putilich

ZoomInfo (NASDAQ:ZI) is a leading data intelligence provider that has recently expanded into a multiplatform solution. This was a risk initially but the bet is paying off exceptionally well. The company has reported outstanding growth beating both revenue and adjusted earnings expectations for growth. In addition, management has raised its guidance on the back of strong momentum. In this post I’m going to break down its business model, financials and valuation, let’s dive in.

Developing Business Model

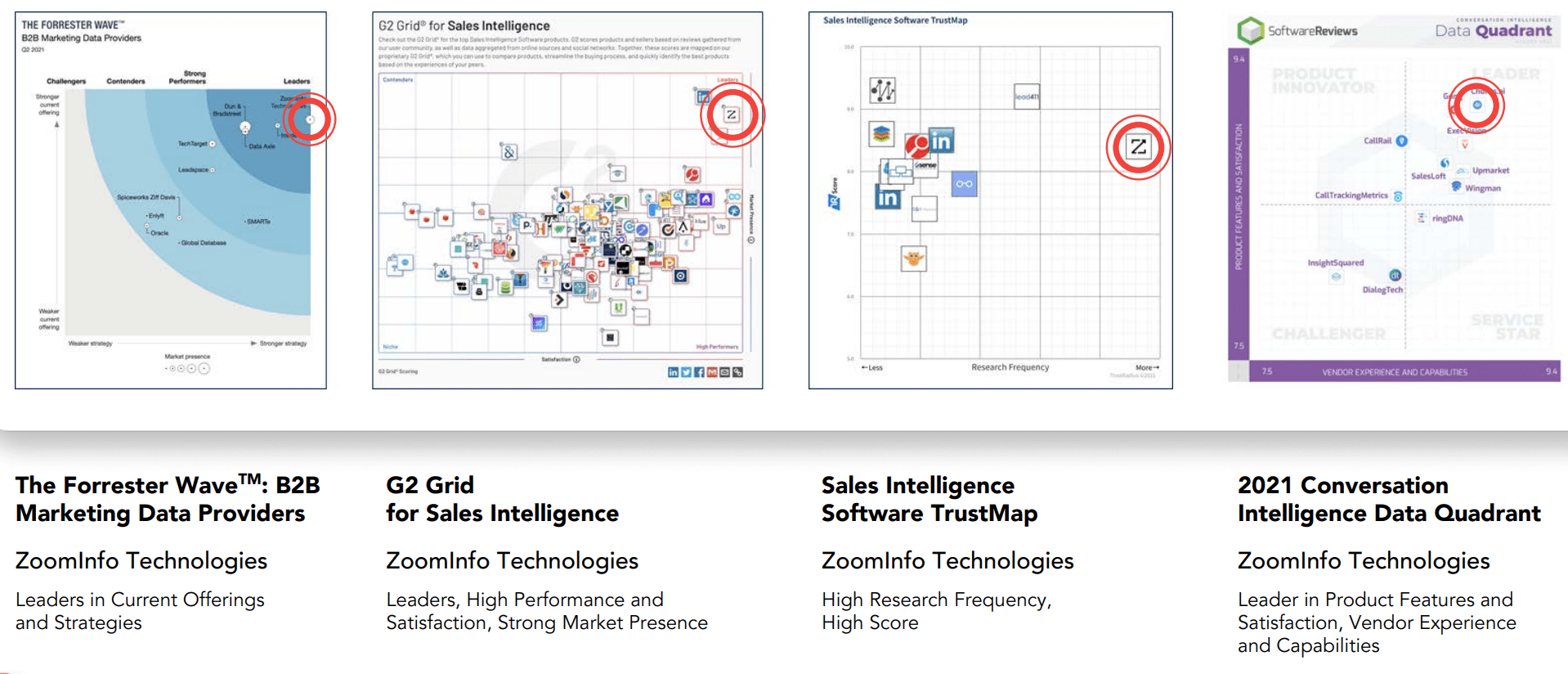

ZoomInfo is a data and software company that is known for providing contact data, which is utilized by B2B salespeople and marketers. This data basically includes the job titles, email addresses, and even phone numbers of various individuals. For example, let’s say a cybersecurity company wants to contact all the Chief Information Security officers [CISO] who work at Fortune 500, pharmaceutical companies. They could use ZoomInfo to generate a list of these people. ZoomInfo has over 80 million direct emails, 46 million phone numbers, and over 4.5 million contacts for C-level individuals. Other “Data intelligence” providers include Bombara, LinkedIn Sales Navigator, and various other “cheap” data providers. ZoomInfo is not known as the cheapest, but it is regarded as one of the best. The business has consistently ranked as a product leader in the various “quadrants” outlined by review companies such as Forrester and G2.

