Eloi_Omella/E+ via Getty Images

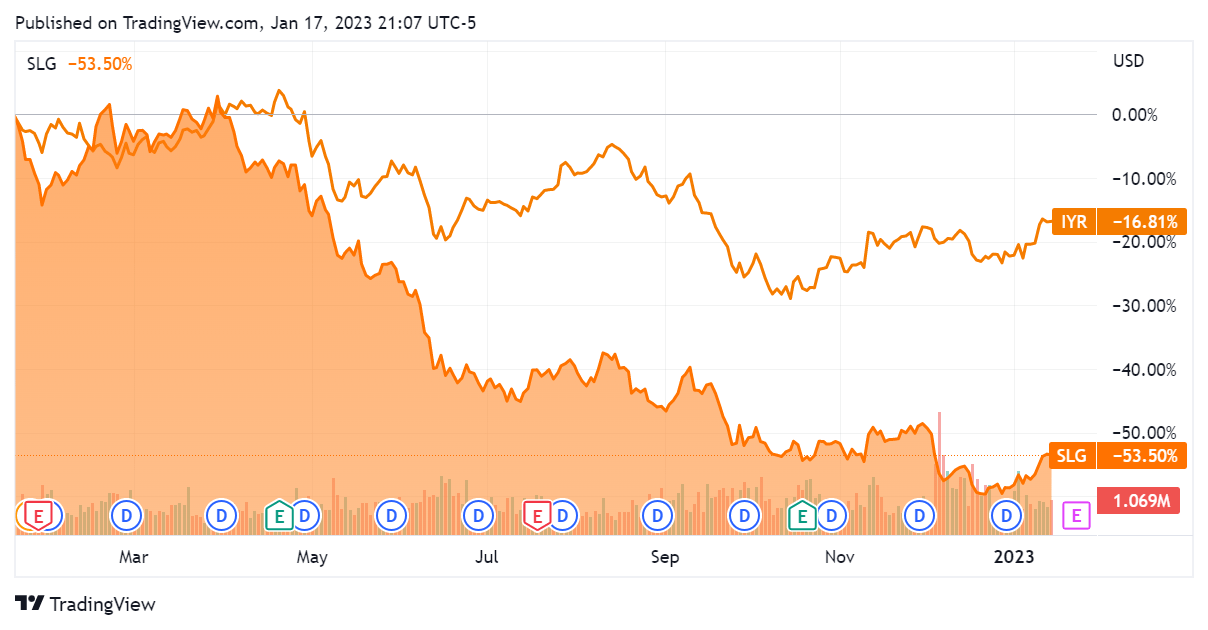

SL Green (NYSE:SLG) stock has fallen hard over the past year and is down over 50%, performing much worse than the iShares U.S. Real Estate ETF (IYR), which was down almost 17% over the same time period. This can be attributed to SLG principally owning and operating offices in Manhattan, a sector and location that work-from-home dynamics have had an outsized impact in. The stock price is down to levels not seen since September 2009, and based on management’s latest guidance for 2023, forward P/FFO is about 7. The shares undoubtedly appear cheap, but there is good reason for that. In this article, we will explore the state of the Manhattan office rental market then have a look at company specific factors.

Seeking Alpha

The Manhattan Office Rental Market

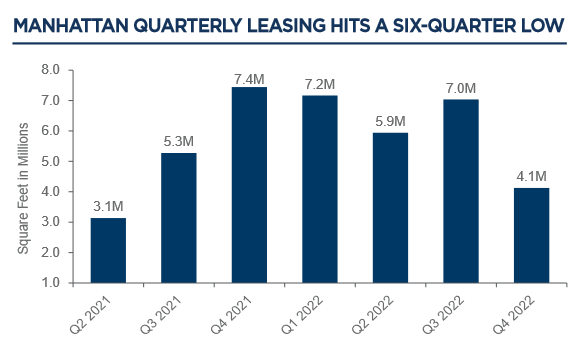

The office rental market in Manhattan faced another difficult year in 2022 as the work-from-home trend persisted. Leasing activity hit a six quarter low as the pace of leasing slowed, with November and December being the least active months of the year. The chart below shows the square footage of office space being transacted for the past 7 quarters. There is a significant dip in leasing activity in Q4 2022 compared to the most recent quarters.

