Just_Super

Zscaler (NASDAQ:ZS) is a cloud native network security vendor that protects both incoming and outgoing traffic. They provide customers with a scalable solution that does not require investments in hardware, a potentially attractive value proposition in the current environment. While the company has secular tailwinds and a strong competitive position, moderating growth and a lack of profitability have been weighing on the stock. Current difficulties are likely to prove temporary though, and with a more reasonable valuation, the stock should do well going forward.

Products

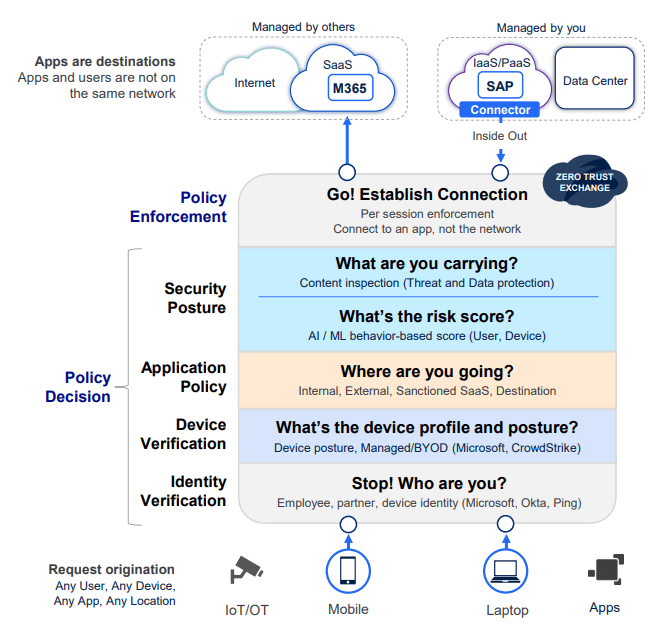

Zscaler provides network security solutions which protect incoming and outgoing traffic, utilizing their own their own global network, across 150+ data centers, which serves as a gateway between the user and the service being requested. Zscaler takes a zero-trust approach to security and aims to reduce the attack surface, stop lateral movement and prevent data loss. Protection is also provided by working with partners like Okta (OKTA) and CrowdStrike (CRWD) to verify identity and ensure device posture.

Figure 1: Zscaler Zero Trust Exchange Architecture (source: Zscaler)

Zscaler Internet Access (ZIA) is a security service edge solution that replaces legacy network security solutions. ZIA secures outgoing traffic, helping to stop attacks and prevent data loss with a zero-trust approach that includes:

- Secure Web Gateway

- Cloud Access Security Broker

- Data Loss Prevention

- Firewall and IPS

- Sandbox

- Browser Isolation

- Digital Experience Monitoring

- Zero Trust Network Access

Data loss prevention continues to be an area of innovation for Zscaler and their offerings are gaining traction with customers. Zscaler’s DLP service provides auto classification of unstructured data to expedite deployments with zero configuration.

Zscaler also acquired ShiftRight in 2022 to integrate security automation workflow technology into their zero-trust platform. The combination of ShiftRight with Zscaler’s DLP solution enables organizations to automate security management and reduce incident resolution times.

Zscaler Private Access (ZPA) is a zero-trust access system for incoming traffic. This provides users with secure access to private apps, services, and OT devices from anywhere, similar to the functionality provided by a VPN.

Zscaler Digital Experience (ZDX) makes it easier for organizations to find and resolve IT issues. ZDX is a natural fit for Zscaler as it utilizes the same endpoint agent as their other services. The product has quickly gained traction with customers and could be a growth area going forward. Cloudflare (NET) recently launched a similar solution.

Zscaler also offers Posture Control through Zscaler for Workloads to help organizations secure their cloud native applications. Posture Control is an agentless cloud native application protection platform (CNAPP) solution which correlates across multiple security engines to prioritize hidden risks caused by misconfigurations, threats, and vulnerabilities. CNAPP helps teams build, deploy, and run secure cloud native applications in public cloud environments. CNAPP also helps to consolidate CSPM, CIEM, IAM, CWPP, data protection, and other capabilities.

Figure 2: Zscaler Zero Trust Platform Offerings (source: Zscaler)

Recessionary Tailwind

While demand for IT services softened significantly in 2022, driven by a post-COVID normalization and recessionary fears, Zscaler is potentially better positioned for this situation than most. Zscaler can reduce costs for customers by eliminating the need for products like security appliances, routers, switches, load balancers, etc. There are also network costs and operational costs that Zscaler can help to reduce. Based on customer studies, Zscaler believes it takes one fifth the resources of a traditional firewall-based solution to manage Zscaler. In an environment where budgets are tight, Zscaler could be a relatively attractive option, particularly as organizations look to consolidate vendors.

