hapabapa

Zillow (NASDAQ:Z) is the number one online real estate portal in the U.S.A. The company has approximately 234 million monthly unique visitors, which equates to approximately 70% of the U.S population. In addition, the word “Zillow” is searched on Google more times than the word “Real Estate”, which is a testament to the company’s strong brand.

Zillow and Real Estate (Google Trends)

Zillow is currently going through a huge business model transition, as it refocuses on its core online platform, after an embarrassing disaster with iBuying. I personally would have written off most other companies at this point, but I think Zillow’s market-leading position and experienced management make a turnaround possible. Zillow’s founder and CEO is Rich Barton, the founder of Expedia and Glassdoor, and he is a true technology veteran. The company has had a strong start to its turnaround as it beat both top and bottom-line analyst growth estimates in Q3,22. In this post I’m going to breakdown its business model, financials, and valuation, let’s dive in.

Business Model Transition

As I reported in prior posts on Zillow, the company is winding down its home-buying business, after it failed to forecast home prices using its models. In the words of CEO Rich Barton, “we swung for the fences and missed”. Overall I believe the exit from home buying is a positive sign, as the company can now focus on its core technology business, which it has competence. Moving forward, management has laid out a new strategy that aims to increase their share of customer transactions from 3% to 6% by 2025. Its strategy to accomplish this focuses around five “growth pillars” which include; touring, financing, seller solutions, enhancing its partner network, and integrating services.

Zillow Business Model (Zillow)

In touring, Zillow has previously acquired the ShowingTime platform which enables customers to see availability for viewings in real-time, without the need to ring up a realtor. The goal of this platform is to reduce the friction between viewing a home online and in person, which is ultimately expected to drive a greater number of bookings. So far the company has seen leading indicators that the platform has increased the intent to buy of a home buyer. Zillow is now focusing on increasing its “successful tour rate” which is expected to convert transactions at around three times the rate of other Zillow actions.

Zillow has also recently (in December) acquired Real Estate media firm VRX media which provides 3D tours, virtual staging, and professional photography. This acquisition acts as the background for two new 2023 product releases inside ShowingTime+, which include Listing Media Services and Listing Showcase. This is a solid acquisition in my eyes, as it further enables Zillow to capture value in the real estate buying process.

On the partnership side, Zillow previously scored a partnership with former rival Opendoor (OPEN). This enables the company to still capture requests to buy from homeowners and just take a commission for the referral to Opendoor. Zillow still has a long way to go on its way to creating a “housing super app” but so far the progress has been solid.

Mixed Financials

Zillow reported mixed financial results for the third quarter of 2022. Revenue was $483 million, which declined by 12.18% year over year, despite beating analyst estimates by $24.89 million. The decline was mainly driven by an unfavorable comparison as the home-buying business was fully exited in September 2023. Breaking revenue down by segment, its IMT [Internet, Media and Technology] revenue was $457 million and declined by 5% year over year, despite being above management’s outlook. Mortgage revenue declined by an eye-watering 63% year over year to $26 million. This decline was driven by the macroeconomic environment of which rising interest rates have caused a depressed housing market, as mortgage rates are now higher.

Revenue (Q3,22 report)

Premier Agent revenue also declined by 13% year over year to $312 million. In addition, Zillow has noted that many homeowners are deciding to delay selling their properties at lower expected prices, thus this has resulted in “tight inventory”. A positive is Zillow has reported better than forecasted conversion and retention rates among its customers.

The rental market was buoyant, as rental revenue increased by 10% year over year to $74 million, which beat management’s expectations. Purchase loan origination volume also increased by 24% over the prior quarter (Q2,22).

Product Improvements

I mentioned a few of the product improvements earlier as the company aims to capture a greater number of property transactions, here are a few more. Zillow has consolidated its partners to enable more scalable testing. For example, the company has managed to gain a 15% adoption rate of Zillow Home Loans in Raleigh, North Carolina. This acts as a solid data point for improvements in other parts of the U.S. Zillow has started to build out a “direct to consumer” purchase mortgage operation. The goal of this service will be to integrate mortgages directly into the customer experience. Zillow’s management believes there’s an opportunity to capture value from the fragmented mortgage market, as the top 25 lenders only have about one-third of market share. Zillow reports ~67% of actual home buyers use Zillow and around 40% of all homebuyers start their journey with financing. Even prior to much investment, Zillow reports that “millions of prospective” Zillow Home loans customers asked for financing help of which Zillow sends these “leads” to third parties. This existing process acts as demand verification for Zillow to capture a greater amount of economic value in the future.

