MattGush/iStock via Getty Images

I’ve been a longtime shareholder of Grupo Aeroportuario del Pacifico (NYSE:PAC), or Pacific Airport Group in English. I named the company my Top Pick for 2017 here at Seeking Alpha and have published a number of subsequent focus articles about the company over the years. I recommend my prior work for readers wanting a general understanding of the company, its assets, and the general thesis for owning shares.

I last covered the company in May of 2022. This article will focus on developments with the company since then, along with some highlights I got from talking to Pacifico’s CFO.

Traffic Growth Remains Exceptional

Pacifico — and Mexican airports more generally — were among the fastest to recover from the pandemic globally among aviation companies. This came about for a variety of reasons. The most obvious was that Mexico had fewer restrictions on its travel and hospitality industry as it relates to lockdowns, vaccine mandates, and other such matters as compared to regional destinations. As a result, Mexico picked up a large portion of Americas travel activity which would have otherwise gone to the Caribbean or other alternatives.

Pacifico has a healthy mix of Mexican airport concessions covering both tourism-focused airports along with properties more tied to industry. Predictably, Pacifico’s tourist airports such as Cabos and Puerto Vallarta bounced back the quickest from the 2020 travel pause. Meanwhile, traffic was slower to rebound in more industry-focused airports like Hermosillo and Bajio/Guanajuato.

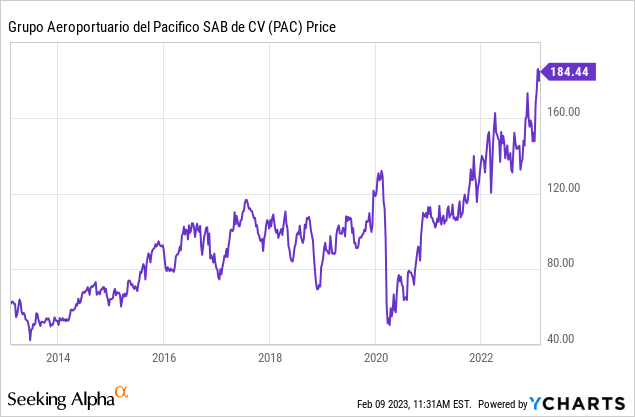

Overall, Pacifico’s total airport traffic returned to pre-pandemic levels in late 2021. This was a speedy recovery, all things considered, and the stock’s total returns largely followed the pattern in passenger numbers.

Pacifico’s stock price moved to new all-time highs in late 2021 just as its passenger numbers surpassed pre-pandemic levels.

However, 2022 is where things started to get really interesting. Some analysts may have expected Pacifico’s traffic growth to taper off recently. After all, traffic was already comfortably ahead of 2019 numbers by early 2022. And surely many folks that were eager to travel had already visited Mexico in 2021.

And yet, this anticipated tourism slowdown simply hasn’t happened. Instead, Pacifico’s tourism-focused airports continue to deliver exceptional results.

And now, adding to the fun, the industrial and big city airports are starting to post 25-30% traffic growth of their own. Adding it all up, Pacifico’s traffic growth is actually accelerating to the upside. For October, November, and December 2022, traffic grew 22%, 22%, and 18% respectively, which is all quite good. However, things were about to get better.

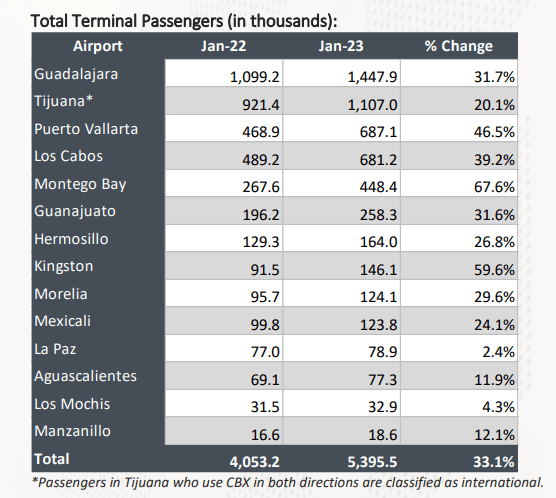

This was shown in dramatic fashion with the company’s just-released January 2023 traffic numbers, where traffic growth skyrocketed 33% year-over-year:

Airport traffic results (Corporate filing)

The company is seeing tremendous growth across almost the entire portfolio. All ten of Pacifico’s ten largest airports grew by at least 20% year-over-year. And, I’d note, January 2022 traffic was already back to pre-pandemic levels, meaning this 33% growth for January 2023 is far into previously uncharted territory.