ZoomInfo leadership (Forrester, G2 etc)

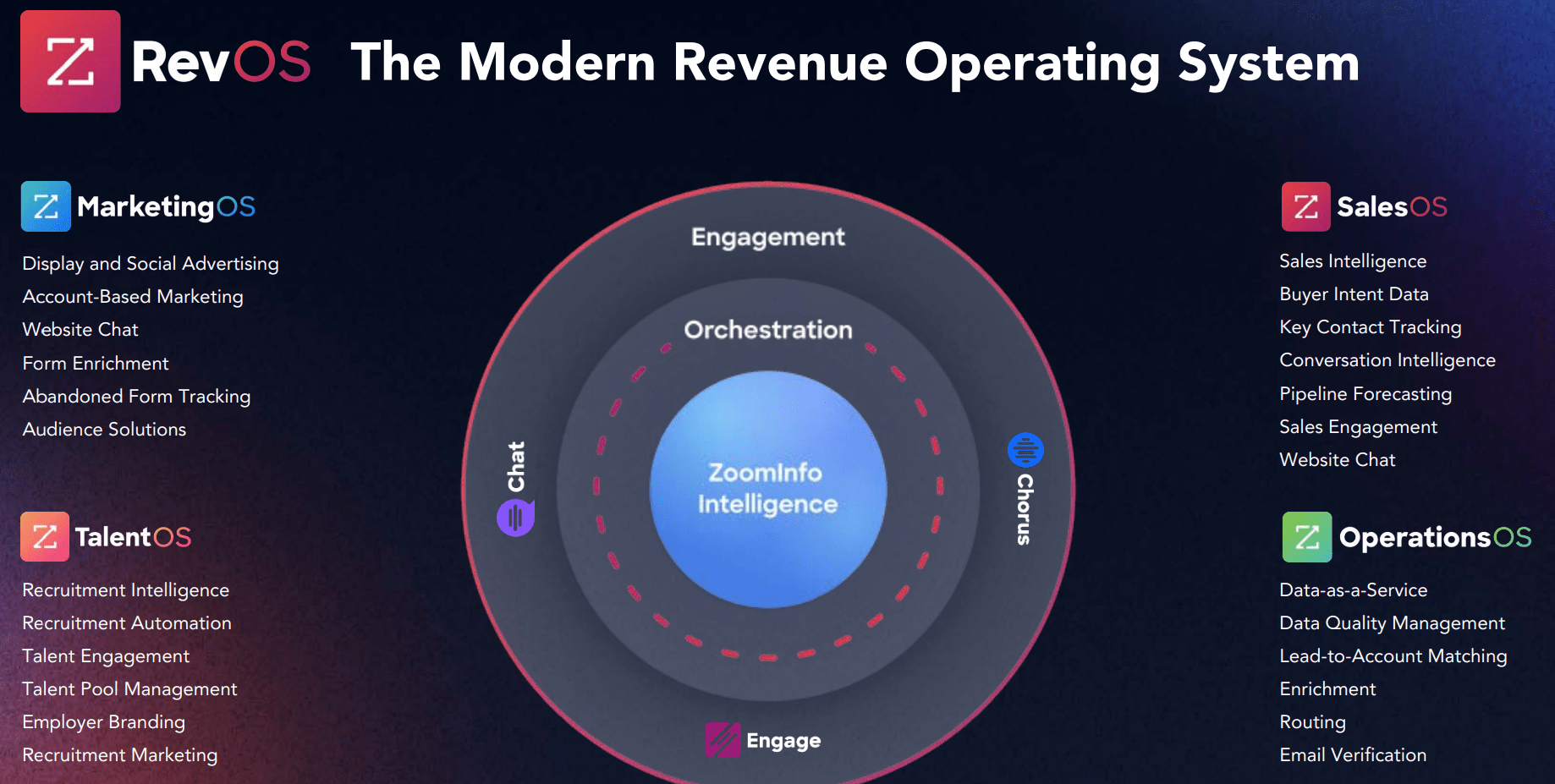

The company has expanded its solution over time from a single-point solution to an entire platform which it calls a “Modern Revenue Operating System”. This includes a SalesOS product that offers Sales intelligence, Sales engagement and even buyer intent data. In addition, we have the MarketingOS platform which offers display adverting, Account Based Marketing, and form enrichment. This platform competes with players such as DemandBase and Salesforce Pardot. ZoomInfo also offers a TalentOS platform for recruitment and even an Operating product.

Modern Revenue Operating System (Zoominfo)

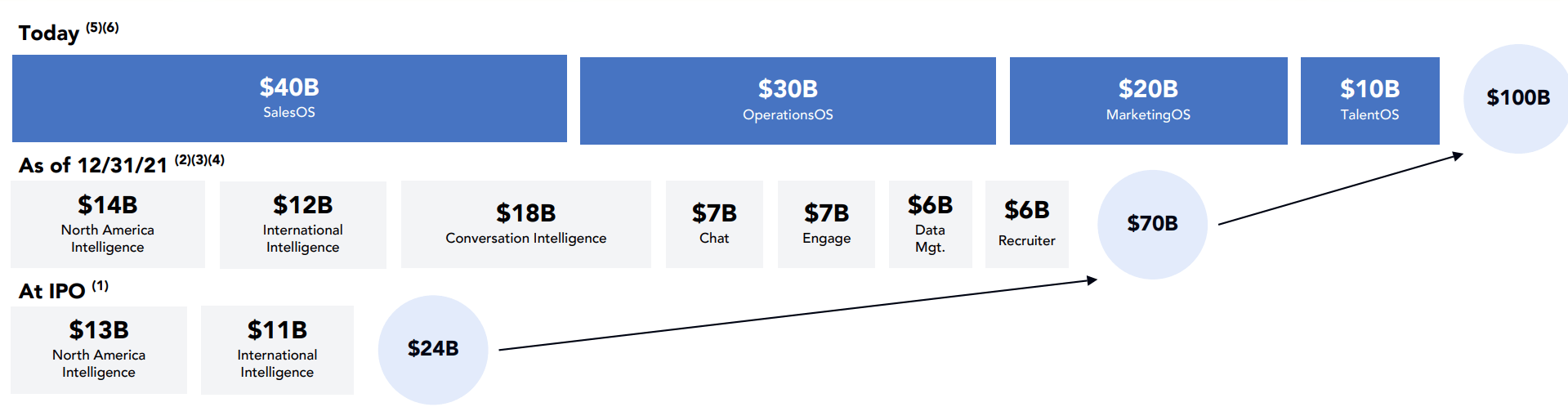

ZoomInfo also offers a popular AI-powered chat bot platform called Chorus. In addition, the business has recently announced integrations with Snowflake (SNOW), one of the world’s most popular data warehouse providers. The expansion into various product categories has caused the company to expand its total addressable market [TAM] from “just” $24 billion in 2020 to over $100 billion, according to ZoomInfo.

ZoomInfo TAM (Q3,22 report)

The company offers its products via a “self-service”, free trial setup, and then additional subscription pricing based on the various modules. The beauty of developing a multi-product solution is that upsells and cross-sells are easy to implement, which I will discuss more in the financial section next.

