Maks_Lab

I expected to discuss why the iShares Core Dividend Growth ETF (NYSEARCA:DGRO) isn’t worth your time. Taking a closer look, though, it’s not as bad as its name implies.

“Dividend growth” is a funny phrase. It’s kind of an oxymoron. A company might pay a dividend because it can’t think of any ways to invest it back into the business – yet that’s the opposite of growth. But, okay, that’s not fair. Dividend growth investing is about owning companies that reward their shareholders with a growing dividend that keeps up with inflation. It’s not the company that’s growing; it’s the dividend that’s growing.

The problem is that DGRO doesn’t do a noteworthy job of providing a dividend or growing one.

What is DGRO?

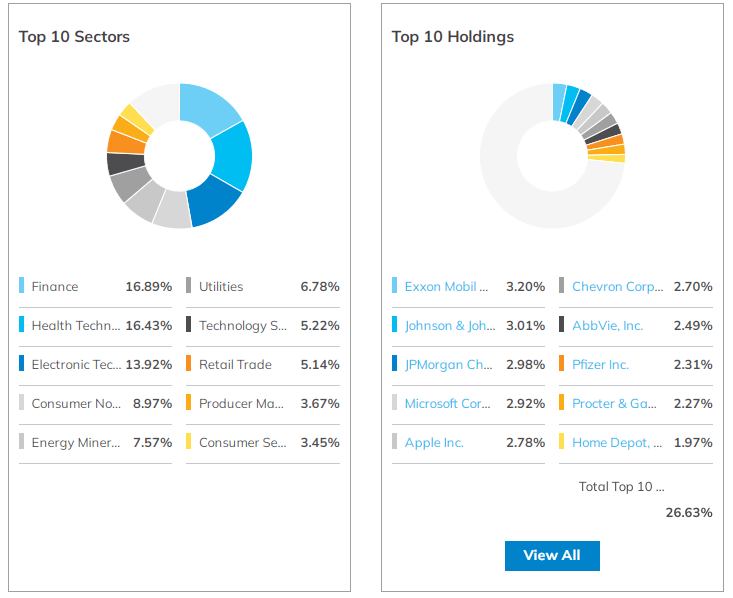

Amassing an impressive $24.5 B in assets, DGRO is an ETF that tracks the Morningstar US Dividend Growth Index. As one might expect, it has a preference towards US large cap value stocks. Many are name-brand, such as Apple (AAPL), Microsoft (MSFT), and Johnson & Johnson (JNJ).

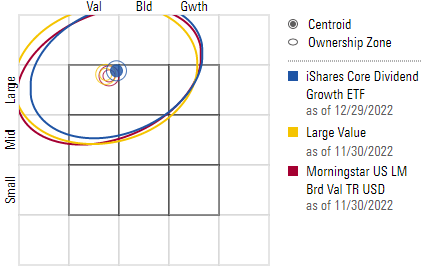

DGRO is best classified as a large cap value ETF. (Morningstar)

Sector diversification is pretty good, and the top 10 holdings constitute around 27% of the ETF. From this metric it’s slightly more concentrated than the S&P 500, which is at 24%, but I can’t imagine the 3% difference amounts to much. Regardless, the concentration can be watered down in a more rounded-out portfolio.

DGRO has reasonable sector diversification and concentration. (ETF.com)

All of this looks good, but there is still a problem – dividend growth. The Morningstar US Dividend Growth Index, which DGRO tracks, does not select companies based on their ability to sustain an inflation-hedged dividend. At least not directly. Stock selection is driven primarily by four criteria:

- The stock does not have a top 10% dividend yield,

- The dividend is qualified income,

- The stock has seen 5 years of uninterrupted dividend growth, and

- The stock has positive consensus earnings forecast and payout ratio less than 75%.

The stock not being in the top 10% dividend yield is a good thing – we want to exclude dividend traps. Wanting qualified income is also nice, though it comes at the cost of REIT exclusion (which I don’t find particularly harmful). The stock needing only 5 years of dividend growth, though, isn’t a terribly reliable indicator of future dividend growth. One can imagine a sector having a hot decade with dividends rising quickly and consistently, only to crash shortly after.

