Justin Sullivan

While NVIDIA (NVDA) has run into major problems with gaming revenues, Advanced Micro Devices (NASDAQ:AMD) has near immunity due to a focus on Data Center revenues and taking market share from Intel (INTC). NVIDIA just cut guidance again and might report a decline in sales while AMD is full speed ahead. My investment thesis remains ultra Bullish on the stock trading near the yearly lows due to weakness by sector players due to issues not impacting AMD.

NVIDIA Cut Numbers Again

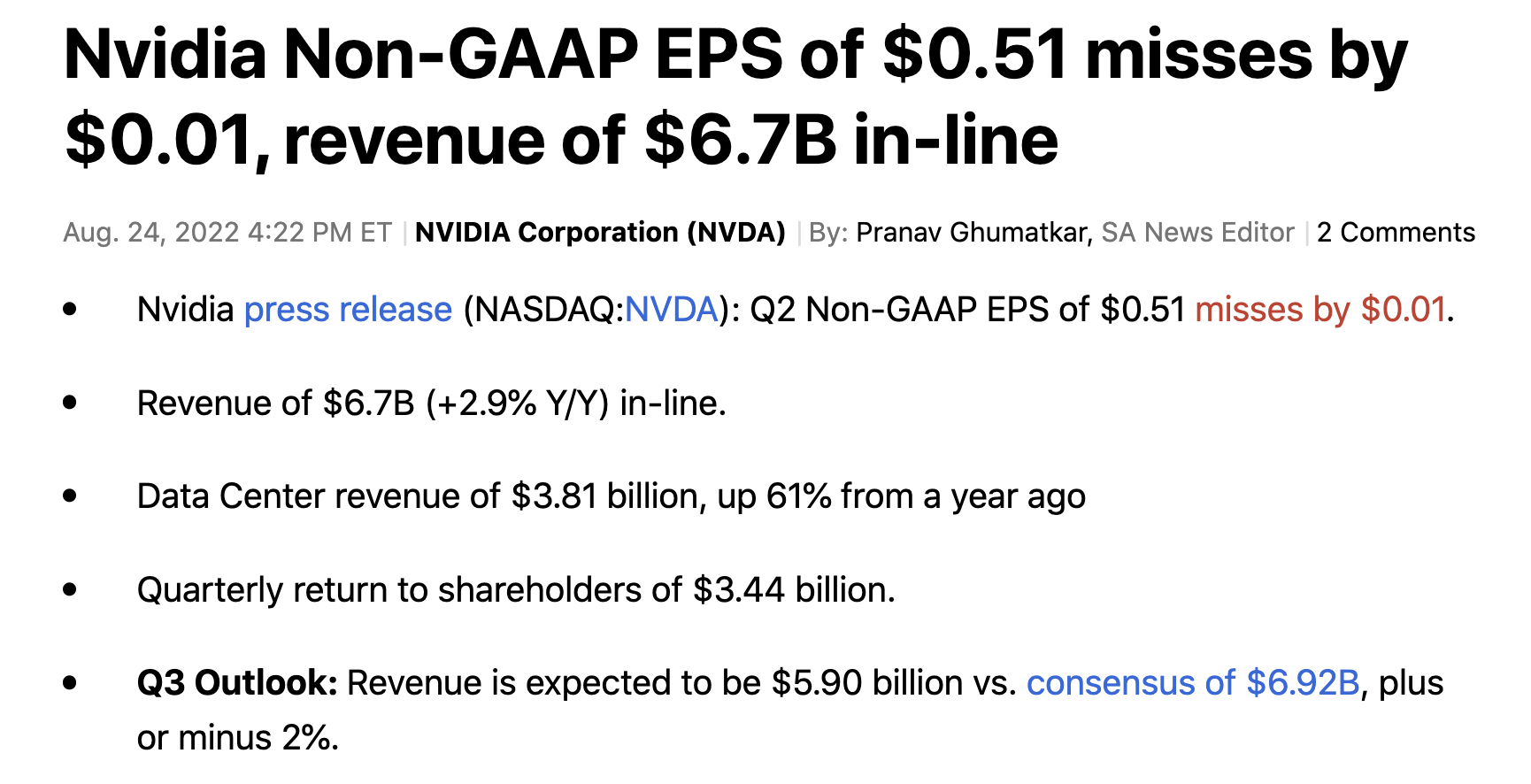

At one point, analysts expected NVIDIA to produce $8.1 billion in FQ2’23 revenues with an expected sequential boost in FQ3. Instead, the chip company only reported FQ2’23 revenues of $6.7 billion and guided to revenues of only $5.9 billion in FQ3.