Cushman & Wakefield

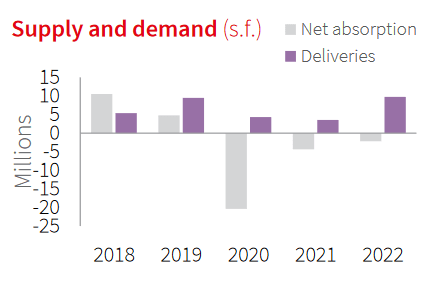

At the same time, supply increased as new properties came online. Demand has not kept up with the new supply, resulting in negative net absorption. The chart below shows the deliveries of new office space and the net absorption by year. Net absorption is the space that has become physically occupied less the space that became vacant. Negative absorption means that more space is becoming vacant that is being occupied.

JLL

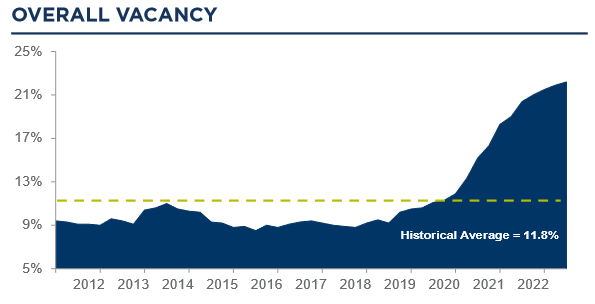

Low leasing activity and a high supply of space have resulted in the vacancy rate hitting an all-time high, around 18-22% depending on which report you are reading. The chart below from the Cushman & Wakefield Q4 2022 report shows a 22.2% vacancy rate, a rate that has increased steadily over the past few years.

Cushman & Wakefield

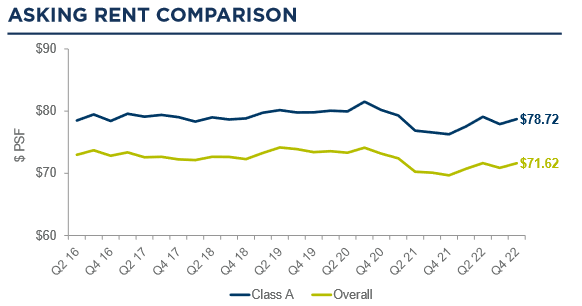

Asking rent surprisingly ticked up in Q4 2022, but is still lower than pre-COVID levels as shown in the chart below. The rise in Q4 rents is attributable to the completion of new buildings that can demand higher rates. If leasing rates remain slow and vacancy levels remain elevated, we would expect asking rent to drop to attract tenants.

Cushman & Wakefield

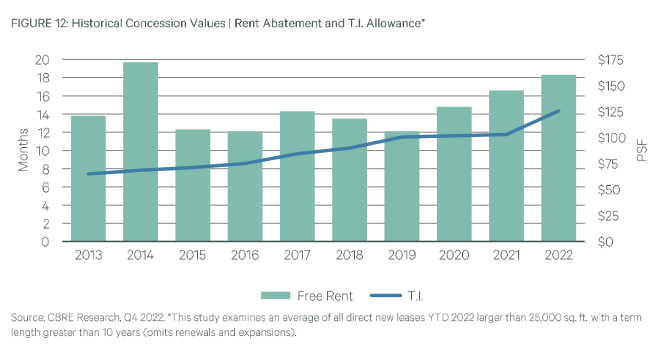

Concessions, including both rent abatement and tenant improvement allowance, have increased in 2022 as shown in the chart below. Similar to asking rents, we expect this to be further impacted if leasing activity remains slow and vacancy rates high.

