Sundry Photography

As I reported in my previous Seeking Alpha articles, Akamai (NASDAQ:AKAM) long-ago began to leverage its legacy global CDN business in order to become a leading cybersecurity solutions provider to its existing customer base (see AKAM: Quickly Becoming A Cybersecurity Power). That being the case, I had been bullish on the company’s prospects going forward. However, in May of this year I changed my rating on Akamai from a BUY to a HOLD based on weak Q1 results and reduced guidance. Now that I have seen the Q2 results and forward guidance, I’m further downgrading AKAM to a SELL.

Investment Thesis

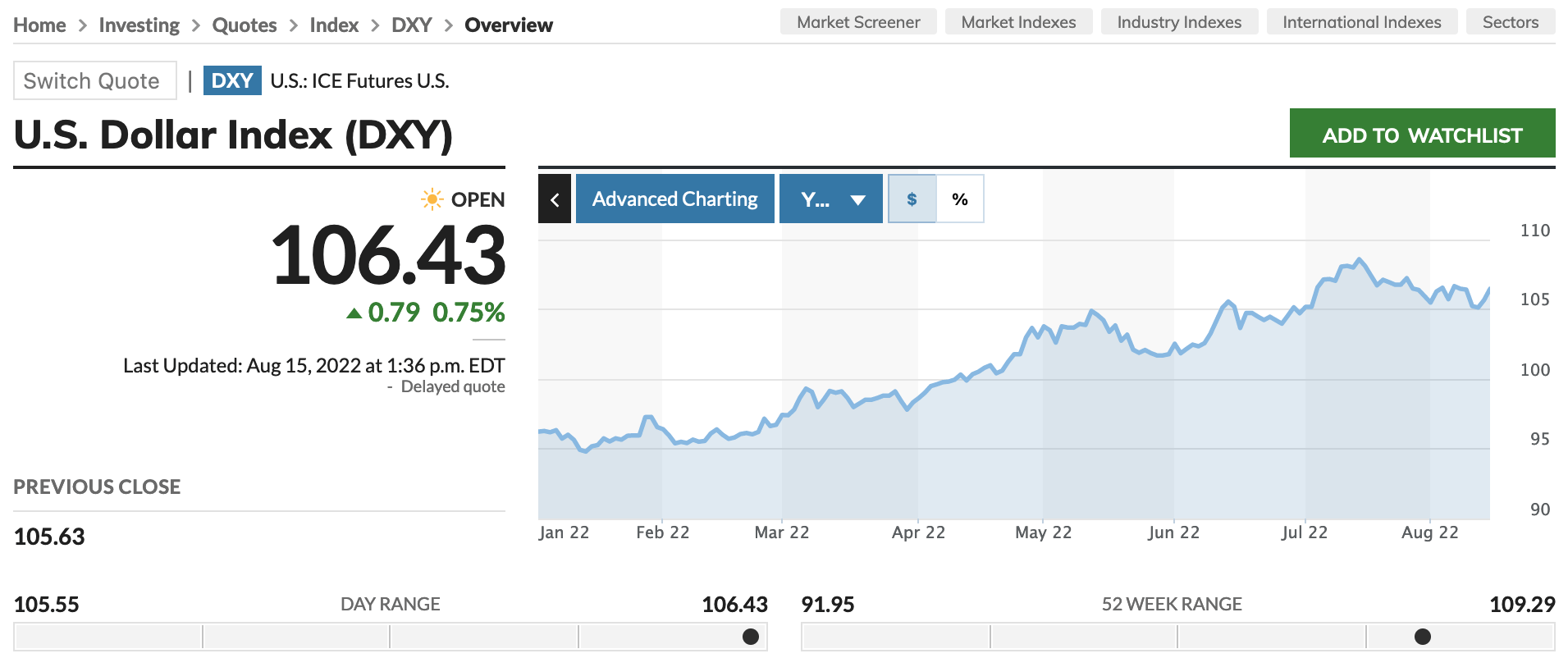

Given AKAM’s leading global CDN position, the company appeared to be ideally positioned to leverage those assets and its long-term relationships with content owners & content deliverers in order to become a leading cybersecurity solutions provider. And it is growing its cybersecurity business at a healthy-clip. However, the company’s CDN business is still its biggest business segment and deterioration is accelerating. In addition, in my earlier last analysis on Seeking Alpha – which I correctly identified potential foreign exchange risks, I failed to anticipate the extent to which Akamai’s global footprint would be exposed to FX stress as a result of a very strong U.S. dollar:

MarketWatch

Q2 Earnings

I reduced AKAM from BUY to HOLD after Akamai’s Q1 report which – despite strong cybersecurity results – was “ok” but forward guidance was reduced (see AKAM: Softening Business & Reduced Guidance). The Q2 EPS Report was released last week and – in my opinion – it was poor. Highlights were:

- Q2 revenue was $903 million, +6% yoy (+9% when adjusted for foreign currency headwinds).

- Q2 Security and Compute revenue of $487 million (+26% yoy, and +30% when adjusted for foreign exchange) was greater than CDN “delivery revenue” of $417 million, which was down 11% yoy.

- GAAP EPS of $0.74 was -21% yoy and -15% when adjusted for foreign exchange.

- Q2 GAAP net income was $120 million, -24% as compared to Q2 last year.

Delivery, AKAM’s largest business segment (and ~50% of revenue), is clearly taking a big hit from the global macro environment: revenue was -11%. AKAM has effectively no-moat to this business, so slowing media traffic and deflationary pricing (which has been happening for years), combined with FX headwinds to make very poor quarterly results. Meantime, it appears AKAM’s momentum in cybersecurity is beginning to decelerate as well.

Over the first 6-months of the year, adjusted EBITDA margin has declined by two full percentage points. Margin deterioration may be partly the result of challenges with the recent Guardicore & Lionde acquisitions. Regardless it doesn’t appear as though AKAM admirable and growing positions in cybersecurity and edge-computing are material enough to overcome continued deterioration of Akamai’s legacy CDN business.

As a result of the poor quarter and FX headwinds, management lowered FY22 guidance to 4% revenue growth at the midpoint (vs 5% previously) and an 8% EPS decline (vs 6 previously). As a result, consensus EPS estimates for Akamai have come down significantly across the board:

Yahoo Finance

Shareholder Returns?

Akamai spent $165 million in Q2 to repurchase 1.6 million shares at an average price of $100.80 per share. At pixel time, AKAM is currently trading at $96.27. It is noteworthy that, in Q1, Akamai spent $103 million to repurchase 0.9 million shares at an average price of $111.25 per share. And note that despite the $268 million AKAM spent on buybacks in Q1 and Q2, the fully-diluted share count has barely moved (161.7 million) due to employee stock compensation plan issuance.

Clearly AKAM’s stock repurchase plan has reached a point of diminishing returns for ordinary shareholders.

Risks

I suppose it is possible that oil prices (and thus inflation) could come down significantly and reduce the potential for future Federal Reserve interest rate increases. But I doubt the Fed is done hiking, and as a result the U.S. dollar is likely to remain strong. In addition, note that just today China cut two key interest rate benchmarks. That being the case, I don’t see AKAM’s FX headwinds changing for the better any time soon.

Big cloud providers like Microsoft (MSFT), Google (GOOG), and Amazon (AMZN) are developing competing CDNs within their own public cloud offerings. That is why I said earlier that AKAM’s CDN business has “no moat” and is ripe to lose market share.

Despite already lowered guidance, I still see downside risks to struggling Akamai in terms of even worse CDN deterioration going forward, decelerating cybersecurity growth, and continued FX headwinds.

Summary & Conclusions

Akamai is a SELL. Cybersecurity is not growing fast enough to make-up for Akamai’s legacy and deteriorating CDN business. In addition, FX headwinds lopped a full 3% off top-line revenue in Q2. Further, the Akamai management team has spent $268 million on share buybacks at prices significantly higher than the current stock price. Not only is that likely to continue throughout the remainder of the year, but note that despite over a quarter-million dollars spent on buybacks, he fully diluted outstanding share count is relatively unchanged due to employee stock compensation.

Don’t get me wrong, I am not advising investors go short the stock, Akamai is still a very profitable business and the forward P/E of ~18x isn’t an exhorbitant valuation level. But I certainly wouldn’t buy AKAM here, and all things being equal (taxes, etc.) I suggest current shareholders SELL their shares. The outlook is muddied at best and in my opinion what FCF the company is generating is being wasted on share buybacks instead of giving ordinary shareholders a fair shake via a decent dividend. That being the case, I just feel there are better places to invest.