Competitors

While Zscaler faces a number of highly successful competitors, management seems confident that their solution is differentiated and favorably positioned relative to key competitors. Palo Alto Networks (PANW) is currently an investor favorite, and they have been marketing themselves as the clear leader in the SASE market, although this is not really supported by independent reviews. Zscaler has suggested that Palo Alto’s architecture leaves them at a disadvantage, and that at the high end of the market firewall vendors are not competitive as sophisticated buyers know what they want. Bolting on solutions through acquisitions has allowed Palo Alto to quickly develop their capabilities, but it is unclear whether this approach will be able to compete against platforms built from the ground-up internally in the long run.

Amongst smaller customers, Zscaler competes with a number of vendors, including firewall companies and Cisco (CSCO) Umbrella. This is a segment that Zscaler has not focused on in the past but they have increased their presence over the past two years. While Gartner considers Netskope a SASE leader, Zscaler believes they are still predominantly a CASB vendor. Zscaler has said that they don’t really see Netskope much on enterprise deals but they are present at the low end of the market.

Competition also varies by use case:

- Proxy vendors (outbound traffic) – Websense, Blue Coat, Symantec and McAfee were competitive in the on-premises market, but moving to the cloud with a multi-tenant architecture is not straight forward.

- Private access (inbound traffic) – VPN vendors like Pulse Secure and Cisco have been key vendors in the past.

Financial Analysis

Zscaler is facing a softer demand environment, and this is beginning to impact growth. Customers are now more price sensitivity and there are more negotiations around deals, although there is no undue pressure on pricing. The financial, federal services and healthcare verticals unsurprisingly performed well in the most recent quarter. It is likely that weakness is being driven by verticals like CPG and tech, and hence a stabilization or recovery in these markets would be positive for Zscaler. Zscaler’s CFO recently suggested the current downturn was going to be tougher than 2001 or 2008, which could be hyperbole or may indicate they expect conditions to get much worse.