To increase the number of home loan customers, Zillow aims to educate its website visitors on its mortgage offering, as management believes many are not aware of the service. Once aware, Zillow aims to filter the website visitors with the “highest intent” to its “loan officers” which can then help customers with mortgages. This will be a challenge as if too many customers who are years away from getting a loan speak to loan officers, it will waste both people’s time and result in higher costs. Zillow aims to bolster its home loans offering through education to its Premier Agent partner, which can then recommend Zillow Home loans as their mortgage provider. The result of this will bring Zillow one step closer to its “Super App” and capture a greater amount of the value chain.

Zillow Super App (Zillow)

Profitability and Margins

Zillow reported earnings per share [EPS] of negative $0.22, which beat analyst expectations by $0.04, despite declining by a substantial 82.95%. The majority of this decline was driven by an unfavorable comparison with the prior home buying business. A positive is the company reported consolidated Adjusted EBITDA of $130 million, which exceeded management’s expectations. This metric made up 27% of revenue, which was down only 1% year over year. Higher than anticipated margins in the IMT segment helped to drive solid results. Management also reported lower than expected advertising costs and increasing operational efficiencies.

Earnings Zillow (Q3,22 report)

Zillow has a strong balance sheet with $3.5 billion of cash and investments. The company does have $1.875 billion in total debt, but the majority of this, $1.659 billion, is long-term debt. The company spent $176 million on share buybacks which shows confidence in the new strategy and current stock valuation.

Moving forward into Q4,22, management has forecasted a 19% decline in its IMT revenue at the midpoint of its outlook. In addition, the company is expecting Premier Agent revenue to be between $250 million and $270 million, which would represent a decline of 27% year over year. These results are expected to be driven by the deteriorating macroeconomic environment, in relation to the housing market. Analyzing the mortgage purchase application [MBA] index and multiplying this by the average purchase loan amount, we get a leading indicator of total transaction dollar volume growth. At the end of the third quarter, Zillow reported this metric has declined by an eye-watering 40% year over year. The rental market still looks to be solid and lower rental vacancies are expected to drive increased rental advertising in Q4.