Growing Financials

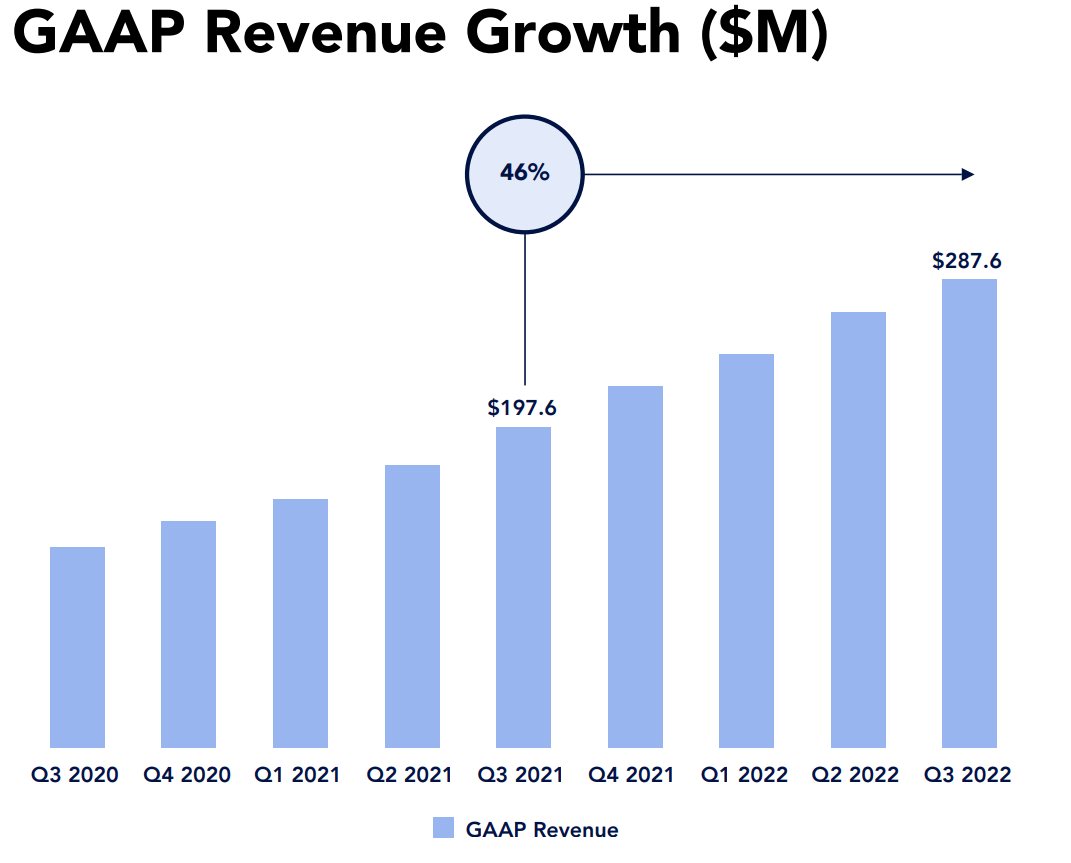

ZoomInfo reported strong financials for the third quarter of 2022. Revenue was $287.8 million, which beat analyst estimates by $9.23 million and increased by a rapid 45.55% year over year. This growth rate was slower than the prior quarters growth rate of 53.51%, but was still solid overall.

Revenue (Q3,22 report)

The top line was driven by strong growth in its larger customers. The company reported a 40% increase in its customers which spend over $100,000 per year with the business to 1,848 customers. These results were a testament to its multiplatform strategy, which has drove record Average Contract Value [ACV] per customer. Over 75% of ZoomInfo’s MarketingOS customers are already SalesOS customers. Alignment between sales and marketing teams in B2B is a hot topic and thus getting teams on the same platform is a natural transition. This is a similar model Salesforce took with its Sales Cloud, Marketing, and Service cloud solutions. Given Salesforce (CRM) has a market cap of over $130 billion, over ten times that of ZoomInfo it is safe to say the strategy works. The competitive advantage ZoomInfo has over Salesforce is it is a contact data provider at its heart, which makes it especially enticing for B2B customers.

ZoomInfo has also integrated platforms such as Slack with its solution, which can help to alert sales teams when intent or contact data is reported by a customer. The company reports that if interested “prospects” are responded to in less than 90 seconds, then conversion rates increase by 40% on average. This is immensely valuable and has many use cases. For example, the system can alert a salesperson if a prospect from one of its targeted accounts (businesses) visits a “high value” webpage such as the pricing page. Its “advanced functionality” solutions now make up 30% of the Average Contract Value.

By industry, the company reported strong growth for its product across finance, insurance, logistics, and the manufacturing sector. Its new and expanded customers in the quarter included the fintech disruptor SoFi, Unilever, Monday.com, Vmware, and many more. This diversification across industries is a strong positive for ZoomInfo, as it makes the company less prone to demand from a specific cyclical sector.

