visualspace

If you want to know what your house is worth, you can put it up for sale and see what you can get. An easier, and less disruptive, way to determine value is to see what your new neighbors paid. A recently announced transaction might provide some insight into market values for South Florida multifamily properties.

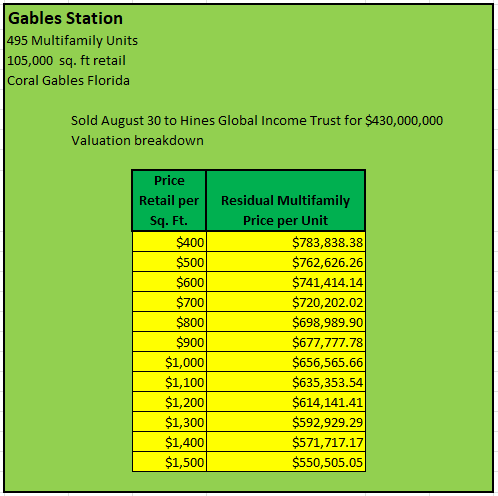

The Real Deal recently reported that Hines Global Income Trust on August 30th completed a $430MM purchase of the 495 apartment unit Gables Station. At first glance, a $430MM acquisition price translates to a whopping $870k per apartment key, but as a 2022 mixed-use development, there is more to consider with this property.

Nolan Reynolds International

In addition to the 495 apartment units, Gables Station includes 105,000 sq. ft. of commercial space occupied by an athletic club, co-working space, a Trader Joe’s, and an Italian restaurant. If we do a simple break out of the commercial space at various valuations, we can get some ballpark ranges for the pricing of the multifamily portion.

2MCAC

Pricing the commercial space in the broad range of $400 to $1,500/square foot and subtracting that from the total transaction price still yields a price ranging from $550k to $780k per apartment unit. While we don’t have a financial interest in either the buyer or the seller of this property, a quick trip to Portfolio Income Solutions’ Property Directory will tell us who owns multifamily property in the neighborhood, and we can start speculating about what those properties might be worth.

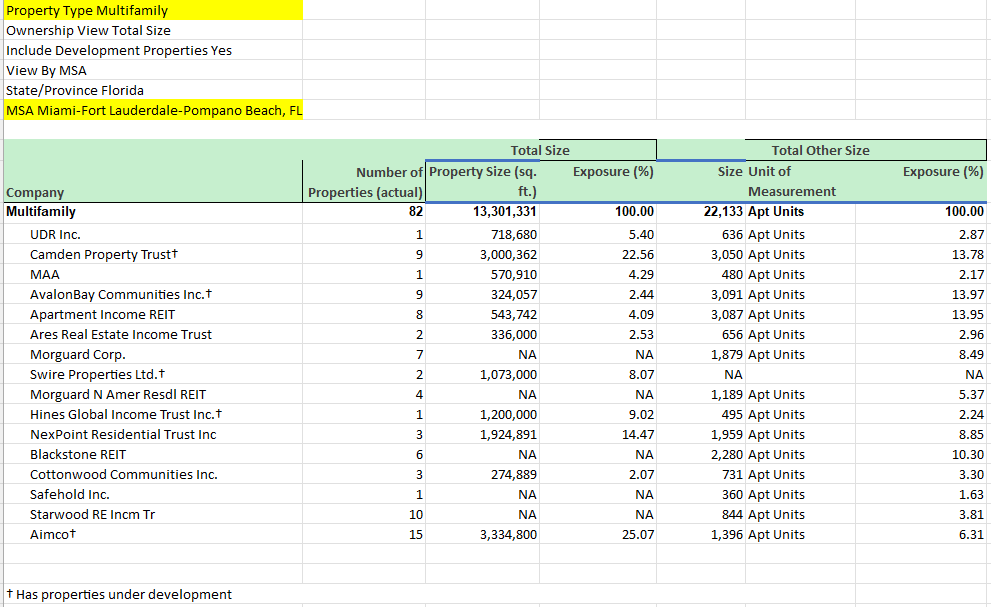

Multifamily in the Miami MSA

In screening for multifamily properties owned by public companies in the Miami-Fort Lauderdale-Pompano Beach MSA, we see 82 properties with a total of more than 22,000 apartments. The data appears to be up to date in that Hines Global Income’s August 30th purchase is on the list.

