loveguli

Thesis

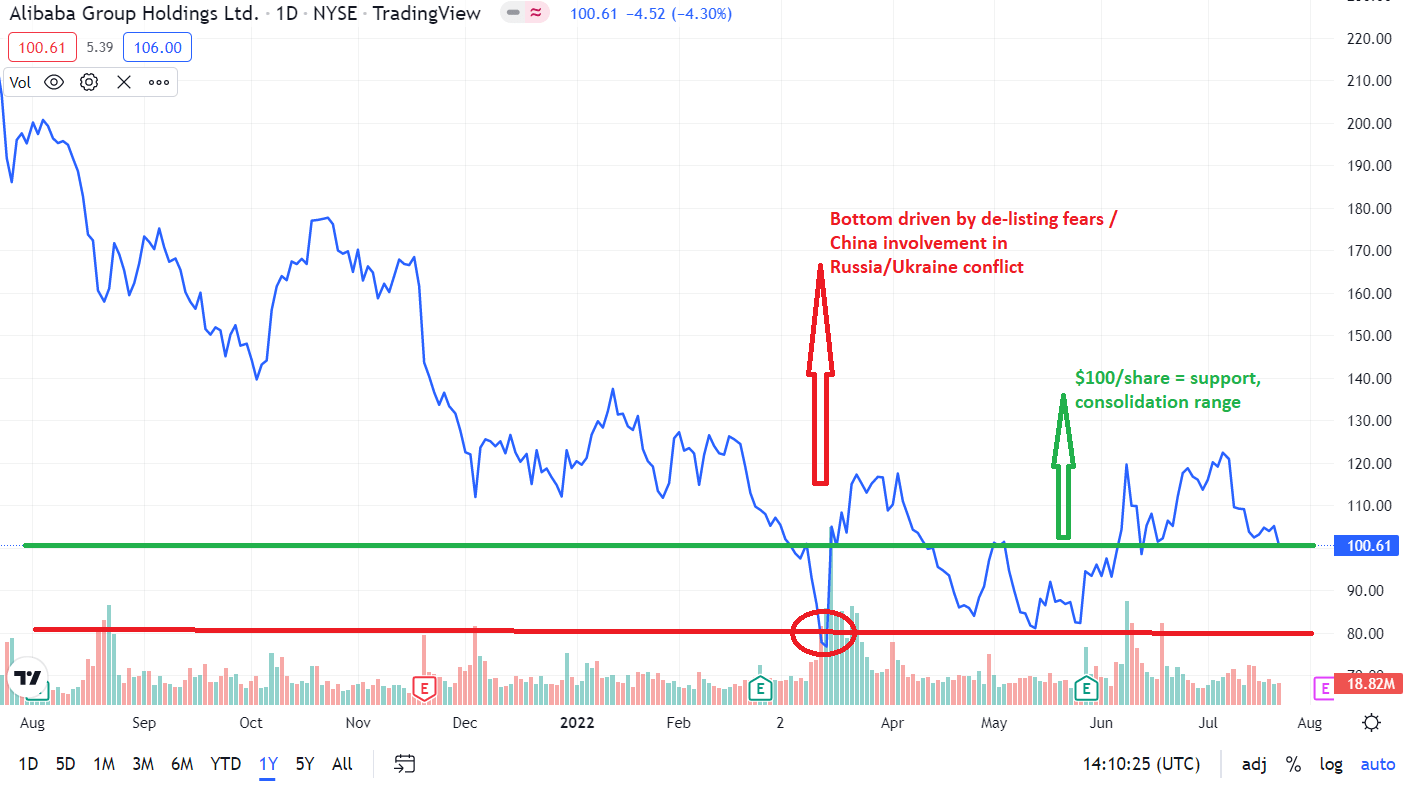

Alibaba Group Holding Limited (NYSE:BABA, OTCPK:BABAF) has been in a consolidation pattern since it bottomed out in mid-March:

BABA 1-year price action (TradingView)

The stock moved sharply lower mid-March on the back of de-listing fears driven by the potential China intervention in the Russia/Ukraine conflict. That fear never materialized and the stock has started forming a bottom and consolidating around the $100 price point. There have been several green arrows from the Chinese regulators regarding their crack-down on Chinese tech companies, and the overall environment is much more constructive now from a macro stand-point. After their infamous “un-investable” call on Chinese stocks earlier in the year (which marked a bottom), JPMorgan (JPM) and other large investment banks are turning constructive on the sector and the economy.

We feel mid-March marked a bottom in the Alibaba stock price, and that the current consolidation is going to be followed by a rally in the stock. However we are mindful that we are still in the midst of a bear market in U.S. stocks, hence we are putting forward a conservative options-based strategy to take advantage of our view on the BABA stock and the high implied volatility exhibited in the option chain. We are putting forward below in the “What is the trade” section a put spread idea that can generate an annualized yield of 26% if the BABA stock price stays above $80/share upon maturity. The strategy contains a tail risk hedge, given that in today’s macro and political environment (as Russian ADRs have shown us) one never knows how politics can blow up sound economic fundamentals to the detriment of retail investors.