CBRE

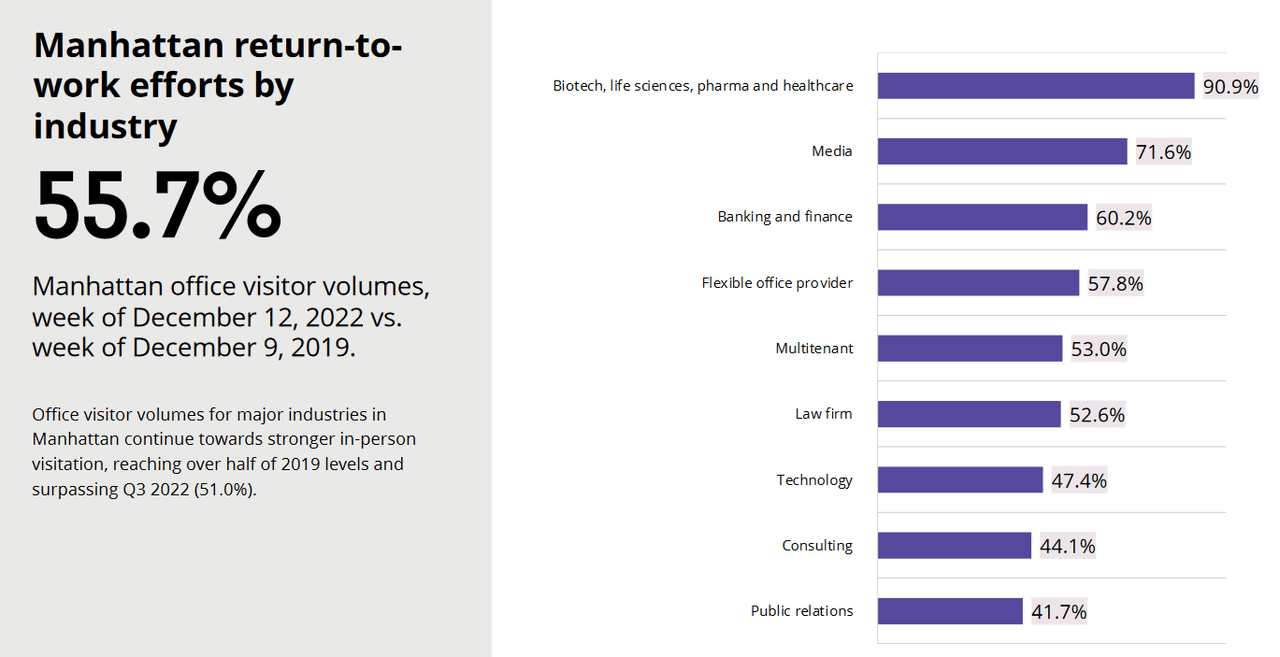

On return-to-work, in-person visitation hit 55.7% of 2019 levels in December 2022. This has improved from 51.0% in Q3 2022 and 45.1% in December 2021, but visitation is still at a much lower level than pre-COVID. By industry, technology, consulting and public relations are bringing down the return-to-work average as shown below.

Avison Young

Overall, the office rental market in Manhattan is weak and appears to be getting weaker as leasing activity slows and the vacancy rate continues to climb. We expect this to have a negative impact on rent rates and on concessions offered to tenants. Now that we have a sense of the office market in Manhattan, let’s have a look at SLG specific factors.

Dividend Cut and Lower Management Guidance

On December 5, 2022, SLG cut the dividend by 12.9% to $3.25 per share, which works out to about 8.5% at the current price. The reason stated by management for the cut was:

“We endeavor to provide our shareholders with a meaningful, sustainable ordinary dividend that has a correlation to operating cash flow while furthering our initiative to maintain substantial liquidity and repay debt amid the backdrop of a rising rate environment. We have reduced the dividend to match our current projection of Funds Available for Distribution (“FAD”) for 2023, which allows us to strike this balance as we continue to provide a yield on our common stock of approximately 8.0%, based on the current share price, while projecting an increase in liquidity to nearly $1.6 billion and a reduction of combined debt by almost $2.4 billion during 2023″.

