Robert Way

Alibaba’s (NYSE:BABA) (OTCPK:BABAF) shares are down 45% over the past year but don’t be tempted to call it a bottom just yet. Latest data reveals that institutional investors have collectively sold off over 25 million of Alibaba’s shares in the last 13F reporting cycle on a net basis. Clearly, these sophisticated investors feel the stock still has ample downside potential from the current levels, despite its recent correction, which should encourage investors to remain on the sidelines for the time being at least and reconsider their long-side thesis for the name. Let’s take a closer look to gain a better understanding of it all.

Tracking Institutional Activity

Let me start by saying that institutional investors have certain resources at their disposal – such as research teams, cutting-edge research tools, and access to company managements – that provide them with an edge over retail investors. So, tracking the trading activity of these sophisticated investors reveals how their sentiment pertaining to any given stock is evolving with time, and if it aligns with our trade direction.

Coming to Alibaba, a group of 437 institutions collectively bought 51.4 million shares, while another group of 704 institutions sold off 76.7 million of the ecommerce company’s shares in the last 13F cycle. This means that institutional investors sold off 25.3 million of Alibaba’s shares last quarter on a net basis. To put things in perspective, this selloff amounts to nearly 1% of the company’s total shares outstanding at the time of this writing.

To make matters worse, note how the number of institutions that sold off Alibaba’s shares (704), greatly outnumbered those that increased their positions (437) in the company. This is a clear indication that the selloff wasn’t concentrated across a few entities and was actually driven by a broad swath of institutions that grew bearish on the name.

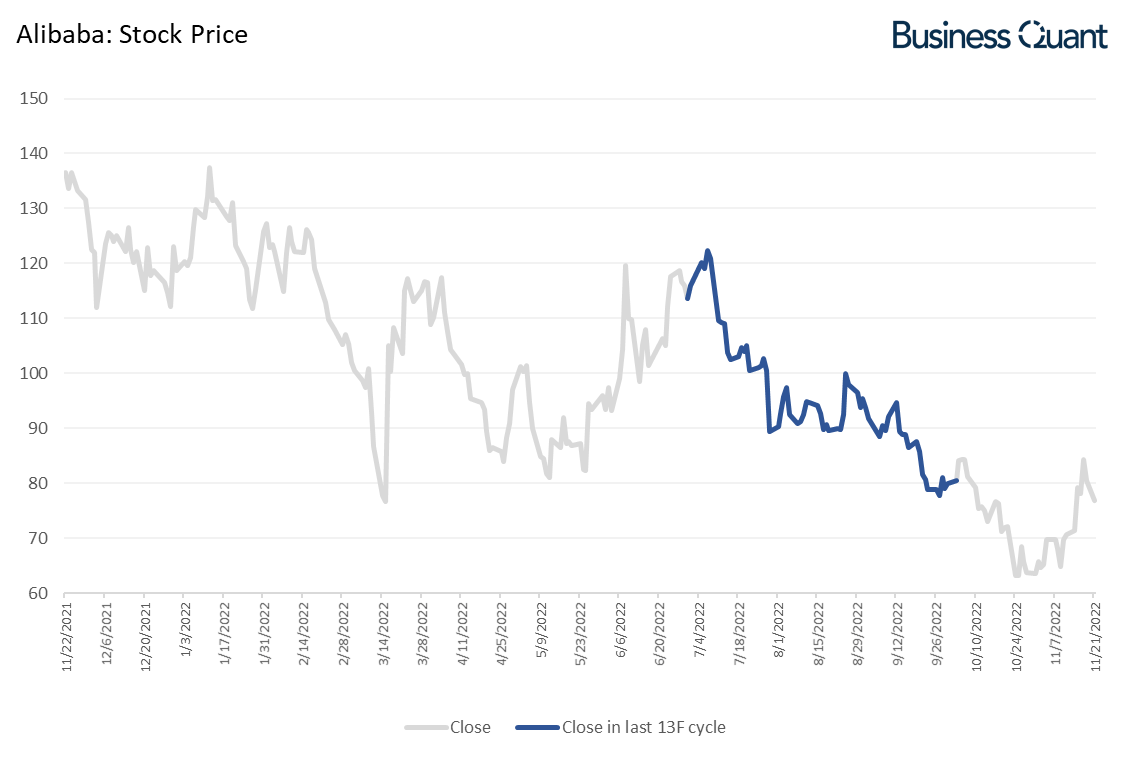

What’s particularly interesting here is that Alibaba’s shares were on a constant decline during the last 13F reporting cycle, when these entities were trimming their positions in the internet giant. These entities clearly did not perceive the stock to be attractive in the $80 and $120 price band, meaning it’s likely to act as a resistance/upper ceiling for the stock should it rally in the coming weeks.