New and expanded customers (Q3,22 report)

In the third quarter, the company scored its “largest” expansion deal in its history with an 8-figure total contract value client.

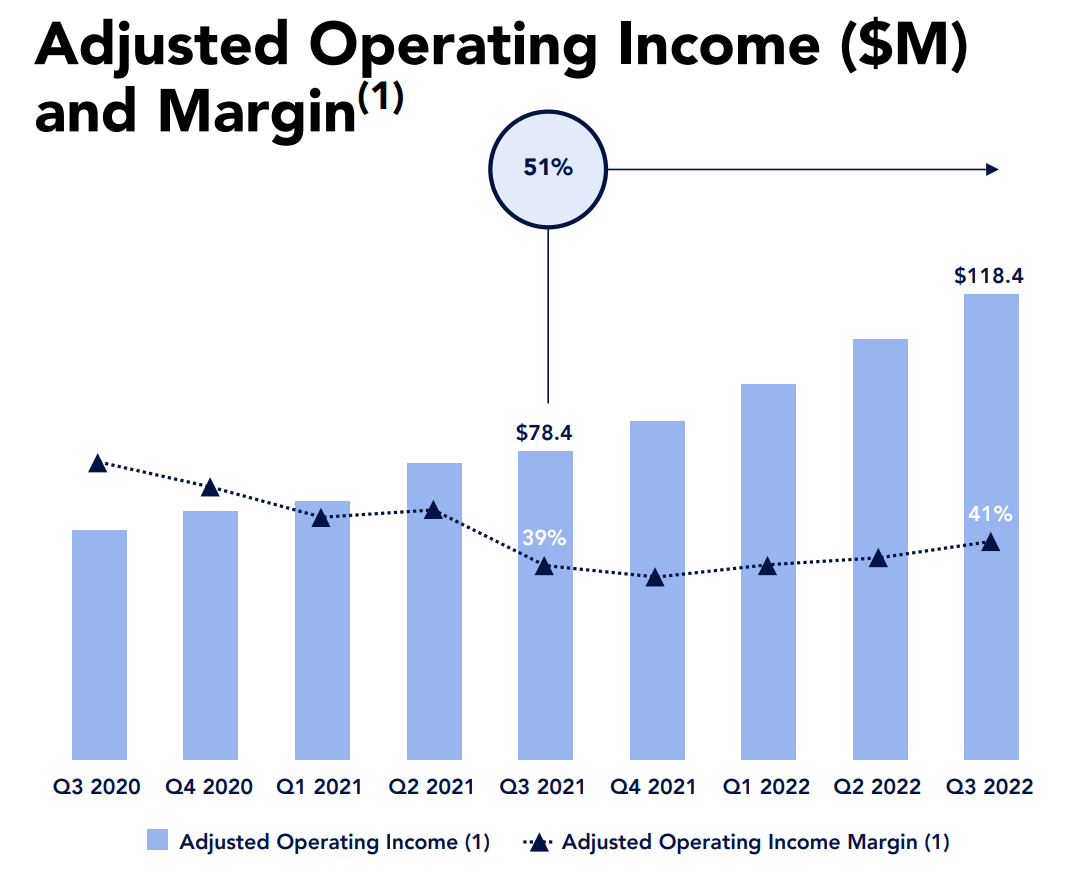

Onto profitability, the company reported an Adjusted Operating Income of $118.4 million, which increased by a solid 51% year over year. Non-GAAP Earnings Per Share was $0.24, which beat analyst estimates by $0.04.

Operating Income (Q3,22 report)

