BING-JHEN HONG

Taiwan Semiconductor Manufacturing Company (NYSE:TSM) registered a successful year in 2022 that, however, has largely gone unnoticed considering the stock performance. In the meantime, the company’s long-term prospects look optimistic. TSMC remains the technology leader in the semi-industry and is actively pursuing geographic diversification of capacity. Although 2023 is expected to be a slight growth year due to the looming recession fears, I believe the chip leader will be able to return at a double-digit run rate beyond.

Outlook

The rapid digitalization of the global economy will be a powerful driver of the rapid transition of the largest manufacturers to the most advanced chips. Looking at the decomposition of production mix, TSMC’s share of ICs manufactured using advanced technologies (7nm and below) reached 53% in 2022 compared to 50% in 2021 and 41% in 2020. How this trend translates to profitability, it’s hard to determine exactly as profitability depends significantly on the utilization level of the fabs, while add to that exchange rate effects and the fact that advanced nodes are initially more expensive in production as a consequence of their novelty.

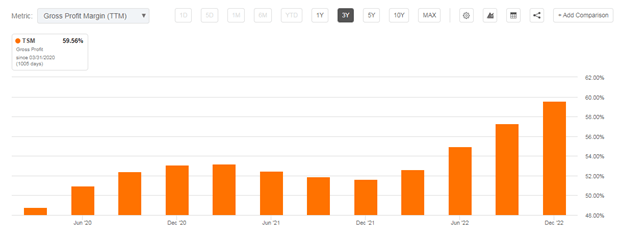

Still, some correlation between technical processes and profitability of TSMC could be spotted. If in 2020 the gross margin of the company was 53%, then in 2022 it approached close to 60%.

Gross profit margin (Seeking Alpha)

At the same time, Moore’s law continues to work properly for TSMC and the company expects to commence production based on 2nm process technology in 2025. Moving to the point, I expect the gradual migration of TSMC’s customers to more advanced nodes in the near term will exhibit a positive impact on the company’s profitability.

TSMC also continues to strengthen its position as a technology leader in the semi-industry following the start of N3 production in late 2022. At the moment, demand for them outstrips supply as the company is rumored to have already received orders from its major clients.

As a primary customer of TSMC, Apple (AAPL) could contribute largely to the commercialization of the 3nm process ahead of iPhone 15, which will be equipped with the innovative A17 processor. The only significant competitor to TSMC in terms of technology remains Samsung (OTCPK:SSNLF), which has also begun mass production of N3 chips.

2022 financials

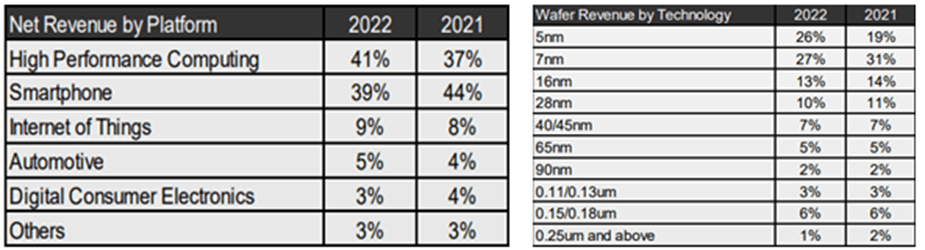

Despite a tough market environment, the company’s financial results were once again strong. Q4 revenue was up by 26.7% YoY to reach $19.9 billion, despite inventory adjustment and demand softness. Total revenue surged 33.5% to $76 billion for the full 2022 year, and the company transferred 45% of it down to the bottom line. The main part of revenue fell on advanced processes – 7nm (27%) and 5nm (26%).

Revenue breakdown (Company Reports)

Breakdown by sales geography has finally shown the first signs of a recovery in demand from the Chinese, as the market share in the revenue mix returned to the level of Q4 2021 of 12%, gaining significantly on a sequential basis from 8%.

However, TSMC is likely to face a slowdown in demand in 2023. On the earnings call, the CEO noted that he expects semiconductor sales to decline by 4% in 2023 (excluding memory chips). The year is deemed to be of moderate growth for the company, with a decrease in revenue of 5-9% YoY in H1’23 and a healthy recovery in H2’23. The main factors behind the slowdown will be further inventory level adjustments by customers and a difficult global macroeconomic environment that threatens a mild recession in 2023.