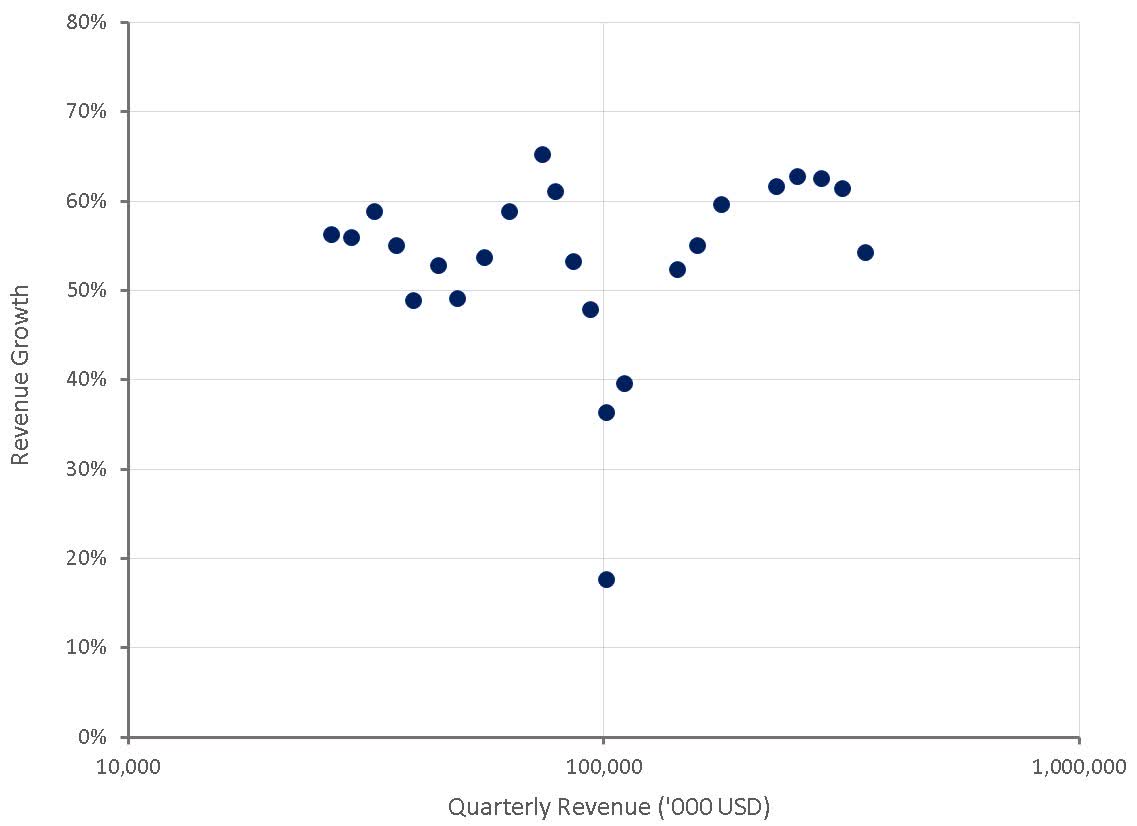

Revenue growth is expected to be 42-43% YoY in the second quarter, indicating that further deterioration in growth is expected going forward. This is being driven by the macro environment though, rather than Zscaler’s size. Zscaler still believes that they have a 72 billion USD market opportunity which they have only just begun to address. Outside of macro events, Zscaler has so far shown no signs of growth deterioration that would indicate they are reaching market saturation. Rather, growth has likely been constrained by the size of Zscaler’s salesforce and inertia in customer buying behavior. While growth could deteriorate significantly in the near term, particularly if there is a recession, growth is also likely to rebound when macro conditions improve.

Figure 3: Zscaler Revenue Growth (source: Created by author using data from Zscaler)

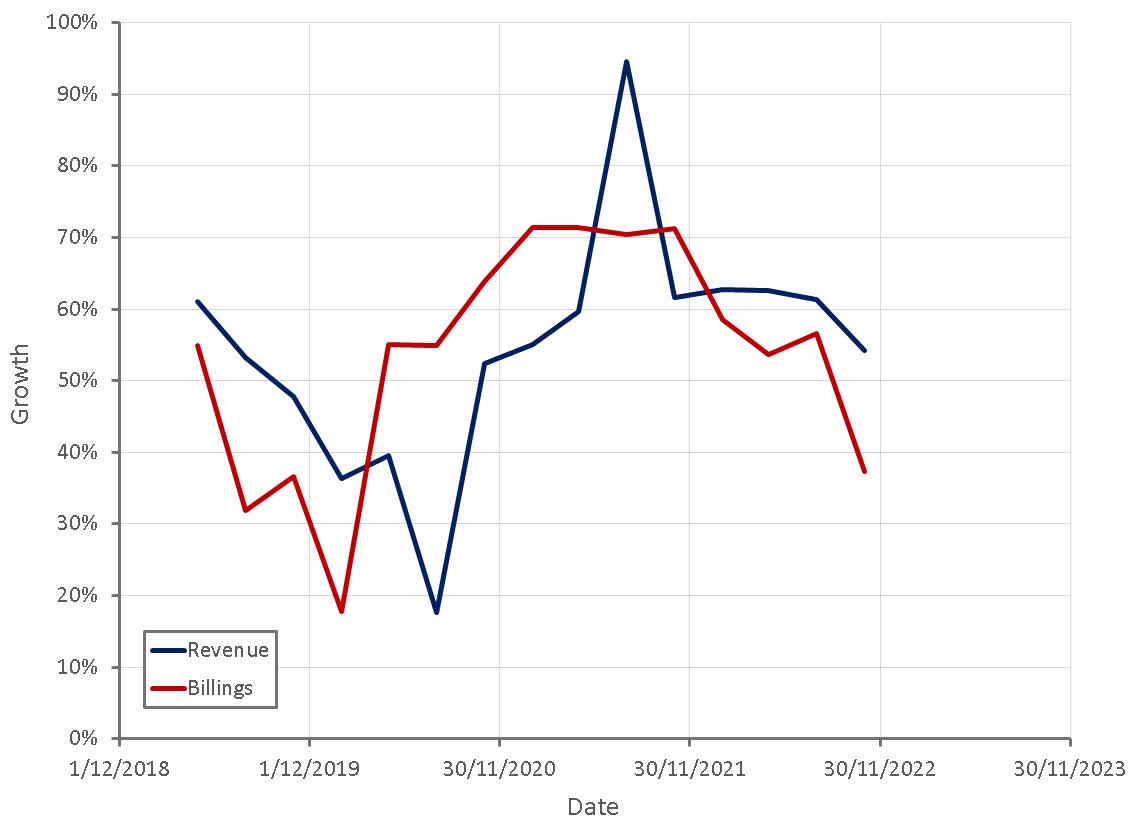

A further deceleration in growth is supported by Zscaler’s billings, which tend to lead revenue.

