thamerpic

Over 2022, the Mare Evidence Lab team provided various publications about the Swiss insurer Zurich Insurance Group (OTCQX:ZURVY). Below are our previous analyses to get acquainted with the narrative up to now:

- 19/01/2022: 10-year analysis on Zurich Insurance’s main financial indicators plus a comment on the Italian optionality thanks to the latest acquisition of Deutsche Bank Italian network of Financial Advisors;

- 12/05/2022: comment on the company’s Q1 results;

- 08/04/2022 – 16/06/2022: Mare Evidence Lab analysis on the company’s exposure in Russia. Since April, we upgraded Zurich with a buy rating at CHF 475 per share mainly due to: a higher margin on the P&C division, lower claims on the Farmer division, better synergies on the MetLife acquisition, immaterial exposure to Russia, safe haven currency coupled also with a strong balance sheet.

Half-year Results

We cannot avoid reporting some of the CEO’s comments: “the company reported the highest first-half business operating profit since 2008 and the second highest ever” adding also that they: “are on track to beat all targets for the second successive three-year cycle. This is particularly remarkable because the last three years have brought unprecedented and unexpected challenges”.

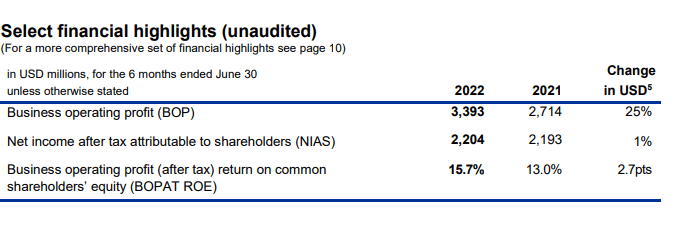

Numbers in hand, the operating profit result was up by +25% to $3.393 billion compared to the first semester of 2021. Double-checking the consensus gathered by the company, it was foreseen to amount at $3.28 billion. Moreover, this is the highest figure since 2008. More specifically, the Non-Life business operating profit rose 32% to $2.055 billion with a combined ratio of 91.9%, an all-time low, thanks to higher prices and fewer natural disasters. Life business operating profit also improved by double-digit 13% to reach $903 million. Despite the adverse effects of the financial markets, the group’s net income was also up by 1% against the same period last year.

Zurich financial snap

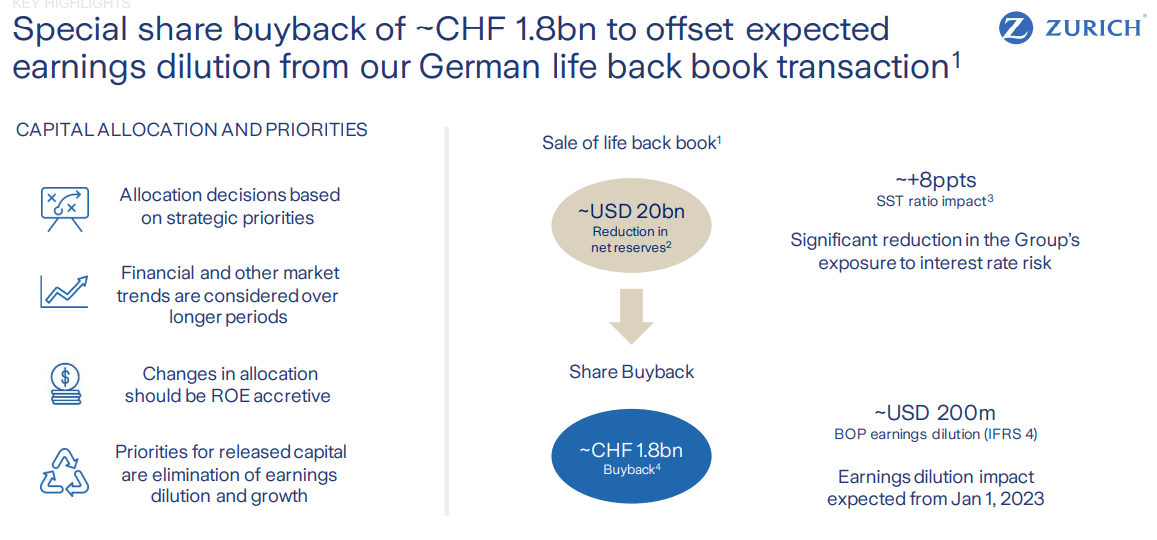

In the coming months, the company will launch a buyback of approximately CHF 1.8 billion to offset the expected dilution of earnings resulting from the German back book sale. This is higher than our internal estimates. The CEO assured the investor community that the share repurchase will not affect the company’s dividend policy.