Despite fears of a tourism slowdown, Cabos notched another 39% rise in traffic in January 2023, and Puerto Vallarta jumped by a stunning 46%. It’s not just the tourism airports, though. Pacifico’s crown jewel, the big city airport of Guadalajara, is now growing more than 30% year-over-year, which is a sharp improvement from much of last year’s numbers. Industrial-focused airports like Hermosillo and Guanajuato are starting to see the impact of the reshoring/manufacturing boom kick in as well.

Finally, I’d note that the Jamaica airports (Kingston and Montego Bay) are both growing at about 60%/year now. Though Jamaica, unlike Mexico, had more strict COVID-19 restrictions so much of this is still recovery from the pandemic rather than additional growth beyond the prior peak. That said, Jamaica has historically been a small piece of the valuation picture at Pacifico anyway, so this sort of rapid headline growth is an added kicker to an already healthy growth story.

What’s Driving Pacifico’s Tremendous Growth?

Some of this traffic gains can be explained by the same factors that have powered the boom in activity for fellow airport operator Centro Norte Airports (OMAB). As I recently described, it is benefitting from the rise in manufacturing companies that are putting new factories in Mexico rather than Asia as supply chains are readjusted in the shifting economic landscape.

However, there’s more nuance to add than that. Specifically, I spoke to Pacifico’s CFO Saúl Villarreal along with the head of the company’s investor relations team last summer. I’ll highlight some key points below. Note that the conversation was in Spanish, and any direct quotes are my translation.

One key consideration has been the new airport in Mexico City. The current Mexican administration blocked the completion of the planned large new Mexico City Airport. This came as a surprise to investors, as the $13 billion facility was already partially built, and the airline industry was looking forward to its completion. However, the then newly-elected president cancelled it on purported environmental grounds along with allegations of corruption by the prior administration.

This airport was viewed as vital, since Mexico City’s existing international airport has already been over its stated capacity for years now and simply can’t accept many more flights. This has blocked the expansion of new routes and frequencies at the capital since the mid-2010s. The planned airport would have fixed these capacity issues, but that was taken out of the equation.

What’s it mean for Pacifico? There are two points. One, the government did open a new airport in the Mexico City area. However, it merely converted a military base that lies far outside of the city into a commercial airport, and — not surprisingly — airlines haven’t rushed to the new facility. Industry analysts view the project as a failure.

That, however, is arguably a positive for Pacifico. This is because Mexico needs to build out other hubs to make up for the foregone traffic capacity at Mexico City. Namely, to that point, Pacifico is planning to increase capacity at Guadalajara dramatically, and Villarreal sees that airport being able to handle 40 million passengers a year in 2040.

This would be nearly a tripling of Guadalajara’s traffic from recent years. Additionally, airports tend to get network effects as they get bigger. You get larger-capacity flights from farther away destinations. You also can build more hotels, retail, advertising, etc. in the airport as you have more passengers passing through.

I’d note that as of now, the only airport in all of Latin America with more than 40 million passengers a year is Mexico City’s existing airport. Other regional leaders like Bogota, Sao Paulo, and Cancun all came in between 30 and 35 million passengers last year. Guadalajara is projecting to be one of the single most important and valuable airports in the Americas over the next 10-20 years.

A decent chunk of this opportunity is thanks to the decision to block new capacity at Mexico City, and thus force the airlines to build hubs elsewhere. But another piece of that is simply from Guadalajara’s continued growth. The city’s metropolitan area has surpassed 5 million people, and it is one of the wealthiest and most developed parts of the country. It has a significant amount of both manufacturing and technology industry jobs.