Figure 4: Zscaler Billings Growth (source: Created by author using data from Zscaler)

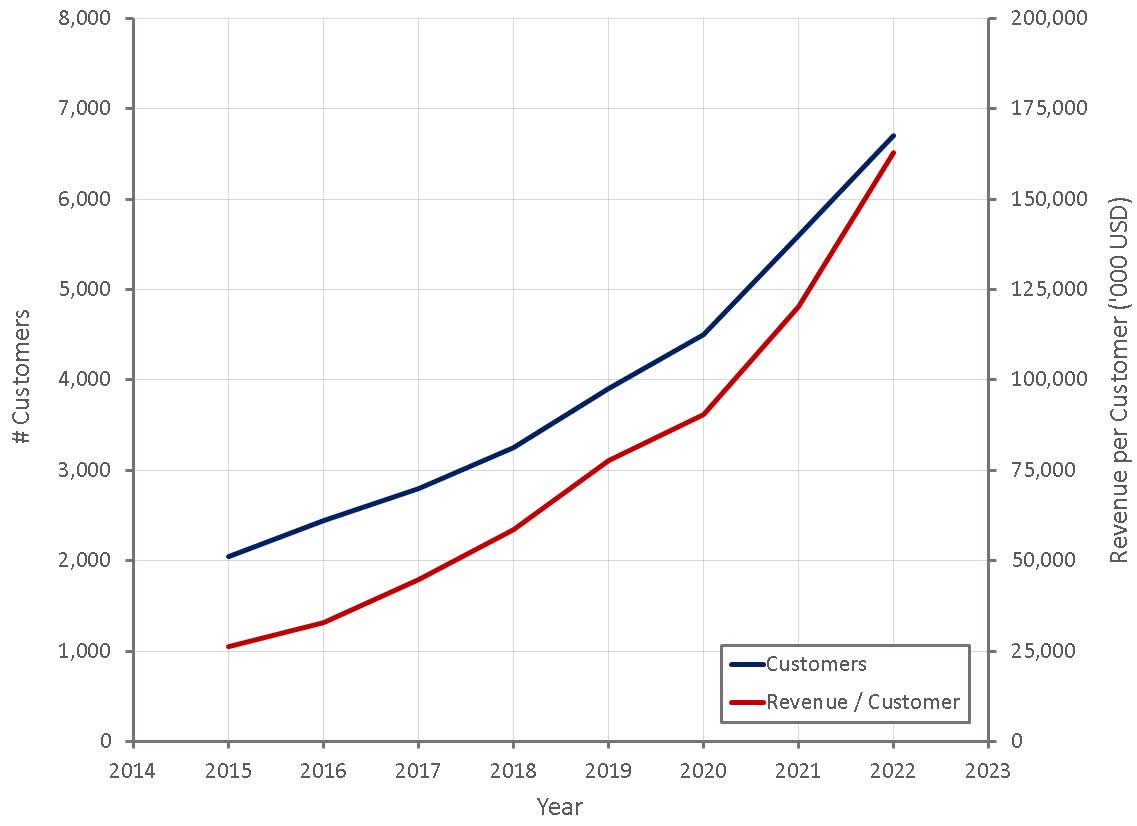

Growth is supported by both solid customer acquisitions and a net retention rate that has exceeded 125% for the past eight quarters. The growth split between new customers and upsell was close to even in the first quarter. Zscaler expects this to be more like 40% new customers and 60% upsell in FY2023, which assuming expansion deteriorates somewhat probably points to mid-30s growth.

Zscaler’s ability to drive expansion within existing customers is one of the most impressive aspects of the company. Despite an increased focus on smaller customers, average revenue per customer continues to increase rapidly. This is likely due to the platform approach gaining traction and high customer satisfaction. The trend towards vendor consolidation and a platform approach to security is leading to more large, multi-year, multi-pillar opportunities than ever before. Zscaler’s Net Promoter Score also continues to exceed 70, which is more than two times the average NPS for SaaS companies.

Figure 5: Zscaler Customers (source: Created by author using data from Zscaler)