Source: Seeking Alpha

The chip company reported Data Center revenues were still up 61% to reach $3.81 billion in the quarter. NVIDIA forecast Data Center and Automotive revenues to grow sequentially in a very positive sign for AMD’s Data Center focus.

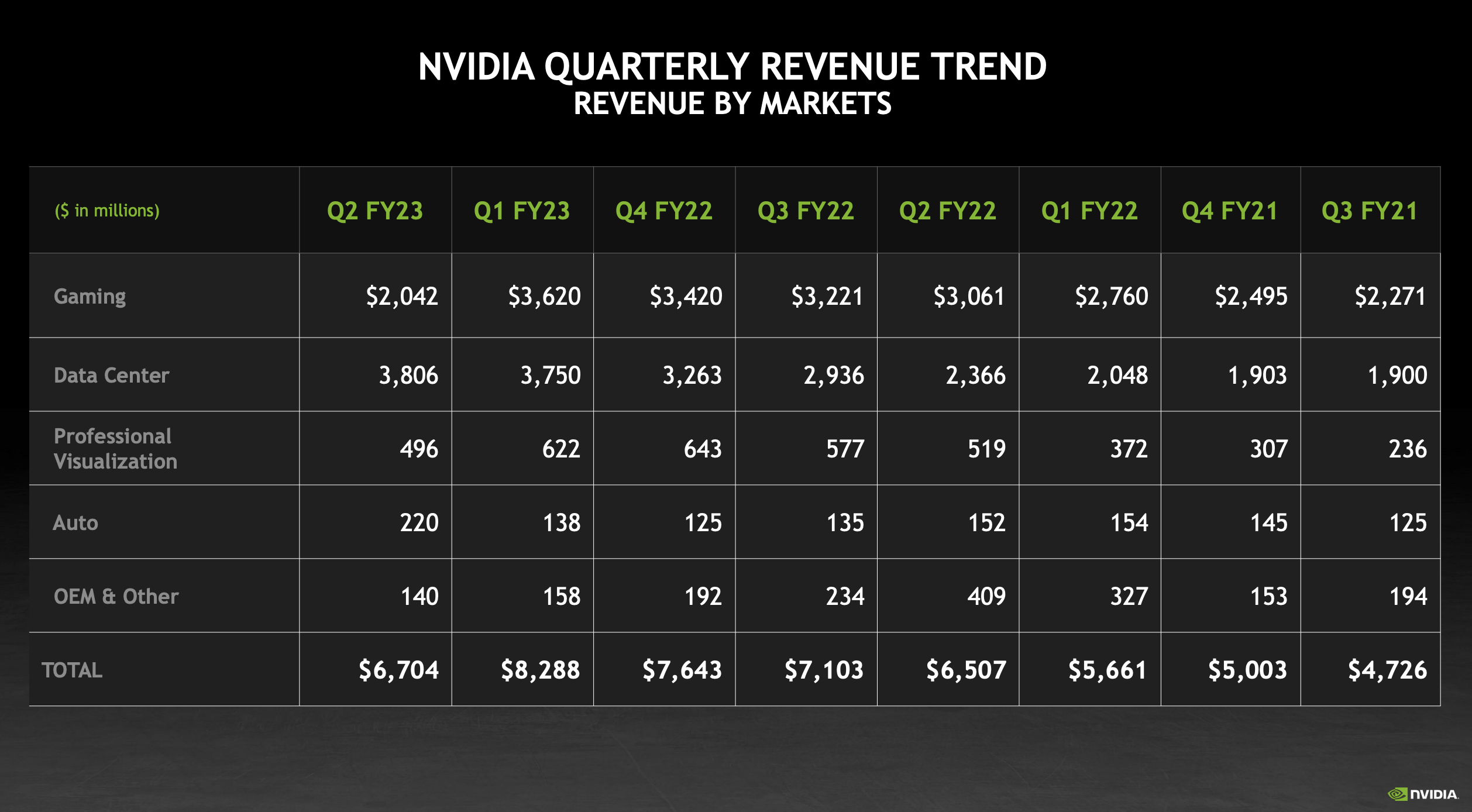

Source: NVIDIA FQ2’23 Revenue Trend

Remember, AMD saw Data Center revenues surge 83% to reach just $1.5 billion. The company continues to take significant market share from Intel in the server CPU space. The chip giant still generated $4.6 billion worth of Data Center revenues in the quarter and the news from NVIDIA suggests this segment continues to grow providing additional revenues for AMD still to grab on top of taking share.