Portfolio Income Solutions

From a key count perspective, Camden Property Trust (CPT), AvalonBay Communities (AVB), and Apartment Income REIT (AIRC) have the most exposure with more than 3,000 apartments each. But these are larger companies, and the Miami MSA exposure is small relative to each of their entire portfolios.

At 1,396 Miami area units, however, the $1.4B market cap Aimco (NYSE:AIV) is a much more interesting comparison to the Gables Station transaction. All in, AIV has 2,896 apartments in the state of Florida, fully 30% of its entire portfolio. While Miami pricing isn’t representative of all of Florida, the in-migration and job creation is the demographic enjoyed state-wide. So, for the transaction at hand, AIV should prove the most illustrative comparative example.

Table by 2MCAC, Data from S&P Capital IQ

Valuing Aimco

After spinning off AIRC at the close of 2020, Aimco stopped looking like or behaving like a multifamily REIT. They ceased paying a dividend. They stopped reporting in terms of FFO/share. They stopped hosting quarterly earnings conference calls. Though they have not stated their preferred pronouns, AIV is no longer a REIT, it looks a lot more like a REOC. Based on its operations, AIV has evolved to become an opportunistic player in the often-exciting realm of multifamily development.

From AIV’s 2Q22 earnings and supplemental report:

Aimco CEO Wes Powell:

“During the year we sold two stabilized multifamily assets above the values used in our internal Net Asset Value (“NAV”) estimate and also added multi-phase development opportunities in South Florida and Washington, D.C. Through opportunities directly sourced by the Aimco team, our future development pipeline has nearly tripled since the start of 2021, and now, in total, has the potential for more than 15 million square feet of residential and mixed-use development.”

Specifically, “In May, Aimco sold Pathfinder Village, a 246-unit apartment community located in Fremont, California, for $127.0 million. Proceeds, net of the repayment of the existing property debt and transaction related costs, were $71.8 million.” The Freemont, CA apartments sold for $516k/unit- well below the bottom estimate for the Miami property sale.

“In July, subsequent to quarter end, Aimco sold Cedar Rim, a 104-unit apartment community located in Renton, Washington, for $53.0 million. The property was owned free and clear of debt prior to the sale.” Renton, WA doesn’t bring the heat of the Miami market, but, still, $510k/unit!

And then, “Aimco is under contract to sell 2900 on First, a 135-unit apartment community with 14,000 square feet of retail located in Seattle, Washington for $69.0 million. This sale of this property is expected to close in August” Again, $511k/unit.

What we see in these transactions is that AIV turned what may have been accurately described as real estate speculation into real market, real world, full cycle trading profits. They follow on with the aforementioned development pipeline that has nearly tripled since the start of 2021.

The Value Proposition

Over the last five years, many apartment-centric REITs have reported successes comparable to AIV’s detailed above. They developed/acquired/rehabbed properties which they then sold for a profit and recycled capital into new opportunity. AIV went two steps further to come closer to delivering full shareholder value.

