It’s time to walk you through one of my favorite dividend (growth) stocks on the market. Florida-based L3Harris Technologies, Inc. (NYSE:LHX) is one of the world’s largest defense contractors. It has a dividend yield close to 2%, high and sustainable dividend growth, satisfying share buybacks, and above all, a well-diversified business model that now benefits from accelerating defense spending. In this article, I will discuss 3 “whys”:

Why (I believe that) dividend growth is so important

Why defense companies are set to benefit from higher defense spending

Why L3Harris is one of my favorite holdings

Without further ado, let’s get to it!

1. Why Dividend Growth Is So Important

The “dividend growth” versus “high dividend yield” debate is complicated and almost as impossible to lead to unity as the debate of who’s the best quarterback in the NFL.

Some investors want a high yield. Some want higher growth.

My position is that it depends on a few things. One of these things is one’s age. It is almost obvious that older investors need a higher yield. After all, the goal of investing is that passive cash flows cover expenses.

Getting to a point where money can be turned into cost-covering investments can be done by investing in dividend growth stocks.

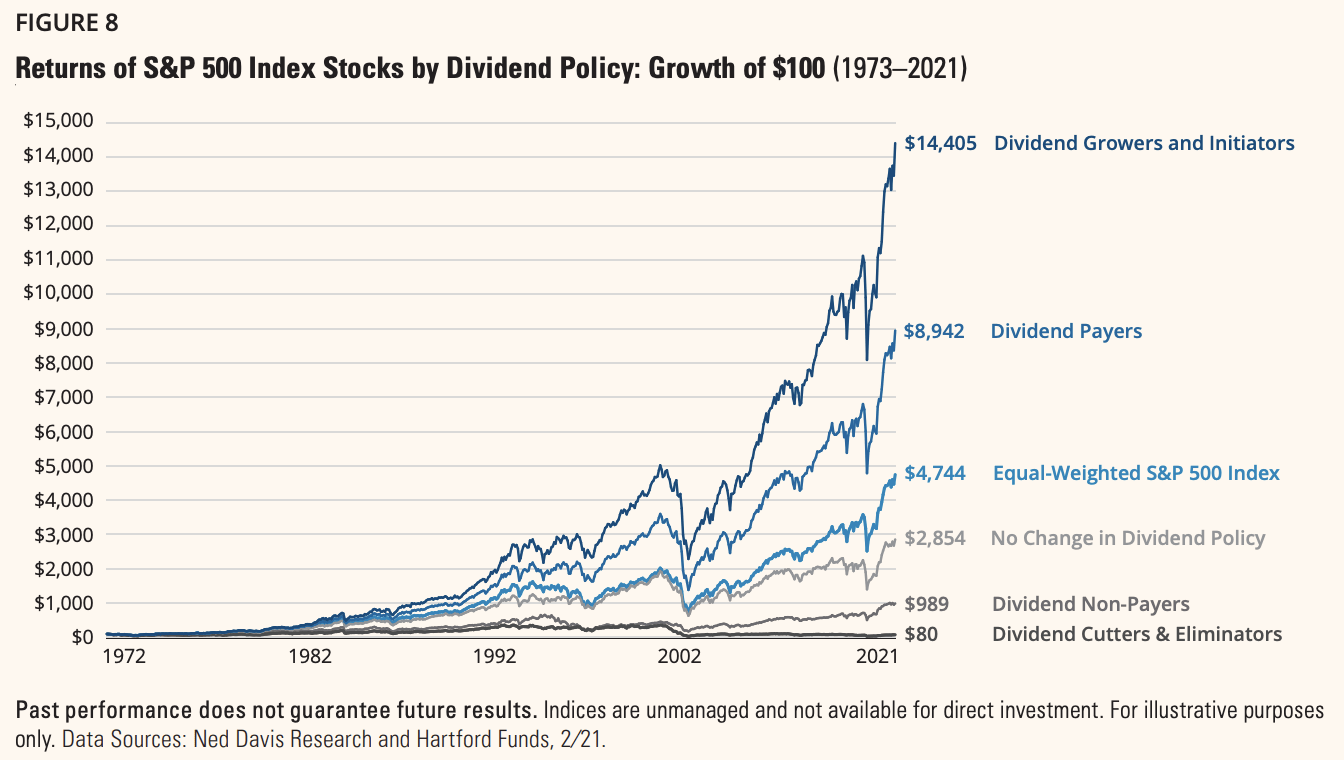

According to Hartford Funds, $100 invested in 1972 would have turned into more than $4,700 in 2021 when invested into the equal-weighted S&P 500. That’s a decent return. However, it would have turned into more than 14,400 when invested in dividend growers and initiators. That’s a huge difference.