What is a put spread

A put spread consists of two put options. In our case, we are taking a bullish view on the stock via our trade, believing that BABA will not breach the $80 mark. First, an investor buys one put option and pays a premium. At the same time, the investor sells a second put option with a strike price that is higher than the one they purchased, receiving a premium for that sale. Note that both options will have the same expiration date. Since puts lose value as the underlying increases, both options would expire worthless if the underlying price finishes higher. Therefore, the maximum profit would be the premium received from writing the spread.

A put spread is a conservative option strategy to take a long position in a stock, with the downside being cushioned by a lower strike and the upside capped at the premium received.

What is the trade

The trade involves selling a June 2023 $80 strike put and concomitantly buying a $50 strike put:

Trade Description (Author)

The trade is done for 5 contracts (each contract is equal to 100 shares), so the max exposure is $40,000 on the first leg. Given that the strategy also implies selling a $50 strike put the net exposure is much better at only $15,000 (40,000-25,000). This means that if theoretically BABA goes to zero tomorrow the investor is on the hook for only a $15,000 loss (less net premium received).

Basically a put spread is a much more conservative way of taking a view on a company’s stock and monetizing the implied volatility than an outright put sell. An investor outright long 500 shares of BABA right now is set to lose $50,000 if the stock goes to zero tomorrow (theoretical example of course). Writing solely a $80 strike put gets your exposure to $40,000, while the put spread strategy narrows the max loss to $15,000.

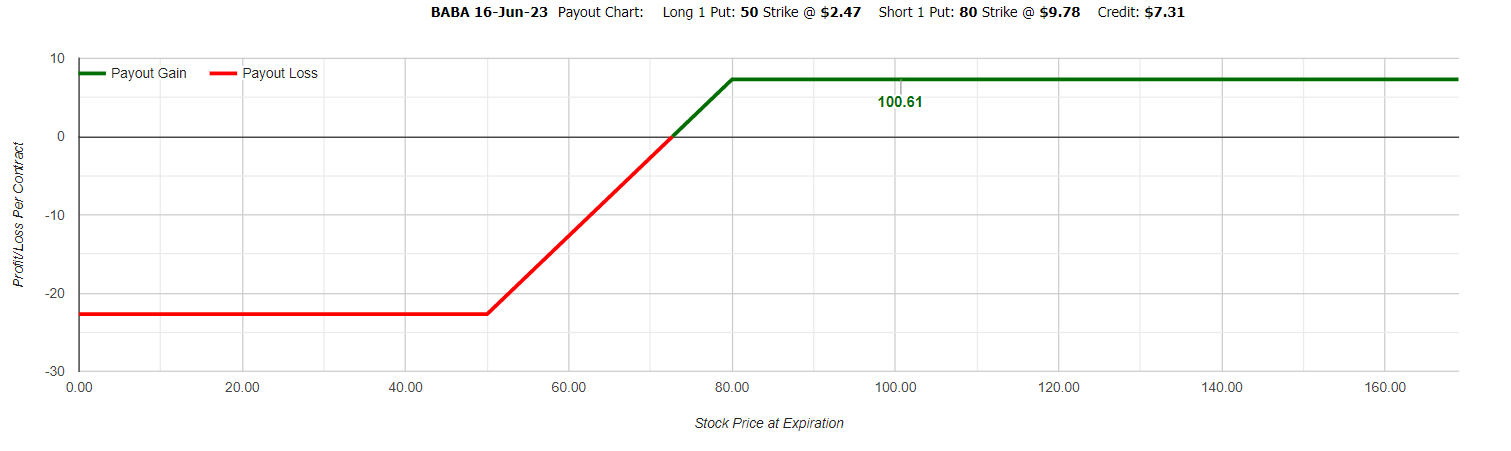

The payout profile for the strategy is as follows (courtesy of MarketChameleon):

Payout profile (MarketChameleon)

The potential scenarios for the strategy upon expiry in June 2023 are:

Scenario 1

- The BABA stock trades above $80/share upon expiry

- Both puts expire without getting triggered

- An investor realizes the premium of $3,490 (net premium on the buy and sell leg)

- The premium translates into an annualized yield of 26%

Scenario 2

- The BABA stock trades below $80/share upon expiry, but above $50

- The investor gets triggered on the written $80 put

- The investor ends up buying the BABA stock at $80 minus premium received

- The $50 put expires without getting triggered

Scenario 3 (doomsday, theoretical)

- BABA stock goes to zero

- Both puts get triggered

- The investor realizes a net loss of $40,000 – $25,000 – $3,490 = $11,510

- The net loss is much lower than an outright put sell

Conclusion

We like BABA here and we like the Chinese economy set-up. China is going through a slowdown and the Chinese government hammered tech companies last year to deal with a widening social inequality in the country. We feel the worst is behind BABA and the stock established a bottom around $80/share back in March when it traded sharply lower on the back of delisting fears. Right now, BABA is consolidating around $100/share and set to move up in the next year in our view. We feel a savvy investor can take advantage of the high stock implied volatility via a put spread strategy which allows for a nice, cheap tail hedge for a Chinese ADR and a 26% annualized yield.

Be the first to comment