adamkaz/E+ via Getty Images

Thesis

We believe that investors should stay away from Zillow Group’s (NASDAQ:ZG) (NASDAQ:Z) stock until the housing market rebounds and their management can prove themselves after the iBuying disaster.

Housing Market Woes

The housing market had a blistering 2020 and 2021 but has struggled in 2022. Thanks to price increases and interest rate hikes housing affordability is hitting a record low.

Median Sales Price of Houses Sold for the United States (FRED)

We can see that the median sales price of houses sold in the U.S. accelerated starting in Q2 2020. This combined with high transaction volumes was beneficial for companies in the real estate industry such as Zillow, but affordability has become such an issue that it is weighing on transaction volumes.

The affordability issue has led to transaction volumes falling off a cliff, with Redfin (RDFN) reporting:

On average, the number of homes sold was down 37.4% year over year and there were 372,522 homes sold in December this year, down 595,428 homes sold in December last year.

This does not bode well for Zillow as they thrive when there is a lot of activity in the real estate market. If the housing market is entering a prolonged period of low transaction volumes Zillow will likely underperform expectations over that period of time. At this time it is difficult to trust that management will be able to execute in a difficult period as they were unable to profit from iBuying when the housing market was red hot.

Management Missteps

iBuying was an unmitigated disaster that damaged the reputation of Zillow and was financially detrimental. For a long time Zillow had sold Wall Street the vision of being able to use their vast data trove to profit from what was essentially house-flipping. This makes sense on paper, a company with a copious amount of housing data should be able to arbitrage some amount of profit and accurately identify when there is a mismatch between price and value. Unfortunately for investors, Zillow managed to execute on this vision so poorly that it brings into question if management is even competent enough to profitably run their core business in a tough environment. When Zillow should have been using their data to buy houses for less than their value and selling them at a slightly higher price, they instead seemed to spend money without regard for price or value. Considering home prices went parabolic while they were engaged in iBuying, all they had to do was buy at market value and they still could have made money by riding the tide of increasing home prices. The fact that Zillow managed to lose money at this endeavor is astounding.

Management’s Side of the Story

In fairness to management, they had a compelling business case for entering the iBuying market and had good intentions in doing so. In Zillow’s Q3 2021 shareholder letter Rich Barton (Zillow’s co-founder & CEO) stated that:

our aim was to become a market maker, not a market risk taker

as well as:

We subsequently set unit economic target guardrails publicly of +/- 200 basis points of breakeven economics.

The rationale that Zillow’s management had with iBuying was to help the housing market function better, which would result in Zillow making money as the business reached scale.

Zillow faced a large amount of market volatility while they were engaged in iBuying and the CEO had this to say:

“In our short tenure operating Zillow Offers, we have experienced a series of extraordinary events: a global pandemic, a temporary freezing of the housing market, and then a supply-demand imbalance that led to a rise in home prices at an unprecedented rate. We have been unable to accurately forecast future home prices at different times in both directions by much more than we modeled as possible, with Zillow Offers unit economics swinging approximately 1,200 basis points from Q2 to an expected -500 to -700 basis points in Q4 2021.

So on one hand, management would claim that the extraordinary amount of volatility is what led to their iBuying endeavors being unprofitable. On the other hand, the massive increase in aggregate housing prices makes it mathematically likely that Zillow would somehow benefit from this upside volatility. The fact that they did not implies that they overpaid for housing inventory. The CEO would disagree that they overpaid, and stated in their shareholder letter:

Because of this price forecasting volatility, we have had to reconsider what the business might look like at a larger size. We have offered sellers a fair market price from the start of Zillow Offers, while also being clear that the business would only become consistently profitable at scale. We have determined this large scale would require too much equity capital, create too much volatility 2 | Q3 2021 in our earnings and balance sheet, and ultimately result in far lower return on equity than we imagined.

The key line of focus is the claim that “We have offered sellers a fair market price from the start of Zillow Offers”. It may be true that Zillow offered what they believed was a “fair price” however it is clear that the market did not view their price as “fair”. This is the core of the issue with iBuying: management thought they were paying a fair price, yet lost money in a roaring housing market. If they had indeed been paying a “fair” market price, by simply holding the inventory they would have been able to take advantage of a broad based rally in home prices and would have made money, or at the very least not lost money. The sheer amount of money that was lost on iBuying heavily implies that they overpaid for inventory on a broad scale. In Q3 2021 alone their iBuying segment lost over $420 million in that three month period. It is extremely unlikely that they could lose that much money in such a short period of time by paying a fair market price in a roaring housing market. We would disagree with management’s assertion that they paid a truly fair price for their housing inventory.

In many regards what happened with iBuying was the result of the problem being difficult to solve. In the end, management was unable to solve it. Many companies are faced with difficult problems and the ones that are successfully able to solve them become the leaders of tomorrow. Despite their best efforts and good intentions the iBuying business was just a problem that was too difficult for management to solve. Unfortunately this explanation isn’t enough to allay concerns of Wall Street and the stock has relentlessly sold off since they encountered issues with iBuying. After all, the managers of public companies are expected to solve difficult problems and if they are unable to do so it becomes concerning to investors. For this reason, management needs to prove themselves and show that they can return to profitably running their core business, which they were good at doing up until they entered iBuying.

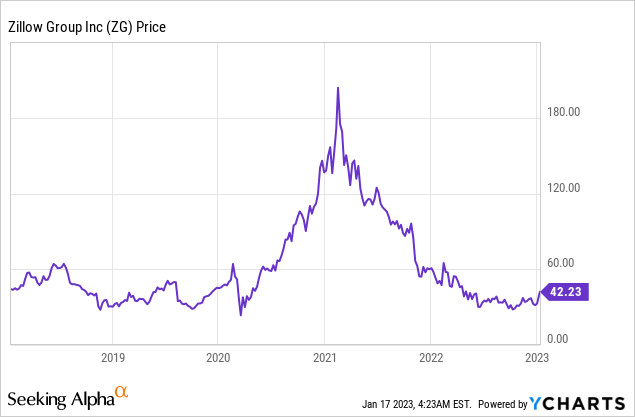

Price Action

Zillow had a stunning run up during 2020 and the beginning of 2021, before the iBuying fiasco and a challenged real estate market sunk the ship. The share price decline has resulted in Zillow trading at a much more reasonable valuation but there is too much uncertainty remaining around their business model going forward.

Valuation

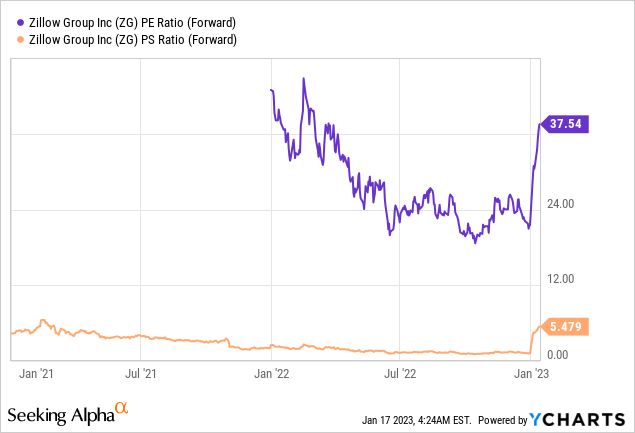

Zillow looks somewhat reasonable on a forward PE and forward PS basis (Important to note that PS was impacted by iBuying in the past). Despite the forward PE looking reasonable we believe that investors should wait on the sidelines until conditions improve in the housing market and Zillow’s management is able to get their act together.

The company trades at a PB of 2.21 and a PC of 2.92. This puts a bit of a floor on the share price and makes it difficult to rate a sell here, as Zillow could be a buyout target for private equity or another company in the real estate industry.

Risks

Zillow may be unable to profitably run their business in the future. This would indicate that their model is either broken or managed poorly. If the answer is the latter then Zillow could end up being a buyout target if management is deemed to be inefficient.

We view the risk/reward as unfavorable here.

Key Takeaway

Despite the decline in Zillow’s stock price we do not view this as a good time to buy shares. The housing market is highly challenged and Zillow’s management have made quite a few missteps in recent memory. We think it is a good idea for investors to wait on the sidelines until the housing market improves and Zillow’s management prove themselves and return the company to profitability.

Be the first to comment