Hartford Funds

This outperformance has multiple reasons. One of them is quality. According to a recent S&P Global report:

Dividend growth stocks tend to be of higher quality than those of the broader market in terms of earnings quality and leverage. Quite simply, when a company is reliably able to boost its dividend for years or even decades, this may suggest it has a certain amount of financial strength and discipline.

The other reason is (low) volatility:

Dividend growth stocks could be attractive to market participants looking for disciplined companies that can endure difficult market and economic environments relatively well.

[…]

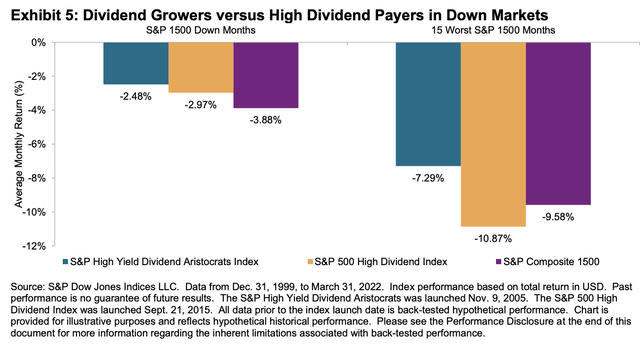

When we focus on the 15 worst-performing months for the S&P 1500 during the same period, the protection provided by the S&P High Yield Dividend Aristocrats was prominent. Its monthly outperformance was 229 bps and 358 bps against the S&P 1500 and S&P 500 High Dividend Index, respectively (see Exhibit 5).

S&P Global

I’m glad that S&P Global brought up low volatility because, this too, is one of the reasons why long-term outperformance is possible as I explained in this article. Basically, low volatility protects investors during a bear market. While some dividend growth stocks may underperform in bull markets, limited downside during bad times really adds up on a long-term basis.

2. Higher Defense Spending

We’re getting a massive tailwind for defense companies – unfortunately for the wrong reasons. The war in Ukraine has changed the game. It has done a number on energy, agriculture, and related markets to an extent that European countries are now going back to using coal and rethinking their defense spending plans – both were unheard of prior to the war.

The other day, I was hit by the following Defense One headline:

Defense One

The alliance will increase its response force from 40,000 to 300,000 to respond to Putin’s threats in the East of Europe.

However, I care about something else Stoltenberg said:

Stoltenberg said allies will need to spend more on defense to be able to fill this growing need for troops and replenish the military aid many are giving to Ukraine. In 2014, NATO set a guideline for members to spend 2 percent of gross domestic product on defense by 2024. Even after eight straight years of growth, Stoltenberg said the alliance should be aiming higher.

“Two percent is increasingly considered a floor, not the ceiling,” he said.

Germany, Europe’s industrial and chemical heart has so far refused to spend 2% on defense. However, the government has agreed to ramp up defense spending via a special EUR 100 billion bill.

The aim is to rapidly modernize its armed forces, including adding Lockheed Martin’s (LMT) F-35 jet.

In the U.S., we’re seeing similar developments. Last week, it was reported that the House Armed Services Committee boosted proposed Pentagon funding for fiscal 2023 by $37 billion, this surpasses the White House’s request. Unfortunately, it’s a bit below the funding approved by Senators a week earlier.

The reason why it’s easier to push for higher funding – in addition to high inflation – is that the world is slowly but steadily becoming a geopolitical mess:

“We need only look to world events in Ukraine, read reports regarding China’s plans and actions in the South China Sea, or simply read the latest headline about Iranian nuclear ambitions and North Korean missile tests, as well as ongoing terrorist threats, in order to see why this funding is necessary,” Golden said Wednesday at a House Armed Services Committee markup of the bill.

Here’s what this additional money can achieve:

The extra money would buy eight more F/A-18 jets, five more C-130 cargo planes, and one more frigate than the Biden administration has proposed, and pay to keep five littoral combat ships that the Pentagon wants to retire. It would also add $550 million to the Ukraine Security Assistance Initiative, $3.5 billion to military construction spending, and $2.5 billion to offset the high cost of fuel.