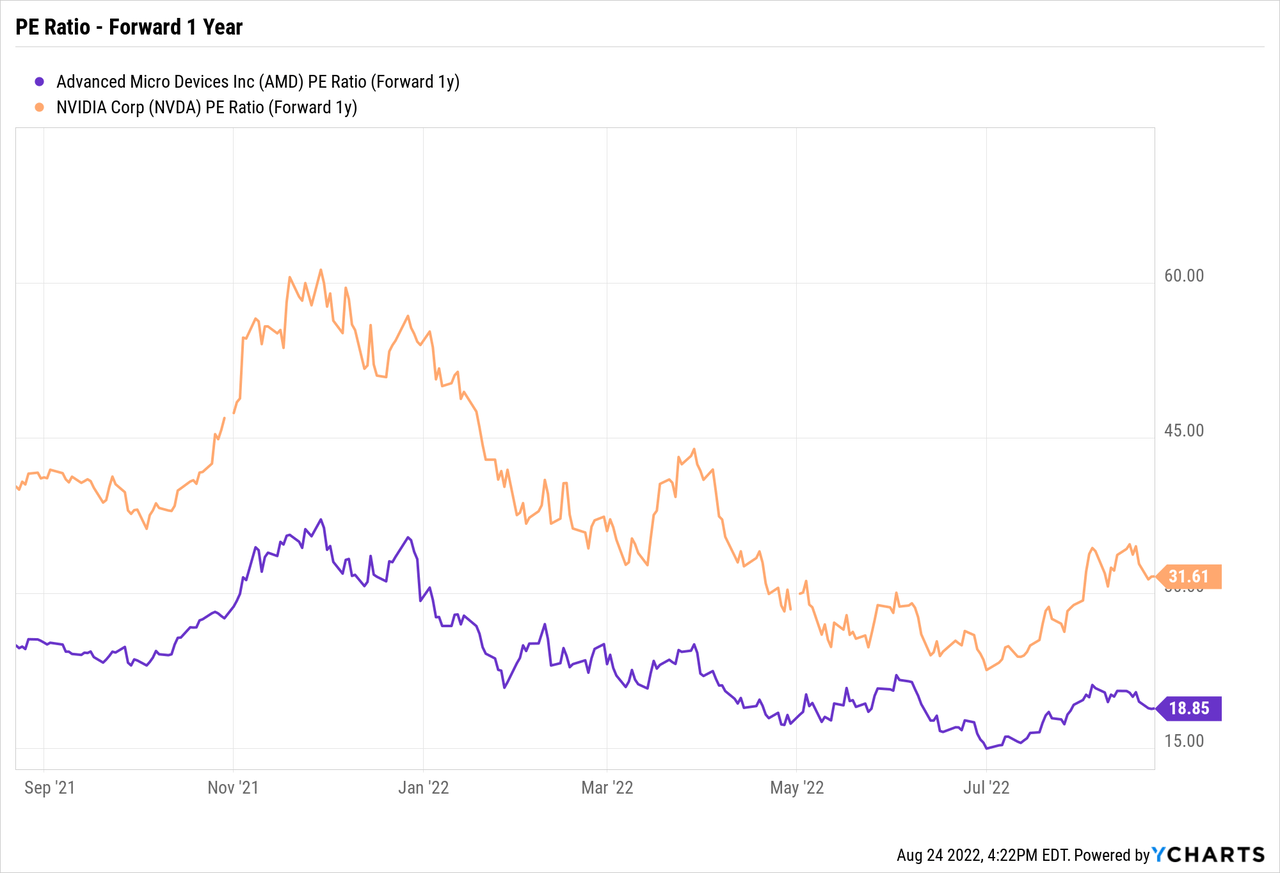

AMD remains on the path for 35% organic revenue growth this year while NVIDIA might actually report FQ3 revenue slide from last year. The odd part is that NVIDIA still trades at a premium valuation multiple to AMD.

Analysts will have to cut NVIDIA estimates for the FQ3 guidance cut, but the stock was already trading at nearly double the forward P/E multiple of AMD. NVIDIA might fall towards the valuation multiple of AMD at only 18x earnings, but the stock isn’t falling materially in initial after-hours trading.

My previous research has AMD on a path to $6+ EPS, placing the stock actually trading at 15x 2023 EPS estimates. Analysts have revised 2023 EPS estimates down to $4.92 due to the weakness of other chip companies, nothing AMD related to company specific reports.