However, Villarreal noted that it has been logistics that has really driven growth for Guadalajara and the airport since the pandemic. Here’s Villarreal describing Guadalajara’s ongoing growth trajectory:

“In Guadalajara, what’s grown the most is the logistics market. Guadalajara has more cargo flights than any other city in Mexico. There’s been a huge growth in logistics centers close to the airport. These are companies that make “last-mile” deliveries, not just for Guadalajara but for surrounding regions including the key port of Manzanillo two hours away. Guadalajara accepts cargo from China, and distributes it […]

Also, in Guadalajara the tech industry has grown dramatically. They call Guadalajara the “Mexican Silicon Valley” because there’s tons of tech industries. And all these firms are situated next to the airport. This industry is powerful and has permitted the Guadalajara economy in general to always grow.”

Guadalajara, with its central location within Mexico and proximity to major rail links and vital American economic regions, has taken on rapidly-increasing importance as companies rush to figure out how to shore up their supply chains. Within Mexico in particular, there were large and persistent shortages of packaging materials and other basic inputs for manufacturing during the pandemic, much of which was due to things being stuck in Asia and/or in sea ports. Thus, companies are rushing to build backup supply chains on-land in Mexico to prevent future outages.

I also brought up a couple of other points I often hear investors worry about. One being the length of the concessions. Contractually, the Mexican airport contracts run through 2048 and are renewable for up to another 50 years after that. However, after talking to management, I get the sense that this 50-year renewal would not be likely to occur at one time, but rather in a series of smaller extensions. This makes sense, as the airport operators already come to an agreement with the government every five years to plan out future airport capital expenditures and tariff increases.

As far as CAPEX goes, the company paused some growth plans during the pandemic but has now gotten the ball rolling on them again. Given the traffic growth we’re seeing, along with the opportunity created by Mexico City being capacity-constrained, there should be ample room for Pacifico’s main airports to continue growing. In addition to the large expansion and adding of more retail and hospitality options at Guadalajara, the company is also pursuing a mixed-use project at Tijuana.

As far as inorganic growth goes, management said that it is constantly looking at additional airport concessions that come onto the market. However, it is conservative in nature, and has chosen not to bid in several auctions where it felt other airport operators were paying too high a price for concessions. My personal expectation is that Pacifico will add more airports to its holdings in due time, but not at the same rate as, say, Sureste (ASR) or Corporacion America Airports (CAAP).

Finally, I asked Villarreal to sum up the company’s value proposition for international investors considering Pacifico as part of their portfolio. Here’s what he said:

“Pacifico is an infrastructure business that is always focused on expansion. Our base is our assets which generate value. All of our airport terminal expansions are to create incremental value, in particular generating more commerce. Pacifico isn’t just focused on maintaining its existing assets but in growing organically and through M&A, such as with our Jamaican airports.

My principal message is that Pacifico has one of the highest dividend payouts [in Mexico] and that we’re always looking for additional ways to grow the business.”

