da-kuk

Thesis

Virtus Total Return Fund (NYSE:ZTR) announced yesterday the results of its rights offering:

Virtus Total Return Fund Inc announced today that it has issued 20.3 million shares of common stock pursuant to its recently completed non-transferable rights offering. Total net proceeds of the rights offering, which are estimated at approximately $140.6 million after deducting for estimated offering expenses, are expected to be invested throughout the Fund’s equity portfolio. Net proceeds were calculated based on a share subscription price of $6.96, which equaled 95% of the average of the last reported sales prices of the Fund’s common shares on September 16, 2022, the pricing date of the offering, and the four preceding business days.

These are absolutely great results for ZTR. Let us have a look:

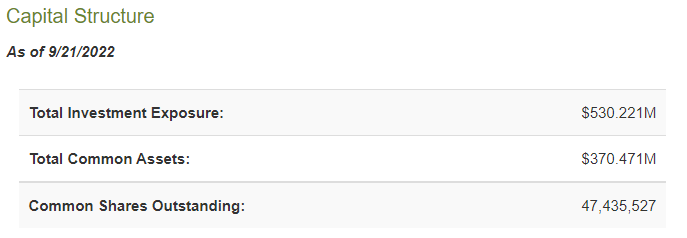

Capital Structure (CefConnect)

We can see from the capital structure pre-issuance that the fund has unleveraged assets totaling $370 mm and around 47k shares. The rights offering basically expanded the asset base by a whopping 40% ! That gives a prospective investor a number of take-aways:

- Investors are realizing how attractive raising cash in this environment is for a CEF

- The investor community views the rights offering and the AUM increase as a very positive development

- In today’s environment CEFs that do rights offerings are emblematic of smart management plays and are rewarded by investors with large share take-outs

To put this in context for a retail investor – prior to the rights offering ZTR was a fully invested CEF with leverage on top. Now ZTR is a CEF sitting on a cash trove amounting to 40% of its unleveraged base and is in an absolutely enviable position to deploy that cash and purchase assets during a bear market when asset prices are at discounts.

What will the end result of this cash raising exercise be? A substantial outperformance in 2023 and longer term. ZTR’s management spoke around this topic:

We see attractive investment opportunities across all sectors of global infrastructure, particularly with the ongoing transition to a clean energy economy and the significant need for continued investments in these essential infrastructure services,” said Connie Luecke, CFA, co-portfolio manager of the Fund and senior managing director, Duff & Phelps Investment Management Co. “We also see global infrastructure as a good defensive strategy in a volatile market because the sector may provide downside protection and diversification within an investor’s larger portfolio due to infrastructure’s historically lower correlation with most other equities and bonds.

We cannot overemphasize the importance of having fresh capital to deploy in this environment. 2022 has seen the worst bond market returns on record and has seen the S&P 500 index down -20% and about to embark on another leg down. Will 2023 be as bad? We do not think so. Being able to have cash to deploy at the lows is a gold mine so to speak in today’s environment, and the investor base has realized this:

Sufficient common shares were available to honor all over-subscription requests in full. Refunds for overpayments are expected to be mailed beginning today. Confirmation statements are expected to be mailed to fund shareholders beginning on September 23, 2022.

Holdings

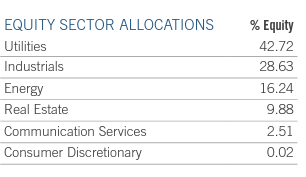

The fund strives to have approximately 60% of its allocation to equities. The fund invests in owners and operators of infrastructure in the communications, utility, transportation, and energy industries that have sizable market caps:

Allocations (Fund Fact Sheet)

Very similarly to the DNP fund, the manager allocates a very high percentage of the equity allocation to the “Utilities” sub-sector. In terms of individual names the top holdings of the fund currently shape up as follows:

Top Holdings (Fund Fact Sheet)

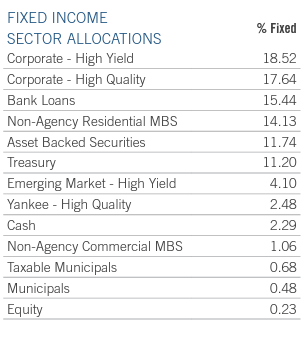

On the fixed income side the fund invests in high yield bonds and leveraged loans mainly:

Fixed Income Parsing (Fund Fact Sheet)

There are buckets for investment grade bonds, non-agency RMBS and some asset backed securities (ABS), but kindly keep in mind that the above percentages represent the “% Fixed Invested Assets”.

Conclusion

ZTR is a 60/40 CEF with an infrastructure focus on the equity side. The fund just announced the results of its rights offering which saw its unleveraged asset base increase by almost 40%. These are great results for the fund’s investors because the vehicle is now sitting on a very large cash allocation which it can use to buy assets at distressed levels during the current bear market. We reiterate our Buy rating on the CEF.

Be the first to comment