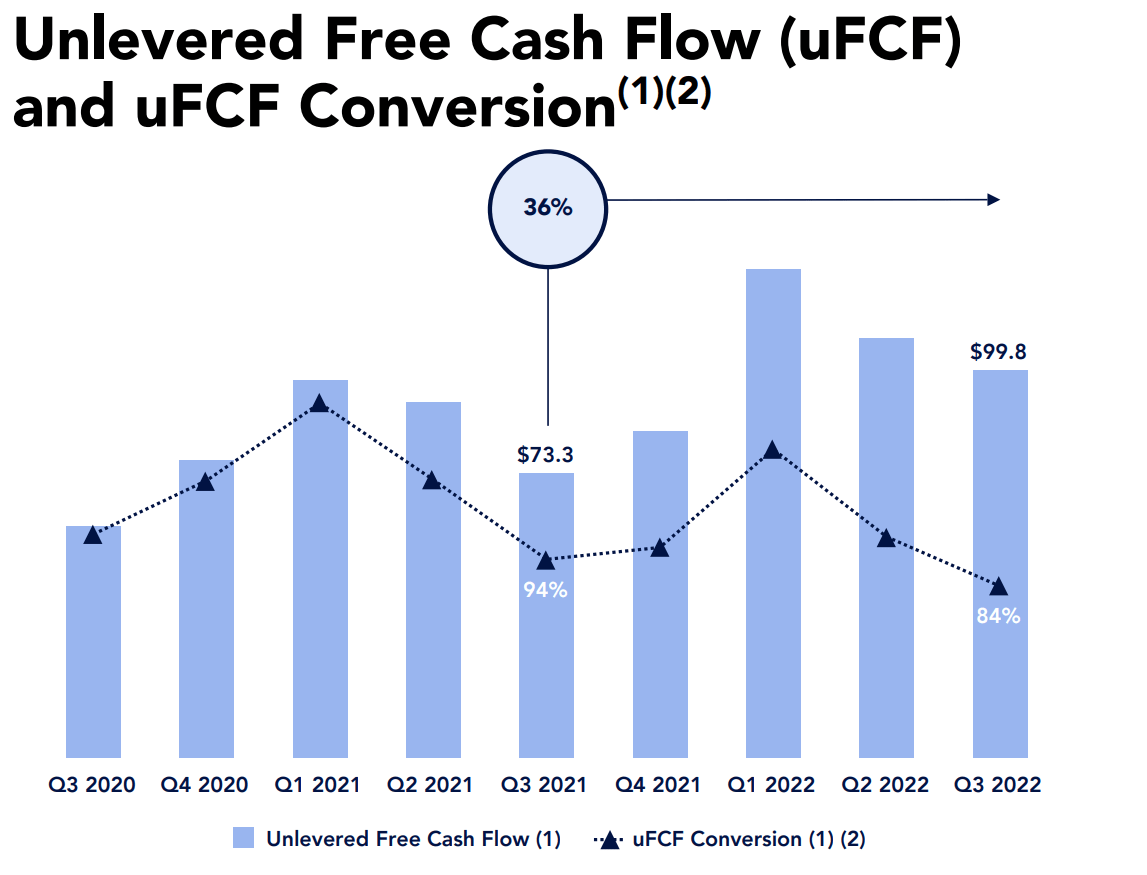

ZoomInfo also reported solid unlevered free cash flow of $99.8 million, which increased by 36% year over year.

Free Cash Flow (Q3,22 report)