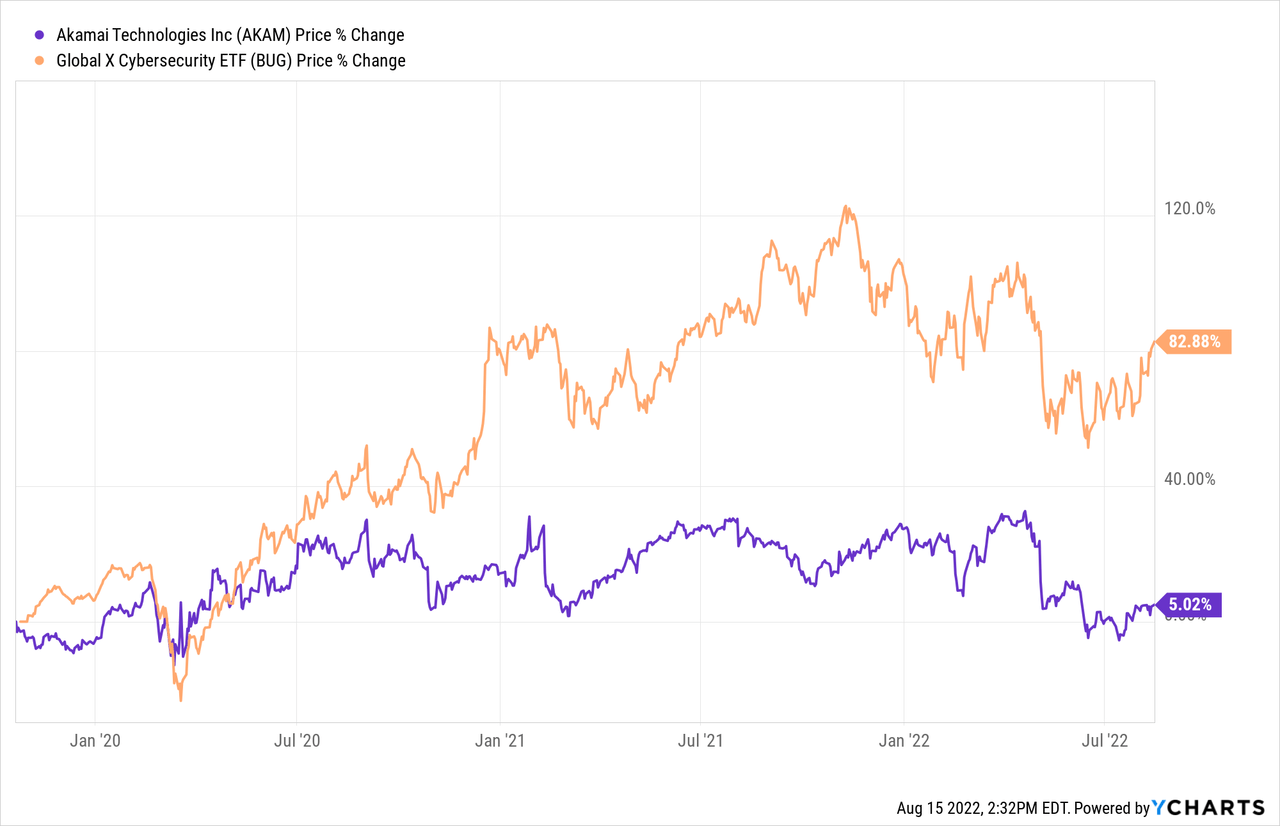

As long as cybersecurity is remains the primary investment thesis for Akamai, investors should instead consider investing in leading pure-play companies like Palo Alto Networks (PANW), Crowdstrike (CRWD), or ZScaler (ZS) – none of which have the CDN boat-anchor tied around their necks. Or, for a more diversified approach to the cybersecurity thesis, consider the Global X Cybersecurity ETF (BUG) – see BUG: No Stopping The Leading Cybersecurity Companies.

I’ll end with a three-year chart (that encapsulates both the recent bull and bear markets) comparing AKAM with the BUG ETF:

Be the first to comment