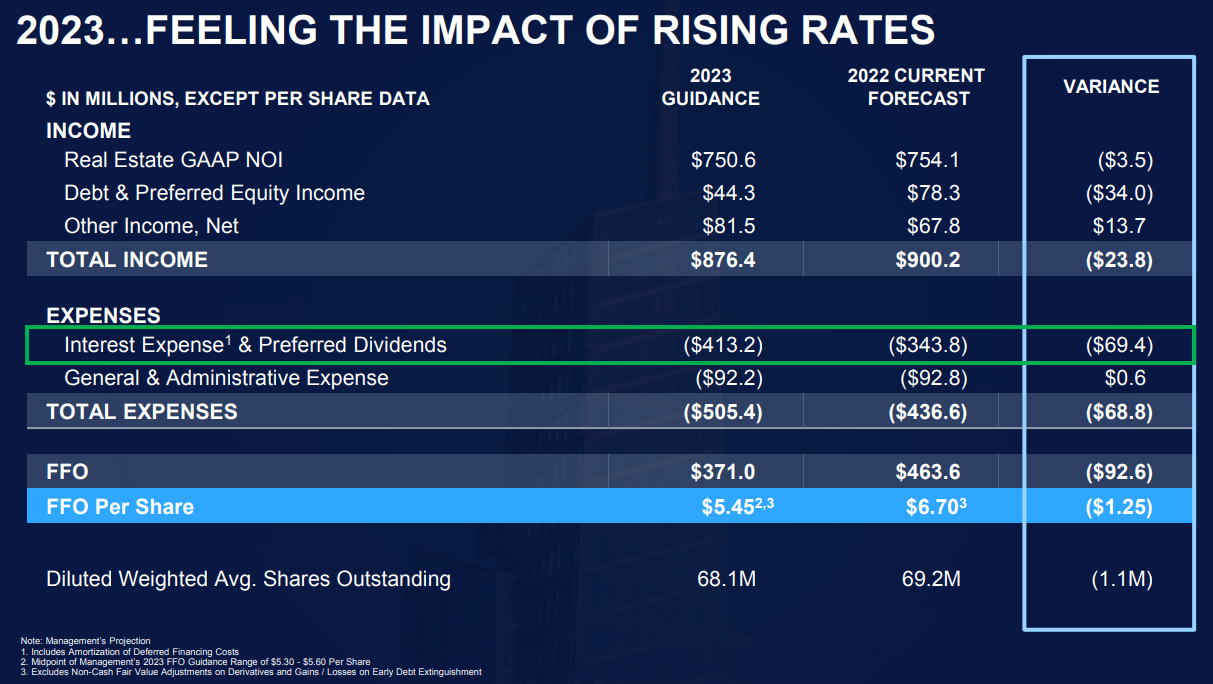

Management was signaling that FFO will drop in 2023 and that reducing debt needs to be prioritized as debt service becomes a bigger challenge. This was confirmed at their investor day presentation on the same day as the cut. The slide below from the presentation shows that interest expenses and preferred dividends are expected to be $69.4 million higher in 2023 (20.2% increase) and FFO will decrease by $92.6 million to $5.45 per share in 2023 from a forecasted $6.70 per share in 2022 (18.6% decrease).

SL Green

That is a significant drop in FFO, mainly from higher interest costs as rates have increased. What we don’t see in the management guidance is a notable impact to the top line from lower rents and higher concessions offered to tenants on new leases, both of which are likely scenarios if the high vacancy rates in Manhattan persist. If rents decrease and more concessions are offered in the form of longer free rent periods or higher tenant improvement allowances, FFO could come down further and SLG’s valuation would become less attractive.