Upside Down Valuations

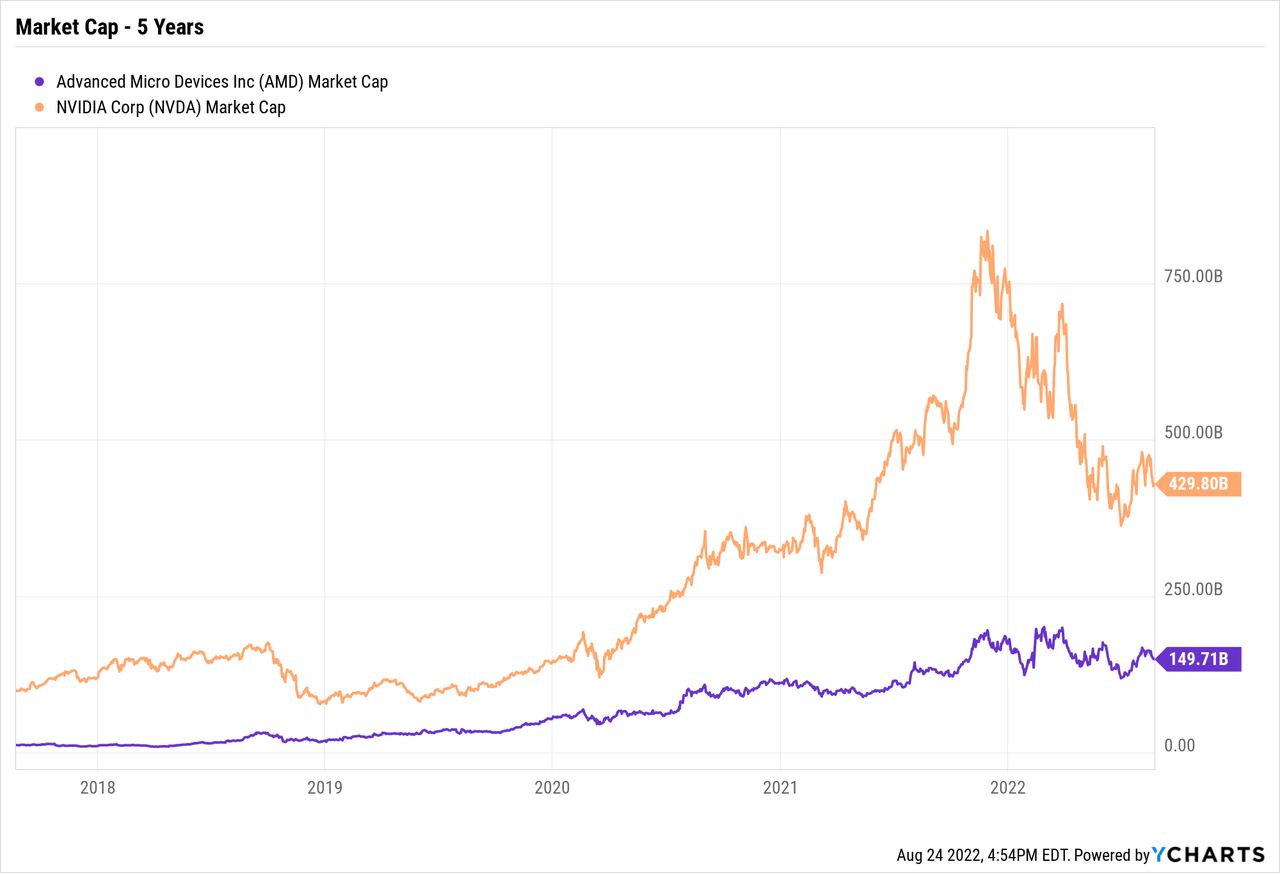

The market cap offers another prime example of how the market valuations are disconnected with AMD oddly out of favor. NVIDIA has nearly triple the market cap now at $430 billion compared to only $150 billion for AMD.

Some of the difference can be prescribed to NVIDIA generating higher gross margins on revenues. The GPU leader forecasts maintaining a 65% gross margin even with sales dipping back down to $5.9 billion while AMD is still pushing towards mid-50% range.

If all else were equal, NVIDIA should probably trade at a premium with higher margins. Of course, quarterly revenues are now equal in the last reported quarters with AMD actually pushing ahead of NVIDIA for the current FQ3 quarter. AMD guided to revenues of $6.7 billion while NVIDIA is just guided down to only $5.9 billion and the company hasn’t exactly hit guidance recently.

Most of the financial metrics point towards AMD worthy of trading with the highest valuation, yet the stock actually trades far below the valuation of NVIDIA. Even another earnings miss isn’t causing a material selloff in NVIDA despite a premium valuation heading into earnings.

Takeaway

The key investor takeaway is that AMD is far too cheap trading at 15x EPS targets. At the same time, NVIDIA continues to maintain premium P/E multiples far in excess of where AMD trades now and close to where the previous smaller chip company traded at peak valuations.

The stock market has to correct with either AMD rising or NVIDIA collapsing to better align the valuations. The likely outcome in the current weak stock market is probably NVIDIA taking another step lower with a test of the recent lows below $150.

Either way, AMD should get a boost due to growing revenues from taking market share versus needing the market to grow. Investors should use any weakness in AMD caused by NVIDIA cutting guidance as another buying opportunity.

Be the first to comment