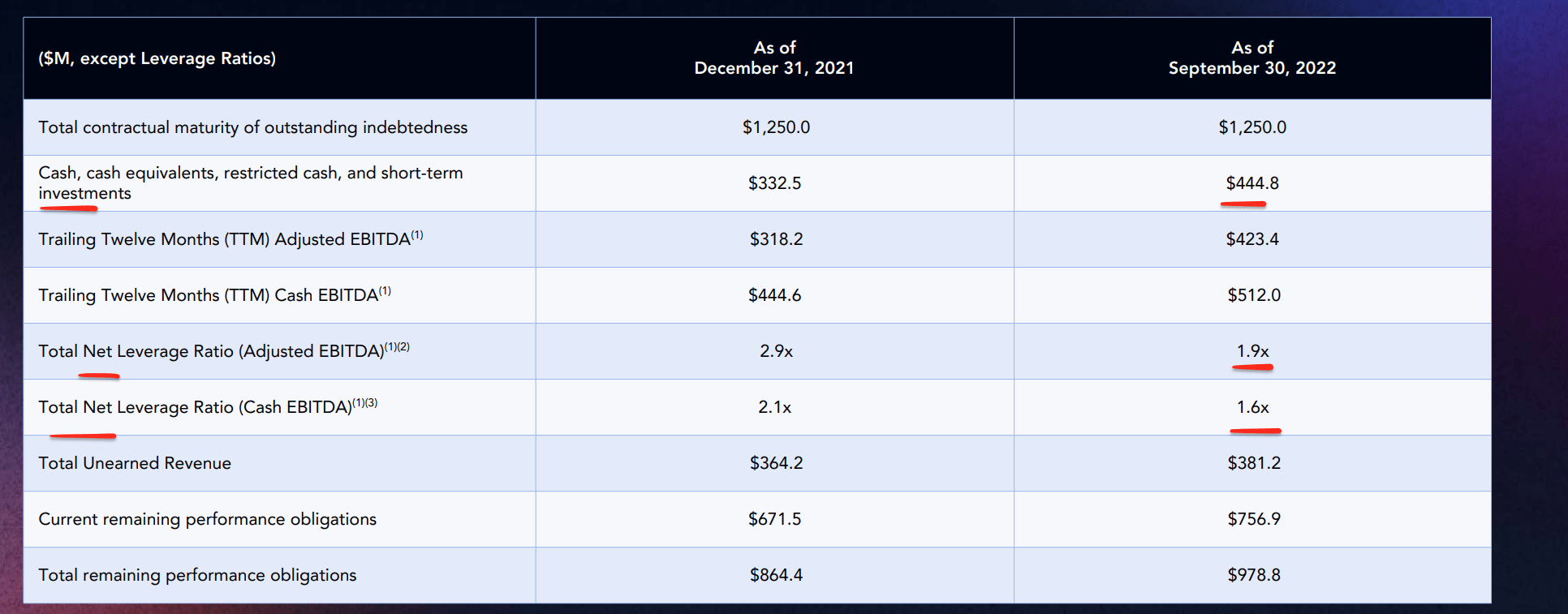

ZoomInfo has a solid balance sheet with $444.8 million in cash, cash equivalents, restricted cash and short-term investments, which increased by 33.7% year over year. Its Total Net Leverage ratio (Adjusted EBITDA) also declined from 2.9x to 1.9x which was a positive.

Balance Sheet calculations (Q3,22 report data)

For the full year of 2022, Management showed confidence as it increased its revenue guidance by $10 million to between $1.094 billion and $1.096 billion, up a rapid 46% year over year at the low end. The company also increased its operating income guidance to between $442 million and $444 million, up from $435 million previously stated.

Advanced Valuation

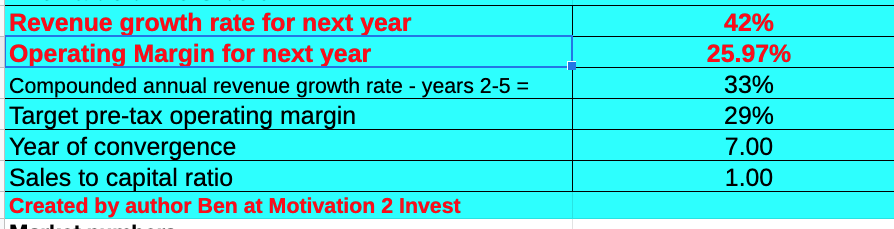

To value ZoomInfo, I have plugged its latest financials into my discounted cash flow valuation model. I have forecasted 42% revenue growth for next year, which is fairly conservative as less than the 46% expected for the full year of 2022. I expect this to be driven by the forecasted recession, which will likely result in longer sales cycles. In years 2 to 5, I’ve reported 33% revenue growth per year. This is fairly conservative again and partially driven by the higher base revenue.

ZoomInfo stock valuation (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation, I have capitalized R&D expenses which has lifted net income. In addition, I have forecasted a pre tax operating margin of 29%, in 7 years. I forecast this to be driven by the continued cross-sells of its multi-platform solution.