Against the backdrop of downturn fears, TSMC’s investment ambitions continue to grow. The company believes that semiconductor demand will return to strong growth from 2024. In this regard, the CAPEX plans for 2023 are expected to range between $32-36 billion, where 70% of the pile will be allocated to advanced technical processes. R&D spending is planned to increase from 7.2% up to 8.5% of revenue, as the company continues to actively work on the 2nm process technology.

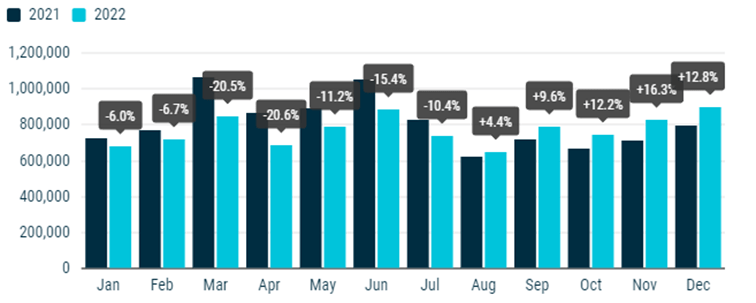

Going forward, TSMC announced that the plans in Arizona and Japan will be expanded, where investment in US factories is set to reach $40 billion with the launch of the second stage in 2026 (the first stage will start operating in 2024). In addition, the company is considering building a specialty fab to supply the automotive market in Europe, which took a hard blow due to chip shortage, and now is exhibiting a good path of recovery, marking the fifth consecutive month of growth.

New passenger car registrations in the EU (ECEA)

Valuation

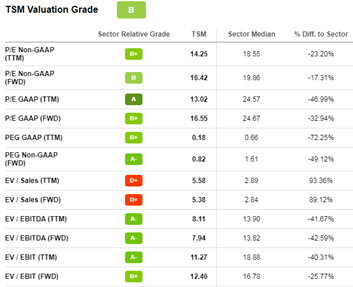

To determine the value of TSMC, let’s take a look at the valuation screen on Seeking Alpha. The company is trading at an EV/EBITDA of 7.9x, which represents a 42% discount to the sector median multiple on a forward basis and implies an attractive upside gap.

Valuation screener (Seeking Alpha Data)

Taking into account the threat of further escalation of relations between China and Taiwan, I think it’s suitable to apply a discount for the geopolitical risk. Given the potential upside on the EV/EBITDA basis and 20% discount, I believe TSMC could still provide at least 20% upside potential at current levels.

Additionally, the purchase of TSM shares by Berkshire Hathaway (BRK.A) (BRK.B) is a positive signal for investors. The fact that it rarely buys tech stocks shows a high degree of confidence in the fund’s managers about TSMC’s long-term prospects.

Risk factors

The cause of concern for TSMC remains difficult geopolitical tensions, which are the main factor of the discount, even though the effects on the company’s operations have not yet been observed. However, this will become a key driver of the company’s geographic diversification of the business. Additionally, a more protracted economic downturn should not be ruled out.

Conclusion

TSMC dominates the semi-industry thanks to a strong focus on the core competencies in the foundry business and advanced manufacturing capabilities. TSMC has a serious purchasing power underling its products in the face of Apple, Qualcomm (QCOM), MediaTek (OTCPK:MDTKF), AMD (AMD), NVIDIA (NVDA), and Broadcom (AVGO), and is capable of producing on a large scale and with high yield. And despite TSMC will face inventory adjustment and a weak demand environment, in my view, nothing can stop the flywheel of the technological progress. I believe TSMC could perform with the above cyclical growth in downturns, and power the adoption of the new advanced nodes to achieve strong profitability going forward. TSMC could also serve as an indicator of where the semiconductor industry is heading, based on the CAPEX and sales guidance it provides. To imagine how the company relates to the world’s cutting-edge chips market, if you are reading this article from a smartphone, there is a 90% chance that it is assembled from the TSMC factory’s chips.

Be the first to comment