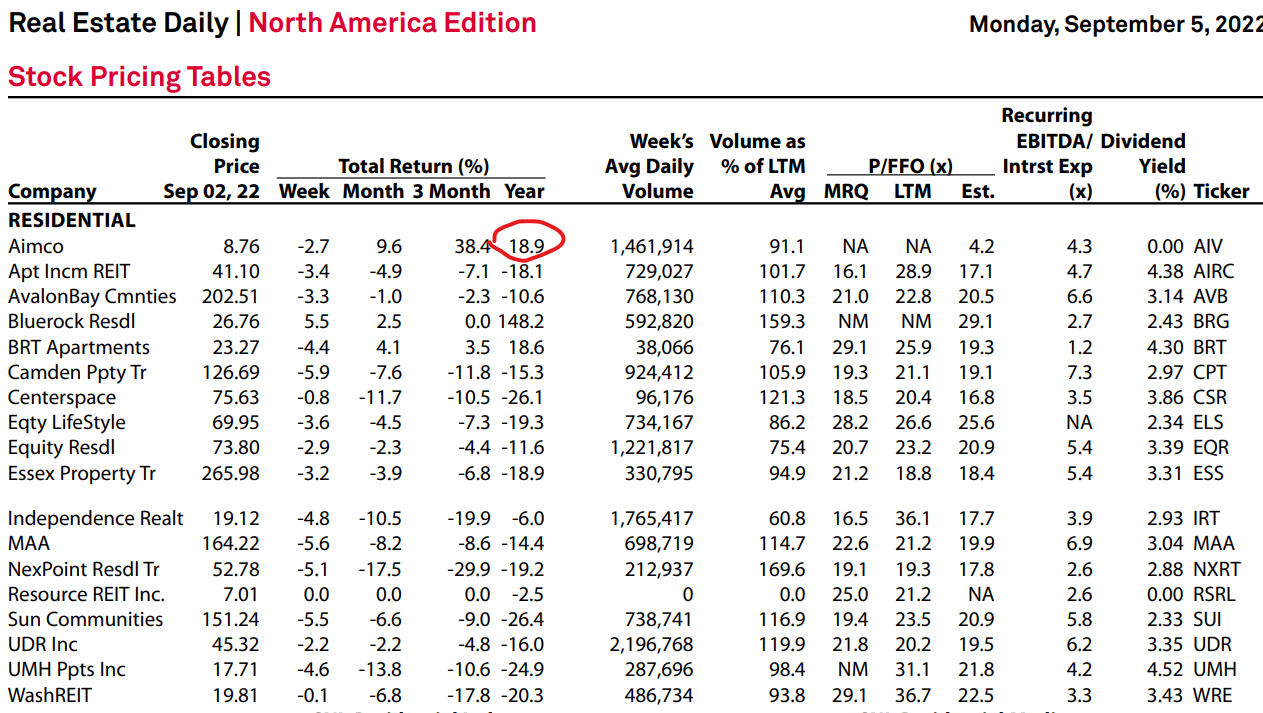

In the table below, please focus on total returns over the last year. We see Aimco turning in an impressive +18.9% while the balance delivered negative returns of an equal magnitude.

S&P Capital IQ

Month-by-month, apartment rents have soared to new levels, and that translated to record NOI growth. Somehow though, REIT investors displayed a collective anxiety and three years’ share price appreciation evaporated in the first eight months of 2022. Operationally, multifamily REITs are performing very well, but it really hurts if you happen to be long the shares.

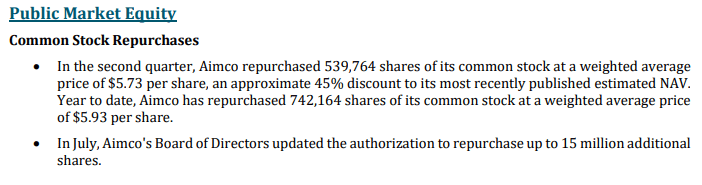

AIV seems to have avoided this decline and I think two active initiatives are responsible for the result. First, Aimco has asserted its share buy-back program.

AIV

You can see that the $5.73 to $5.93 weighted average purchase prices are not only a huge discount to recently published NAV, but also to their recent market closing price of $9.00. AIV continues to recycle capital back in to promising new development, but they have also actively pursued the accretion that presents itself in the repurchase of their own, heavily discounted shares.

The second effective initiative of delivering value to shareholders comes in the form of securing long horizon capital. While other REITs have succumbed to the whims of retail investors who soil themselves every time they hear the Fed might raise interest rates, AIV on August 11 announced a joint venture agreement with Alaska Permanent Fund Corporation for up to $1 Billion new multifamily development. If I understand the historical behavior of institutional investment, Aimco will still be investing Alaska Permanent Fund money even if our fear of recession becomes a real recession.

Buy, Sell, or Hold?

While I am long an AIV holding that is large enough to keep my attention, I confess that I wasn’t prescient enough to buy below $6.00 like the company stock repurchase program did.

I think our property transaction exercise demonstrated that while AIV share prices are up, the shares may still be trading at a discount to their NAV. Share prices of other multifamily REITs that own assets in the same submarkets as AIV are down 15%, 20%, even 25% YTD. I own some of them and, optimistically, feel they have a greater going forward potential than AIV.

Be the first to comment