3. L3Harris – Dividends & Outperformance

With a market cap of $46.0 billion, L3Harris is the sixth-largest aerospace & defense company in the United States. Located in Melbourne, Florida, L3Harris is the result of the merger between L3 and Harris that closed in June of 2019.

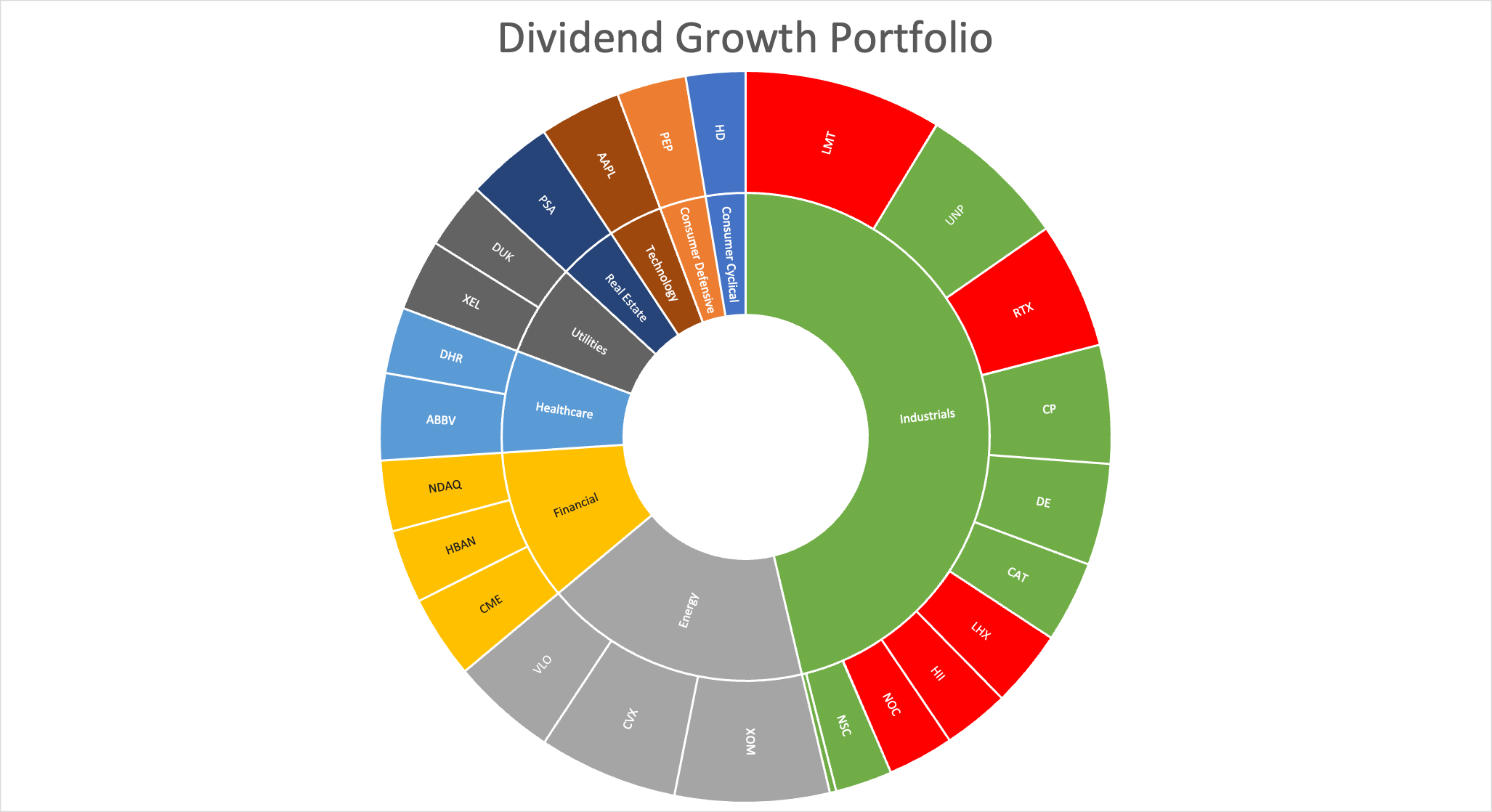

I own five defense companies in my dividend growth portfolio. While it’s not a “must” to own this many, I like the value these companies bring to the table. Especially because they are all unique.