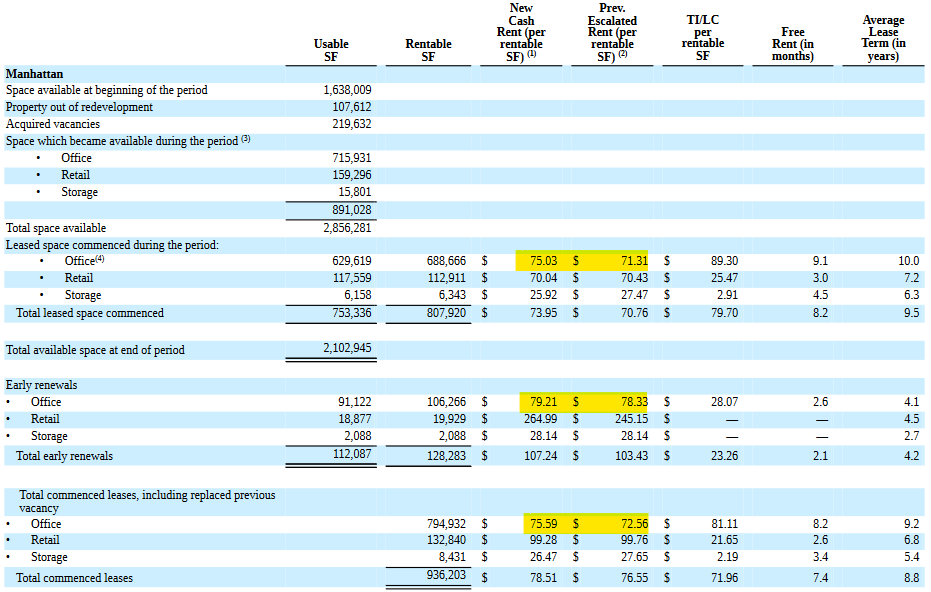

The impact to the topline hasn’t manifested yet for SLG. For year to date Q3 2022, SL Green was still able to increase office rents for new leases and early renewals as shown in the table below. Overall, office rents increased from $72.56 to $75.59 per square foot for new leases during the year. Considering the current market dynamics in Manhattan, SLG has done well with their rental rates on new leases. Management also deserves credit for maintaining an occupancy rate above 90%, which is much stronger than the overall market in Manhattan with a vacancy rate above 18%.

SL Green

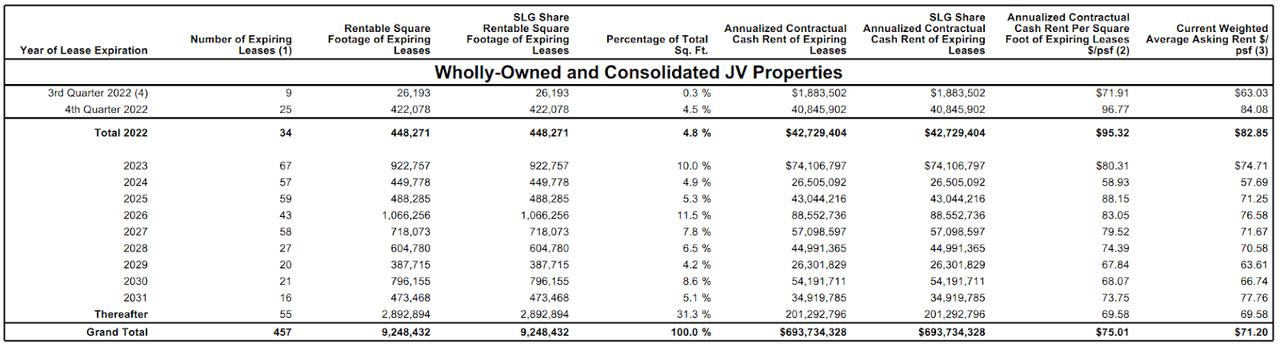

The chart below shows the lease expiration schedule for SL Green, which shows 4.5% of leases expiring in Q4 2022 and 10% of leases expiring in 2023. It will be worth watching whether SLG can keep rent rates higher on these renewals.

SL Green

In conclusion, SL Green has done well in 2022 considering the overall market conditions for Manhattan office rentals. However, management has cut the dividend and has lowered FFO guidance in 2023 due to higher interest costs. In addition, as vacancy rates hit an all-time high and leasing activity slows in Manhattan, we see further risk of FFO not meeting targets. Although a lot of risk is priced into the shares, we are not buyers yet and will wait for more evidence of a recovery.

Be the first to comment