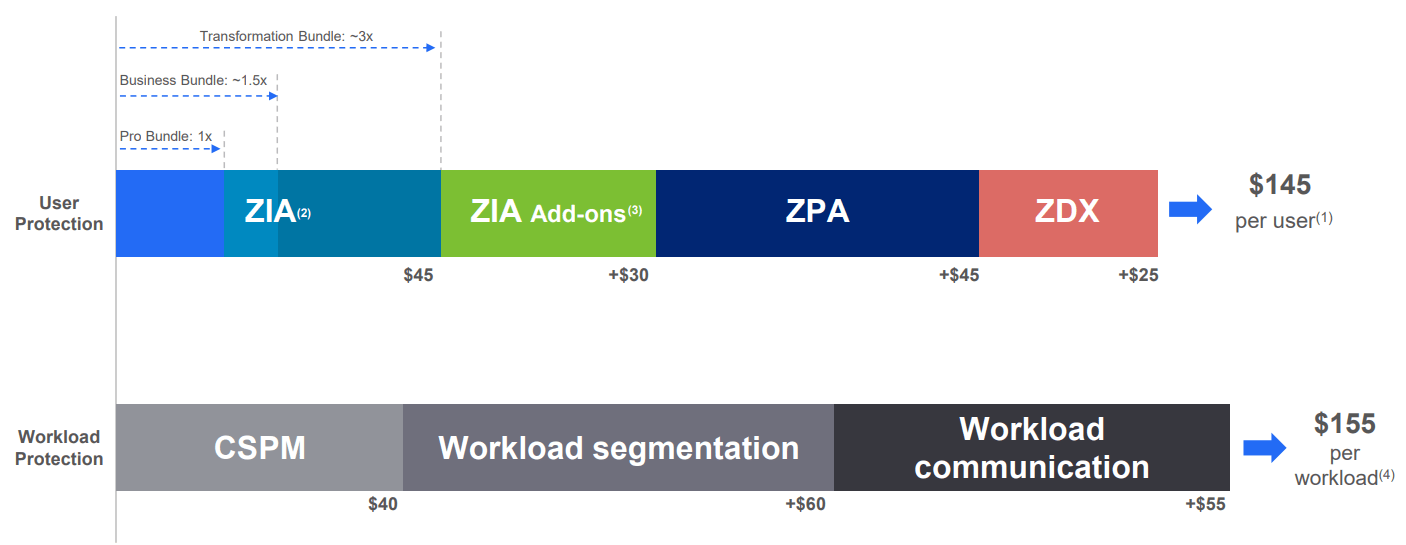

Zscaler is now able to offer a wide range of solutions, and can increase customer spend by offering more services and protecting more users / workloads. Zscaler believes they have a 6x upsell opportunity within their existing customer base, just for their core ZIA and ZPA products.

Figure 6: Zscaler Expansion Opportunities (source: Zscaler)

Large customer growth has been fairly solid recently, although it weakened in the most recent quarter. Zscaler already has a commanding presence across larger organizations, counting 40% of the Fortune 500 and 30% of the Global 2000 as customers.

Figure 7: Zscaler Customer Additions (source: Created by author using data from Zscaler)

Zscaler has the scope to increase revenue significantly by expanding within their existing large customers and moving down market. Based on employee numbers, the commercial segment could offer the largest TAM for user protection and Zscaler likely has little current presence in this segment.

Figure 8: Zscaler Customer Segments (source: Zscaler)

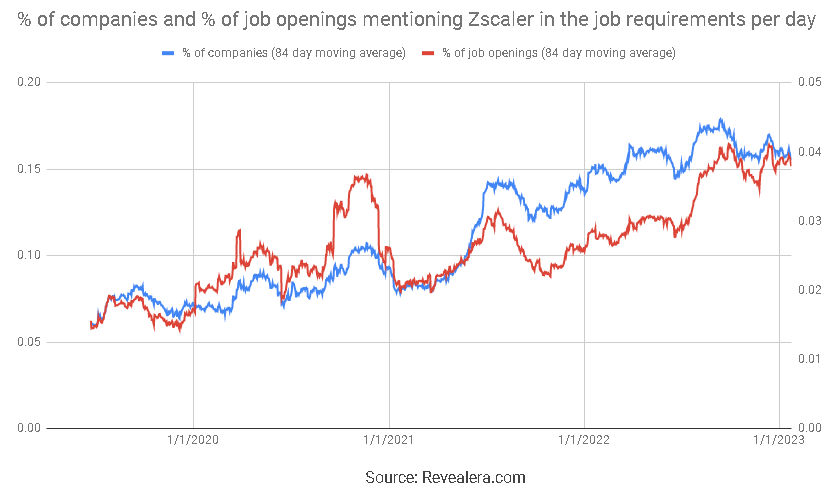

The number of job openings mentioning Zscaler in the job requirements has increased steadily over the past few years, and unlike many peers has so far shown little weakness. This could be due to Zscaler’s relatively low market penetration and low exposure to the SMB segment.

Figure 9: Job Openings Mentioning Zscaler in the Job Requirements (source: Revealera.com)