The 5-years screen is also somewhat arbitrary. At 0 years, we basically have an S&P 500 index. At 25 years, we’d get something similar to a dividend aristocrat index. Then, it should not be a coincidence that DGRO has a 60% overlap by weight with NOBL (according to the ETF Research Center). I am a fan of NOBL, but at the same time I am a fan of 25 years of history. Not so much a fan of 5 years of history. Moreover, the overlap between DGRO and the S&P 500, by weight, is just about 53%.

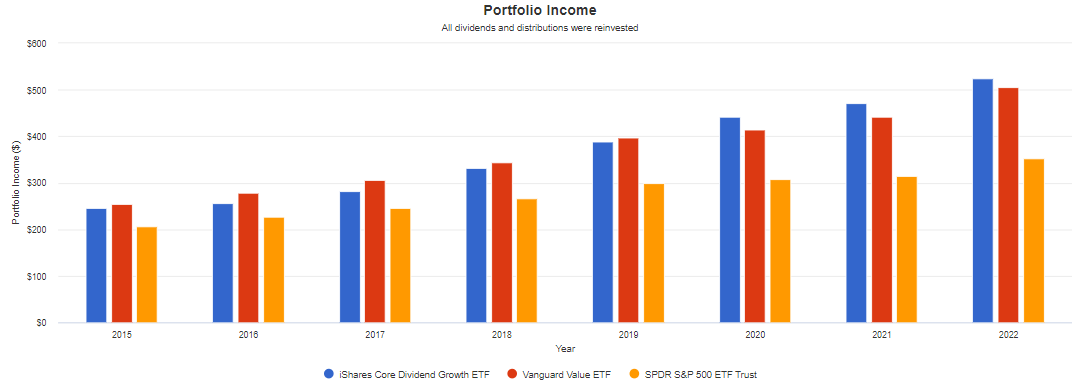

Do Morningstar’s quant screens actually result in dividend growth? Sort of. Dividend growth is better than the S&P 500, but it’s better only by accident. To illustrate this point, below are yearly dividends based on an initial $10,000 investment in DGRO, the Vanguard Value ETF (VTV) (an example large value ETF that naively targets dividend growth), and the S&P 500. Case in point: VTV, in red, has grown its dividend pretty much exactly how DGRO has, in blue.

DGRO has better dividend yield than the S&P 500, but it isn’t clearly better than other value ETFs. (Portfolio Visualizer)

In other words: are you really getting the dividend growth portfolio you want? Probably not. It’s similar to the S&P 500 but with a slant towards quality firms. You’re going to end up with higher dividend yields because quality firms naturally have higher dividend yields anyway. Certainly, it’s not the only ETF capable of growing a dividend consistently. Even the S&P 500 could do that.

DGRO is still preferable to the S&P 500 in my opinion. Morningstar’s screens are good: they exclude junk stocks and have some good, rules-based criteria for picking dividend growers. But, given how lax the screening is, it looks as if iShares is intentionally trying to minimize tracking error from the total market. I question what DGRO offers that another ETF, like VTV, cannot.

DGRO Doesn’t Stand Out From The Pack

If DGRO’s dividend and dividend growth aren’t stellar, then what does DGRO bring to the table? Apart from its interesting index construction methodology, I don’t think it stands out at all. At least for long-term total returns, we can turn to factor analysis. Below are Fama-French 5-factor regressions (since 2014, admittedly), for DGRO and comparable dividend growth and value ETFs. They’re all low beta, and tilt towards large value stocks. It’s not clear where DGRO has excelled or will excel compared to the competition. Why would you not choose the Schwab US Dividend Equity ETF (SCHD) or VTV over DGRO? I struggle to find a compelling reason.

DGRO hasn’t been much different from other value ETFs in terms of factor regression. (Portfolio Visualizer)

Should You Buy DGRO?

Meh. If you want a value-tilted ETF that selects holdings based on a firm’s ability and consistency to reward their shareholders with growing dividends, then DGRO seems like a decent bet. If you’re looking primarily for dividend growth, though, then you might be disappointed. The dividend growth is more like a secondary or tertiary feature of the fund, and I don’t think it’s special. What you’re really getting is a value-oriented ETF.

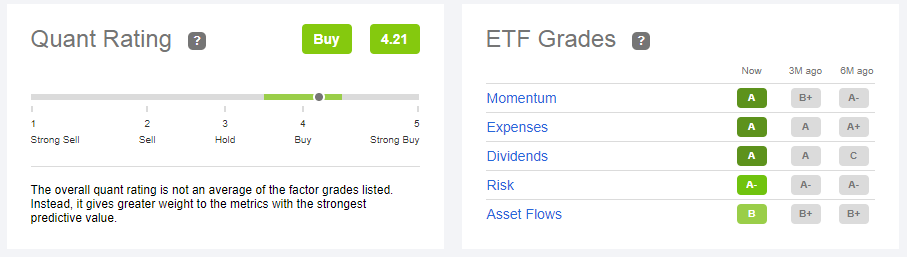

Seeking Alpha’s Quant suggests buying DGRO right now. But, Quant likes every dividend growth ETF right now. DGRO isn’t special in Quant’s eyes.

Quant likes DGRO right now, unsurprisingly. (Seeking Alpha)

Still, if dividend growth is important to you, you could go worse than choose DGRO. I can’t see it being materially better than the S&P 500, but the quant screens will probably do something useful. Better to be safe than sorry.

Model Portfolio

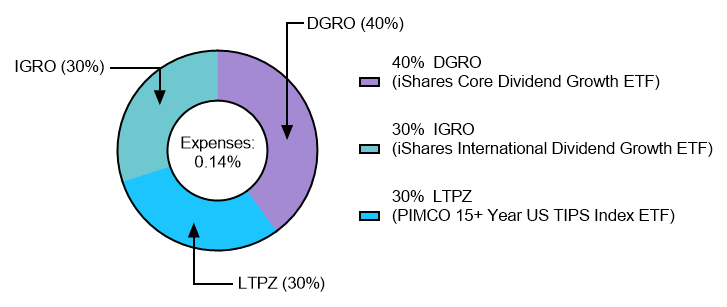

DGRO may be useful in a portfolio that generates inflation-beating income without sacrificing portfolio growth. You could go 100% DGRO, but I’d imagine a few more funds could help round out things. DGRO covers US stocks, so we might benefit from an international stock fund too. And maybe some bonds.

Who needs international exposure? You need international exposure. If US firms are unable to keep up their dividends in the coming financial crisis (and we can count on one is coming eventually…), then maybe international firms still have a fighting chance. If our goal is securing consistent dividends such that we don’t need to sell off shares, then it is irrational not to protect against all potential dividend shocks. For intentional diversification, the iShares International Dividend Growth ETF (IGRO) seems thematic.

Finally, 30% of the portfolio is allocated to long-term TIPS via the PIMCO 15+ Year US TIPS Index ETF (LTPZ). In the coming global financial crisis where even international stocks can’t save you, the flight-to-quality of government bonds provides inflation-protected income while stocks recover (and some price appreciation to boot). The bonds are long-term because of their higher yields, their weaker correlation to stocks, and because our time horizon is… long. Long-term Treasuries are also an interesting choice (probably better, actually) because they are even less correlated to global market shocks. If you’re wealthy enough to retire with 70% in dividend-paying stocks, then you probably don’t need to inflation-protect your bonds anyway.

Sample portfolio involving DGRO. (FM Research)

And that’s our setup: an internationally-diversified portfolio from which we hopefully never need to sell a single share, even in the worst of drawdowns.

Conclusion: DGRO Isn’t All That Bad

DGRO is probably a sensible choice if you’re chasing a dividend growth strategy, but the ETF excels at neither dividends nor growth. It does feature growing firms with increasing dividends, but from several angles it’s very similar to other large cap value ETFs that don’t have the same goals. Actually, I’m surprised iShares hasn’t upped the expense ratio a few notches to eke out more money from diehard dividend growth investors. Maybe iShares already has?

There are worse investment vehicles out there than DGRO. DGRO is alright, I guess. You could have invested in ARKK at the top.

Be the first to comment