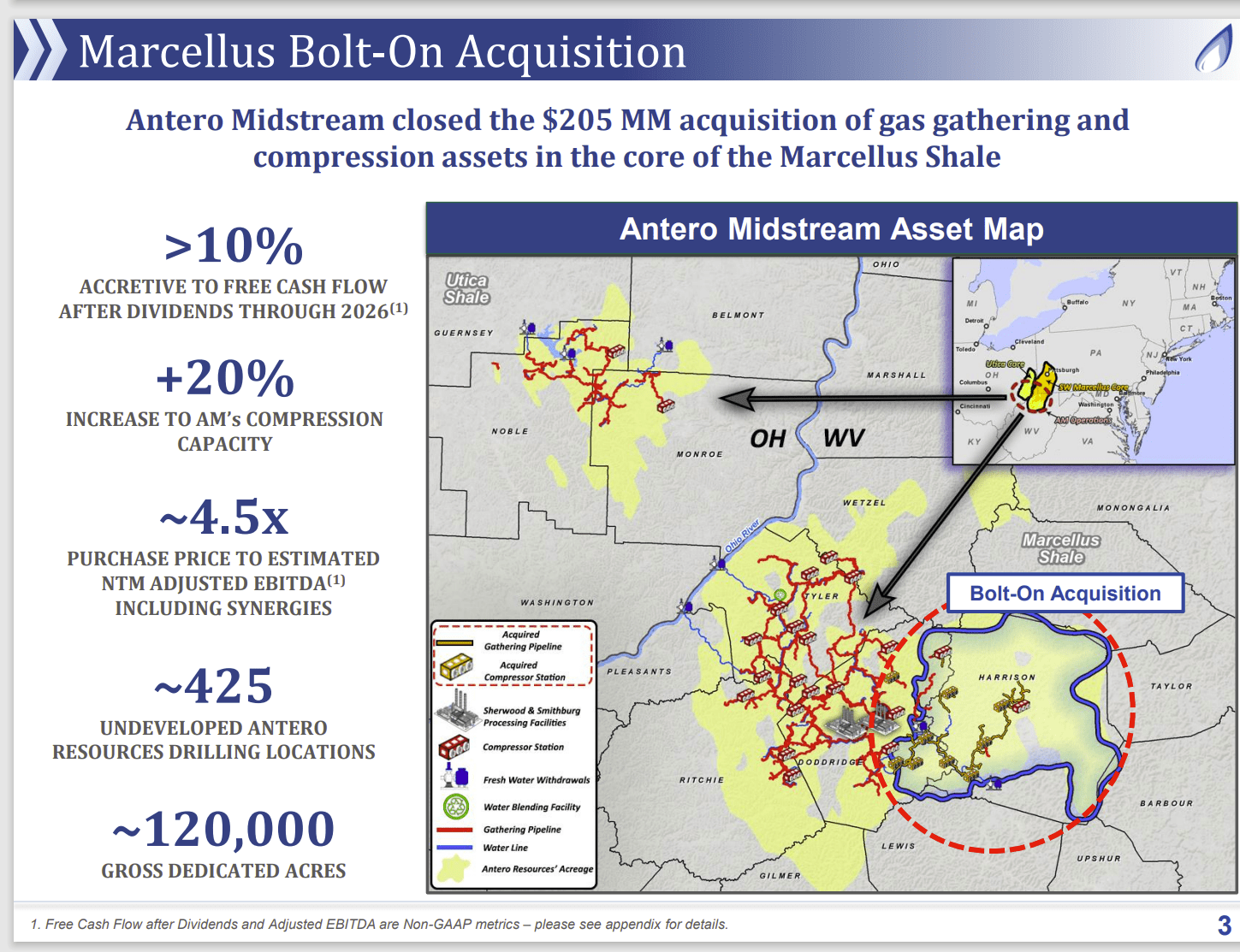

Antero Midstream will likely grow earnings in the single digit range for the foreseeable future. There will likely be an occasional boost to earnings from an opportunistic acquisition that would periodically (but irregularly) occur.

Antero Midstream Description Of Latest Acquisition (Antero Midstream Third Quarter 2022, Earnings Conference Call Slides)

The latest acquisition should boost earnings growth a couple of percentage points. The interesting thing was that management financed the acquisition with debt while keeping the debt ratio constant. That shows discipline when making the offer. It also means the strong balance sheet ratios will allow the company to continue to be opportunistic in the future.

Antero Midstream Advantages

Antero Midstream is the key part of Antero Resources superior marketing strategy in the Marcellus basin. Antero Resources has long gotten superior pricing due to the ability to ship production to strong pricing markets. The ability is largely unmatched in the Marcellus basin. This ability is likely to continue in the future.

But it is hard to understate the value of being able to flexibly send production to better pricing markets. Antero Midstream will likely have an advantage over other midstream companies in the basin for a very long time because midstream contracts are typically long term.

Financial Advantages

Captive Midstream companies with one major customer tend to be conservatively run. However, the financial strength of a midstream company with one major customer is usually capped by the strength of that customer. In this case Antero Resources is investment grade.