Author Portfolio

What I like about L3Harris is its diversified business. Whereas Lockheed is highly dependent on its F-35 fighter, L3Harris is a supplier of all major defense companies, offering a wide range of smaller products and services.

The company operated four business segments going into this year. Because they are so diverse, I’m quoting the company:

“Integrated Mission Systems, including multi-mission intelligence, surveillance and reconnaissance (“ISR”) and communication systems; integrated electrical and electronic systems for maritime platforms; and advanced electro-optical and infrared (“EO/IR”) solutions;

Space & Airborne Systems, including space payloads, sensors, and full-mission solutions; classified intelligence and cyber defense; avionics; and electronic warfare;

Communication Systems, including tactical communications; broadband communications; integrated vision solutions; and public safety radios; global communications solutions and

Aviation Systems, including defense aviation; commercial aviation products; commercial pilot training; and mission networks for air traffic management.”

Earlier this year, the company announced a new alignment, reducing the number of segments to three: Integrated Mission Systems, Space and Airborne Systems, and Communication Systems.

Some people asked me if this means the company is selling its Aviation Systems business. That’s not the case. It’s a simple re-alignment.

On top of that, the company services high-tech projects, which are now taking priority over more “traditional” hardware. The war in Ukraine shows that defense priorities are shifting away from ground hardware to next-gen technologies.

Budget dollars have and are expected to continue gravitating towards agile, advanced and affordable solutions domestically and internationally to address a range of threats. In addition, while the slow contracting activity from late 2021 has carried into the early part of the year, based on recent events, the company is optimistic regarding the trajectory of new awards.

In the 1Q22 quarter, the company’s last-twelve-months book/bill ratio was 1.01, which is quite good given that 2021 was rather slow. I expect this number to accelerate, providing the company with a steady flow of orders.

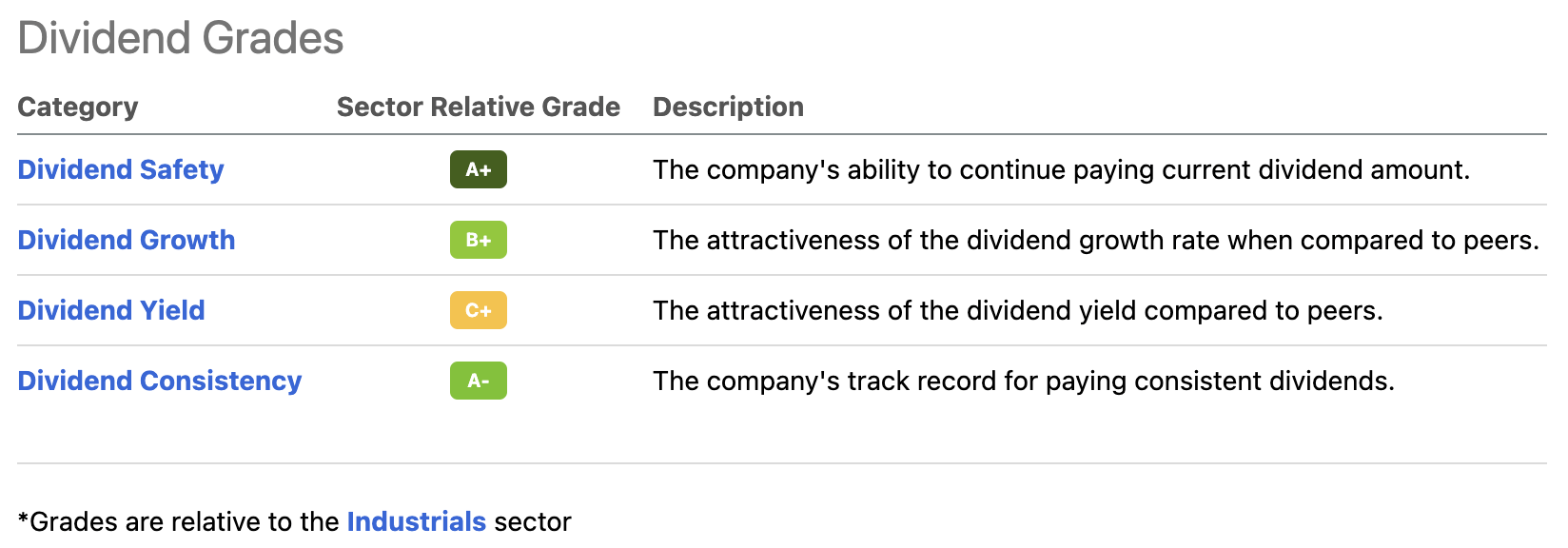

With that said, the company is scoring very high on Seeking Alpha’s dividend scorecard – these scores are compared to the industrial sector.