ZoomInfo stock valuation 2 (created by author Ben at Motivation 2 Invest)

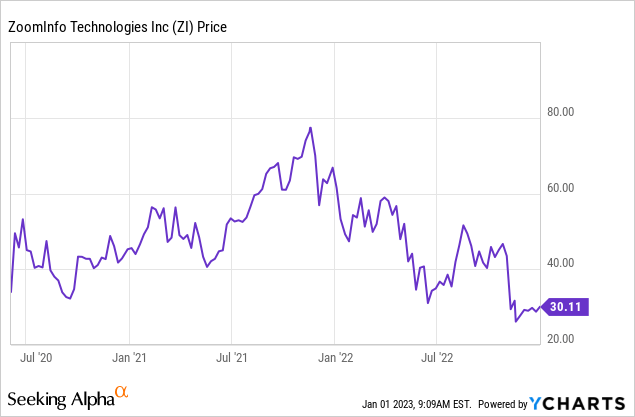

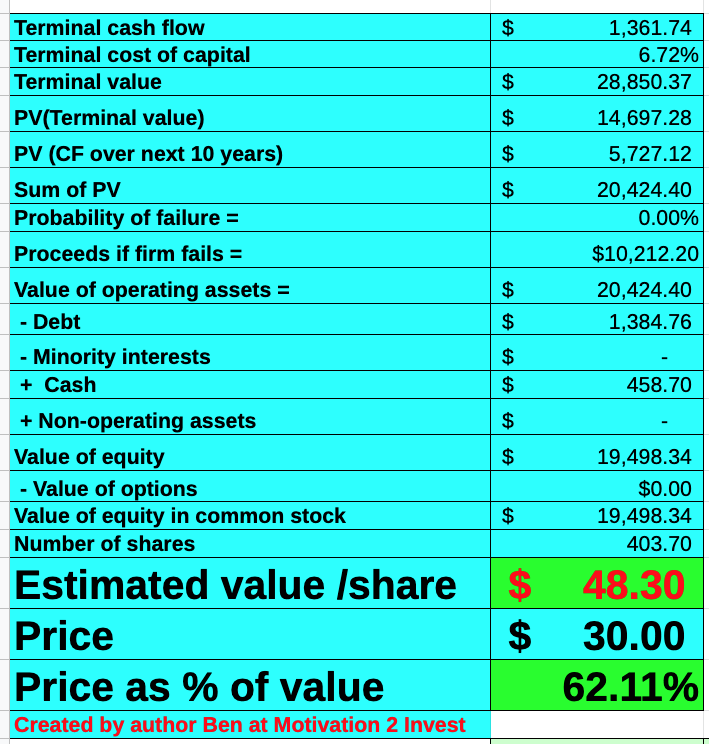

Given these factors I get a fair value of $48.30 per share, the stock is trading at ~$30 per share at the time of writing and is thus nearly 40% undervalued.

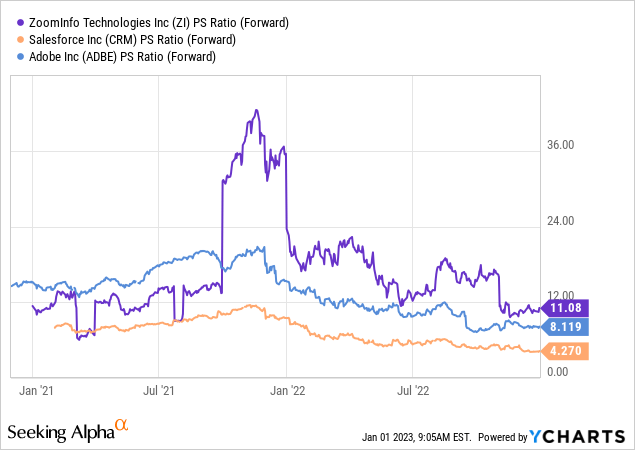

As an extra datapoint, ZoomInfo trades at a Price to Sales ratio = 11.78, which is 29.25% cheaper than its 5 year average. This is slightly higher than other SaaS sales/marketing companies, but ZoomInfo is growing at a faster rate.

Risks

Longer sales cycles/recession

Many analysts have forecast a recession and thus I am expecting longer sales cycles, as decision-makers delay spending on new products. This will likely result in slower growth in the short term, but long term the company has a large market opportunity.

Final Thoughts

ZoomInfo is a strong leader in data intelligence solutions and is now using its position to expand into larger business segments. This would seem like an uphill battle given the strong competition and recessionary environment, but ZoomInfo has generated rapid growth so far. Its stock is also undervalued intrinsically and relative to historical multiples, thus it could be a great long term investment.

Be the first to comment