Advanced Valuation

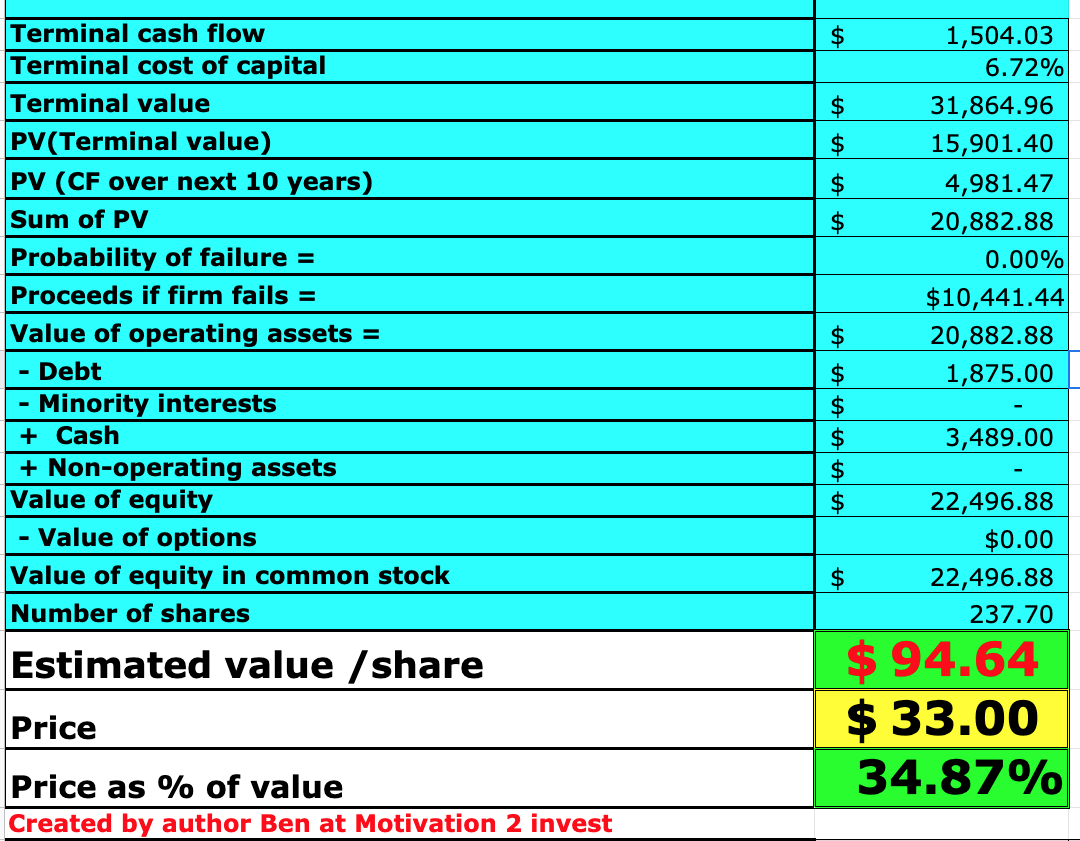

Valuing Zillow is fairly challenging given its transitioning business model and housing market headwinds. However, I have plugged its most recent financial data into my advanced valuation model, which uses the discounted cash flow valuation method. I have forecasted negative 20% revenue growth for next year, driven by the harsh macroeconomic environment for housing. However, in years 2 to 5, I have forecasted revenue to increase by 10% per year, as economic conditions improve.

Zillow stock valuation 1 (created by author Ben at Motivation 2 Invest)

To increase the accuracy of the valuation model, I have capitalized R&D expenses which has lifted net income. In addition, I have forecasted a pre-tax operating margin of 23% over the next 8 years. I forecast this to be driven by Zillow’s strategy to increase the percentage of customer home-buying transactions.

Zillow stock valuation 2 (created by author Ben at Motivation 2 Invest)

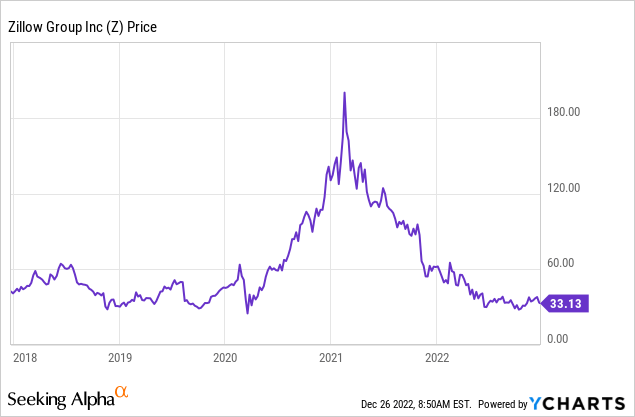

Given these factors I get a fair value of ~$95 per share, the stock is trading at $33 per share at the time of writing and thus is ~65% undervalued.

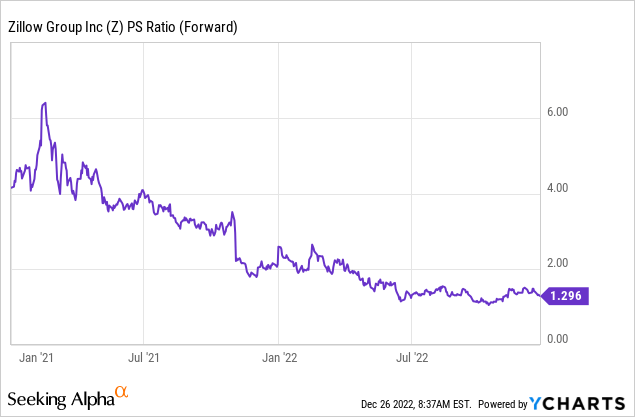

As an extra datapoint, Zillow trades at a P/S ratio = 0.98, which is 79% cheaper than its 5 year average.

Risks

Tepid Housing Market

As mentioned prior, the rising interest rate environment increases mortgage rates and debt servicing costs, which can cause a slowdown in the housing market. This will likely impact Zillow massively in the short term as transactions slow and customers stay at their current property.

Final Thoughts

Zillow is the king of the U.S. real estate market and is currently going through a major transition period. In the short term, I expect further challenges especially given the macroeconomic environment. However, CEO Rich Barton is one of the best people around to execute Zillow’s new online strategy. Capturing a greater portion of real estate transaction value makes complete sense and looks to be achievable given Zillow’s dominant market position. Zillow stock is undervalued intrinsically and thus could be a great long-term investment.

Be the first to comment