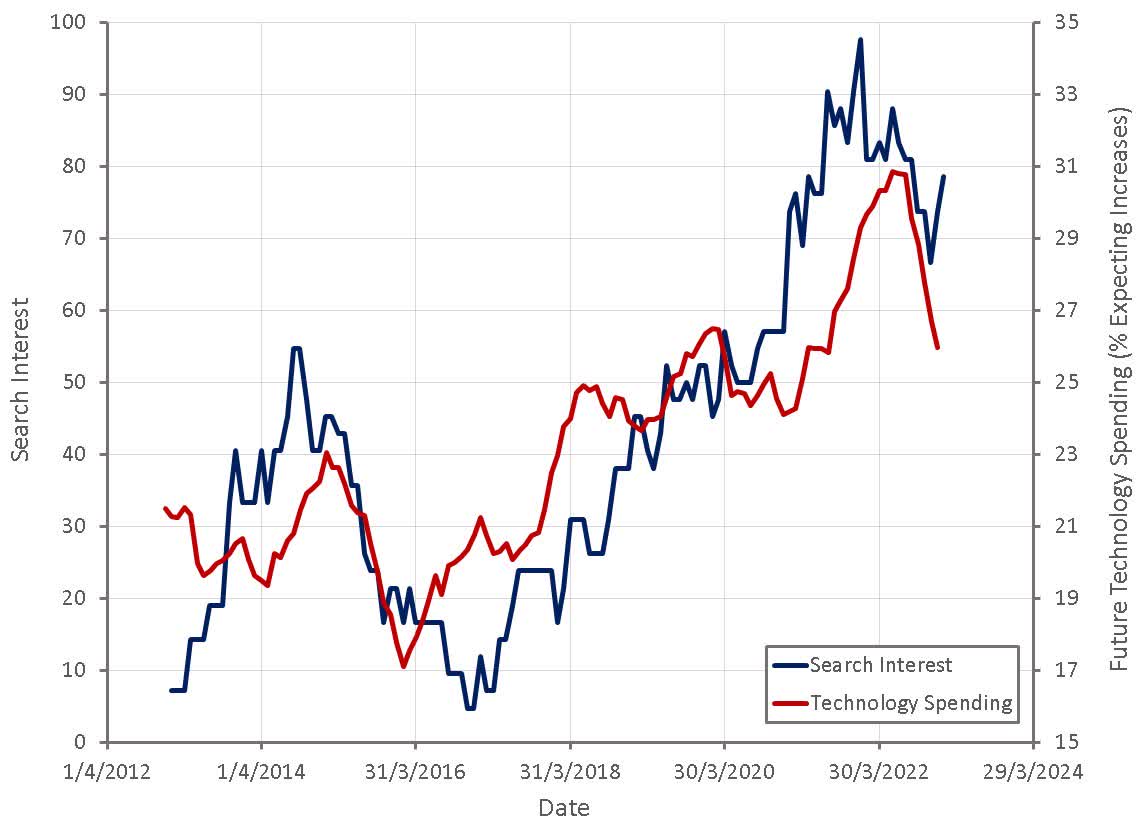

Search interest for Zscaler pricing potentially indicates a softening of demand in 2022, which may be beginning to bounce back slightly.

Figure 10: “Zscaler Pricing” Search Interest (source: Created by author using data from Google Trends and The Federal Reserve)