Seeking Alpha

The only segment that scores low is the dividend yield.

L3Harris is paying a $1.12 per share quarterly dividend. That’s $4.48 per year. That’s roughly 1.9% of the company’s stock price.

Dividend growth, however, is much better. If we go back 10 years, prior to the merger, we get a 10-year average annual dividend growth rate of 14.1%.

These are the most recent hikes (all post-merger):

February 25, 2022: 9.8%

February 26, 2021: 20.0%

February 28, 2020: 13.3%

These growth rates are impressive and the result of high free cash flow generation and the fact that net debt is low. Net debt is expected to remain close to 1.5x EBITDA, proving LHX with the opportunity to distribute its free cash flow. Free cash flow is consistently above net income, indicating high-quality earnings that end up as cash on the company’s balance sheet or in investors’ portfolios through dividends.

TIKR.com

Next year, the company is expected to do $2.9 billion in free cash flow. This implies a free cash flow yield of 6.3% based on the company’s $46.0 billion market cap.

This implies that the company can return more than 6% of its market cap in 2023 through dividends and buybacks. The dividend yield won’t be hiked to 6.3%, but it shows how much upside there is – without incorporating future free cash flow growth.

It explains the high dividend growth rates of the past few years and aggressive buybacks. Between 2019 and 2021, the company bought back roughly 20 million shares. That’s a decline of 9% in just 2 full years.

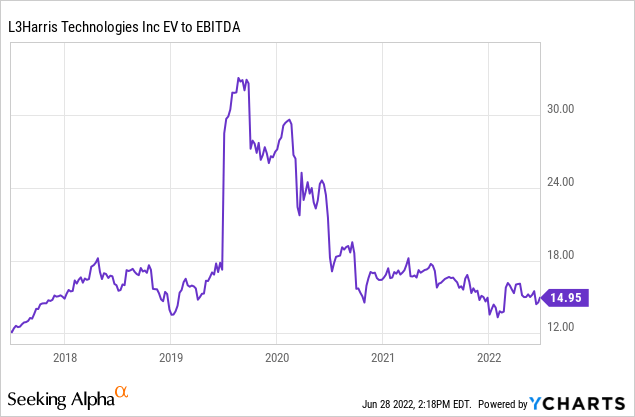

When it comes to the company’s valuation, we’re dealing with a 13x 2023 EBITDA multiple. This is based on a $52.2 billion enterprise value consisting of a $46 billion market cap, $5.6 billion in expected net debt, $110 million in minority interest, and $520 million in pension-related liabilities.

2023 EBITDA is expected to be $4.0 billion.

13.0x EBITDA isn’t deep value, but it’s one of the lower valuations in the company’s short history and a very fair valuation based on strong EBITDA and free cash flow growth.

The market is in turmoil. Volatility is high, and economic and geopolitical uncertainty has gone through the roof.

I have almost all of my money invested in my long-only dividend growth portfolio. I, too, have seen my net worth decline this year. Yet, I haven’t worried for a single second.

While it’s certainly not fun to be in a bear market, it’s fun to buy quality stocks at great prices. Moreover, owning high-quality dividend growth stocks is one of the reasons why I haven’t lost any sleep.

L3Harris Technologies has been in my portfolio since 2020. The company benefits from great management, a well-diversified business portfolio, high-quality earnings, strong free cash flow, and management willing to distribute cash to its shareholders.

The company is now trading at 13.0x 2023 EBITDA and a 1.9% dividend yield. The dividend yield is expected to remain in double-digit territory on a longer-term basis, providing investors with the opportunity to beat the market without being exposed to high volatility.

L3Harris is also benefiting from higher (expected) global defense spending, which I believe will fuel new orders for years to come.

Long story short, I will keep adding to LHX and believe that investors looking for quality dividend growth shouldn’t look any further.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment