Scott Olson

The Investment Thesis

Enterprise Products Partners L.P. (NYSE:EPD) is a large midstream-related company in the United States with a market cap of over $55 billion. It provides midstream energy services to a number of different producers and consumers, both related to natural gas and natural gas liquids. In the company, there are four different segments that make up the business, and they have managed to set up 19 individual facilities across the country. Besides just natural gas, the company is also involved with crude oil and petrochemicals.

With growing revenues and a healthy balance sheet, I think EPD is a very good company to add to a portfolio if you want a dividend-paying and steadily growing one. Right now, the upside seems favorable, and the downside is limited.

Last Earnings Report Highlights

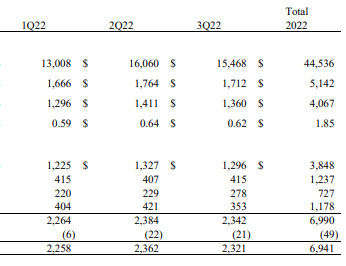

In the latest earnings report by the company, investors were greeted with impressive top-line growth. As revenues grew over 44% YoY, it seems the management has outperformed estimates and left investors satisfied in my opinion. Moving over to the bottom line, the growth was impressive but not as much as the top line. The net income saw a YoY increase of just under 18%, which meant an EPS of $0.62 was achieved for the quarter.

Revenue Statement (Q3 Earnings Report)

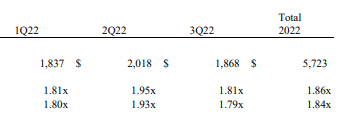

Besides the top and bottom line increasing year over year, the distributable cash flow has also steadily been moving upwards. In the last quarter, it topped out at around $1.8 billion, compared to $1.6 billion a year earlier. This is a great sign as more cash can be distributed to shareholders and your hold in the company improves in value.

Distributable Cash (Q3 Earnings Report)

Looking at the volumes the company handled in the quarter, I can see that the natural gas segment saw the largest increase. The fee-based natural gas processing improved around 30% YoY, which I think is something that greatly helped with the revenues coming in as they did. In general, natural gas transportation is what has increased heavily, and I don’t think the trend will stop any time soon, in all honesty.

All in all, I think the company had a standout quarter, and it’s great seeing the shares outstanding decreasing a little bit too, even though it’s just around 0.3%. The future seems promising for the company.

Sector Outlook

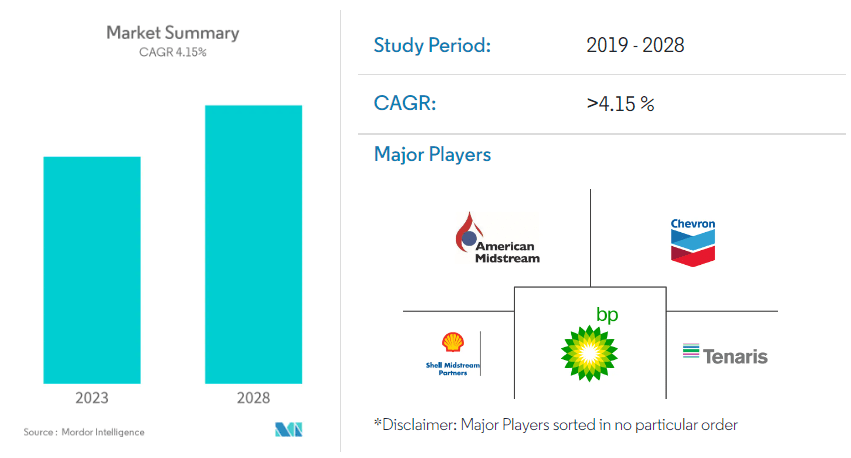

The midstream market that EPD helps supply with services does seem to have a growing future ahead of itself. Until the year 2028, the market is expected to grow around 4.15% YoY. The market remained rather resilient to the Covid-19 pandemic and the demand for the product is continuing.

Midstream Outlook (mordorintelligence)

Transportation for the commodities like crude oil and natural gas will be important to see. There are currently several projects where they are building out the transportation infrastructure. Perhaps if there are any significant delays, that could harm the revenues of companies in the sector. I am not too worried, however, as they can most likely pass down some of the costs.

Looking at the natural gas market, it has actually been shrinking since 2021. In the year 2022, the demand for it was actually expected to decline by about 0.8% worldwide, as the consequence of a 10% contraction in Europe and unchanged demand in Asia. I think there will be volatile prices ahead, as the conflict in Ukraine continues to develop.

Competitors

There are several different companies in the midstream industry, all competing for their share of the market. They all offer similar services in that they provide transportation to producers and consumers across the United States. Taking market share comes down to developing and securing new projects where they can be the sole operator.

I think that Enbridge (ENB) and Energy Transfer (ET) are some competitors to EPD that could provide a fair match. From an investment point, however, I think the edge lies with EPD as they are both expected to grow faster and also have recent proof of it too. With a very generous dividend as well. Maybe EPD doesn’t beat them on the net margin with 9.12% and ENB having 11.3%, but looking at the leveraged cash flow margin, EPD wins out by a bit. I like this metric as it normally translates into more money which can be transferred to the shareholder whilst also having some left over to expand further.

The Balance Sheet

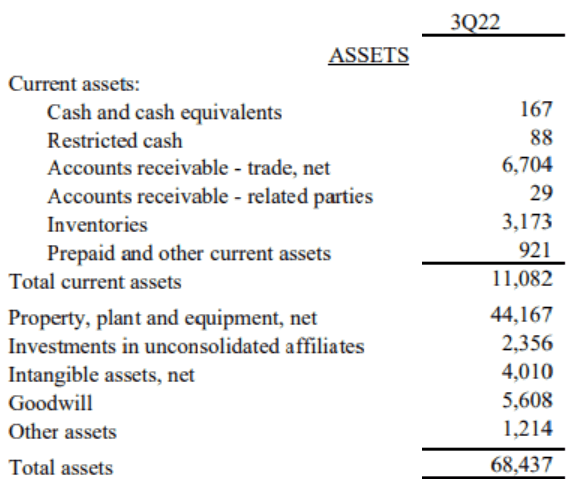

Moving over to the balance sheet, the company has seen a decrease in the cash position by quite a lot YoY. It might be a bit unfair as in Q3 2021 the company held over $2 billion, which is the highest amount in a long time. In the latest earnings report, the total amounted to around $167 million.

Current Assets (Q3 Earnings Report)

But as a positive, the long-debt has been reducing steadily and sits now around $26.5 billion instead of $28 billion a year earlier. The current debt the company needs to pay is $2.6 billion right now, which might seem worrying as the company does not hold too much cash. But I don’t expect it to become an issue as the free cash flow the company has is very high.

All in all, I am not worried that the company will see any issues with its liabilities. Currently, the ratio between assets and liabilities is 1.6 which is a healthy one in my opinion. On top of this, the company has maintained a return on assets of 7.45% in the last 12 months.

Looking ahead, I don’t think share dilution will be an issue. With such a high free cash flow right now, I believe the management will try and build out the cash position whilst distributing dividends to shareholders. There are in the last few years been some dilution, but nothing to worry about I think.

Valuing The Company

Companies in the midstream sector are perhaps known for explosive growth. Instead, investors are attracted by a large number of cash flows and steady top and bottom lines.

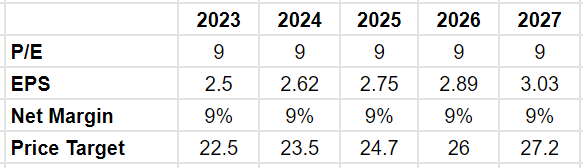

Future Estimates (Author’s Own Calculations)

I think that the future seems bright for EPD. In my estimates, I keep a terminal p/e ratio of 9, which I do to just have a little bit more conservative valuations. I think it helps reduce some of the downside risks, and any potential upside is just a welcomed gesture instead. The p/e is also a little bit higher than the sector average of 8, which I think is justifiable as the company has very high cash flow and manageable debt whilst continuing to grow a bit.

I think that during these 5 years, the bottom line will increase about 5% YoY, slightly higher than what the market expects for the industry. As the company is well established I don’t expect the margins to be volatile, instead, I think they will sit comfortably around 9%.

Share Price (Seeking Alpha)

I should mention that I am not including the dividend in these calculations. From the current share price, the return would only be about 7%. But if you add on an annual dividend rate of 6-7% the investment case becomes a lot more clear. For an investor looking for a stable company with a good dividend, I think EPD is a great choice, and the current price offers little downside.

Conclusion

Enterprise Products Partners L.P. is a massive company with a market cap of over $55 billion. Operating in the midstream industry, the company has steady outlooks of growth as markets expect a 4.15% YoY increase until 2028.

Revenues have been increasing impressively in the latest quarter as the company continues to pass value to shareholders through both dividends and small share buybacks.

Right now, the company doesn’t offer too much value if you can’t include the dividend. But as I believe in the management’s ability to generate large amounts of cash flows, I think the downside is limited and the upside promising. If you are looking for a stable dividend-paying company in the midstream sector, I think EPD is at a great entry price, and therefore, I have a buy for them.

Be the first to comment