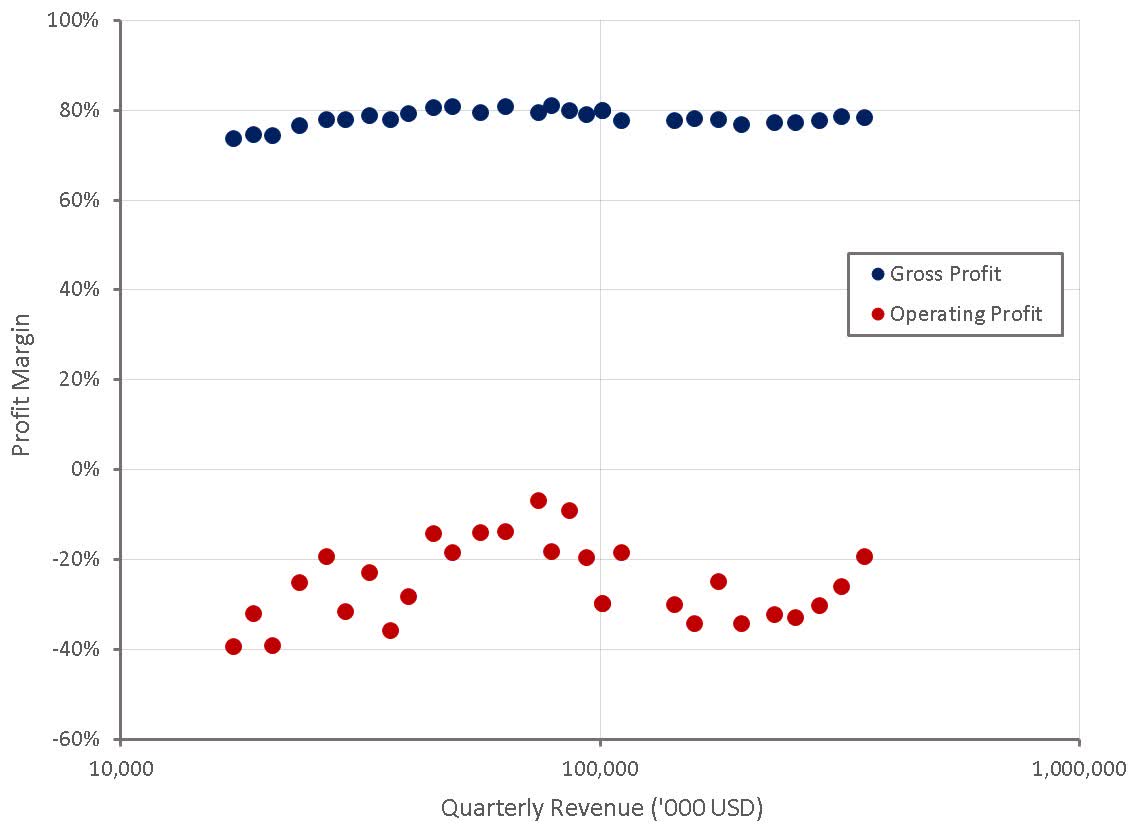

Zscaler has extremely strong margins for a SaaS company, which is somewhat surprising given that they have to maintain their own global network, but this speaks to the high value that their service offers customers. Zscaler believes that their decision to build out their own network is a competitive differentiator and is supportive of margins because they avoid paying high margins to the hyperscalers.

Zscaler is yet to reach operating breakeven, in part due to heavy investments in the business over the past few years. Zscaler remains confident of reaching 20-22% operating margins in the long-term though, which is supported by their high 90% gross retention rates. This could take time though as management has suggested that while growth is in excess of 30%, margin expansion of less than 3% annually should be expected.

Figure 11: Zscaler Profit Margins (source: Created by author using data from Zscaler)

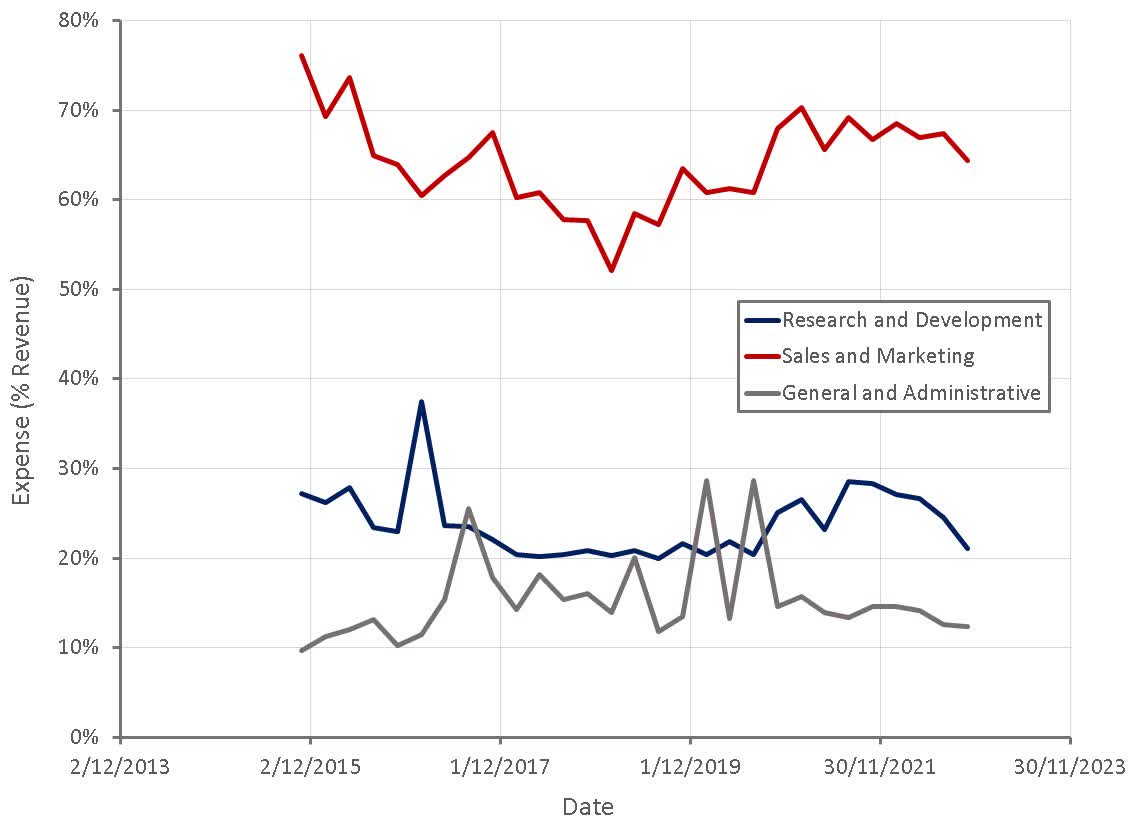

The burden of R&D and sales and marketing expenses is beginning to moderate after heavy investments through the pandemic. These costs are not particularly concerning as Zscaler’s R&D and general and administrative expenses are already fairly low, and sales and marketing is reasonably efficient.