BusinessQuant.com

For the record, the last 13F reporting cycle spanned from July through September and the data was fully disseminated only last week. This means the data being referenced in this article is still fresh and relevant to our discussion here.

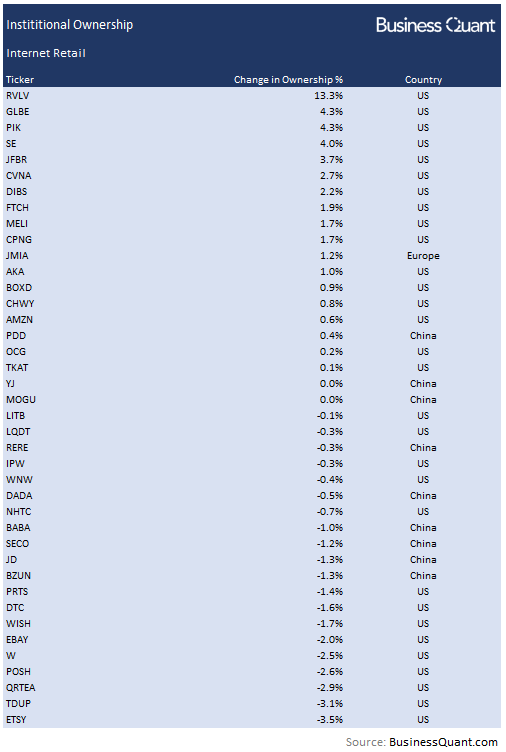

Moving on, I also wanted to check if institutional investors were bearish on Alibaba in particular, or if they were bearish on the entire e-commerce industry. If these entities were bearish on the entire industry, then Alibaba wouldn’t stand out and our discussion would end right here. So, I compiled the institutional ownership data relating to 40 internet retail companies that are currently listed on US bourses.

Interestingly, there wasn’t any dominating bullish or bearish sentiment in the internet retail industry as a whole. But note in the table below that these investors were bearish on internet retail stocks from China in particular, such as Alibaba, JD.com (JD), and Baozun (BZUN) amongst others. So, it seems like a deliberate effort to cut exposure to Chinese internet retail stocks.

BusinessQuant.com

We cannot argue that Alibaba is better than JD or Baozun just because institutions sold off only 1% of its shares while its mentioned peers saw a 1.3% selloff. First, there’s only a marginal difference in both the selloff figures due to which we cannot speculate that institutions have different approach towards any of these mentioned stocks. Secondly, a selloff is a selloff, and the data indicates institutional bearishness towards Chinese internet retail stocks. So, I’d say, all three mentioned stocks are in the same boat.

This establishes the fact that institutional investors grew bearish on Alibaba in the last 13F cycle. But this leads us to an important question – what’s the underlying reason for this widespread bearishness?