Zurich Buyback

Conclusion and Valuation

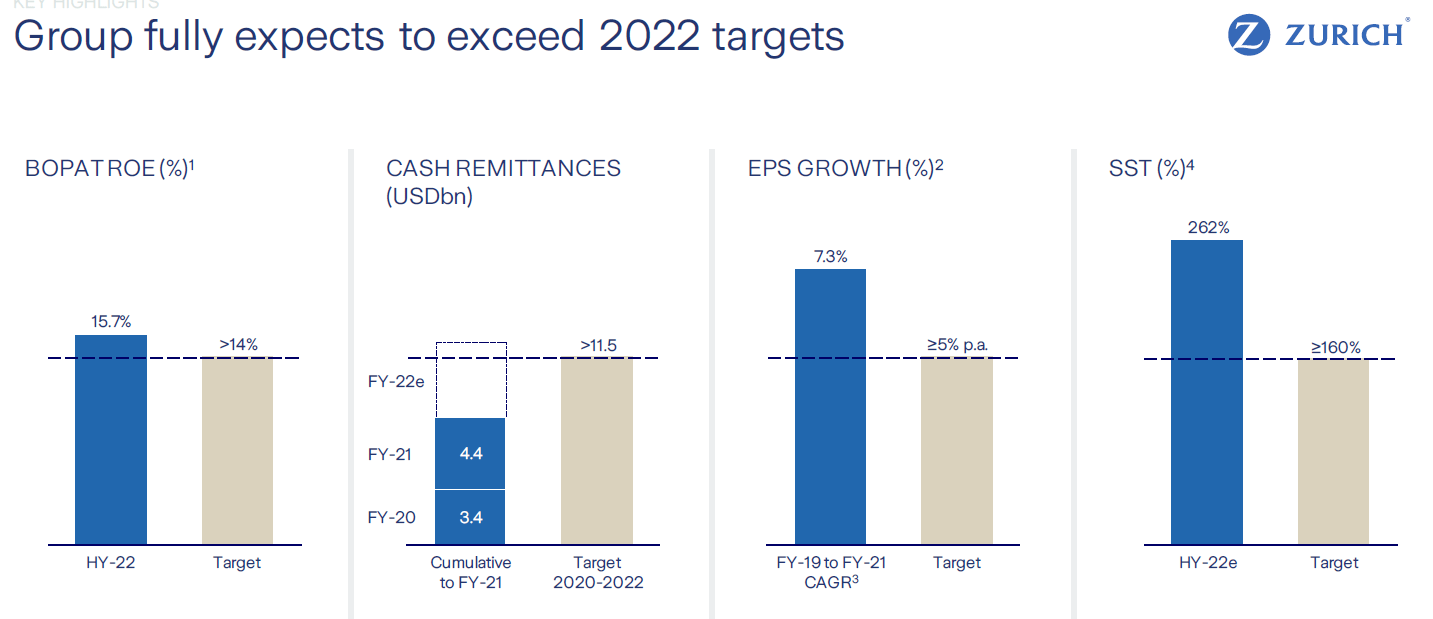

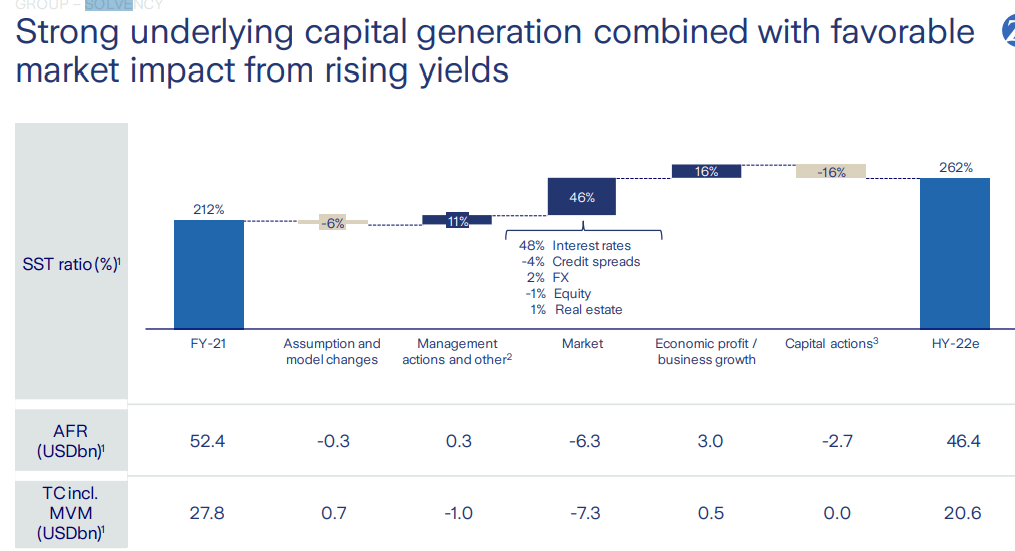

During the call, the CEO reported strong commercial pricing power well ahead of cost trends. Zurich anticipated the beating of all the internal targets. Indeed, the ROE is comfortably higher than the 14% guidance as well as the EPS growth. It is worth highlighting the strong performance achieved at the Solvency II Ratio level. This unbelievable result (262%) was mainly driven by the hedging policy that the company anticipated versus the higher interest rate environment.

Zurich targets

Solvency II Ratio evolution

Given the strong capital position and cash flow generation, the management is not prioritizing inorganic acquisition and is looking for organic growth. We should note that Zurich recorded an increase in new retail customers of approximately 850k in the first semester. However, during the Q&A call, the CEO said that they have the financial flexibility to execute acquisitions wherever there may be an opportunity.

The next catalyst is Investor Day in November when Zurich will present its next three-year plan (we might expect a higher dividend per share growth in the coming years). After these outstanding results, our internal team expects to see earning upgrades in line with our valuation. Here at the Lab, we based Zurich’s valuation on a sustainable ROE reaching a target price of CHF 475 per share.

Q2 results of our European insurers’ coverage:

Be the first to comment