Figure 12: Zscaler Operating Expenses (source: Created by author using data from Zscaler)

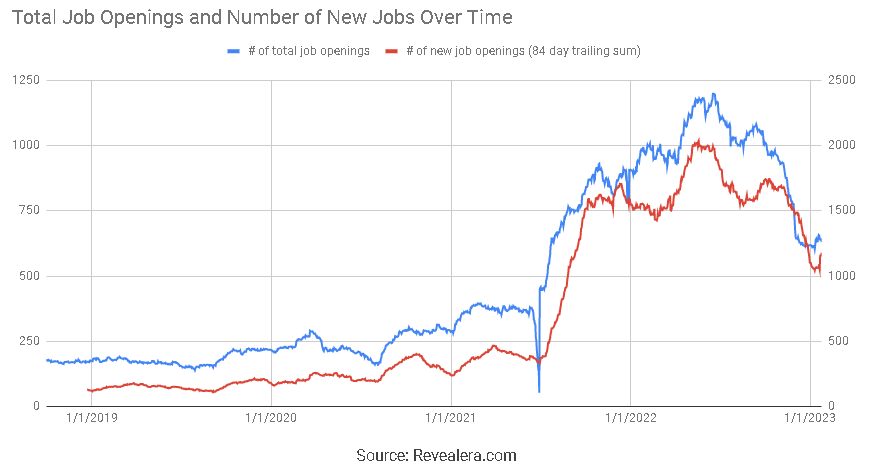

Zscaler expects to moderate hiring going forward, which will be supportive of margin expansion. Hiring is focused on quota carrying sales reps and R&D. Half of Zscaler’s engineering team is in India, which reduces the burden of R&D by an estimated 10% of sales relative to having the entire engineering team in the Bay area.

Figure 13: Zscaler Job Openings (source: Revealera.com)

Valuation

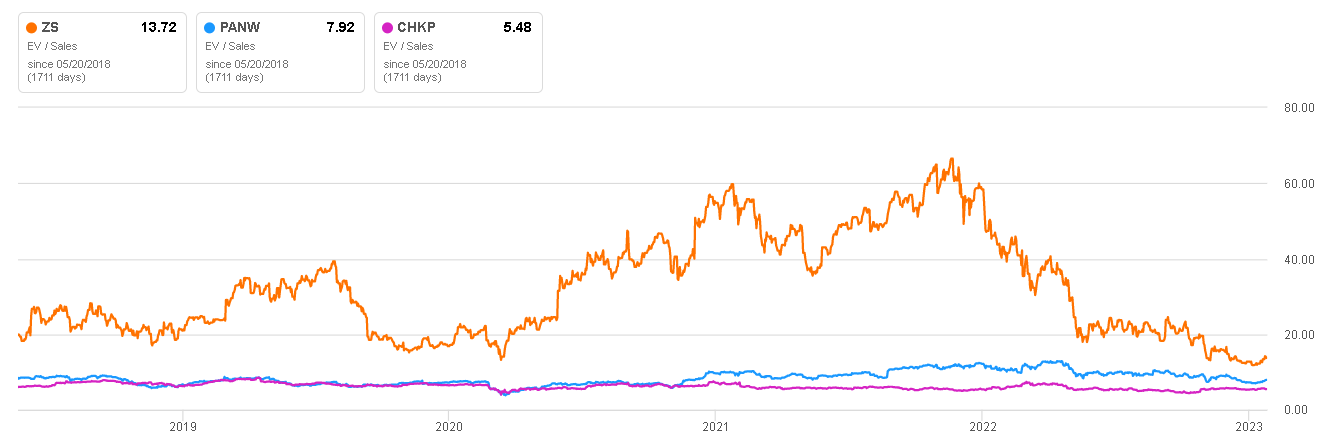

Investors probably only need to look forward around three years and Zscaler will be trading on a similar revenue multiple to a company like Check Point Software (CHKP). While Zscaler is unlikely to achieve Check Point like margins, there is far too little value being placed on growth at the moment.

Higher interest rates have crushed the valuations of high duration stocks like Zscaler, as would be expected, but with inflation rapidly declining there has been little rebound. This appears to be based on an expectation of a recession hampering growth, but this is not being priced in evenly across all stocks.

Figure 14: Zscaler EV/S Multiple (source: Seeking Alpha)

Conclusion

Zscaler should be highly profitable at scale and still has a long growth runway ahead. Little of this is currently priced into the stock due to uncertainty shortening the time horizons of most investors. While the near term may be volatile, Zscaler’s stock is likely to do well over the long term given the relatively modest current valuation.

Be the first to comment