Reasons for Exercising Caution

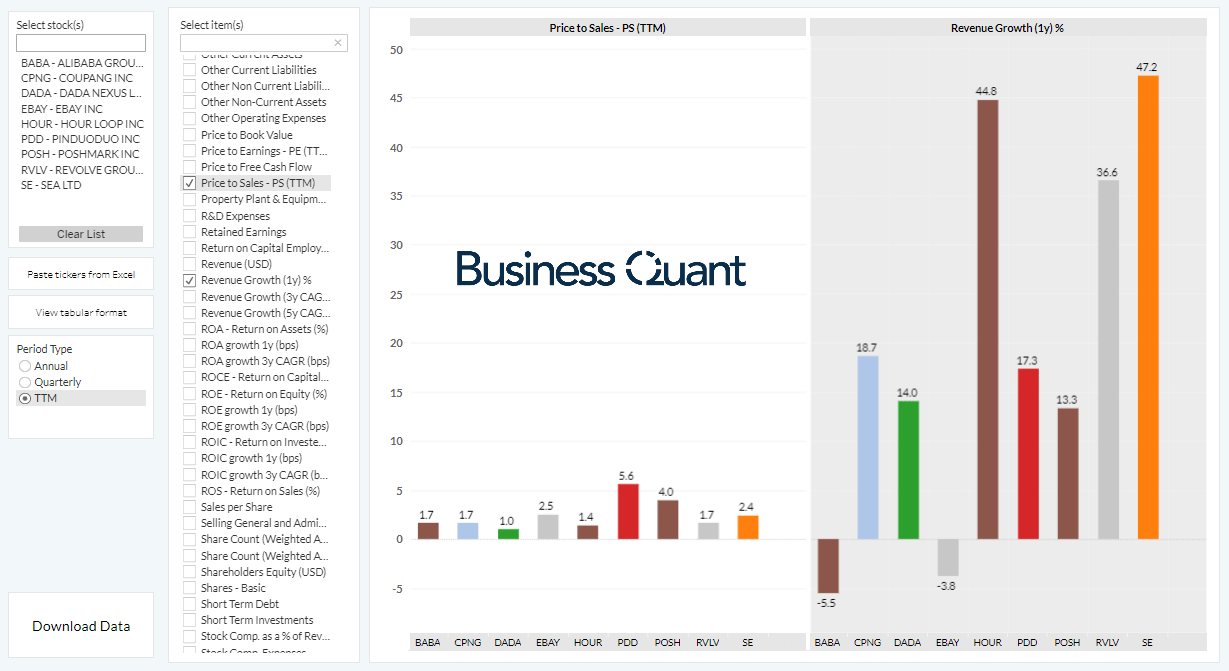

First of all, there’s the common misconception that Alibaba’s shares are undervalued at current levels. The stock is trading at just 1.7 times its trailing twelve-month sales, which seems quite low and attractive on a standalone basis. But low valuation multiples aren’t the sole determinant of how attractive an investment might be.

It’s important to remember that Alibaba’s trailing twelve-month revenue is down 5.5% per its latest earnings release. In contrast, there are several other internet retail companies that are trading at similar Price-to-Sales (or P/S) multiples whilst still posting elevated levels of revenue growth, going as high as 47% in certain cases. This means Alibaba makes for a really poor investment on a relative basis.

BusinessQuant.com

Secondly, Alibaba won’t be able to turn the tide anytime soon, and it’s likely to remain revenue challenged in the coming quarters as well. I say this because COVID-19 cases have spiked in China this week, and the country’s regulators are now intensifying their lockdowns to prevent the infection from spreading further (like here).

I believe this development will have a two-fold effect. First, it will cripple China’s logistics operations as the movement of goods will be restricted across cities. Secondly, Chinese citizens won’t be able to go to their workplaces, and they’re likely to face mass layoffs/pay cuts all over again, which will limit their purchasing power. For Alibaba and its shareholders, this means Alibaba’s ecommerce operations in China will post a yet another revenue decline next quarter.

BusinessQuant.com

Lastly, Chinese government is intensifying its push towards the common prosperity goal. This involves the transfer of wealth to the poor by way of tinkering with how private companies such as Alibaba conduct business, breaking them apart should they become too big or grow too quickly. These regulatory interventions limit Alibaba’s growth potential and add uncertainty to its growth prospects, essentially souring the investment sentiment.

Final Thoughts

There’s no denying that Alibaba has grown at a spectacular pace in the past decade and has been extremely rewarding for its shareholders. But those days seem to be over and in the past. The company is now mired with regulatory uncertainty, its growth prospects are limited, and the stock isn’t appealing when looking at industry comparables.

As the valuation comparison chart above indicates, there are several other stocks in the internet retail industry that are trading at low P/S multiples but growing their revenue at a rapid rate. This, in my opinion, is another major reason why a broad swathe of institutional investors has been dumping Alibaba’s shares of late.

Considering these issues, I believe it’s best to avoid Alibaba for the time being and have a “Hold” rating for the name. This, however, should not be construed as a call to sell the stock. Good Luck!

Be the first to comment