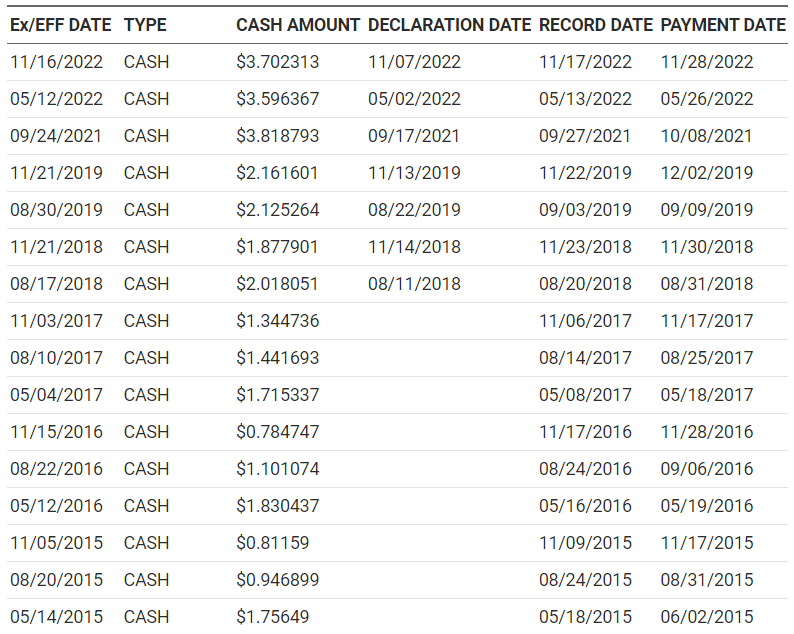

To that point on the dividends, Pacifico has been an incredible capital return story. The company pays a variable dividend, based on its free cash flow. While some investors may not appreciate the variability in said dividend, given the company’s long-running track record of compounded double-digit EBITDA growth, dividend increases have been frequent and significant:

Pacifico Dividend History (Nasdaq.com)

The company typically pays two dividends per year of a somewhat regular amount, along with a special dividend based on additional profitability for a given year. In the mid-2010s, the company tended to pay out around $3.50 per ADR share per year. This continued to increase until 2020, when the company suspended the dividend for obvious reasons.

In 2021, however, the dividend returned at nearly $4/share, which amounted to a rather strong yield for anyone that bought while shares were grounded during the pandemic. In 2022, the company’s dividend soared to more than $7/share thanks to the sharp upturn in traffic and profitability.

With 2023 traffic kicking off at a 33% growth rate in January, along with an upturn in the value of the Mexican Peso (and thus the value of dividend payments when converted to dollars) it wouldn’t be surprising if we see $9-$10 a share of annual dividends in the not-too-distant future. And, as management indicated, it is a priority for the company to increase the profitability of its assets so that the company can share more distributions with its holders.

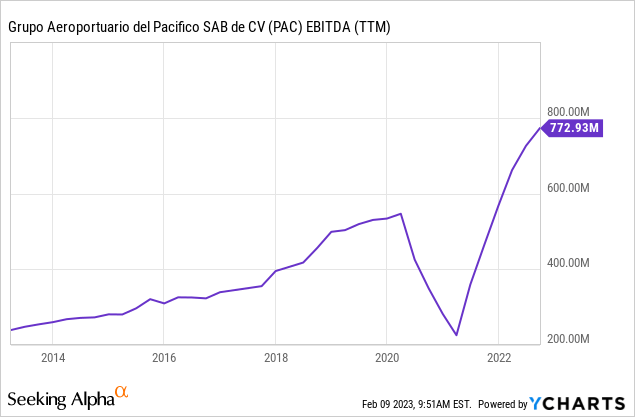

This sort of direct focus on shareholder returns is, in my experience, fairly rare among emerging market companies. When you combine that trait with the positive features of airports as an asset class, along with the boom we’re seeing in the Mexican economy, I’m sticking with my bullish call on Pacifico shares. Sure, the stock is up a lot. But on the other hand, so is profitability:

You won’t find many travel companies with a more agreeable V-shaped recovery in their earnings since 2020. And with the company’s traffic growth now accelerating to the upside — contrary to the prior expectations of a tourism-related slowdown — 2023 should be another excellent year for the company.

The Mexican airports have historically tended to run around 15x EV/EBITDA. Figure that Pacifico will be pulling in $1 billion of annual EBITDA in the near future given current traffic growth rates, and we’re looking at a $15 billion price tag for Pacifico overall, whereas the current enterprise value is still under $10 billion.

The stock is certainly up a lot from where it was trading 12 or 24 months ago. However, I think investors are underappreciating the profitability increases and sustained traffic growth occurring at the company, and in Mexico in general. The Mexican aviation industry didn’t just return to 2019 levels of activity and stop there.

Rather, Pacifico is now reporting numbers far in excess of 2019 levels with additional 33% year-over-year growth as of the latest update. This is what a combined tourism boom and major manufacturing buildout looks like, and the fundamentals are in place for Mexico to enjoy this sustained momentum for years to come.

Be the first to comment