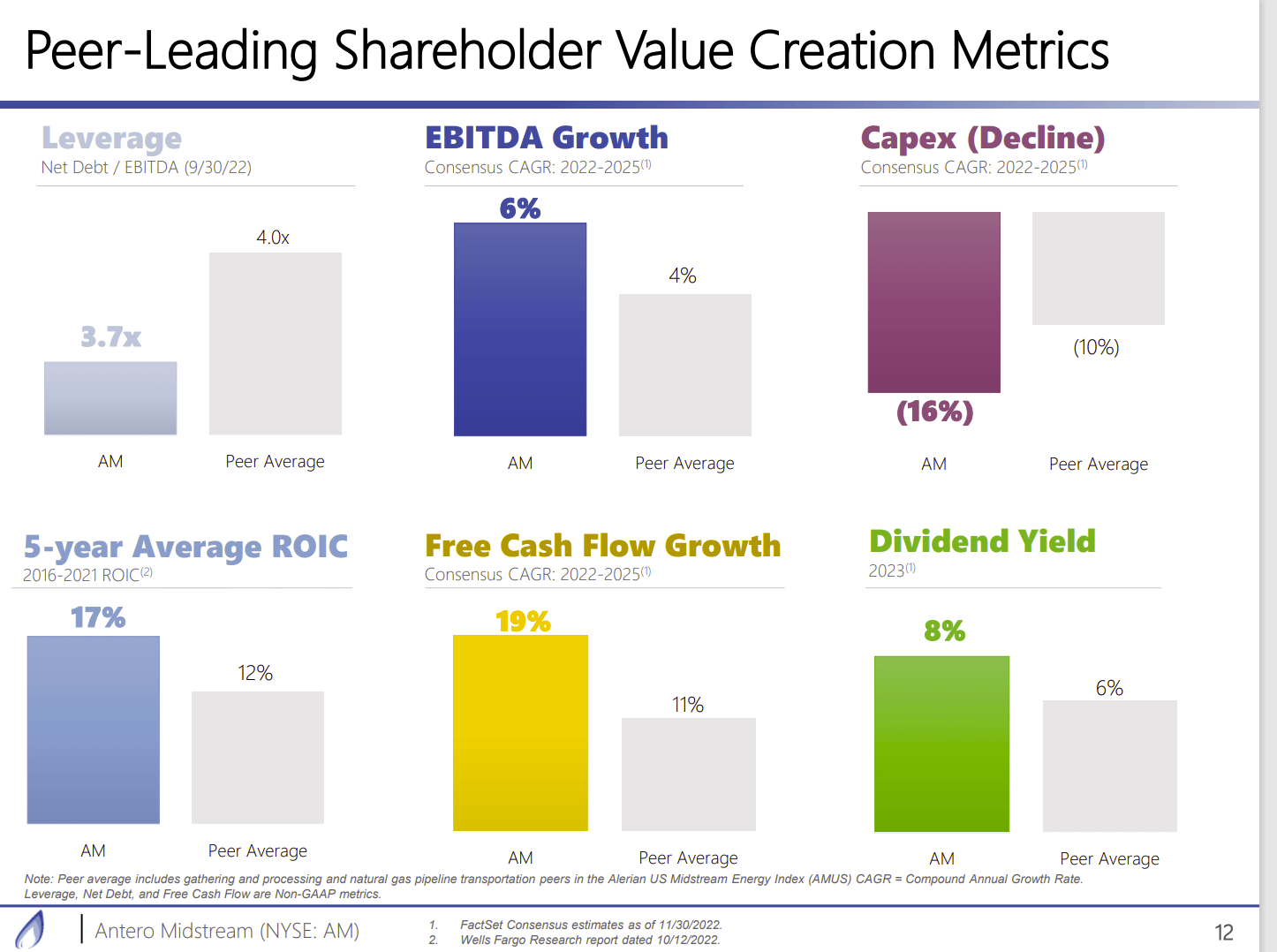

Antero Midstream Comparison Of Reported Ratios To Industry Averages (Antero Midstream Corporate Presentation December 2022)

Antero Midstream has some of the best ratios in the industry. The dividend is back by one of the lowest midstream debt ratios of midstream companies I follow. Therefore, management has a lot of flexibility with the dividend.

Free cash flow growth got a boost from the acquisition. So, the above average growth rate is likely to continue for some time. the high return on capital helps to keep cash requirements low for new projects. Investors can expect this well managed company to continue to outperform the industry.

The Future

The market really only values the ability of the company to pay a current dividend. But the profitability of the parent company opens up the future to considerable upside potential. Very profitable entities often become takeover candidates for the right price. The combined operations of Antero Resources and Antero Midstream are very profitable. That is exactly the kind of situation with the potential to surprise to the upside.

Mr. Market will not price in any upside potential until that upside become tangible. But that gives investors an advantage over Mr. Market because a basket of well-managed companies will likely outperform the industry to the benefit of the investor.

In this case, the investor already receives a dividend that is slightly in excess of the long-term average return reported by most investors. Any opportunistic acquisitions or even an eventual proposal to purchase the company are “icing on the cake”. This well managed company has a lot of attractions for a potential buyer. For a long-term buy and hold investor, this investment could prove to be a decent holding with above average returns.

Be the first to comment